Figuring out how to split your paycheck can be tricky. It’s like trying to find your way through a foggy harbor. We need a clear plan so each dollar goes to the right place.

Why do we risk getting lost if we skip a step? As of 2024, approximately 63% of Americans reported they could cover a $400 emergency expense using cash or its equivalent, indicating many live paycheck to paycheck.

“Money flows best when each dollar knows its job,” says a Maine credit-union director. I felt relieved when I divided my salary and tackled $80k debt.

For more insights, check this essential guide.

Quick hits

- Rank monthly needs with discipline.

- Set clear limits for wants.

- Automate savings from day one.

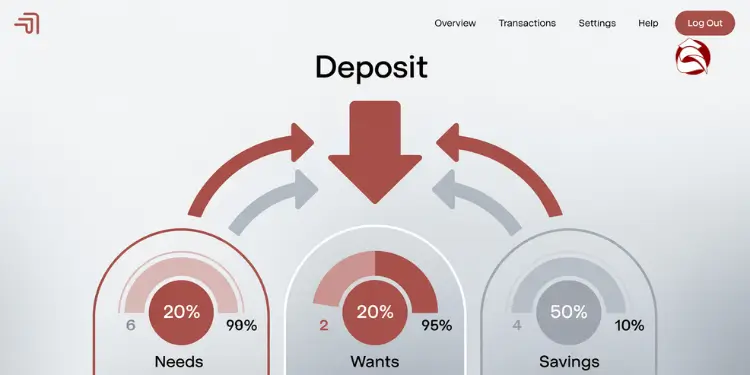

Split direct deposit into three main accounts

We envision a Maine fishing boat with three sturdy components. Each part gets a share of our paycheck. This way, we save for bills, treats, and the future.

We follow the 50/30/20 rule to manage our money. Half goes to needs, a part to wants, and a bit to savings. Automatic transfers help us stay on track.

Ask employer HR for multiple split options

Many HR offices let you split direct deposits into different banks. We just need to ask for the right form. This makes budgeting easier and helps us save.

Specify flat amounts or percentages precisely

Some like to save exact amounts for goals. Others save a certain percentage as income grows. Both ways keep us focused and protect our savings. Talking to HR for just five minutes can make a significant difference in these changes.

Allocate needs category percentage on payday morning

Tides roll into Portland Harbor whether we’re ready or not. Fixed bills come in, no matter our mood or when we get paid. Setting aside money for basics keeps our budget in order.

Studies show about half our income goes to rent, mortgage, utilities, and minimum debt. Paying for shelter first helps us stay grounded.

In 2023, U.S. households allocated 32.9% of expenditures to housing, 12.9% to food, and 17.0% to transportation—closely matching the 50/30/20 needs allocation benchmark. Ref.: “U.S. Department of Agriculture, Economic Research Service. (2024). Food expenditure series and household spending shares. USDA ERS.” [!]

Prioritize rent mortgage and utility drafts

We prioritize housing costs at the top of our list. Setting up automatic payments for rent, mortgage, and electricity helps avoid late fees and ensures timely payments. Scheduling them on payday morning helps us avoid extra charges.

We can adjust amounts based on 50/30/20 vs 60/20/20 budget ideas to make managing money easier.

Leave buffer for fluctuating grocery bill

Maine winters can make groceries more expensive. A small extra amount helps when prices go up. Skipping this buffer can leave us short on food.

Let’s take a few extra minutes to adjust direct deposits. This way, we can cover all our needs without last-minute worries.

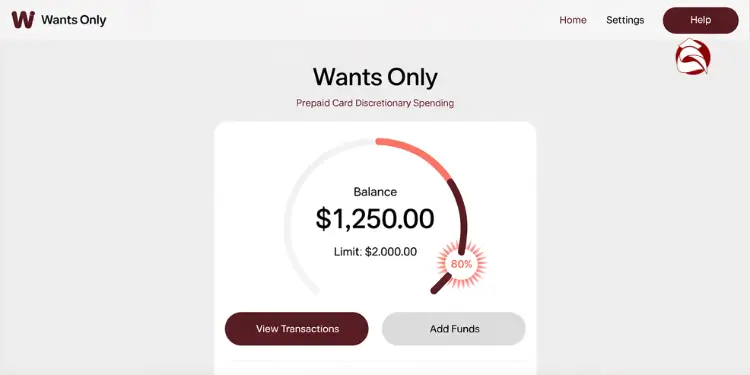

Distribute wants allotment using separate spending card

Allocating 30% of income to discretionary spending ensures enjoyment without compromising savings goals. A special card keeps us on track and stops us from spending too much.

Studies show we can cut down on impulse buys by a quarter. This is when we use a card just for fun money.

We can enjoy life’s little pleasures without touching our savings. This way, we keep our budget safe. Learn more about this idea in this guide.

Choose fee free prepaid or debit option

Smart choices include:

- Cards with no monthly fees to save money.

- Brands with local ATMs that don’t charge extra.

- Apps that show your balance in real-time.

This method keeps our spending in one place. It helps us stay disciplined and clear.

“Full Comparison: 50/30/20 vs 60/30/10 budgeting rules“

Receive instant alerts when limit approaches

Mobile alerts tell us when we’re near our spending limit. They’re like signals, reminding us to slow down. A quick pause can stop unexpected costs and keep our money flexible.

Take ten minutes to find a new card and set up alerts. This small action can bring peace to your budget soon.

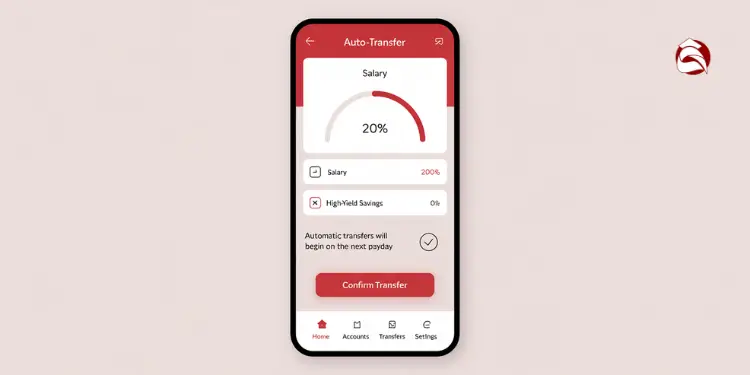

Route savings transfer immediately to high interest account

When we get our paycheck, we put a part of it into an account that earns more. According to the Federal Reserve’s 2024 report, 63% of Americans could cover a $400 emergency expense, highlighting the importance of automated high-yield savings transfers. This shows we need quick ways to save.

Using the 50/30/20 formula, we save at least one-fifth of our income. This helps us stay stable in the long run. The U.S. personal savings rate was 3.4% in June 2024. We cut this gap by moving money to a high-yield account fast, stopping us from spending too much.

Federal Reserve data show 37% of Americans lack enough cash to cover a $400 emergency expense, underscoring the importance of automated high-yield savings transfers. Ref.: “Federal Reserve Board. (2024). Report on the Economic Well-Being of U.S. Households in 2023. Federal Reserve.” [!]

Automate transfer within minutes of deposit

Transfers happen automatically. As soon as money comes in, some of it goes to savings. This stops us from buying things we don’t really need.

Select FDIC insured online bank partner

We choose an online bank with high rates and good tools. It’s FDIC-insured for safety. For more on automating transfers, see this guide.

“Compare Methods: Zero budgeting vs percentage budgeting deciding the better fit“

Nickname account to visualize specific goals

We name our savings account something like “Coastline Cabin Fund” or “Next Nest Egg”. This keeps us motivated. It reminds us why we can’t spend that money on impulse buys.

| Bank | Automation Feature | Approx. APY |

|---|---|---|

| Ally Bank | Multiple buckets for goals | 4.00% |

| SoFi | Round-up deposits | 3.75% |

| Capital One | High-yield savings | 3.40% |

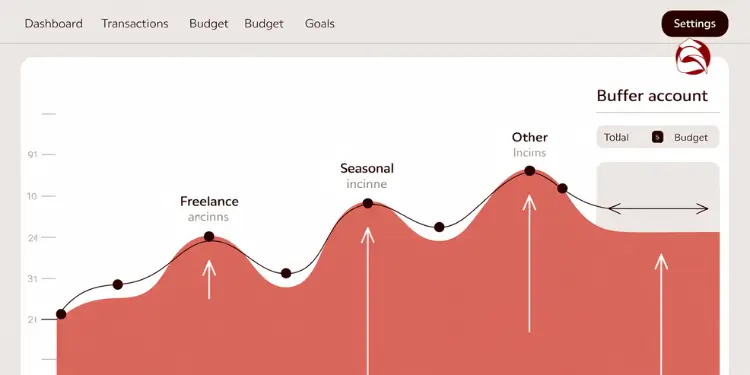

Handle irregular income and side gig payments

Unpredictable earnings can throw us off like a rogue wave. Jobs in Maine and weekend gigs cause cash flow issues. We stay afloat by saving a part of each deposit.

With 36% of employed Americans working independently, irregular income streams demand dedicated buffer accounts to smooth cash flow variability. Ref.: “Dua, A. et al. (2022). Freelance, Side Hustles, and Gigs: Many More Americans Have Become Independent Workers. McKinsey Global Institute.” [!]

“Quick Start: 50/30/20 budget basics for first time budgeters“

Hold percentage in buffer holding account

We save a percentage as soon as side gig money comes in. This builds a safety net for rent, food, or sudden repairs. The Bureau of Labor Statistics says freelance income is highest in summer (BLS, 2022).

| Side Hustle | Estimated Weekly Earnings | Payment Frequency |

|---|---|---|

| Freelance Writing | $200–$600 | Weekly or Monthly |

| Seasonal Lodging Staff | $300–$700 | Biweekly |

Reconcile totals monthly then distribute remainder

We check the buffer account balance, add up all deposits, and make sure we’ve paid taxes. Then, we put extra money into savings or to pay off debt.

- Look at bank statements on a set date.

- Track each gig’s net earnings and taxes withheld.

- Send extra money to a chosen goal.

Spend two minutes moving a part of side hustle cash to a buffer today.

“Deep Dive: 50/30/20 budget breakdown of needs, wants, and savings“

Track paycheck splits with budgeting automation tools

We’ve helped over a thousand families at Pine Coast Bank. They watch each deposit as soon as payday comes. This way, they see if rent takes too much from savings or if “Wants” grow too big.

A $3,000 monthly income means $900 for fun, hobbies, or new clothes. This helps keep our spending, savings, and wants in balance.

“Essential Guide: How to calculate 50/30/20 budget for your income“

Compare Top Apps Integrating Multiple Banks

We can see balances from different banks in one place. Some apps use color gauges for rent, food, and trips. This lets us adjust spending before the month ends.

Daily alerts help avoid surprise bills. They also push us to save more.

“Beginner’s Steps:

Use Spreadsheet Template for Granular Visibility

A simple spreadsheet tracks each category with direct deposit. We match each expense—like utilities and fun money—to see if we meet the 50-30-20 rule. The 50-30-20 budget calculator helps when income changes.

This one-page view helps us stay on track. It adapts to life’s changes, keeping our finances strong.

{kind=link}