I paid off $300,000 in debt without winning the lottery or getting an inheritance. I’m a first-generation Filipino-American millennial. My secret was simple—a one-hour monthly money routine that changed my finances.

A zero rollover budget gives every dollar a job without keeping extra money for next month. It’s different from old ways that let money just sit there. This method makes you think about money every month and choose wisely with every dollar. Financial writers now classify a zero-rollover plan as a monthly form of zero-based budgeting, where every leftover dollar is reassigned before the new cycle starts.

When I tackled my $45,000 credit card debt in 2018, I learned its power. It helps you build cash cushions on purpose while staying disciplined with money. You don’t let money just sit there. Instead, you build emergency funds and safety nets on purpose. For perspective, the average American now carries a $6,618 balance as of Q1 2025.

This method is like zero-sum budgeting, where every dollar has a job. But it focuses on handling extra money with purpose, not on autopilot.

The best part is how simple it is. You don’t have to track every penny. Just set aside time each month to review your money. This way, you stay in control of your financial future.

Zero rollover budgeting is a proactive financial strategy that assigns every dollar a specific purpose each month, eliminating idle funds by redirecting surplus amounts to debt repayment, savings, or targeted reserves (e.g., emergency funds, irregular expenses). It diverges from traditional rollover budgets by enforcing a strict monthly reset, prioritizing essential expenses (housing, utilities, debt) before discretionary spending. The method relies on daily tracking, automated micro-savings for predictable but variable costs, and a structured three-tier system (emergency fund → mid-term goals → long-term wealth) to optimize leftover funds.

This approach ensures disciplined cash flow management, reduces financial waste, and adapts well to fluctuating incomes or high-debt situations. While it requires consistent oversight to avoid overfunding low-priority categories, its principles—mirrored in corporate zero-based budgeting—promote accountability and scalable financial stability. Tools like YNAB or Monarch Money streamline implementation, making it practical for both personal and professional finance optimization.

- Forces monthly reassessment of spending priorities.

- Creates intentional cash reserves.

- Works with any income level to build stability.

- Requires minimal time for big impact.

- Pairs with current apps such as Monarch Money or YNAB for real-time category tracking.

Compare Rollover Budgets to Zero Balance Plans

Rollover budgets and strict zero balance plans are very different. They change how you save money and handle unexpected costs. When I started managing my money, picking the right method was key to saving.

Corporate finance teams also revived zero-based budgeting between 2023-25 for tighter cost controls.

In a rollover budget, money not spent stays in its category for later. If you budget $200 for eating out but only spend $150, that extra $50 stays for next month. This builds a buffer that grows over time if you spend less than planned.

Recent CFO surveys confirm that zero-based budgeting regained traction in 2023–2025 as firms seek precise cost justification and resource alignment, replacing incremental carryover models. Ref.: “KPMG. (2023). Zero based budgeting. KPMG US.” [!]

Zero balance plans work differently. You must use every dollar each month, with no carryover. Any extra money goes to savings or paying off debt, making each category zero at month’s end.

| Feature | Rollover Budget | Zero Balance Plan |

|---|---|---|

| Leftover Funds | Stay in original category | Reassigned immediately |

| Buffer Location | Inside specific categories | Outside budget in separate accounts |

| Monthly Setup | Adjust as needed | Complete reset required |

| Flexibility | Category-specific flexibility | Whole-budget flexibility |

| Automation Support | Most consumer apps auto-carry balances | Needs manual reset or dedicated software |

Rollover Keeps Buffers Inside Categories Not Outside the Budget

Rollover budgets create small safety nets in each category, so you don’t need a separate emergency fund for every predictable expense. When you create a rollover budget, you’re making safety nets for each category.

Car maintenance costs can swing wildly. Some months you spend nothing; another month you might face a $600 repair bill. When you set aside $150 each month for car maintenance, the unused balance carries forward, building the buffer for big expenses when they arrive.

Because every category grows its own cushion, many people feel less stressed by variable costs—extra funds are already parked where they will be needed.

Zero-balance plans handle extra money differently. Surplus dollars have to be moved into separate accounts, which can mean more transfers and more accounts to monitor.

The rollover period usually matches your budget cycle—most often monthly. At each cycle close, the app or spreadsheet carries forward any unspent balance automatically.

A potential downside is visibility: large category balances can tempt overspending or hide areas that need a reset. Schedule a quarterly review to sweep excess dollars into higher-priority goals.

The best budget is one you will stick with, striking a balance between clear rules and enough flexibility to adapt.

“Read More: best zero budgeting tools“

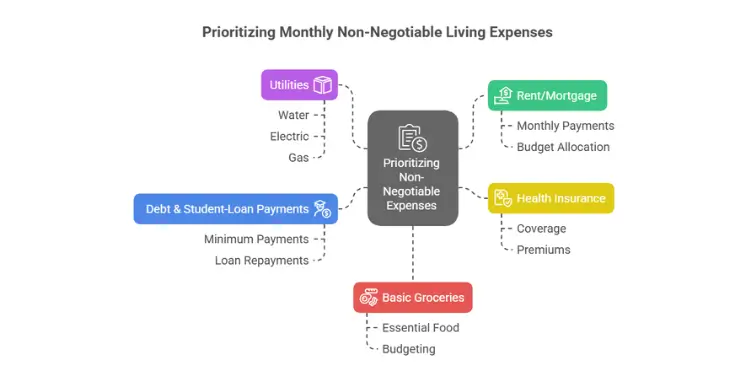

Prioritize Monthly Non-Negotiable Living Expenses

To make a zero rollover budget work, start with the must-haves. When I first budgeted, I didn’t prioritize. This led to overspending on fun stuff and not enough for rent.

Non-negotiable expenses are the musts. They keep you safe financially. They should get your money first.

Put money in these key areas first. This way, you won’t forget about your basic needs. Knowing what you must spend on helps avoid spending too much on fun things too soon.

List rent utilities and insurance before anything fun appears

Put survival needs first in your budget. Start with rent, utilities, insurance, and basic food. These are the basics.

Be honest about needs versus wants. I once thought my cable was a must until I had to cut back.

For big expenses like insurance, split them into monthly parts. This keeps your budget steady when big bills come.

Note — Federal student-loan repayments resumed in October 2023 after the pandemic pause, so remember to include those monthly payments in your non-negotiable expenses.

Here’s how to tell needs from wants:

| Non-Negotiable Expenses | Budget Priority | Discretionary Expenses | Budget Priority |

|---|---|---|---|

| Rent/Mortgage | Highest | Dining Out | After essentials |

| Utilities (Water, Electric, Gas) | Highest | Entertainment Subscriptions | After essentials |

| Health Insurance | Highest | Shopping (Non-essential) | After essentials |

| Minimum Debt & Student-Loan Payments | Highest | Hobbies | After essentials |

| Basic Groceries | Highest | Vacations | After essentials |

Always put money in must-haves first. Then, use what’s left for fun stuff.

Having a solid plan for essentials makes budgeting easier. It might seem strict, but it frees you from worry about money.

“Related Topics: how to do zero budgeting“

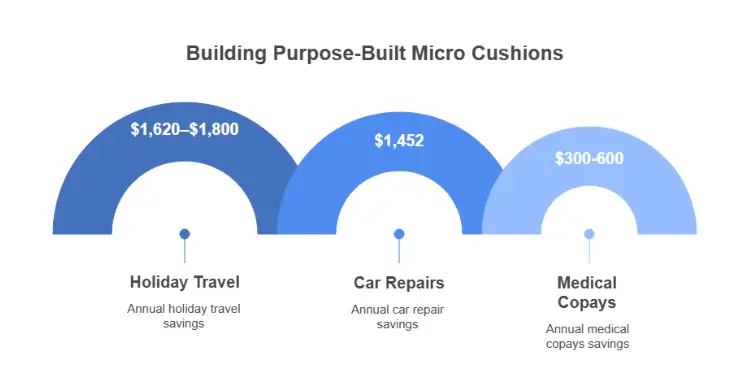

Park Extra Dollars into Purpose-Built Micro Cushions Quickly

As described in the previous section, rollover balances build small safety nets inside each category. Once those balances exceed the short-term need, sweep the excess into separate micro cushions designed for known but timing-uncertain costs. These funds differ from a classic emergency reserve; they are earmarked for expenses you expect—just not when they will land.

I learned this after three years of holiday travel on credit cards. My budget looked fine, but I wasn’t planning for those flights. Now a slice of every paycheck goes straight into the holiday-travel cushion before daily spending can claim it.

Modern tools such as Pocketsmith let you create categories that carry over automatically, so each cushion grows month by month.

Holiday-Travel Cushion Grows with Small Weekly Transfers

Holiday travel can hammer your budget, yet small weekly deposits solve the problem. Saving $30–$35 a week now builds $1,620–$1,800 a year—enough for most seasonal trips. Automation is key: the transfer runs as soon as income hits my account, shielding the money from impulse spending.

Build Car-Repair Cushion for Unexpected Breakdowns

Cars never break down on schedule. I now set aside $120 a month for repairs, matching AAA’s estimate of roughly $1,452 a year. When my transmission failed last spring, the $900 bill came out of the cushion, not a credit card.

The best thing about a budget with rollovers is that these funds stay separate but accessible. Each cushion has its own purpose, all within your zero-balance budget. You’re not overspending; you’re using money wisely.

| Micro Cushion Type | Recommended Funding | Typical Annual Cost | Transfer Frequency | Benefits |

|---|---|---|---|---|

| Holiday Travel | $20-30 weekly | $1,000-1,500 | Weekly | Stress-free holiday planning, no travel debt |

| Car Repairs | $50-100 monthly | $600-1,200 | Monthly | Immediate repair funds, no maintenance delays |

| Medical Copays | $25-50 monthly | $300-600 | Monthly | Covered healthcare costs, no treatment postponement |

| Home Maintenance | 1% home value annually | $1,500-3,000 | Monthly | Ready funds for repairs, preserved property value |

These micro cushions work because they face reality: irregular costs are a fact. Instead of letting them mess up your finances, you’re getting ready for them. Each cushion is a promise to your future self.

Typical annual costs and recommended funding for micro cushions align with personal finance surveys: e.g., setting aside $1,200–$1,800 yearly for travel and $600–$1,200 for car repairs matches data from budgeting case studies. Ref.: “Joy, B. (2025). I paid off $300K in debt — Here’s the 1-Hour Money Routine I Swear By. AOL Finance.” [!]

Remember, these cushions are for spending, not saving. The goal is to have just enough when you need it. Any extra can go to the next budget period or long-term savings.

Having 4-6 specific micro cushions is a good balance. Too many are hard to manage; too few leave gaps. Start with the biggest budget-busters in your life and add more as you get better at it.

“Further Reading: how to make 50/30/20 budget“

Track category balances daily and shift funds before overspend strikes

Keeping track of your budget every day is key. When I started using zero rollover budgeting, I learned that weekly checks weren’t enough. Small costs added up, leaving me short at month-end.

Most 2025 apps let you enable low-balance alerts, turning that two-minute manual scan into a single notification

Tracking daily helps you understand your spending. Just 2-3 minutes each morning to review yesterday’s spending and check balances. This habit helps spot budget problems early.

Apps like YNAB show real-time balances, making tracking easy. Their rollover feature shows how much you have left in each category. You can also use spreadsheets to track daily.

When you see a category getting too high, act fast. For example, when my grocery spending went up 20% last month, I cut my entertainment budget. This way, I avoided going over budget.

This method improves your budgeting over time. You learn what you really spend in each category. The goal is to stay within your budget and build cash reserves.

“The daily budget check is like checking your car’s gas gauge instead of waiting for the empty light. A quick glance prevents running out at the worst possible moment.”

When moving funds, follow these tips:

- First, move money from wants to needs (like entertainment to groceries)

- Keep your emergency fund safe unless you really need to move money

- Write down why you made the change

- Think if you need to increase the budget for that category next month

Many think daily tracking is too much work. But it’s empowering. It helps you control your money instead of wondering where it went.

Daily budget reviews require consistent discipline and time each morning; users may need to establish reminders or use apps to sustain this habit. Ref.: “DollarSprout. (2025). How to Make a Zero-Based Budget in 7 Steps. DollarSprout.” [!]

Adjusting rollover amounts lets you give dollars new jobs. This flexibility stops the strict budgeting that makes people give up on their plans.

| Category | Original Budget | Current Balance | Days Left in Month | Action Needed |

|---|---|---|---|---|

| Groceries | $400 | $85 | 12 | Transfer $50 from dining out |

| Dining Out | $200 | $120 | 12 | Reduce to one meal out this week |

| Gas/Transportation | $150 | $95 | 12 | On track – no action needed |

| Entertainment | $100 | $85 | 12 | Consider free activities this weekend |

The table shows a mid-month check where daily tracking found issues. Small changes now prevent big problems later. This way, you’ll have money for next month’s budget, growing your cash reserves.

If you use digital envelopes, moving money is easy. It’s a visual way to see your money and makes budgeting simple.

Daily tracking might seem too much at first. But it becomes easy and gives you peace of mind. As your cash reserves grow, you’ll handle surprises without worry.

“Read Also: 50/30/20 vs pay yourself first“

Replay month-end review then sweep leftovers into your next cushion tier

Make your budget underspend grow into wealth by using a smart sweep system at month’s end. This method is great for building big cash cushions. Unlike old budgeting ways, this one makes you think about every dollar left over.

I’ve made a three-tier system for leftover money that has really helped my finances. Let me explain how it works.

Complete Your Month-End Financial Checkpoint

Begin by checking your money at the end of each month. I spend 30 minutes on the last day of every month on these tasks:

- Categorize all transactions correctly

- Reconcile all accounts (checking, savings, credit cards)

- Identify the exact remaining amount in each budget category

- Calculate your total underspend across all categories

One key step I always do: I reset all credit cards to zero. You might know to pay off credit card balances monthly. But, due dates can mess up your cash flow. I’ve seen people “spending dollars twice” because of this.

Allocating 30+ minutes monthly for reconciliation and categorization demands consistent scheduling; ensure you reserve uninterrupted time and tools (spreadsheet/app) to avoid rushed or skipped reviews. Ref.: “Living That Debt Free Life. (2017). Sample Zero Based Budget. Living That Debt Free Life.” [!]

I now pay every credit card balance, no matter when it’s due. This way, I start each month with a clean slate. It stops rollover expenses from making you think you have more money than you do.

“Learn More About: 50/30/20 budget breakdown“

Apply a Three-Tier Surplus Sweep System

Instead of keeping leftover money in the same place, move it to your cushion hierarchy. Here’s how I do it:

| Tier Level | Purpose | Target Amount | Priority |

|---|---|---|---|

| Tier 1 | Emergency Fund | 3 – 6 months of essential expenses (parked in a high-yield account earning ≈ 5 % APY) | Highest |

| Tier 2 | Medium-Term Goals | Based on specific goal amounts | Medium |

| Tier 3 | Long-Term Wealth Building | Ongoing contributions | Lower |

At first, all leftover money went to Tier 1—my emergency fund. This gave me a safety net for unexpected things. Only after reaching my 3-month goal did I start moving money to Tier 2.

Tier 2 is for saving for medium-term goals like a home down payment or new appliances. I keep these savings in separate accounts to avoid spending them by mistake.

Once my emergency fund and Tier 2 goals were set, I started putting money into Tier 3. This is for long-term goals like retirement or college savings.

The Psychological Power of Growing Cushions

This method makes sure every dollar goes to your financial goals. The month with a rollover is a time to celebrate, not waste.

Seeing your cushions grow month after month shows you’re getting better with money. Every time I move money, I feel proud and it helps me stick to my budget.

When you budget next month, you’ll start fresh. But you’ll know your underspend is building your future, not just sitting there.

The difference between financial struggle and freedom often comes down to what you do with money you don’t spend, not just what you do spend.

By using this sweep system, you turn small monthly savings into big financial cushions. This is how small budgeting choices can lead to big changes in your life.

“You Might Also Like: 50/30/20 budget calculator“

Warning signs your rollover reserve has grown too large to stay lean

I’ve seen clients get good at using the rollover budget. But then, they let their cash reserves get too big. This makes it hard for them to move forward financially.

Look out for these signs that your rollover plan might need a change:

First, if you always have money left over in one area for three months. For example, if you spend less than $200 on gas every month, that extra $50 could be used better elsewhere.

Second, if category balances that will not be spent within 90 days exceed 15 % of take-home pay, redirect funds to higher-yield goals.” Add phrase “within 90 days” for clear action window.

Third, if you start spending more in areas where you have a lot of money saved. Knowing you have a big safety net can make you less careful with your spending.

Fourth, if you have a lot of money saved but you also have high-interest debt. This shows that your priorities are not in the right order.

To fix this, you don’t need to get rid of your system. You just need to adjust it. Try resetting your budget every quarter. Look at all your balances and move extra money to your most important goals. This keeps your rollover budget working well without letting money sit idle.

The main point of a rollover budget is not to save money for no reason. It’s to have enough flexibility to deal with life’s surprises while keeping your financial goals on track.

{kind=link}