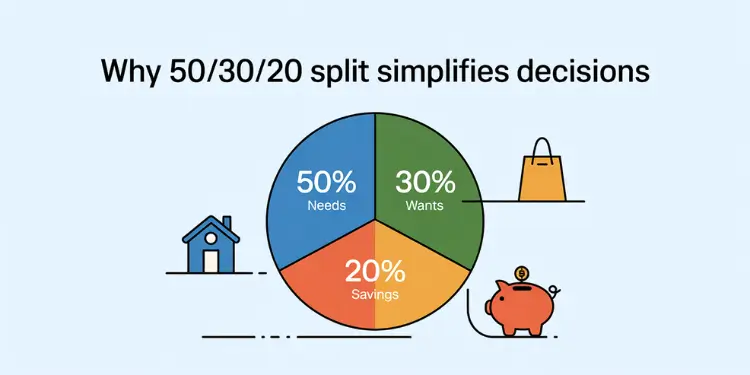

If you’re new to managing money, the 50/30/20 budget is key. It divides your after-tax income into three parts. These are needs, wants, and savings.

Budgeting & Saving is easier than you might think. Did you know 56% of Americans don’t have a $1,000 emergency fund?

Elizabeth Warren said, “A budget rule explained puts families at peace.” I paid off $80k of debt using the 50/30/20 method. Let’s explore it together.

Learn more at Budget Design Methods.

The 50/30/20 budget framework divides after-tax income into three fixed categories: 50 percent for essential expenses (housing, utilities, food), 30 percent for discretionary spending (entertainment, dining, non-essentials), and 20 percent for savings and debt repayment. This rule-based allocation reduces decision fatigue by prescribing clear percentage caps, requires minimal ongoing tracking, and accommodates integration with zero-based budgeting tools to ensure every dollar is assigned.

Implementing the 50/30/20 split streamlines financial planning by automating transfers or envelope allocations, which mitigates overspending risk and fosters consistency. The model remains adaptable—households in high-cost areas can recalibrate ratios (e.g., 60/20/20) or adjust savings rates seasonally—while maintaining its core principle of balancing needs, wants, and long-term goals.

Key Takeaways:

- Splits income into three distinct categories.

- Caps spending on needs, wants, savings.

- Requires minimal weekly tracking effort.

- Automates allocations to savings and debt.

- Reduces decision fatigue in budget planning.

- Adapts ratios for varying cost structures.

Why 50/30/20 split simplifies decisions

Imagine a lobster trap guiding the catch. This budget idea helps us manage money well. We split our income into three parts: needs, wants, and savings.

This makes budgeting easy. It helps us avoid spending too much.

In high-cost living areas, basic needs often exceed 50% of income, making the standard 50/30/20 split impractical; some households adjust to 60/20/20 or 70/15/15 models Ref.: “Not Ordinary Blogger. (2025). When the 50-30-20 Rule Isn’t the Best Saving Strategy — and What to Do Instead. NotOrdinaryBlogger.com.” [!]

Automatic caps reduce overspending risk

Setting limits on each part of our budget protects it. This way, we focus on our financial goals. It keeps us from getting into debt.

Using a zero-based budget helps us track every dollar. We set aside money for bills, fun, and savings. This builds a steady pace towards our goals.

The 50/30/20 rule is endorsed by financial leaders like Goldman Sachs for its straightforward framework and broad applicability Ref.: “Goldman Sachs Bank USA. (2024). The 50-30-20 Rule and Other Budgeting Methods. Marcus by Goldman Sachs®.” [!]

Clear categories curb budget fatigue

Handling our income is easier when we divide it by percentage. This method avoids confusion. It helps us know what to spend on and save.

This approach keeps us on track. It encourages better spending habits.

Quick math saves setup time

Many want a simple way to budget. The 50/30/20 rule makes it fast. It cuts down on guesswork and lets us plan quickly.

It helps us shop, pay bills, and save money confidently. Check this approach to see how it works. In minutes, we have a budget that fits our life and helps us succeed.

Read More:

Improving cash flow visibility each month

We’ll track where our money goes every month. A simple dashboard shows how much money goes into our accounts. We aim to save for emergencies and pay off debt.

Keeping track helps us adjust our spending. It’s hard to balance student loans and daily needs. But seeing our money on one screen makes it easier to save.

Tracking needs wants savings in dashboard

We use a budget calculator to check our spending. It helps us see if we spend too much on wants. Tracking needs helps us know what’s essential.

One study found 30% of our budget goes to non-essentials. This makes it easier to cut back on spending.

“Families who track detailed expenses catch trouble spots early and maintain greater peace of mind,” said a local credit union partner.

Spotting leaks before debt snowballs

Hidden expenses can add up quickly. Watching for utility increases and extra subscriptions is key. If you notice a rise, move money to savings or adjust your budget.

Learn how to set monthly limits by visiting this guide. It helps you save instead of scrambling later.

Strengthening habit with percentage automation

Imagine sailing with the wind behind you. That’s what happens when you automate your money management. A recent study found 65% of Americans forget their spending from last month.

So, saving for emergencies or planning expenses can be easy to forget. But, we can help you stay on track.

Automatic enrollment and default auto-escalation in retirement plans raise annual net savings rates by 0.5%–0.7% of income Ref.: “Choi, J., Laibson, D., Cammarota, J., & Beshears, J. (2023). Do Automatic Savings Policies Actually Increase Savings? NBER.” [!]

Using paycheck splits for effortless allocation

We’ll split your after-tax income into three parts from the start. This makes budgeting easy, whether you’re new or paying off debt. Some people save for wants, needs, and future goals.

By setting up direct deposits, you’ll have a built-in budget. It’s like having a budgeting template.

Leveraging banking rules to lock savings

We make saving automatic by putting part of your paycheck into savings. This helps you avoid spending too much. It also encourages saving for retirement.

Tools like this guide suggest using automatic transfers. Another resource shows budgeting apps can help reach big goals.

We’ll plan your money so each deposit helps pay off debt. Just set a reminder and choose which account to use. Spend a few minutes picking the right percentages.

Balancing lifestyle flexibility and financial goals

Imagine a harbor where we adjust sails for changing winds. This budget helps us live freely while keeping our finances stable. We’ll guide your money to different places, making sure each dollar has its own path.

One study found 40% of Mainers spend half their budget on fun things. This can lead to big bills later. But, finding a balance can bring peace.

We want to watch your spending and save for the future. Some money goes for needs, and 20% for extras. You can spend 30% on small treats if it helps you save.

This leaves 20% for safe savings. Each part of your money goes toward things you want, without hurting your future.

Allowing guilt free spending percentage

Some things make us happy. Setting aside a bit for fun lets us enjoy life more. It keeps us from feeling trapped.

Preventing burnout through fun money

Small rewards keep us going for big goals. Give yourself time to relax or travel. The right mix keeps your energy up.

| Wants Category | Typical Monthly Range |

|---|---|

| Restaurant Meals | $60–$120 |

| Entertainment (Netflix, Spotify) | $15–$25 |

| Non-Essential Shopping | $50–$90 |

| Vacations & Travel | $100–$200 |

| Hobbies & Recreation | $40–$80 |

Want to learn more about this budget method? Check out this budget overview. It shows how to enjoy fun times without forgetting your goals.

Adapting the rule for irregular income

We’ve seen many ups and downs with people who have side jobs or seasonal work. This simple rule works well when we adjust it to fit our income and spending. We keep track of what we need and want, and change our savings rate as needed.

The 50/30/20 framework assumes stable earnings and may not fit those with variable income, such as freelancers and gig workers Ref.: “Nut & Meg. (2024). The 50/30/20 Rule: Simple Budgeting for Every Household. Nut & Meg.” [!]

Seasonal side hustle income tweaks

Busy months are like catching lots of lobster. We save more during these times. If we make more money, we save more or pay off debt faster. Slow months mean we save less and focus on what we really need.

Building buffer fund during lean months

We save some money in a special fund when we can. This fund helps when our income drops or costs go up. It keeps us going and helps us reach our goals. For more tips, check out this breakdown.

{kind=link}