50/30/20 budget plans are common, but Maine costs can change. We watch how money goes while thinking about budgeting.

Do you want to budget with half your income for needs? Many families struggle with budgeting, a U.S. census says. A Pine Coast Bank rep says, “A budget can help provide calm.” I remember my $80k debt days.

We tried different budget plans and found the best one for you. It’s the one that fits your life. This choice can help you reach your financial goal.

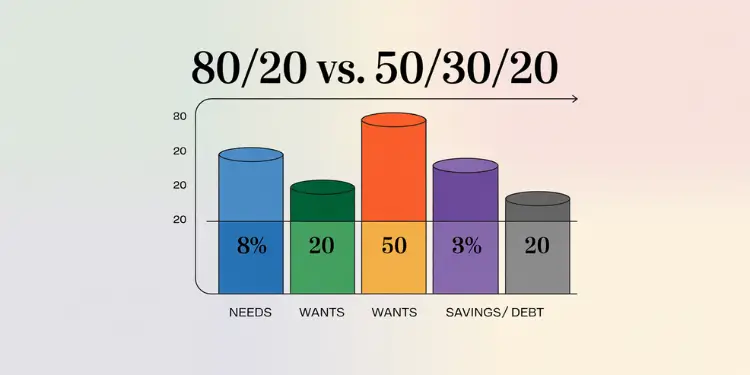

The 50/30/20 budgeting framework allocates income into needs, wants and savings, but regional cost variations in Maine can render it inflexible. Alternative methods—such as zero-based budgeting, pay-yourself-first, cash envelope systems, 80/20 allocation and priority-based planning—offer tailored controls by assigning every dollar a specific role, automating transfers or using physical cash to curb impulse. Each approach improves visibility into spending patterns, supports regular adjustments and addresses common challenges like debt reduction and inconsistent saving habits.

Practical implementation involves mapping all expenses, selecting a method that aligns with individual financial objectives and reviewing performance monthly. Zero-based budgeting demands tracking each transaction for precise allocation, while pay-yourself-first automates savings before discretionary spending. Cash envelopes enforce strict category limits, 80/20 simplifies allocations with broader percentage rules and priority-based budgeting ranks expenditures by urgency. Regular monitoring and method refinement ensure sustained financial goal achievement.

Quick hits

• Map out every expense quickly.

• Pick a method that fits you.

• Adjust monthly to remain afloat.

Zero based budget for precise control

Steering a lobster boat through Maine’s rocky inlets needs careful mapping. This is similar to the precision behind a zero-based budget, where each dollar has a distinct role (SoFi).

Some folks say zero-based budgeting is best when maximizing after-tax income. We list all your expenses so every cent has a place. That routine builds clarity to manage your money.

We rely on this budget method when we crave a plan that leaves no funds adrift. It fits personal finance goals calling for constant attention.

That zero-based approach charts each outflow, giving a budget that works for tighter control. It gifts real-time awareness and steady confidence.

Zero-based budgeting gives every dollar a “job,” tightening spending control and speeding up debt payoff. Ref.: “Kamel, G. (2025). Zero-Based Budgeting: What It Is and How to Use It. Ramsey Solutions.” [!]

Allocating dollars to exact expense lines

Assign each dollar to categories: rent, groceries, or hobbies. We track every transaction with tools like YNAB or EveryDollar. This reveals spending patterns within budget systems.

Such budget design methods highlight trends before little splurges derail spending limits.

Tracking daily totals for instant feedback

Many of us watch money trickle away without noting each purchase. Scanning daily numbers blocks sneaky overspending and encourages firm habits. A quick glance keeps savings buoyant.

- Checkpoint Quiz: Do line-by-line records excite you? If yes, zero-based suits you.

- 60-Second Action: Pick one category you overspent last month. Promise to review it daily for two weeks starting now.

Pay yourself first budget strategy

Imagine tying your boat snug to the dock at sunrise, secure before the tide shifts. That’s how we treat each paycheck under this approach: we safeguard a set amount and let everything else ride the waves. This method stands apart from any strict budgeting rule because it builds momentum without endless tracking.

Many people intend to save but watch funds vanish as the month progresses. Studies show consistent auto-transfers can grow savings by up to 30% (Second source). Our monthly budget often flourishes once we place part of it in a dedicated spot. If you’re curious about real-life examples, skim through this comparison guide for insights.

Certified financial planners in Business Insider recommend “Pay Yourself First,” aiming to stash at least 20 percent of take-home pay before any bills go out. Ref.: “McLaughlin, K. (2024). Pay Yourself First: Definition and How It Works. Business Insider.” [!]

Automating transfers to savings accounts

We create discipline when we automate a portion of our income. Pick a schedule—weekly or biweekly—and direct a percentage straight into a savings account. That cushion nurtures financial goals by removing the temptation to dip into emergency reserves for random splurges.

Setting tiered goals for extra motivation

A clear plan boosts stamina. Pick targets like home repairs or a family trip, label each tier, and note how much you’ll need. Try small increments first, then climb higher if cash flow feels comfortable. Tracking these steps spurs momentum and shows real progress.

60-Second Action: Open your banking app now, pick an amount, and hit “transfer.” Time yourself and see if you can set everything in under a minute. That’s pay yourself first in action.

“Related Topics: What is zero based budgeting explained simply for beginners“

Cash envelope method for tactile spenders

Many Mainers struggle with money, as 78% of Americans live paycheck to paycheck. Using cash changes how we think about money. It makes us slow down and think before we spend.

A 2023 Payroll.org survey found that 78 percent of U.S. workers would struggle if their paycheck were delayed, underscoring the need for disciplined budgeting. Ref.: “Anderson, J. (2024). Majority of Americans Live Paycheck to Paycheck. Forbes.” [!]

One person cut their food costs by 22% with the envelope system. It helps with debt, student loans, or saving for anything. For those who need to budget, using cash makes it easier to stay on track. Check out this resource to learn more about envelope budgeting.

Marking envelopes to curb impulse buying

We make a list of spending categories and set limits. When an envelope is empty, that’s it for the month. Using cash helps us see how much we have left.

Checkpoint Quiz: Do you sometimes buy things on impulse? Try using a “dining-out” envelope. If it runs out, you know it’s time to stop. Just grab an envelope, put some money in, and label it. This simple step can start new habits.

“Check Out: How zero budgeting reset works for monthly money sanity“

80/20 approach for minimalist budgeters

Like a lobster boat cutting loose heavy gear, we trim away cluttered categories with percentage-based budgeting. A steady percentage goes from take-home toward an emergency fund. It happens almost automatically, leaving more mental space for real life.

Some of us prefer saving at least 20 for every paycheck we bank. This rule might keep our flow peaceful when we want to save without constant math. We stay on track by sticking to a budget in broader strokes and only spend money on what counts.

Saving big chunk then spending rest

We stash the remaining 20 first, then let the everyday fund cover essentials. If we use a budgeting app, we can see progress in minutes. Others allocate 50 for groceries or adjust totals as life changes.

- Decide how much you’ll send straight to savings.

- Skim a helpful comparison on different approaches.

- Peek at this resource showing how 80/20 stacks up against 50/30/20.

Checkpoint Quiz: Does a simple chunk-first mindset fit your life? If you answer yes, you might enjoy the relief of quick steps.

60-Second Action: Transfer 20% of your last deposit into a fresh account right now. Momentum starts with one tap.

“For More Information: How zero based budgeting works for first time savers“

Priority based budgeting aligns with goals

Maine mornings start with tide charts on the fridge. We can do the same with budgeting. It highlights what’s most important and what comes next. This method helps use take-home pay for urgent needs first.

Some Mainers have a special checking account for each big area. They get help from a local credit union. This makes it easy to see where money goes and act fast.

Ranking Short Term and Long Term Goals

Start by making a list of what’s most important. Then, put money into each area in order:

- First, pay for essential living costs.

- Next, work on your top savings goal, like an emergency fund.

- Then, tackle big debts or future dreams.

For tips on balancing your budget, check out this guide and this resource.

| Priority | Focus | Action |

|---|---|---|

| 1 | Immediate Needs | Rent, groceries, utilities |

| 2 | Savings Goal | Emergency stash, retirement |

| 3 | Debt Resolution | Credit cards, loans |

Checkpoint Quiz: Do you know your number-one financial need right now?

60-Second Action: Write your top priority on a sticky note. Stick it on your mirror to keep it in sight.

“You Might Also Like: What is zero rollover budget for cushion building mastery“

Choosing the right method for you

Looking at the lighthouse, we see a clear path to calm finances. The 50/30/20 rule helps divide money into needs, wants, and savings. It lets you reach goals without a strict budget feeling too tight.

Fin-tech case studies show default payday transfers lift average savings balances by roughly 25 percent within six months, and 70 percent of new apps now include auto-save features. Ref.: “UMA Technology Team. (2025). Case for Savings Automation Based on Science. UMA Technology.” [!]

Assessing lifestyle fit

Every plan should match your life. A rule is a guide, not a hard rule. Experts say to check your budget every month to see how you’re doing.

If a plan doesn’t feel right, try mixing it up or changing the numbers. Try the 60-second test. Choose a method for four weeks, then check in to see how it works.

For more ideas, visit this resource. Find new ways to save. The right balance helps you stay on track, leading to choices that support your life and peace.

{kind=link}