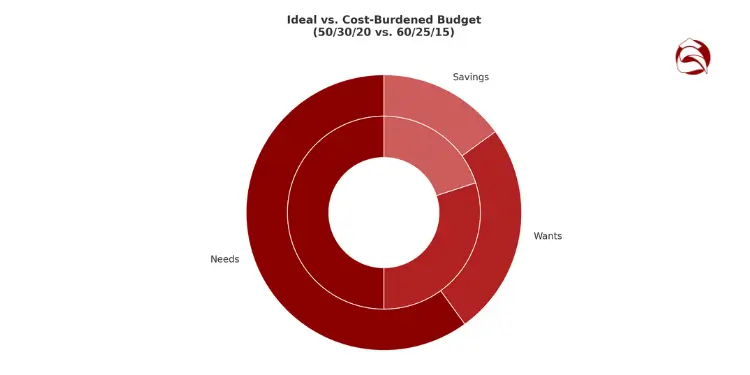

Learning to budget using the 50/30/20 rule helps keep your money safe. It makes sure you spend on needs, wants, and savings. This way, your money stays balanced.

A 2025 Bankrate poll shows that 42% of U.S. adults still skip formal budgeting, despite being regular budgeters. Report higher savings rates. However, a Federal Reserve study suggests that a reasonable budget helps you stay stable in the long term. I trimmed $80,000 of debt in three years by following the 50/30/20 rule and automating extra payments.

Want to see how families feel more secure with our 50/30/20 plan?

Quick hits

- Split your after-tax income into three parts.

- Use 50% for essential costs like rent and food.

- Spend 30% on things you enjoy.

- Save or pay off debt with 20%.

Identify take home income after deductions

Think of your net pay as a strong pier. We start by taking out taxes, health premiums, and retirement funds. This leaves you with your real take-home income.

The 2024 Federal Reserve SHED data show 33 % of workers have more than one income source. We’ll look at each income source carefully to keep your budget balanced.

Calculate average earnings on irregular pay

When pay changes from week to week, collect the last six months of pay stubs. Add up these amounts and divide by six. This method helps smooth out the ups and downs, so you don’t have to guess.

If you work in an office and also have seasonal jobs, add both incomes together. We aim for stability, even when things change.

Exclude bonuses and overtime windfalls

Big bonuses can make you think you can spend more than you can. A holiday bonus might feel like extra money, but it can make you overspend. Stick to regular income to know what you can really afford.

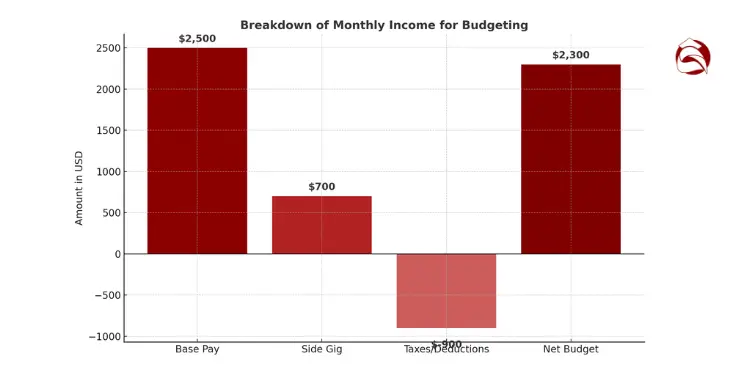

Check out a helpful 50/30/20 example. It shows how a family manages $1,950 in monthly wants on a $6,500 net income.

| Pay Source | Monthly Amount | Details |

|---|---|---|

| Base Pay | $2,500 | Stable salary after withholdings |

| Side Gig | $700 | Average from past six checks |

| Taxes/Deductions | -$900 | Federal, state, and coverage |

| Total Take-Home | $2,300 | Monthly net for budgeting |

Categorize needs, wants, and savings percentages

Sort every dollar into Needs, Wants or Savings buckets. We do the same with our money. We save for needs, wants, and future security. Maine families spend almost half their income on basics.

We’ll navigate these waters together by grouping must-have bills, smaller joys, and our savings slice. This last part is our safety net for unexpected costs. Our wishes include meals out, music, and quick trips. This budgeting plan suggests these wants should be 30% of our income.

List Mandatory Bills and Living Costs

Utilities, rent, and insurance are here. Heating in the north can be expensive. But we keep it affordable by watching our usage. These costs usually take up half of our monthly income.

Separate Discretionary Treats and Small Luxuries

Dinner spots, online services, and fun buys go here. We cut back on fun spending but remember we need it.

Define Short Term and Long Term Savings

Emergency funds, paying off debt, and retirement savings are here. High-interest debt needs a big part of our savings. Set a timer for 90 seconds and write down one goal for each savings goal. Let’s keep our savings safe for a smooth journey.

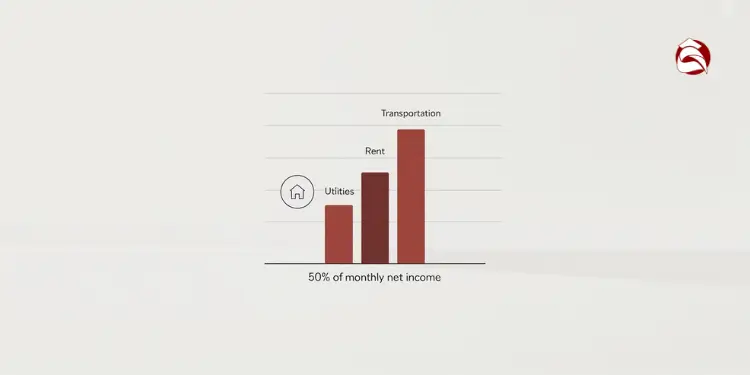

Apply 50 percent rule to necessities cost

Imagine a calm Portland harbor. Half of our boat’s cargo keeps us steady. We anchor our core needs like rent, utilities, and car expenses in this 50 percent slice.

According to MaineHousing.org, 36% of local households pay too much on housing. This can throw our ship off course. We aim to keep these costs in check.

MaineHousing’s 2025 Outlook shows 53.2 % of renter households earning $35k–$50k are cost-burdened (paying >30 % of income on rent), illustrating why some budgets must flex the “needs” share above 50 %.Ref.: “Maine State Housing Authority. (2025). Maine’s Housing Outlook 2025. MaineHousing.” [!]

Also See: 50/30/20 vs zero based budgeting which budget strategy fits you

Benchmark housing, utilities, transportation spending

First, list every monthly bill for shelter, heat, water, and commuting. Then compare that total with half of your take-home pay. If the percentage is too high, we adjust.

We might cut rent or mortgage by getting roommates or smaller apartments. Or, we could lower costs by carpooling or using public transit.

- Evaluate energy use, like turning off lights and unplugging devices.

- Renegotiate utility contracts for competitive rates.

- Explore budget-friendly maintenance plans for vehicles.

Adjust shared expenses with household partners

Coordinating expenses with loved ones needs clear communication. We split bills based on income or agreed shares. This way, no one gets caught in unexpected charges.

Take 10 minutes this week to make a fair plan. This ensures our shared journey stays balanced on stable financial currents.

Quick Guide: 50/30/20 vs 60/20/20 budget full comparison guide for you today

Allocate 30 percent toward flexible lifestyle choices

This part of our budget is for fun. It’s for that day trip to the Maine coast or your favorite streaming show. It helps us avoid burnout.

A report from the U.S. Bureau of Labor Statistics shows breaks help us work better. So, setting aside this money helps us enjoy life and stay balanced.

Budgets often say to use 30 percent for fun in the 50/30/20 framework. It shows we all need fun without forgetting our duties. We watch it closely to keep it separate from rent or mortgage.

Set personal fun money weekly allowance

We set aside a little each week for surprises. It could be local beers on Friday or an art class. Breaking it into weekly parts helps us stay on track.

There’s no worry about spending too much at the start of the month.

Prioritize experiences aligning with core values

We try to make our fun meaningful. Maybe it’s hiking in Acadia National Park or eating fresh lobster. It’s about spending on things that matter.

One study from the American Psychological Association says enjoying life makes us happy for longer. For tips on keeping to your budget, visit Faharas.net. Start small and see how it works.

Cornell research shows consumers gain more lasting happiness from experiential purchases (e.g., trips, classes) than from material goods—suggesting that directing part of the 30 % “fun” budget toward experiences maximizes well-being.Ref.: “Gilovich, T., Kumar, A. & Killingsworth, M. (2014). Doing makes you happier than owning – even before buying. Cornell Chronicle.” [!]

Related Topics: 50/30/20 budget calculator for quick planning and spending balance guide

Direct 20 percent into saving and debt goals

We stand together at this next financial channel. This final slice of the 50/30/20 rule ensures we lock in a steady future. By funneling 20 percent of our paychecks into savings and debt reduction, we stay on course for long-term calm. Learn more about the 50/30/20 rule and see how it keeps us anchored.

Think of it like heading into the harbor—no sharp turns, just clear direction. Some folks, earning $3,400 a month, place $680 toward debt paydown or emergency funds each payday. We’ll map these currents together, starting with a cushion.

Build emergency fund before investments start

A target of three months’ worth of living costs can lessen storms. We set aside a little each paycheck, trimming the sails on casual purchases until our emergency fund reaches a comfortable level. This buffer grants peace of mind.

The Federal Reserve’s 2024 SHED report shows only 63 % of adults could cover a $400 emergency with cash—leaving 37 % vulnerable—underscoring why the first 20 % slice of the 50/30/20 rule should fund an emergency buffer.Ref.: “Board of Governors of the Federal Reserve System. (2025). Economic Well-Being of U.S. Households in 2024. Federal Reserve.” [!]

Snowball high interest balances for momentum

Consider listing balances in ascending order or by highest rate. Pay extra on one until it’s gone, then roll those payments into the next. Quick wins energize us to tackle bigger totals.

Automate retirement contributions on payday

Automation spares us from guesswork. We route a set percentage into our 401(k) or IRA. That steady beam of retirement savings helps us stay on course, no matter the weather.

Vanguard’s How America Saves 2024 finds participant-weighted plan participation hits 94 % in auto-enrollment 401(k)s versus 67 % in voluntary plans—proving automation sharply boosts saving rates.Ref.: “Vanguard. (2024). How America Saves 2024. The Vanguard Group.” [!]

Read More: 50/30/20 budget basics every first time budgeter should know now

Automate transfers and monitor plan progress monthly

We’re like boat captains guiding our finances. We might get off track, but good habits and data keep us afloat. Dr. Nodin Laramie, CFP, cleared $80k of debt with a routine. Automated transfers help us stay calm.

Use separate sub accounts for clarity

Open “needs,” “savings,” and “fun” sub accounts at your bank. Auto-split your money each payday. This way, 50% goes to living, 30% for fun, and 20% for goals.

This makes your budget easy to see. Learn more in this 50/30/20 budget breakdown guide.

Fresh Insights:

Review category drift every three months

Regular checks prevent surprises. Maybe you spend more on groceries or a new subscription. Look at your spending and decide what to change.

Our monthly check is like scanning the harbor for dangers. It helps us avoid debt and stay on track for financial comfort in the United States.

{kind=link}