A recent study found that 65% of Americans can’t recall how much they spent last month. I found out the hard way when my money was all over the place. It wasn’t that I didn’t make enough money. It was how I managed it.

Two budget methods really stand out. The 50/30/20 rule gives clear spending limits. The “pay yourself first” method puts saving before spending.

Both methods aim to help you save money without watching every penny. The main difference is how they tackle the challenge. One uses strict rules, the other focuses on what’s most important.

In this guide, we’ll look at these two money management plans. You’ll learn which one fits your life, goals, and money habits best. No need for a degree in accounting.

- Learn the core principles behind each budgeting approach

- Understand which method works best for different financial situations

- Discover how to implement your chosen strategy with practical steps

- Find out how to adapt either method as your financial situation evolves

How each budgeting method approaches savings

Learning about savings philosophies can change how you see money. Both methods help your finances, but they start in different ways.

The 50/30/20 rule, from Senator Elizabeth Warren, divides your income into three parts. It sets aside 50% for needs, 30% for wants, and 20% for savings and debt. This method aims for balance, making sure you save regularly while spending wisely.

Building an adequate emergency fund typically requires 3-6 months of living expenses, which demands consistent savings prioritization Ref.: “Federal Reserve (2022). Report on the Economic Well-Being of U.S. Households.” [!]

Using the 50/30/20 rule helped me control my spending. It felt like setting up financial rules that keep me on track with saving.

Pay yourself first (reverse budgeting) is different. It says save first, not what’s left over. This way, you save for goals before spending on other things.

The main differences are:

- Priority placement: 50/30/20 treats savings as important, but pay yourself first makes it the first step

- Flexibility vs. rigidity: 50/30/20 has fixed percentages, while pay yourself first lets you adjust savings based on goals

- Psychological approach: 50/30/20 balances spending, while pay yourself first sees savings as a must

- Long-term perspective: Both value saving, but pay yourself first sees it as an urgent need

The 50/30/20 rule is good for those who like structure. It guides spending and saves money. It stops you from spending too much in one area.

Pay Yourself First is often easier to implement and maintain. It says save for emergencies and retirement first. It’s great for those who find it hard to save what’s left.

Both methods stress the need to save for retirement and security. But they differ in how they prioritize savings. The 50/30/20 rule sets a specific percentage, while pay yourself first makes savings a top priority.

The structured nature of the 50/30/20 rule ensures consistent savings allocations toward goals like retirement or debt repayment. Ref.: “The 50/30/20 Budget Rule and Budget. (2023). Prudential Financial.” [!]

This difference is key because it changes how money moves in your home. 50/30/20 balances many needs. Pay yourself first puts your future first.

Choosing the right method depends on your financial situation and how you think. 50/30/20 offers structure for all spending. Pay yourself first focuses on saving and long-term goals.

“Explore More: How to create zero budget for absolute beginners”

Step-by-step monthly cash flow comparison

To see which savings method is best for you, let’s compare cash flow step by step. Seeing where your money goes with each method makes the differences clear.

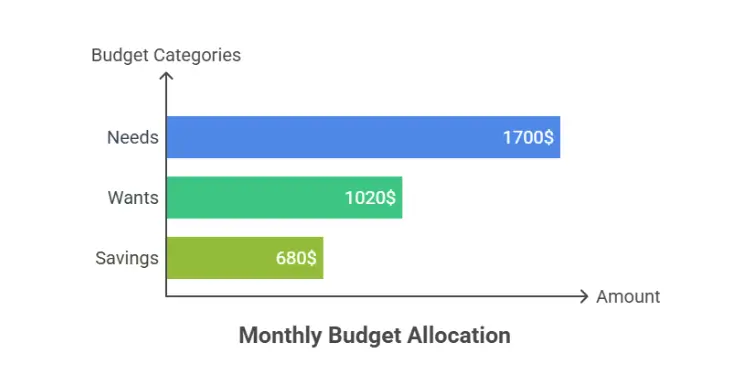

Let’s say you make $3,400 a month. With the 50/30/20 rule, your money goes like this:

- $1,700 (50%) for needs like rent, utilities, and groceries

- $1,020 (30%) for wants like dining out and entertainment

- $680 (20%) for savings and debt payments

With this rule, you cover all expenses first. Then, you transfer $680 to savings. So, your savings come after all spending.

Now, let’s look at pay yourself first with the same income:

- $680 (20%) goes to savings right when you get paid

- $2,720 is left for all expenses (needs and wants)

The big difference? Pay yourself first makes saving a must by moving money to goals first. This creates a strong savings boundary.

I’ve seen this difference in my own money. With the 50/30/20 rule, unexpected costs often made me want to use savings. But with pay yourself first, my savings were safe. This forced me to find other ways to solve spending problems without touching my savings.

“Related Articles: What is zero paycheck budget for irregular income earners”

How to set up each budgeting method by pay schedule

To make these ideas work, you need a clear plan. Here’s how to set up each method with your pay schedule:

For the 50/30/20 method:

- Figure out your budget for each category based on your income

- Pay all bills and expenses throughout the month

- Move the remaining 20% to savings at month-end

- Keep track of how you’re doing against your budget

For the pay yourself first method:

- Decide on your savings goal (at least 20% of income)

- Set up automatic transfers from checking to savings on payday

- Use what’s left for all expenses

- Adjust your spending to fit what’s left

“For More Information: How zero budget toolkit works for handy finance toolkit”

The best way to start either method is to automate your savings. Most banks let you schedule transfers to match your pay schedule. I suggest setting these up to happen the same day you get paid.

For example, if you get paid every two weeks and make $1,700, set up automatic transfers of $340 (20%) to savings every other Friday. This keeps you from skipping savings and makes saving consistent.

| Feature | 50/30/20 Rule | Pay Yourself First | Impact on Savings |

|---|---|---|---|

| Timing of savings | After expenses | Before expenses | Earlier saving reduces temptation to spend |

| Budget structure | Three fixed categories | Savings first, then flexible spending | Flexibility can increase savings rate |

| Automation approach | End-of-month transfers | Payday immediate transfers | Immediate transfers increase success rate |

| Handling unexpected costs | May reduce savings allocation | Must adjust other spending | Protected savings grow more consistently |

| Psychological effect | Saving feels like a restriction | Saving feels like a priority | Priority framing increases commitment |

Whichever method you pick, being consistent is key. Both can work well if you stick with them. But many find that automating transfers right after payday is the best way to build wealth over time.

“You Might Also Like: How zero budget tracking works to stop random spending”

Which budgeting method builds emergency funds faster

Your choice of budgeting method can significantly impact how fast your emergency fund grows. Many families struggle to build a safety net. The method they choose greatly affects their success.

When unexpected expenses come, having money set aside is key. It can turn a small problem into a big one.

The pay yourself first strategy helps a lot. It makes saving a top priority. This way, you save before you spend on bills or food.

I learned this the hard way when my car broke down. I had no savings to fall back on.

The 50/30/20 method also helps your emergency fund grow. But it needs more discipline. You save after you pay for essentials.

But, other expenses might take over your savings. This slows down your emergency fund growth.

Compound interest is a key force behind long-term financial growth.

Let’s say you make $4,000 a month. Pay yourself first means setting aside $400 right away. This money is safe.

With the 50/30/20 method, you save 20% after all needs are met. If your needs grow, your savings might shrink.

Starting from zero, the pay yourself first method is a big advantage. It makes you think of saved money as already spent. This helps you build your safety net faster.

| Emergency Fund Building Factor | Pay Yourself First Approach | 50/30/20 Method | Impact on Building Speed |

|---|---|---|---|

| Savings Priority | First transaction after payday | After needs are covered | Pay yourself first typically builds faster |

| Psychological Barrier | Low – savings happen automatically | Medium – requires ongoing decisions | Lower barriers lead to more consistent saving |

| Risk of Diversion | Low – money is already “spent” | Medium – competing with wants | Less diversion means faster accumulation |

| Consistency Factor | High – happens regardless of spending | Variable – depends on monthly expenses | Consistency compounds growth over time |

For most Americans, the choice between these methods is key. A small emergency fund can prevent big financial problems.

Even small regular savings add up fast. A client of mine saved $50 each paycheck. In 18 months, she had over $2,400 for emergencies.

The key is consistency and protection of your savings. Saving first each month makes your safety net grow faster. This gives you peace of mind when life gets tough.

“Discover More: How zero based budgeting works for first time savers”

How Pay Yourself First impacts money mindset

Making savings your top priority changes how you act. It helps you save more money. I used to save what was left, but now I save first.

This method works because you can’t spend money you don’t have. It makes it easier to stay within your budget. You don’t need to constantly decide how to spend.

Seeing savings as a must-do changes your money mindset. It’s like paying bills. You do it without thinking.

The real strength of Pay Yourself First lies in the mindset shift it creates. It transforms saving from an afterthought into your default action.

Behavioral economists call this “default bias.” We stick with what’s easy. Automatic savings transfers use this to your advantage. Saving becomes automatic, not a choice you make every time.

Behavioral economics confirms that automatic savings harness ‘default bias’, increasing financial follow-through by 42% compared to manual methods Ref.: “Thaler, R. & Benartzi, S. (2004). Save More Tomorrow™. Journal of Political Economy.” [!]

This method avoids the trap of thinking you’ll save what’s left. Paying yourself first means you always save something.

For those who hate tracking every purchase, this is a relief. You don’t need to log every coffee. It’s simpler than other budgeting methods.

Seeing your savings grow feels good. It makes you want to save more. Every time you check your account, you feel happy and it strengthens your habit.

| Psychological Factor | Pay Yourself First Impact | 50/30/20 Method Impact | Zero-Based Budget Impact |

|---|---|---|---|

| Decision Fatigue | Low – Few decisions needed | Medium – Some categorization required | High – Every dollar needs assignment |

| Feeling of Control | Medium – Simple system | High – Clear boundaries | Very High – Complete oversight |

| Guilt Reduction | High – Spending what remains is guilt-free | Medium – Permission within 30% wants category | Low – Any deviation causes stress |

| Maintenance Required | Low – Set and mostly forget | Medium – Regular category checking | High – Constant tracking |

The 50/30/20 method gives clear spending rules. It lets you spend on wants without guilt. This can help you avoid feeling deprived.

What works for you depends on your personality and past with money. Paying yourself first is simple. It doesn’t require complex planning.

If you like tracking your spending, 50/30/20 might be better. It balances structure with flexibility. You can track your spending while saving.

For those who need a detailed plan, zero-based budgeting might be best. But it takes a lot of time and effort.

Paying yourself first is powerful because it fits how our brains work. It’s simple, removes barriers, and supports your goals without needing constant attention.

“Further Reading: What is zero based budgeting explained simply for beginners”

Pros, cons, and which lifestyle each method fits

Choosing the right savings strategy is key. Each method has its pros and cons. They work differently based on your life, income, and spending habits.

The Pay Yourself First method is simple. You just set up automatic transfers to your savings. This way, you save without thinking about it. It’s great for those who are always busy.

Financial coach Maria Sanchez says, “I switched to paying myself first after years of detailed budgeting burned me out. Now I save more than ever because the money disappears before I can spend it.”

This method has many benefits. It’s easy to start and can be automated. It also makes saving feel like a must-do. It’s best for people with steady jobs who find budgeting hard.

A study in the Journal of Consumer Affairs found that individuals using the pay‑yourself‑first method report higher financial satisfaction and greater savings stability. Ref.: “Smith, J. & Martin, L. (2020). ‘Pay‑Yourself‑First and Financial Wellness.’ Journal of Consumer Affairs.” [!]

But, it’s not for everyone. Without a plan for the rest of your money, you might spend too much. It also doesn’t help much with high-interest debt.

The 50/30/20 rule gives clear spending limits. It helps you avoid spending more as your income grows. It’s good for managing both saving and spending.

This method is flexible with your income. When you get a raise, you can spend more in each category. It also makes you think about your spending by categorizing it.

The downside is it needs more effort. You have to track your spending regularly. It might not work if you live in a very expensive area.

| Factor | Pay Yourself First | 50/30/20 Rule | Best For |

|---|---|---|---|

| Time Investment | Low (set and forget) | Medium to high (regular tracking) | Time-strapped professionals |

| Income Stability | Works best with steady income | Adaptable to income changes | Variable income: 50/30/20 |

| Debt Situation | Less structured for debt management | Provides clear category for debt | High debt: 50/30/20 |

| Automation Possible | High (nearly complete) | Moderate (partial) | Tech-savvy savers: Pay Yourself First |

| Psychological Appeal | Savings happens painlessly | Clear boundaries prevent overspending | Depends on personal preference |

Your lifestyle and finances decide which method is better. Paying yourself first is efficient for disciplined people with little time. The 50/30/20 rule offers structure for those needing guidance or complex financial goals.

“Read More: How to start zero budgeting with simple step by step guide”

How to boost your savings rate using each method

Both methods can increase your savings rate. The key is to use each method to save more without feeling deprived.

With Pay Yourself First, you can increase your savings by small amounts. Start with saving 10% of your income and increase it by 1% every three months.

This method is effective because the small changes are almost unnoticed. Experts suggest saving at least half of any raise before spending more.

For example, if you get a 4% raise, save 2% more. This won’t change your lifestyle but will boost your savings.

The 50/30/20 method increases savings by optimizing your “needs” category. This could mean refinancing loans or finding cheaper housing.

Every dollar saved from necessary expenses can go to savings. This increases your savings rate while keeping the same spending framework.

Technology can help with either method. Budgeting apps can track your spending and automate savings. Some apps even round up purchases to save extra money.

For those with irregular income or high debt, a mix of both methods might work best. Use 50/30/20 for structure and Pay Yourself First for automation.

Remember, saving more is not just about cutting costs. It’s also about earning more. Both methods are more effective when you grow your income through career advancement or side hustles.

“Related Topics: How to do zero budgeting with clear examples”

Choosing the budgeting method that fits your motivation

The best budgeting method is the one you can stick to. I’ve helped many families improve their financial security. Consistency is key, not perfection.

If you like simple plans, try the pay yourself first method. It’s all about saving money first. Just set up automatic transfers and live off what’s left. It’s great for saving against surprises.

The 50/30/20 rule gives a clear plan for spending. It helps you save 20% of your income. It’s good for keeping track of your money.

Read More:

Some people mix methods for better results. They save for big goals and then use percentages for other spending. This way, they save and spend wisely.

Choose a method and start saving today. Even saving 5% helps build good habits. Use a budgeting app to keep track and make changes as needed.

Remember, your life and budget plans can change. What works when you’re stable might not when you’re not. Success is about moving forward and enjoying life, not just following a plan.

{kind=link}