Learning to use the 50/30/20 budget can change how we handle money. A clear, percentage-based budget can feel like steady sails guiding your financial journey.

Do you think setting aside 30% for wants is okay? According to the Federal Reserve’s 2024 SHED survey, 37% of U.S. adults would be unable to cover an unexpected $400 expense. Sen. Elizabeth Warren says, “Simplicity is power.” Her book helped start this budgeting idea. I paid off $ 80,000 in debt by combining different budgeting methods with a flexible plan.

Let’s set sail for success with the 50/30/20 budget. Check out this budget strategy to guide your after-tax income into different areas.

Key Takeaways:

- Balance needs and wants for sustainable budgeting

- Track progress to build momentum

- Automate debt repayments early

- Adjust allocations for local costs

The widely-cited 50/30/20 split traces back to Senator Elizabeth Warren’s book All Your Worth, which first codified the “needs-wants-savings” percentages that underpin modern percentage-based budgets.Ref.: “Pigford, J. (2024). The 50/30/20 Rule: A Simple Path to Financial Wellness. Maybe Finance.” [!]

Why Percentage-Based Budgeting Works

We’ve all felt budget stress like a rising tide. A recent survey shows 44% of Canadians worry about money. In Maine, households feel the same stress.

Using a simple budgeting strategy can change how we see money. It turns worries into clear steps. We’ll guide you to align every dollar with your dreams.

FP Canada’s 2024 Financial Stress Index confirms that 44 % of Canadians rank money as their single greatest life stressor—up from 40 % in 2023—highlighting the mental-health payoff of a clear budgeting framework.Ref.: “FP Canada (2024). Financial Stress Index 2024. FP Canada.” [!]

Align Your Budget with Personal Values

Figuring out what’s truly important shapes our spending. Our budgeting method connects every purchase to a deeper reason. This helps keep savings and debt repayment steady.

If family security is key, focus on that. Aim for a fixed percentage each month. The 50/30/20 plan is a classic strategy, explained here by Faharas.net.

Create a Compelling Savings Vision

Picture a cozy home or a big outdoor party. This vision makes budgeting a path to real rewards. Every step brings us closer to our dreams.

Action step: Take two minutes to write down your top value. Keep it in sight when making purchases. It helps you stay focused against temptation.

Set clear goals anchoring your motivation early

Imagine a Maine harbor lamp guiding boats through fog. Our budget lamp is like a clear set of financial goals. It keeps our eyes on the next step, even when money is tight.

Write Vivid Goal Statements With Deadlines

We start by thinking about what we really want. Maybe it’s saving for half a year’s rent or paying off debt. We pick a specific date and amount to aim for.

This makes our savings plan clear. It helps us see why we save. It also tells us what to spend on and what to save. For more tips on deadlines, check out this guide.

Break Objectives Into Actionable Micro Steps

We track our progress by breaking goals into three parts. We have everyday needs, fun extras, and saving goals. Each part has small steps, like saving $25 when we can.

We might also cut a streaming bill to save more. These small steps help our emergency fund grow. They show us how to use our money wisely.

Stopwatch Tip: Choose one goal today. Write it down. Set a date. Then list the small steps to stay on track. Do them now before things change.

The latest Federal Reserve SHED survey shows only 63 % of adults could cover a $400 emergency with cash—meaning 37 % remain financially fragile, underscoring the need to prioritise emergency-fund savings within the 20 % bucket.Ref.: “Fed Communities Staff (2025). Economic Well-Being of US Households in 2024. Fed Communities.” [!]

Custom spending plan matching unique circumstances

The rocky coastline teaches us that small shifts in tide can change our route. We adapt the 50/30/20 approach to fit Maine living, aiming for financial stability across every season.

We start by listing every monthly cost in a spreadsheet. This snapshot shows how much net income goes toward essentials. It leaves room for fun spending. We always note our unique savings goals, whether it’s a weekend getaway or building a robust savings account for long-term financial security.

We decide which purchases spark real satisfaction. Farm-fresh groceries might outrank streaming subscriptions. Let’s examine our financial situation in practical terms: does each expense align with our vision? This method shapes a budget that frees us from guilt and fosters healthy boundaries.

- Rank monthly bills based on joy or value.

- Identify adjustments that keep you anchored to purposeful spending.

- Track small wins to stay motivated.

“Further Reading: 50/30/20 budget for beginners simple steps toward money confidence today“

List current expenses by emotional importance

We focus on what truly enriches our day-to-day. Deep awareness of priorities puts us at the helm, steering funds toward meaningful targets. This ensures every choice carries a sense of purpose.

“Discover More: 50/30/20 budget basics every first time budgeter should know now“

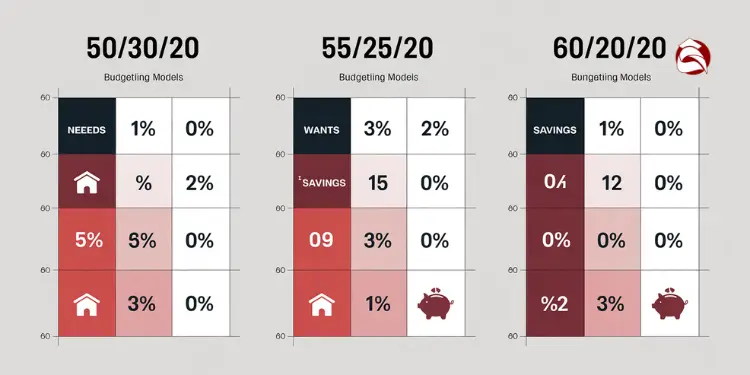

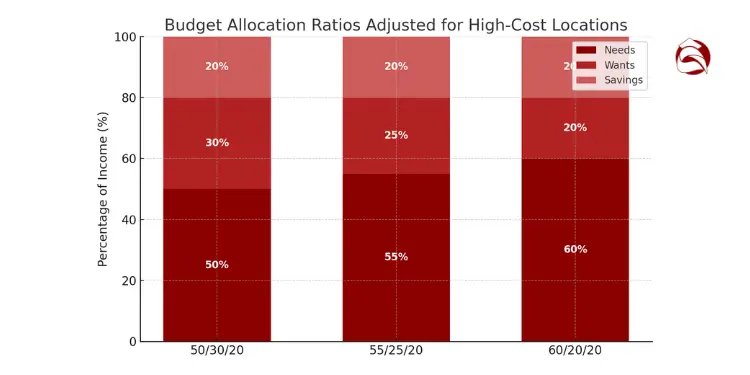

Adjust percentages for high cost locations

When housing costs soar, we tweak the ratio to 55/25/20. One highlight of the 50/30/20 method is its flexibility. Rent in coastal towns may demand extra funds, yet we preserve a solid portion for saving. This table shows sample allocations:

| Ratio | Needs | Wants | Savings |

|---|---|---|---|

| 50/30/20 | 50% | 30% | 20% |

| 55/25/20 | 55% | 25% | 20% |

| 60/20/20 | 60% | 20% | 20% |

Small adjustments keep our budget steady, fueling each savings goal without sacrificing enjoyment. That balance builds peace of mind and nurtures a lasting commitment to healthy finances. We spend a few minutes each week reviewing our progress. By comparing actual spending patterns to the chosen ratio, we protect both short-term comforts and long-term achievements. Let’s keep this momentum going and revise these allocations as life changes. Try setting a 10-minute timer to list your top three financial must-haves right now, and mark them in your plan. It’s an easy way to steer your finances toward a calmer horizon.

In higher-cost regions, 34 % of Connecticut households already spend more than 30 % of income on housing, a Census-tracked threshold for cost burden—illustrating why some budgets must flex needs above 50 %.Ref.: “Stavish, V. (2025). How much of my paycheck should go to rent? CT finds it hard to follow the advice. CT Insider.” [!]

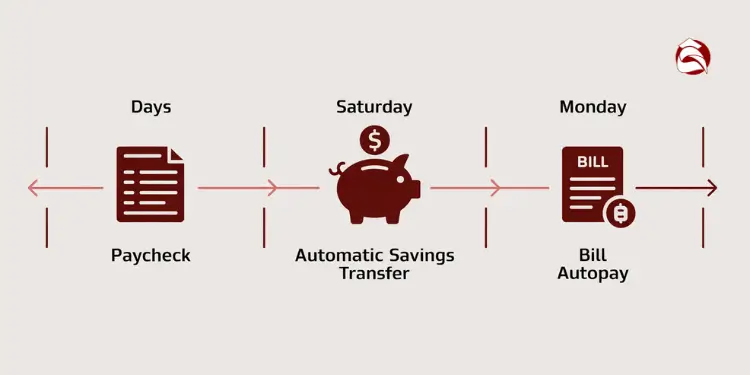

Build automation systems reinforcing budget routine daily

We’ll keep our budget plan strong with a steady, automated process. It feels like reliable tides guiding each paycheck. This habit is key for anyone new to budgeting who wants a balanced approach.

An automatic transfer is a big help. It makes sure we save money for emergencies or debt before we get distracted. We do this right after payday, keeping our momentum and helping our financial future grow.

- Link a reminder: Set a calendar alert the day your paycheck hits.

- Auto-save option: Schedule a precise amount for savings or debt repayment.

- Autopay for essentials: Aim to cover critical bills so you never stray.

A structured outline keeps us on track. A study at pay yourself first shows prompt transfers can stop overspending. Every day, we protect our budget from last-minute temptations that harm our goals.

Below is a quick timeline showing how autopay can flow through each week without friction:

| Weekday | Action |

|---|---|

| Monday | Confirm paycheck deposit |

| Tuesday | Initiate auto transfer for savings or debt repayment |

| Wednesday | Check any upcoming bill autopay |

Automation makes our routine solid, keeps small errors away, and gives us room to breathe. Step by step, we build a better connection between daily choices and long-term success.

Plans that default workers into automatic enrollment reach 94 % participation—versus just 64 % for voluntary plans—according to Vanguard’s 2025 How America Saves report, proving the power of paycheck-automation for building savings momentum.Ref.: “Boyle, E. (2025). Automatic Plan Features Help Participant Savings Rates Stay Resilient in 2024, Says Vanguard. PlanAdviser.” [!]

Use accountability partners to boost discipline

Imagine a Maine lighthouse guiding ships through dark waters. An accountability partner is like that light for your money. We share our goals, keep plans open, and stay on track together.

“Accountability fosters success, when you stick to your budget goals.” – All Your Worth

We might spend too much or forget to save. A support system helps us make a budget that works for us. Having someone to celebrate with and watch out for mistakes is key.

“Related Topics: 50/30/20 budget calculator for quick planning and spending balance guide“

Share Budget Dashboard with Trusted Friend

A friend or family member can quickly see your spending. They help you stay on track to save for retirement. They make saving exciting, turning a boring spreadsheet into a reason to keep going. You can share a page for ideas with them.

Hold Monthly Check Ins over Coffee

Meet up to talk about your money management. Look at your budget app or papers together. Discuss any changes you need to make.

This meeting strengthens your commitment. It’s a chance to adjust your goals, like saving more or spending less online. Small changes add up, helping you make better choices for the future.

Evaluate progress and refresh targets each quarter

Like a Maine lobsterman checking traps, we measure how well our monthly plan aligns with real expenses. This routine helps us take control of your finances. We adjust the percentage of your income if costs shift.

We spot overspending in wants and retool priorities. Or we direct more funds into an emergency cushion.

“Read More: 50/30/20 budget breakdown separating needs wants savings without confusion for beginners“

Compare Actual Ratios Against Written Targets

One local study suggests families who revisit their way to budget every three months see a 34% boost in long-term savings. This popular budgeting habit strengthens confidence. It offers a straightforward budgeting method that promotes financial stability.

For flexible approaches, visit this guide and refine each category as life changes.

“You Might Also Like:

Celebrate Improvements Then Raise Challenge Level

Every achievement deserves a small reward—a homemade treat or a quick trip along the coast—before we push our next goal. We might raise retirement contributions next or pay extra on a credit card.

Or increase your children’s college fund contributions to keep momentum going for long-term goals. That momentum drives us forward. It cements these budgeting habits for a lifetime of steady growth.

{kind=link}