Choosing the right budget can change your financial future. Recent data shows approximately 86% of U.S. households do use a budget—but 74% say rising costs make it hard to stick with it. Yet, experts say using a percentage-based system is best.

When I graduated and got my first bills, I was lost. Should I spend half my paycheck on rent? Was saving 10% enough? The numbers were confusing.

“When you ask, ‘What do I want my money to do for me?’ you’re deciding how you’ll use your money to get closer to the life you want,” said financial author Jesse Mecham. “It shows our values and dreams.” This changed how I saw money.

The 50/30/20 and 60/30/10 methods help divide your income into useful parts. The main difference is how much they focus on needs versus saving for the future.

This guide will show you which budget rule is best for you. With today’s high costs for housing and food, it’s important to choose wisely.

Household budget constraints are exacerbated by persistent inflation in essential costs—rent and housing climbed faster than incomes from 2000 to 2020. Ref.: “Rent, House Prices, and Demographics”, U.S. Department of the Treasury. [!]

- Learn the main differences between these budget methods

- Find out which one suits your financial situation better

- Get tips on using either system in your daily money management

Philosophical focus of each budgeting ratio

Every budgeting ratio has its own money philosophy. The 50/30/20 and 60/30/10 methods show different ways to balance today and tomorrow. They are not just numbers.

As financial advisor Waymire explains,

“One of the things that the 50/30/20 and the 60/30/10 budget have in common is that they’re just starting points to provide a general allocation for where your money goes. Neither of these budget guidelines are meant to be hard and fast rules because everyone’s situation is different.”

Your budget should match your financial goals. Let’s look at what each ratio says about its philosophy:

- 50/30/20 Philosophy: This method focuses on saving (20%) and essential costs (50%). It says saving for the future is key.

- 60/30/10 Philosophy: This method knows many people spend a lot on basics like housing and healthcare. It says you might need to spend more than half your income on these.

- Shared 30% View: Both methods save 30% for fun. They say you need room for enjoyment in your budget.

The 50/30/20 method is great for those who want to save a lot. When I was paying off my mortgage, it helped me stay on track without feeling poor.

The 60/30/10 method is better for those in expensive places. It says you can save, even if you spend a lot on basics.

“For More Information: Should I use 50/30/20 budget or another budgeting method“

Balancing Lifestyle Comfort with Disciplined Savings

Budgeting is not just about cutting spending. It’s about finding a balance that fits your life. Both methods keep room for fun.

This 30% for wants is smart. Cutting out fun can make budgets fail. I’ve seen people give up on budgets because they’re too strict.

The main difference is how they balance now and later:

| Aspect | 50/30/20 Approach | 60/30/10 Approach |

|---|---|---|

| Priority Focus | Balanced between needs and future | Acknowledges higher cost of necessities |

| Savings Rate | Higher (20%) | Lower (10%) |

| Best For | Debt reduction, building wealth | High cost-of-living areas, lower incomes |

| Financial Security | Faster emergency fund building | Slower but consistent saving |

Neither method is better. They just show different views and life situations. The 50/30/20 might fit some stages, while the 60/30/10 might fit others.

What’s key is finding a budget that lets you meet needs, enjoy now, and plan for the future. The right ratio should feel empowering, not limiting.

When choosing, ask yourself:

- What are your top financial goals? (Debt, homeownership, retirement)

- How much do you really need for basics?

- How much fun spending do you need to stay happy without hurting your goals?

- Which method feels right for your life now?

Remember, these ratios are just starting points. The best budget changes with you, staying true to balance and purpose.

Studies show combining percentage-based budgeting with tools like envelope systems can significantly improve financial discipline and outcomes. Ref.: Rosales, B. A. et al. (2020). “Assessment on Effectiveness of Using 50‑30‑20 Rule…”, AASGB Publisher. [!]

“Explore More: 50/30/20 budget for families tackling kids expenses and monthly bills“

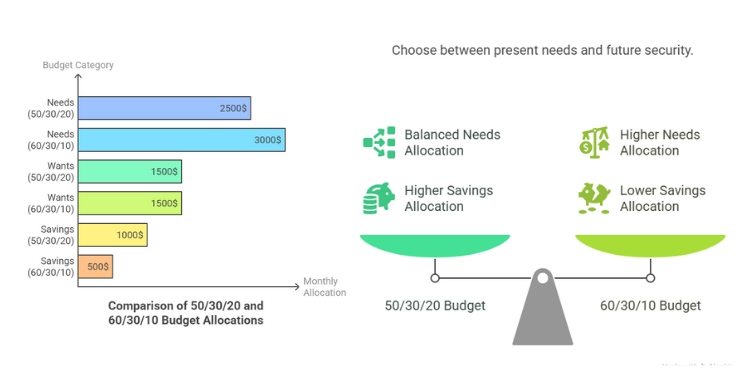

Side‑by‑Side Budget Allocations

It’s important to know how your money is split between needs, wants, and savings. Both budgeting systems divide your money into three parts. But, the way you spend your money can change a lot.

Let’s look at how your money is spent differently. For a family with $5,000 a month after taxes, here’s how it’s split:

| Category | 50/30/20 Budget | 60/30/10 Budget | Key Difference |

|---|---|---|---|

| Needs | $2,500 (50%) | $3,000 (60%) | +$500 for essentials |

| Wants | $1,500 (30%) | $1,500 (30%) | No change |

| Savings | $1,000 (20%) | $500 (10%) | -$500 in savings |

| Monthly Impact | Tighter essential budget | More breathing room | Trade-off between present needs and future security |

This table shows a big choice: the 60/30/10 method gives more money for now but less for later. For many, this helps with high costs and debt.

Essential Spending Coverage Under Higher Needs Share

The 60/30/10 budget helps with high costs. It lets you spend more on must-haves like:

- Rent or mortgage payments in high-cost areas

- Utility bills and basic services

- Groceries and necessary food items

- Healthcare costs and insurance premiums

- Minimum debt payments, like credit card debt

This way, families in expensive places or with big medical bills have more room. When I was fixing my credit, this helped me not feel stuck.

For example, a family might spend $1,800 on housing, $400 on utilities, $800 on groceries, and $300 on insurance. This is already more than 50%. The 60% helps without cutting too much.

Savings Acceleration With Reduced Discretionary Spending

The 50/30/20 budget focuses on saving 20% of your income. This can really change your financial future. With $5,000 a month, you save $500 more each month or $6,000 a year for things like:

- Building an emergency fund faster

- Contributing more to retirement accounts

- Paying down high-interest debt more aggressively

- Saving for big purchases like a home down payment

More savings means more money over time. An extra $500 a month at 7% interest grows to about $87,500 in 10 years. This can help you retire early or reach big goals sooner.

But, saving 20% needs careful planning. You must decide if you can save this much without hurting your daily life.

Success comes from knowing what you really need. Many things we think we need are just wants. True needs keep us living and earning, while wants make life better but aren’t essential.

Step‑by‑Step Budgeting Setup

Are you ready to start using your budget ratio? Let’s go through a simple plan for your first month. Whether you picked the 50/30/20 or 60/30/10 method, setting it up is similar.

First, think about your financial goals. Financial advisor Mark Guntrip says, “Start with short and long-term goals. This could be paying off debt, saving for a vacation, or a down payment for a house. Then, track your expenses to see where your money goes each month.”

Now, let’s get started with your budget:

- Find out how much money you have left after taxes each month.

- Look at last month’s spending to see what you usually buy.

- Sort your expenses into needs, wants, and savings.

- Use your chosen ratio to decide how much to spend in each area.

- Open special accounts for each category.

- Choose how you’ll track your spending, like an app or spreadsheet.

Setting Realistic Category Caps And Tracking

Setting the right spending limits is key to a good budget. Many people underestimate their expenses at first. I did too, setting my grocery budget too low.

Look at your spending from the last three months to set better limits. If you’re using the 50/30/20 method, your needs might include:

| Need Category | Typical Items | Tracking Tips | Common Pitfalls |

|---|---|---|---|

| Housing | Rent/mortgage, utilities, insurance | Set automatic payments | Forgetting seasonal utility changes |

| Food | Groceries, essential meals | Keep receipts or use store apps | Mixing food and non-food items |

| Transportation | Car payment, gas, insurance, public transit | Use a dedicated gas card | Not counting maintenance costs |

| Healthcare | Insurance, medications, appointments | Request itemized receipts | Not planning for annual deductibles |

To track your spending, use a budgeting app like Mint or YNAB. I like apps that update automatically. This way, you can’t forget to record your expenses.

For discretionary spending, try the envelope method. This means using cash for wants and putting it in labeled envelopes. When an envelope is empty, you know you’ve reached your limit. This method helps avoid overspending.

Adjusting After Reviewing Initial Expense Data

The first month is just a test. Don’t worry if it’s not perfect. After 30 days, review and adjust your budget based on real numbers.

Ask yourself these questions with your tracking tool:

- Which categories did you go over budget on?

- Were there any surprise expenses?

- Did you move money between categories?

- Did your spending match your target ratio?

Use this info to tweak your budget. If you’re spending too much on needs and not enough on wants, adjust. Some “wants” might really be “needs” for you.

For example, I first thought my gym membership was a want. But it really helped my health, so I changed it to a need.

Feel free to switch between 50/30/20 and 60/30/10 if needed. Some people start with 50/30/20 and then switch to 60/30/10 as they save more.

Remember, managing your money is a journey, not a one-time task. Each month, you’ll learn more and can improve your budget. The goal is to create a system that helps you reach your financial goals, not just follow numbers.

“The best budget isn’t the one that looks perfect on paper—it’s the one you’ll actually stick with month after month.”

Managing Variable Income & Bonuses

When your income changes with the seasons or you get unexpected bonuses, you need to adjust your budget. The 50/30/20 and 60/30/10 methods help you manage these changes well. But, you must plan carefully to avoid financial setbacks.

I learned a hard lesson with my first year-end bonus. I thought it was extra money and spent it all. But soon, I missed a chance to reach my financial goals.

Dealing with income that changes or comes in unexpectedly? Here’s how to adjust your budget:

Allocating Bonuses Without Lifestyle Inflation Creep

Bonuses and tax refunds can make you want to spend more. But, this can lead to spending more as your income grows. Instead, use these funds to secure your financial future.

For the 50/30/20 budget, try this:

- 50% toward debt repayment or building an emergency fund

- 30% for a specific savings goal (like a home down payment)

- 20% for something fun (like a small treat)

With the 60/30/10 rule, adjust it this way:

- 60% toward debt repayment and emergency savings

- 30% for long-term savings goals

- 10% for enjoying life

This way, you can celebrate while also moving forward financially. My second bonus helped me pay off a high-interest credit card. That felt better than buying something new.

“The true cost of lifestyle inflation isn’t just what you spend today, but the compound growth those dollars could have generated over decades.”

For income that changes with the seasons, make a plan. Save extra money in good months for bad ones. This keeps your budget steady.

If you have side jobs or freelance, first subtract taxes and expenses. Then, use what’s left for your budget. Set reminders to move this money to your savings regularly.

| Income Type | 50/30/20 Approach | 60/30/10 Approach | Key Benefit |

|---|---|---|---|

| Annual Bonus | 50% to debt/emergency fund | 60% to debt/emergency fund | Accelerates financial security |

| Tax Refund | 50% to mortgage principal | 60% to mortgage principal | Reduces long-term interest costs |

| Seasonal Income | Bank surplus for lean months | Bank surplus for lean months | Creates income stability |

| Side Gig Money | Dedicated to specific goal | Dedicated to specific goal | Prevents lifestyle creep |

When you make more money, don’t spend more on wants. The 60/30/10 rule helps because it spends less on non-essentials. This leaves room for important things.

When living costs go up, you need to adjust your budget. The 60/30/10 rule helps with this because it saves more for essentials.

Remember, budget rules might need to change during big life events. But, try to budgets may require adaptation amid inflation or rate shifts.

“Related Articles: 50/30/20 budget for low income households that stretches every dollar“

Behavioral factors influencing long term consistency

Math is important, but so is how you behave. I’ve helped many neighbors with their money. The best budget is one you can keep up with for life. 28% of Americans are actively increasing their financial literacy built-in trend toward mindful budgeting.

Sticking to your budget is key to reaching your money goals. Many start strong but give up soon. It’s not just about the numbers, but the habits you build.

“By being really mindful about your spending, you have the tools to cut down on areas that aren’t a priority, so you can free up money for the important things that bring you the most joy,” Waymire said. “Without a budget, it can be challenging to make sure there’s actually money at the end of the month to put towards your big goals and dreams.”

Being mindful is what makes a budget work. It doesn’t matter if you spend 50% or 60% on needs. What matters is if you can keep up with it. Let’s look at what makes you stick to it.

“You Might Also Like: 50/30/20 budget calculator for quick planning and spending balance guide“

Accountability Partners and Visual Progress Tracking

Having someone to check up on you helps a lot. When I started managing my money, my sister checked in every month. This made me more careful with my spending.

Your accountability partner doesn’t need to know all your spending details. They just need to ask if you’re sticking to your budget. This helps you stay on track when you want to spend more.

Seeing your progress is also very helpful. It gives you a boost when you’re making smart financial choices. This makes it easier to keep going.

| Accountability Method | Best For | Implementation Tips | Success Rate |

|---|---|---|---|

| Budget Buddy System | Social learners | Monthly coffee meetings to review progress | High (78% consistency) |

| Visual Progress Charts | Visual learners | Wall-mounted savings thermometer or app dashboard | Medium (65% consistency) |

| Financial Coach Check-ins | Those needing expertise | Quarterly professional reviews of budget adherence | Very High (82% consistency) |

| Family Budget Meetings | Households with shared expenses | Weekly 15-minute spending reviews with partners | High (75% consistency) |

Make your budget a little fun. Set aside some money for things you enjoy. This stops you from feeling like you’re missing out.

Try your budget for at least three months. This helps you get used to it and see the benefits. It makes it easier to keep going.

Automating your savings helps too. Set up automatic transfers for your savings. This way, you won’t forget to save.

Don’t worry if you slip up. The best budgeters plan for mistakes. Having a way to get back on track is key to success.

Being consistent is more important than being perfect. A 60/30/10 budget can work better than a 50/30/20 one if you stick to it. Choose what works for you, not just what sounds good.

“Read More: 50/30/20 vs 60/30/10 budget full comparison guide“

Choosing the Right Ratio for Your Life Stage

Choosing the right budget rule depends on your unique financial situation and goals. The 50/30/20 approach offers balance. The 60/30/10 rule works better for those facing higher living costs in today’s economy.

First, look at your current spending patterns. Housing costs have risen a lot, with Between 2000–2020, inflation‑adjusted housing prices rose ~65%, with rents increasing over 20%—outpacing stagnant income growth.

Many Americans now spend about 30% of their income on rent alone. This makes the 60/30/10 split a better fit for many.

Next, think about your long-term financial goals. Are you trying to pay off credit card debt with record high interest rates (now averaging 20.74%)? The 60/30/10 budget may help you allocate more toward these essential payments.

- 50/30/20 budget breakdown of needs, wants, and savings

- 50/30/20 budget example for a typical monthly income

- How to make 50/30/20 budget with clear practical step by step

Remember that both systems organize spending into three main categories – they just adjust the proportions. The best monthly budget is one you’ll actually follow. Start with the ratio that fits your current situation, then take control of your finances by adjusting as your circumstances change.

Different budget approaches serve different purposes. What matters most is picking a system that helps you balance today’s needs with tomorrow’s dreams.

{kind=link}