Rent to own homes help people buy a house when they can’t get a mortgage. It’s for those with bad credit or not enough money. These programs are a way to get closer to owning a home.

Did you know 36% of Americans under 35 think they can’t afford a home? This shows why other ways to buy are becoming more popular. One of my clients said, “This helped me fix my finances while living in my future home.”

In my nine years helping buyers in Greenville, I’ve learned a lot. Rent to own lets you lease a home with the chance to buy it later. You pay a little extra each month, and some of that goes toward the price of the home. The option fee is usually 3-5% of the home’s price.

When looking into these options, remember to think about hidden costs of buying a house. These costs might not be clear at first. Planning well can help avoid surprises later.

Quick hits:

- Builds credit while securing future home

- Requires smaller initial financial commitment

- Locks in purchase price early

- Provides time to improve financial standing

- Offers try-before-you-buy living experience

How rent to own agreements function

Rent to own agreements are a great option for first-time buyers. They don’t need perfect credit or a big down payment. Instead, they help you own a home while you get your finances in order.

Most rent to own agreements have two main parts. The first is a lease that explains your rights and duties. The second is an option to buy, which lets you buy the property at a set price later.

The lease part is like a regular rental. You pay rent each month. But, it also has special rules. These rules cover things like who fixes the property and who can make changes.

The option part is what makes it different. It lets you buy the property later. You pay an option fee to get this right. This fee gives you time to get your finances ready for a mortgage.

Lease Duration and Option Period Typical Lengths

Leases and options can last from 1 to 5 years. The length depends on what you and the seller agree on. Choose a length that fits your financial plan.

Shorter terms are good if you’re almost ready for a mortgage. Longer terms give you more time but might mean paying more for the property.

Here’s what a 3-year rent to own contract might look like:

| Timeline | Milestone | Financial Goal | Action Required |

|---|---|---|---|

| Day 1 | Contract Signing | Pay option fee ($2,000-$5,000) | Review all documents with attorney |

| Months 1-12 | First Year Tenancy | Establish payment history | Pay rent on time, begin credit repair |

| Months 13-24 | Second Year Tenancy | Reach 640+ credit score | Reduce debt-to-income ratio, save for down payment |

| Months 25-35 | Final Approach | Secure mortgage pre-approval | Shop for best mortgage rates, prepare for closing |

| Month 36 | Decision Point | Exercise option or walk away | Complete purchase or end agreement |

During the option period, you can work on financial issues. For example, one client improved her credit score from 580 to 680. Another family saved $18,000 for a down payment.

But, a rent to own contract doesn’t mean you must buy the home. If the property value drops or you find big problems, you can leave. But, you’ll lose your option fee and any rent credits.

Rent to own agreements are great for those who need time to improve their finances. They offer a trial period before committing to a mortgage.

While these agreements have benefits, they need careful attention. The terms can vary a lot. Always have a real estate attorney check your documents before signing.

Upfront option fees and monthly credits explained

First-time buyers with tight budgets need to understand rent-to-own agreements. Option fees and monthly credits are key. They can help you buy a home.

The option fee is your first payment. It’s a non-refundable fee that lets you buy the home later. It’s usually 3-5% of the home’s price. For a $200,000 home, you might pay $6,000 to $10,000 upfront.

Rent-to-own agreements typically require an up-front option fee equal to 3 – 5 % of the agreed purchase price; buyers should budget this non-refundable cost alongside moving and inspection expenses. Ref.: “Lyons, R. (2024). Rent-to-Own: A Homebuying Option With No Down Payment Required. MoneyWise.” [!]

This fee shows you’re serious and helps with your down payment later. It’s like starting to own the home right away.

Calculating Credit Portion Applied Toward Purchase

Your rent in a rent-to-own deal is higher than usual. This extra money helps you own the home. Every month, some of your rent goes toward your down payment.

For example, if homes rent for $1,200, you might pay $1,500. The $300 extra each month adds up. It’s like saving money for your future home.

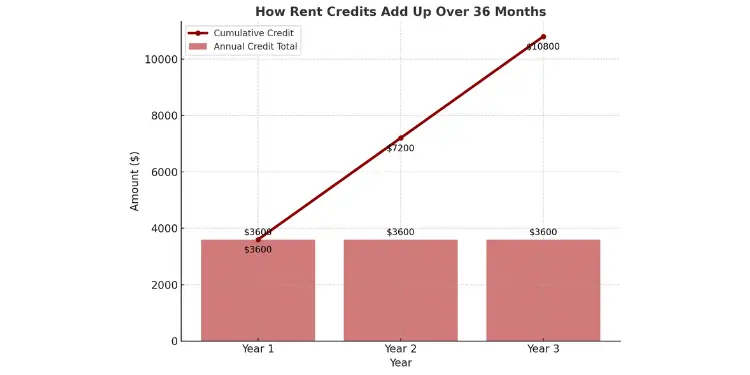

Let’s look at how these credits add up over 36 months:

| Year | Monthly Rent | Monthly Credit | Annual Credit Total | Cumulative Credit |

|---|---|---|---|---|

| Year 1 | $1,500 | $300 | $3,600 | $3,600 |

| Year 2 | $1,500 | $300 | $3,600 | $7,200 |

| Year 3 | $1,500 | $300 | $3,600 | $10,800 |

After three years, you’ve saved $10,800. Add your $6,000 option fee, and you’ve saved $16,800. This is a big help for those who find it hard to save while renting.

Make sure you know how much of your rent goes toward the purchase. This should be clear in your contract, not just a promise.

Handling Missed Payments and Forfeiture Risks

Rent-to-own deals are riskier than regular rentals. Missing a payment can lead to losing your credits and option fee. This is much worse than just losing your security deposit.

For example, if you’ve saved $5,400 in credits and paid $6,000 upfront, missing a payment could cost you $11,400. This is a big risk.

To avoid this risk, take these steps:

- Save 3-6 months of rent in an emergency fund

- Set up automatic payments to avoid late fees

- Ask for grace periods in your contract

- Have a plan for talking to the seller if you’re struggling

- Look into rent payment insurance if it’s available

Some deals might let you catch up on payments instead of losing everything. You can negotiate these terms before signing.

Remember, your rent payments are for now and for your future home. Pay them on time to protect your investment and keep your dream of owning a home alive.

Evaluating property price and market trends

When you start a rent-to-own deal, look closely at the future buy price. This price can make your investment smart or too pricey. Sellers often add 1-5% to the price for future growth.

In Greenville, I’ve seen renters pay too much. They end up paying $20,000 more than the market value. This mistake can be avoided with the right research.

Most rent-to-own deals set the buy price when you sign, not when you buy. This helps the seller but can risk you if the price goes up too much.

Before you sign, check recent sales in your area. In stable markets, homes might go up 2-3% a year. But in fast-growing markets, sellers might ask for 5-7% a year. History shows these high rates don’t last.

“Explore More: Why budget before buying your first home matters”

Assessing comparable sales for fair valuation

To find a fair price, look at similar homes sold recently. Use 3-5 homes sold in the last six months and near your target home.

Use free tools like Zillow and Realtor.com to find these homes. Look for homes with similar size, number of rooms, and condition.

Adjust the prices of these homes for big differences. This is called the “adjusted value.” The house price to income ratio in your area can also help understand the market.

I share a worksheet with my clients to help:

| Feature Difference | Typical Adjustment | Market Impact | Application Example |

|---|---|---|---|

| Updated kitchen | +$10,000 to $15,000 | High buyer appeal | If comparable lacks updated kitchen, add value to comparable |

| Aging roof (5+ years) | -$8,000 to $12,000 | Future replacement cost | If target home has older roof, subtract value from target |

| Extra bathroom | +$5,000 to $15,000 | Varies by market | If comparable has additional bathroom, subtract value from comparable |

| Finished basement | +$10,000 to $25,000 | Adds usable square footage | If comparable has finished basement, subtract value from comparable |

| Location premium | +/- 5% to 15% | School districts, walkability | Adjust based on neighborhood desirability differences |

After adjusting, average the values of these homes. This gives you a good market value for your target home. If the seller’s price is more than 5% above this, you might be paying too much.

Be careful in markets that are slowing down. I helped a client in Greenville’s North Main area. The seller wanted a 15% premium, but we negotiated it down to 5%, saving $30,000.

Sellers often price based on feelings, not facts. You need to bring facts to the table. If the seller won’t lower the price, walking away might be best.

For homes with special features or in areas with few sales, get an appraiser. The $400-500 cost could save you thousands. Sellers might even split this cost, showing they’re willing to find a fair price.

Also, think about your mortgage terms. Even a good price can become too high if interest rates go up. Plan for this by saving extra money.

Legal protections and inspection contingencies buyers need

When you sign a rent-to-own agreement, you need strong legal protection. This is because these contracts are not like regular home purchases. They have fewer rules to follow.

These deals are different. The tenant gets to lease with the option to buy later. The seller agrees to sell the property after a set time. This unique setup needs special legal care.

Attorney Review Clauses Safeguarding Buyers

An attorney review clause is your first defense. It lets you have 3-5 business days to check the contract with a lawyer. This makes sure you understand it before it’s too late.

In Greenville last year, a couple found a big problem with their contract. They learned the seller wouldn’t fix major repairs during the lease. A $400 lawyer review saved them from thousands of dollars in unexpected costs.

Real-estate attorneys customarily add three-day review windows and contingency language, giving buyers legal leverage to renegotiate or exit if red flags emerge—an approach widely recommended by practitioners. Ref.: “Investopedia Team. (2024). Do You Need a Lawyer to Buy a House? Investopedia.” [!]

Getting a lawyer to review your contract costs $300-600. They will check:

- How much you pay for the option to buy

- How your rent payments add up to the purchase price

- Who is responsible for repairs during the lease

- What happens if you miss payments

- How the purchase price is figured out and when

Don’t skip this step, even if the seller wants you to. It’s your chance to make changes before you commit.

Home Inspection Rights Before Agreement Execution

Rent-to-own agreements should let you get a home inspection before you sign. This is because you’re not just renting. You might be buying this property.

A home inspection for rent-to-own costs $350-500. It checks:

- The foundation and structure

- The roof and how long it will last

- The HVAC system and its age

- The electrical system and any code issues

- The plumbing and water pressure

Your contract should let you back out or change terms if big problems are found. Make sure it says who fixes any issues found during the inspection.

One client found the HVAC was 15 years old. We got the seller to put $5,000 in escrow for a new HVAC if needed.

“Discover More: Basic lease agreement terms every renter must read”

Title Search and Lien Discovery Essentials

Getting a title search is a must before signing a rent-to-own deal. It shows if the seller can legally sell the property. It also checks for any liens that could stop you from getting clear title later.

A title report costs $75-200. It can find big problems like:

- Tax liens that need to be paid off

- Liens from contractors who weren’t paid

- Judgment liens against the owner

- Mortgage problems that could lead to foreclosure

- Easements or restrictions on the property

Make sure your contract says the seller must give you an updated title report every year. This way, you’ll know if new liens appear that could stop your purchase.

One family I worked with found $27,000 in IRS tax liens on their home. We made the seller clear the liens before they could buy, with a new title search to prove it.

Never sign a rent-to-own contract without fully understanding it. Get clear answers to these essential questions before committing to rent-to-own payments.

These legal protections are not just formalities. They are key to avoiding bad deals. With these three protections, buyers can take on rent-to-own with less risk.

“Further Reading: Low income home buyer grants and assistance programs”

Negotiating terms to fit limited budgets

First-time buyers on a tight budget can make their rent-to-own deal better. By negotiating key terms, they can fit their financial situation. Each part of the deal is important for success.

I’ve helped many with little money. The right way to talk can make a big difference. It can turn a good deal into a bad one.

Start by looking at the seven parts of a rent-to-own deal that can be changed. These parts can help fit your budget:

- Monthly rent amount – The rent can be changed by 5-10% from the start

- Rent premium percentage – The part of your rent that goes toward buying (usually 15-30%)

- Option fee size – The upfront payment to buy (usually 1-5% of the home price)

- Maintenance responsibilities – Who fixes things and at what cost

- Purchase price calculation – Fixed now or based on future value

- Lease duration – How long you have before you must buy

- Exit clauses – What if you can’t buy before the lease ends

Before talking to the seller, make a worksheet. It should have three columns: “ideal terms,” “acceptable terms,” and “walk-away terms.” This helps you make smart choices during talks. For example, if you can pay $1,500 a month, your ideal might be $1,350.

When talking about the option fee, think about trading things. If the seller wants $10,000 but you can only pay $6,000, offer to pay more rent each month. This way, you can pay less upfront but more over time.

| Negotiation Element | Standard Terms | Budget-Friendly Alternative | What to Say |

|---|---|---|---|

| Option Fee | 3-5% upfront | 1-2% upfront with higher monthly credits | “I can offer a smaller option fee with larger monthly credits toward purchase.” |

| Purchase Price | Fixed today | Today’s price with smaller annual increase | “Let’s set today’s price with a 1% annual increase instead of the standard 3%.” |

| Maintenance | Tenant handles all repairs | Seller covers repairs over $500 | “I’ll handle routine maintenance if you’ll cover major repairs exceeding $500.” |

When committing to rent a property with plans to buy, who fixes things is key. Sellers often want you to fix everything. But if you can’t afford big repairs, ask the seller to cover costs over $500.

The way the purchase price is figured out matters a lot. A fixed price is sure but might be higher. A price based on future value could save money but is riskier. For those watching their budget, a fixed price with a small increase each year is best.

Look out for unfair lease clauses when negotiating. Make sure you understand what happens if you miss a payment. Ask for grace periods and to keep some of your credits even if you don’t buy.

“Buying a quality storage building can cost thousands of dollars. RTO breaks that large expense into smaller, more manageable monthly payments. This structure, with affordable monthly payments, fits better into many household budgets than a single large cash pay transaction.”

This idea works for homes too. Rent-to-own makes a big upfront cost into smaller payments. But only if you negotiate well to fit your budget.

Good negotiation is about finding terms that work for both sides. Explain how your proposals help the seller while fitting your budget. For example, asking for a longer lease can help you improve your credit score. This makes the deal safer for the seller.

Focus on what matters most to you. If your problem is credit, ask for a longer lease. If you can’t afford a down payment, negotiate a higher rent premium. By focusing on your needs, you can create a lease purchase option agreement that’s a real step toward owning a home, not a financial burden.

“Read More: Rent to own home basics for budget constrained buyers”

Exit strategies if financial circumstances unexpectedly change

Life doesn’t always go as planned, which is true for rent-to-own deals. Having a plan to get out is key to keep your money safe on your way to owning a home.

Early purchase option exercise considerations

Think carefully before you decide to buy early. Check if you can afford it by adding up your rent credits and any home value increase. Remember, closing costs can be 2-5% of the home’s.

Make a plan to see when you can get a loan. FHA loans start at 580 credit, but you usually need 620+ for regular loans. Watch your credit score to find the best time to buy.

“Related Articles:

Assigning agreement or finding alternative financing options

If you can’t buy but have built up equity, think about assigning your deal to someone else. This means:

1. Check your contract for rules on assignment

2. Look for buyers through real estate agents

3. Talk about a fee that lets you keep some of your equity

If regular loans are hard to get, look at other options. Seller financing, loans from local banks, or programs for first-time buyers might be easier. They offer more flexibility than usual mortgages.

Talk openly with the property owner if money problems come up. Most contracts let you get out early without hurting your credit. This helps keep the equity you’ve built safe.

{kind=link}