My paycheck used to disappear before I knew where it went. But then I found a budgeting method that changed how I see money.

This method is easy to understand. It means giving a job to every dollar you make. By the end of the month, your income minus expenses should equal zero. It’s not about spending all your money. It’s about using it wisely for needs, wants, savings, and paying off debts.

The zero-based budget is great for beginners because it’s clear and simple. No more wondering where your money goes. You get to decide what each dollar does for you.

Zero-based budgeting makes sure all your money goes toward your goals. This helps you build strong personal finance habits that last.

- Gain instant visibility into where every cent goes

- Eliminate financial guesswork by assigning purpose to all income

- Create a solid foundation for long-term money management

- Develop intentional spending habits that support your goals

Set starter goals to anchor your very first zero based budget

Before you start with numbers, set goals for your zero-based budget. This gives you lasting motivation. Many budgets fail because they lack clear goals.

Your budget needs specific targets. These targets answer the “why” behind your planning. When you connect your spending to what matters, budgeting becomes a tool for achieving your dreams.

Identify 1-3 financial goals that are important to you now. Maybe you want to stop living paycheck to paycheck. Or maybe you dream of saving for a vacation without feeling guilty. Write down your goals and keep them where you can see them as you build your zero-based budget.

Emergency Cushion Target Supplies Motivation and Direction

For first-time savers, building an emergency fund is key. Financial surprises happen to everyone. Without a safety net, these surprises can lead to debt.

Start with a goal of saving $1,000. This goal is modest and feels achievable. Once you reach this goal, you can work toward saving 3-6 months of expenses.

Having a clear goal gives you motivation when budgeting is hard. Instead of just “saving more,” you can see how close you are to your goal. This helps you make better spending choices.

Visual Goal Trackers Boost Follow-Through for Beginners

Visualization is powerful in keeping your budget on track. Our brains respond well to visual cues of progress. Seeing your savings grow helps you stay committed.

Choose a tracking method that fits you. Options include:

- A simple progress bar on your fridge

- A digital tracker in your budgeting app

- A savings thermometer you color in after each deposit

- A jar filled with marbles for each $10 saved

These visual reminders make you feel good when you make progress. For beginners, seeing your progress makes saving feel real.

Set clear, specific targets with deadlines. “$1,000 emergency fund by December 1st” is better than vague goals. This way, you can plan exactly how much to save from each paycheck.

Start with goals that are ambitious but realistic. Goals that are too high can lead to frustration. Begin with small wins to build confidence before tackling bigger goals.

Visual goal tracking tools enhance motivation and adherence to budgeting plans. By providing tangible representations of progress, such tools can improve financial behavior and increase the likelihood of achieving savings goals. Ref.: “The Power of Personal Finance Visualization: Visual Tools for Financial Success. Enrichest.” [!]

Gather bank statements to reveal real spending patterns quickly

Starting a zero-based budget means looking at how you really spend money. When I first tried it, I made a budget based on what I thought I spent. But it didn’t match my real spending, and it failed after three weeks. Don’t make the same mistake—start with your financial records.

Get bank statements, credit card bills, and app histories for at least three months. This gives you enough data to spot patterns without feeling overwhelmed. If you use many accounts or methods, get statements from all of them to see your whole financial picture.

Sort your expenses into basic categories like housing, transportation, and food. This helps you see where your money really goes, not just where you think it does.

Three Month Lookback Uncovers Sneaky Subscription Creep

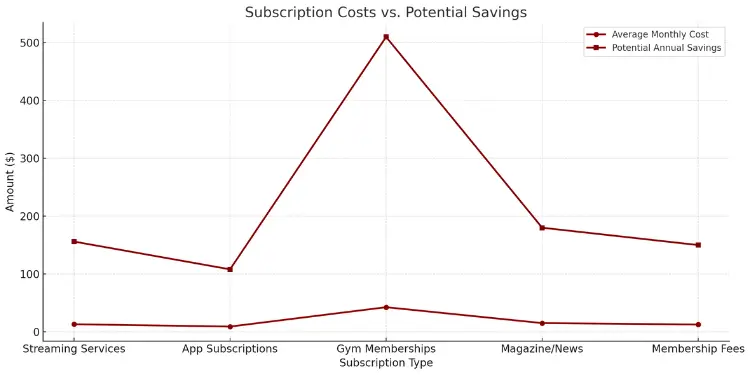

Looking at bank statements often reveals forgotten subscriptions. These small monthly charges can add up a lot over time.

I found I was paying for three streaming services I rarely used, a magazine I forgot to cancel, and a premium app for a one-time project. These unused services cost me nearly $65 a month, or almost $800 a year!

Make a list of all your recurring charges. Include the service name, monthly cost, billing date, and if it’s worth it. This can help you save hundreds of dollars.

| Subscription Type | Common Hiding Places | Average Monthly Cost | Questions to Ask | Potential Annual Savings |

|---|---|---|---|---|

| Streaming Services | Credit card statements | $8-18 each | Do I watch this monthly? | $96-216 per service |

| App Subscriptions | App store charges | $3-15 each | Could I use a free alternative? | $36-180 per app |

| Gym Memberships | Bank auto-drafts | $10-75 | Have I gone in the last month? | $120-900 |

| Magazine/News | PayPal or bank drafts | $5-25 | Do I read this content? | $60-300 |

| Membership Fees | Annual credit card charges | $5-20 (monthly equivalent) | Does this provide real value? | $60-240 |

Identify Seasonal Spikes to Plan Buffers Upfront

Spending changes throughout the year. Reviewing several months of statements helps you spot these changes. These patterns are key to a realistic budget.

Look at utility bills for changes. Do they go up in summer or winter? My electric bill goes up 40% in July and August, but I didn’t plan for it until I looked at my spending.

Holiday spending also changes a lot. Check your statements from November and December to see how much you spend more. This helps you save a little each month instead of using credit cards at holidays.

Don’t forget about quarterly or semi-annual expenses like car insurance or property taxes. These costs can surprise you when they come up. By finding them in your statements, you can save money each month.

After reviewing three months, you’ll know how you really spend money. This data helps you make a budget that works. You’ll know exactly how much to spend on things like groceries or gas.

Tracking your spending is not about judging. It’s about understanding where your money goes. This lets you make smart choices about your money instead of wondering where it all goes.

Build bare-bones fixed expense list before adding variable plans

Before you start with variable spending, list your fixed expenses first. These are costs you can’t change. They are key to financial stability. I learned this the hard way when I planned for fun before paying rent.

Fixed expenses are costs that don’t change much each month. They are the base of your budget. They usually take up most of your income.

Experts say 50% of your income should go to needs, 30% to wants, and 20% to debt and savings. Your fixed expenses are a big part of that 50%.

“You Might Also Like: How zero based budgeting works for first time savers“

The 50/30/20 budgeting rule recommends allocating 50% of income to necessities, 30% to discretionary spending, and 20% to savings and debt repayment. This guideline serves as a benchmark for individuals to structure their budgets effectively. Ref.: “The 50/30/20 Budget Rule Explained With Examples. Investopedia.” [!]

Rent Utilities and Insurance Secure Roof and Safety

The most important fixed expenses are for shelter, safety, and security. Housing costs, like rent or mortgage, are usually the biggest monthly expense. In many U.S. cities, housing costs 25-35% of your income.

Utilities like electricity, water, gas, and internet are also key. While they can change a bit, they’re mostly fixed. Use your highest bill from last year as your budget to avoid surprises.

Insurance is another critical fixed expense. Health insurance protects you from big medical bills. Auto insurance keeps you safe on the road. Renters or homeowners insurance protects your stuff and you.

Be honest about what you really need versus what you want. A basic cell phone plan is a need, but a fancy plan is a want. Basic internet is needed for work, but streaming services are wants.

“The foundation of financial freedom is not about having more money, but about managing the money you have more effectively.”

Even fixed expenses can have some wiggle room. You can talk down insurance rates, use less water, or find better service plans. I saved $43 a month by calling my internet provider.

“Further Reading: What is zero based budgeting explained simply for beginners“

Transfer Minimum Debt Payments on Autopilot Day After Payday

Debt payments are another key fixed expense. This includes credit card minimums, student loans, auto loans, and personal loans. Missing payments can hurt your credit score and lead to extra fees.

Set up automatic transfers for debt payments right after payday. This “pay yourself first” approach makes sure you cover your essential costs before spending on fun things.

If you get paid on the 1st, set up payments for the 2nd or 3rd. This avoids overdrafts and keeps your needs first. Most banks let you choose when you pay, so match it with your pay day.

For debts with high interest, try to pay more than the minimum. Even a little extra can save a lot of money in interest. But only add to these payments after all your fixed expenses are covered.

Make a table with all your fixed expenses, when they’re due, and how much. This helps you remember everything. Here’s how I organize mine:

| Expense Category | Due Date | Amount | Payment Method | Priority Level |

|---|---|---|---|---|

| Rent | 1st | $1,200 | Bank Transfer | Highest |

| Electric Bill | 15th | $85-120 | Autopay | High |

| Health Insurance | 5th | $240 | Autopay | High |

| Credit Card Minimum | 18th | $35 | Autopay | High |

| Internet | 22nd | $65 | Autopay | Medium |

Some fixed expenses come less often, like car insurance or property taxes. Divide these costs by the number of months to make monthly payments. This way, you won’t be caught off guard when the bill comes.

After listing all your fixed expenses and setting up autopayments, you’ll know how much money you have left for other things. This solid foundation lets you spend wisely without worrying about missing payments.

“Discover More: Zero budgeting vs traditional budgeting choosing the right method“

Split remaining cash across variable categories with realistic caps

Zero-based budgeting shines when you split your leftover money into different categories. After paying for fixed costs like rent and insurance, you might have some money left. This is where budgeting gets interesting.

I’ve helped many families improve their finances with the “digital envelope system.” It’s a modern twist on the old cash envelope method. You assign each dollar to a specific use before spending it.

“Related Topics: How to do zero budgeting with clear examples“

Groceries, Transport, and Hobbies Get Separate Envelopes Digitally

Variable spending falls into key areas that need focus. Digital envelopes help you see where your money goes each month.

Start with groceries, a big expense. I once spent 40% more than I thought! Look at your past grocery bills to set a realistic budget. Try to cut 5-10% from that amount.

Transport costs change with gas prices and travel. Save a bit extra for unexpected price jumps.

Household supplies need their own spot too. They add up fast with groceries. This helps you see your food costs better.

| Variable Category | Typical Percentage | Example Amount | Tracking Method | Adjustment Frequency |

|---|---|---|---|---|

| Groceries | 10-15% | $400-600 | Receipt scanning | Weekly |

| Transportation | 5-10% | $150-400 | Gas app or mileage log | Bi-weekly |

| Household Supplies | 2-5% | $50-200 | Dedicated credit card | Monthly |

| Hobbies/Personal | 3-8% | $100-300 | Budgeting app category | Monthly |

| Dining Out | 5-10% | $150-400 | Cash envelope or app | Weekly |

Hobbies and personal interests need a budget spot too. Whether it’s books or sports gear, plan your spending. I save for my photography hobby each month.

The digital envelope system modernizes traditional cash-based budgeting by allowing users to allocate funds into virtual categories. This method enhances spending awareness and control, particularly for variable expenses. Ref.: “How To Use A Digital Envelope System. Clever Girl Finance.” [!]

Budget Fun Money Openly To Prevent Guilt-Based Splurges Later

Budgets need fun to stay alive. Without it, people often give up. Too little freedom leads to rebellion.

Set aside “fun money” each month. It’s not wasteful; it’s smart. Even $25-50 can make a big difference.

Couples should budget together but also have their own fun money. My wife and I each have our own, keeping our spending independent yet aligned.

Use a budget app to track spending in real-time. It helps avoid overspending and keeps you on track.

When setting budget caps, aim for a balance. Too tight and you’ll fail, too loose and you won’t save. Find that middle ground.

If you spend less than budgeted, celebrate! Use the extra for next month, another goal, or your emergency fund.

Don’t worry if your first budget isn’t perfect. Zero-based budgeting is about making progress, not achieving perfection.

Track every transaction in real time using phone friendly tools

Tracking every transaction in real time makes your budget work better. I learned this after trying three times to budget without success. The key is to update your budget with what you spend.

Today’s tech makes tracking easier than old paper ledgers. You need a system that fits your daily life. Phone-friendly tools have changed how we budget.

“Read More: How to create zero budget for absolute beginners“

Free Apps, Envelopes and Spreadsheets Each Have Pros and Cons

Dedicated budgeting apps make zero-based budgeting easy. Apps like YNAB and EveryDollar help you track spending. They let you categorize transactions quickly.

These apps connect to your bank accounts. This means they can update your budget automatically. EveryDollar is simple for beginners. YNAB gives detailed reports but is harder to learn.

Spreadsheets are good if you don’t like apps. Google Sheets and Microsoft Excel have free templates for phones. But, you have to enter each transaction yourself.

The envelope system works for those who prefer not to use apps. It involves using cash for different spending areas. When an envelope is empty, you stop spending in that area.

Each method has its own tradeoffs. Apps are convenient but might cost money. Spreadsheets give control but take time. Cash envelopes help you stay aware but aren’t good for online shopping.

While budgeting apps like YNAB and EveryDollar offer convenience and automation, they may come with subscription fees and varying learning curves. Users should weigh these factors against their budgeting needs and preferences. Ref.: “YNAB vs. EveryDollar: Which Is the Best Zero-Based Budgeting App? Ramsey Solutions.” [!]

Push Notifications Keep You Accountable on Busy Weeks

Life gets busy, and it’s easy to forget to track spending. Push notifications help keep you on track. They remind you to categorize each purchase.

These alerts help me avoid overspending. They pause me before I make impulse buys. This keeps me aware of my spending.

Set a time each day to check your notifications. Even a few minutes can help. Some apps also send alerts when you’re close to spending limits.

The most important thing is to be consistent. Choose a method you’ll use every day. Start simple and adjust as needed. Tracking becomes automatic with practice.

“Related Articles: Zero budgeting vs envelope budgeting which method wins“

Review adjust and redeploy each paycheck not just month end

Zero-based budgeting works best when you check your budget often. It’s better to match your budget cycle with your paychecks. This helps a lot, even when you’re new to budgeting.

Aligning budget reviews with each paycheck cycle, rather than monthly, allows for more responsive financial adjustments. This approach can lead to improved cash flow management and better adherence to budgeting goals. Ref.: “Zero-Based Budgeting 101: Everything You Need to Know. Budgeting Craft.” [!]

Shorter Cycles Reduce Overwhelm And Catch Mistakes Sooner

If you get paid every two weeks, check your budget every two weeks too. This way, you have 26 chances to review your budget each year. It’s a lot easier than just 12 big checks.

When I started doing this, I could see my money better. I even found a $45 charge I forgot about quickly. It’s all about being smart with your money.

When you review, ask simple questions. Like, where did you spend too much? Or where did you save extra? Use these answers to make your next budget better. It’s not about being hard on yourself, but about learning and growing.

Repeat Process Until Saving Becomes Second Nature

At first, making a budget takes a lot of time. But it gets faster with practice. Your budget gets smarter as you learn your spending habits.

“Explore More:

After three months, saving becomes easier. You won’t even think about it anymore. Start a new budget for each pay period. It keeps you connected to your money and helps you plan for the future.

This process might take time, but it’s worth it. Your relationship with money will change. You’ll go from reacting to money to planning ahead. It’s a big change, but it’s worth every minute.

{kind=link}