Finding the right percentage-based budgeting method is like searching for the perfect recipe. It must match your financial taste and lifestyle.

As of April 2025, the U.S. personal saving rate stands at 4.9%, still below the long-term average of 8.4%, signaling continued difficulty for many Americans to build savings.

“The best budget isn’t what experts say,” my financial advisor once told me. “It’s the one you’ll stick with.” This advice changed how I manage money.

When I started organizing my finances, I felt lost. But then I found dividing my income by percentages worked well. It gave me structure without the stress of tracking every penny.

Today, we compare two ways to split your monthly income. We look at the 50/30/20 rule and the 70/20/10 rule. The 70/20/10 rule is detailed in this article and is seen as more realistic by many.

The 70/20/10 budgeting model allocates 70 % of take‑home pay to all expenses, 20 % to savings/investments, and 10 % to debt repayment or giving—offering a deliberately simplified yet flexible structure. Ref.: “What Is the 70‑20‑10 Budget? – Clever Girl Finance.” [!]

By the end of this guide, you’ll know:

- How each budgeting method works with your after-tax income

- Which approach fits your financial situation better

- How to start your chosen budget right away

- How to adjust percentages for your financial goals

Origins and goals of each allocation model

The 50/30/20 and 70/20/10 budget models came from different times. They were made to solve money problems in different ways. Each one helps balance today’s needs with tomorrow’s dreams, but they started in different places.

The 50/30/20 rule started in formal money lessons. U.S. Senator Elizabeth Warren and her daughter Amelia Warren Tyagi wrote about it in 2005. They wanted a simple way to budget without getting lost in details.

Warren’s plan splits after-tax money into three parts: 50% for must-haves, 30% for fun, and 20% for saving. This has helped many middle-income families stay financially stable. It works well for those with steady jobs and not too much debt.

“The 50-30-20 rule is intended to help individuals manage their after-tax income, mainly for emergencies and retirement savings.”

The 50/30/20 rule is all about balance. It lets you enjoy life while working on your money goals. The 20% for savings and emergencies helps you move closer to financial security.

The 70/20/10 budget came from real life. It’s not from a famous money expert. It started because housing costs went up and wages stayed the same. It shows that many people need to spend more on basics just to survive.

Experts note that the 70/20/10 rule emerged largely as an adaptation to rising living costs, combining both essential and discretionary spending into one broader “living expenses” category. Ref.: “Where the 70/20/10 Budget Shines, And When it Falls Short – The Ways To Wealth.” [!]

The 70/20/10 plan assigns 70% to all living expenses (needs and wants), 20% to savings or investments, and 10% to debt or charitable giving. It shows that for many, living costs take up more of their income.

| Budget Model | Necessities | Discretionary | Savings | Best For |

|---|---|---|---|---|

| 50/30/20 | 50% | 30% | 20% | Moderate income, stable expenses |

| 70/20/10 | 70% | 20% | 10% | High cost areas, lower incomes |

| Difference | +20% | -10% | -10% | Practical adaptation to reality |

Both models aim to make money management easier. The main difference is how they balance today’s needs with tomorrow’s goals. The 50/30/20 rule is better for those with more money to save.

The 70/20/10 model is more realistic for those in expensive places or with less money. It says you might need to spend more on basics. Saving 10% is a start, but it’s better than not saving at all.

What’s great about these models is how simple they are. They’re not like complicated systems that track many things. These simple rules help make choosing how to spend money easier.

These models show how budgeting changes with the economy. Warren’s plan was for stable times, while the 70/20/10 came when housing costs rose too fast.

Choosing either model helps build good money habits. It’s about controlling what you must spend, not spending too much on fun, and saving for the future.

“You Might Also Like: 50/30/20 budget breakdown of needs, wants, and savings“

50/30/20 vs 70/20/10 Budgeting Side-by-Side

Let’s look at how each dollar is spent in two popular budgeting ways. These methods show big differences in what people value and how they manage money. They help organize your money into clear groups, but they do it in different ways.

Each system has its own way of dividing your paycheck. The 50/30/20 method puts half your money into needs, a third into wants, and one-fifth into savings. The 70/20/10 method, on the other hand, puts more money into needs and less into wants and savings.

| Category | 50/30/20 Budget | 70/20/10 Budget | Key Difference |

|---|---|---|---|

| Necessities | 50% of income | 70% of income | +20% for essentials |

| Discretionary | 30% of income | 20% of income | -10% for wants |

| Savings/Debt | 20% of income | 10% of income | -10% for financial future |

| Monthly Example ($5,000) | $2,500/$1,500/$1,000 | $3,500/$1,000/$500 | $1,000 shift to necessities |

How Each Budget Handles Fixed Costs

The biggest difference is how each method handles fixed monthly costs. The 50/30/20 rule limits your needs to half your income. This makes you spend more carefully on essential things.

With the 50/30/20 method, your needs bucket must cover all these fixed expenses:

- Housing (rent or mortgage payments)

- Utilities (electricity, water, gas, internet)

- Groceries and essential food

- Transportation (car payment, insurance, gas, public transit)

- Healthcare (insurance premiums, regular medications)

- Minimum debt payments

This 50% cap works well in areas with moderate living costs. But in high-cost places like New York or San Francisco, it’s hard to stay under 50%. Housing alone can take 40-45% of your income.

The 70/20/10 method offers a more realistic approach. It lets you allocate 70% of your income to needs. This acknowledges the high cost of housing, childcare, and healthcare. The extra 20% helps families cover basic living costs.

Choosing between these methods means understanding what you can afford. List all your fixed expenses first. Then decide which percentage split fits your needs better.

“Discover More: Should I use 50/30/20 budget or another budgeting method“

Comparing Fun Money Freedom in Each Budget

How you spend your “fun money” shows a big difference between these methods. The 50/30/20 method gives you 30% of your income for non-essentials. This is money for dining out, entertainment, hobbies, travel, and small luxuries.

For someone earning $5,000 monthly after taxes, that’s $1,500 for wants. This big discretionary budget lets you enjoy life while staying financially disciplined. You can have that daily coffee, subscribe to streaming services, and go out regularly without ruining your finances.

The 70/20/10 approach cuts your discretionary spending to 20% of your income. With the same $5,000 example, your wants budget drops to $1,000 monthly. This is a $500 difference that makes you think harder about what you really want.

People adapt to this tighter budget by:

- Prioritizing experiences over material possessions

- Choosing free or low-cost entertainment

- Being more selective about impulse buys

- Focusing on hobbies that bring the most joy

- Using the cash envelope system to avoid overspending

The key to success is knowing what’s a need and what’s a want. That gym membership? Unless your doctor says so, it’s a want. Premium cable? Definitely a want. By knowing where your money goes, you can spend more wisely.

Remember, the goal is not to deprive yourself but to spend on what truly adds value to your life. Both budgeting methods can help you do this. They just offer different balances between enjoying now and securing your future.

| Spending Category | 50/30/20 Approach | 70/20/10 Approach | Best For |

|---|---|---|---|

| Dining Out | More freedom ($300-400/month) | More limited ($200-250/month) | 50/30/20 offers more flexibility |

| Entertainment | Multiple subscriptions, events | Selective choices, fewer options | 50/30/20 for entertainment lovers |

| Shopping | Regular non-essential purchases | More thoughtful, occasional treats | 70/20/10 encourages mindfulness |

| Travel/Hobbies | Larger budget for passions | Requires more saving/planning | Depends on personal priorities |

“Further Reading: Zero budgeting vs percentage budgeting deciding the better fit“

How Budget Percentages Impact Long-Term Savings

Choosing to save 10% or 20% can change your future a lot. It might seem like a small choice now. But it can really affect your financial security later on.

If you make $60,000 a year after taxes, saving 20% means setting aside $12,000 each year. Saving 10% means setting aside only $6,000. That’s half as much saved each year.

Over time, this difference grows a lot. Let’s say you get a 5% return on your investment. Here’s what happens:

| Budget Method | Annual Savings | 5-Year Total | 10-Year Total | Growth Difference |

|---|---|---|---|---|

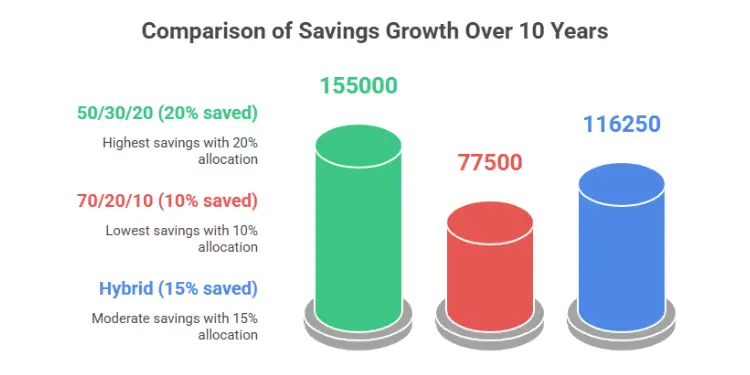

| 50/30/20 (20% saved) | $12,000 | $69,600 | $155,000 | +$77,500 |

| 70/20/10 (10% saved) | $6,000 | $34,800 | $77,500 | – |

| Hybrid (15% saved) | $9,000 | $52,200 | $116,250 | +$38,750 |

After 10 years, saving 20% can mean having about $155,000. Saving 10% means having only $77,500. That’s a big difference of $77,500! This gap grows every year because of compound interest.

Saving 20% instead of 10%, assuming a 5% annual return, can lead to $77,500 more after 10 years—highlighting the compounding advantage of higher savings rates. Ref.: “6 Steps to Becoming a Millionaire – Investopedia.” [!]

More savings means you can handle unexpected costs better. This gives you peace of mind. It’s hard to measure, but it’s very valuable.

For big goals like buying a house or retiring, saving 20% helps you reach them faster. You’ll get there months or years sooner than with saving 10%.

But even saving 10% is better than the

Recent data shows savings at 4.9% in April 2025 a modest rise from recent lows but still below historical norms. Americans save very little. So, 10% is a big step up.

In my experience helping families manage their money, I’ve seen many shift their savings strategies as their income grows. They start with 70/20/10 and then move to 60/25/15 and 50/30/20 as they make more money or pay off debt.

If saving 20% is hard right now, don’t worry. Start with what you can, even if it’s just 5%. The goal is to save regularly and increase your savings over time.

Remember, saving is not just for fun later. It’s about having options and security for your future. Every extra percentage point you save grows your money faster through compound growth.

“The best time to plant a tree was 20 years ago. The second best time is now.” This old proverb applies perfectly to saving money – start where you can, but start today.

For those with irregular income, save a percentage of each paycheck. This way, your savings adjust with your income each month. It makes saving easier during tough times.

How much you save shows your commitment to financial freedom. Whether it’s 10%, 20%, or something in between, saving regularly helps you reach all your financial goals.

“Read More: What is Zero Based Budgeting“

Budgeting Tips for Irregular or Freelance Income

When your income goes up and down like a roller coaster, budgeting is harder. I learned this when I was freelancing before Fahras. You need to adjust the 50/30/20 and 70/20/10 methods to fit your income.

First, calculate your average monthly income using at least six months of earnings to smooth out fluctuations. This average helps you decide how to split your money.

When you make more money than usual, spend normally. But save most of the extra money.

Freelancers and those with variable income should try a three-tier approach:

- High-income months: Use a 40/20/40 split (40% needs, 20% wants, 40% savings) to save more

- Average months: Stick to your chosen method (50/30/20 or 70/20/10)

- Low-income months: Use 80/10/10 or 90/5/5, using savings if needed

What you spend on fixed costs like rent and utilities helps decide your budget. If these costs are high, the 70/20/10 method might be better. Freelancers with lower costs might prefer the 50/30/20 method for saving more.

Automating savings is key for variable income. Set up automatic transfers to your savings when you can. This helps you save without spending extra money.

“Related Topics: 50/30/20 vs zero based budgeting complete comparison guide“

Building a Savings Buffer for Variable Income

Building a buffer is important, no matter your budget method. The 50/30/20 method already saves 20%, which helps build reserves. For variable income, save 10% of your income in a special fund.

This buffer is meant to smooth monthly cash flow and is separate from an emergency fund meant for true crises. Once it covers 3-6 months of expenses, you can save more for long-term goals.

The 70/20/10 method has less for savings. You need to plan carefully. Here’s how to split your money:

| Income Period | Needs | Wants | Savings | Buffer Strategy |

|---|---|---|---|---|

| High Income | 70% | 10% | 20% | Double savings rate temporarily |

| Average Income | 70% | 20% | 10% | Split savings: 5% buffer, 5% long-term |

| Low Income | 80% | 10% | 10% | Use buffer funds if needed |

Use your buffer only when really needed. I suggest using it when your income drops 20% or more. This keeps your savings safe for emergencies.

Zero-based budgeting works well with variable income. It means every dollar has a job. This helps avoid spending too much in good months. Many apps now help with variable income.

If you have credit card debt, adjust your budget to pay it off faster. Use 15-20% of your high-income months for debt. This will help you get out of debt quicker.

Remember, these are just guidelines. The goal is to be financially stable and reach your goals. Adjust your budget based on your unique situation.

“Read More: 50/30/20 vs 80/20 rule detailed comparison guide“

Long-Term Pros and Cons of 50/30/20 vs 70/20/10

Any budgeting system is tested over years, not just months. I’ve helped many families with percentage-based budgeting. I’ve seen patterns in how each method works over time.

The 50/30/20 method is great for long-term money health. It saves 20% for savings and debt, helping you grow wealth and prepare for emergencies. Clients often build big emergency funds in 18 months, feeling safer than before.

This high savings rate also helps pay down debt fast. One client paid off $24,000 in credit card debt in two years. After paying off debt, they use that 20% to grow their wealth.

The 30% “wants” category in 50/30/20 also helps. It stops you from feeling too deprived. This way, you’re more likely to stick with your budget because you have room for fun.

But, 50/30/20 can be tough in expensive places. Housing and basic needs can take up more than 50% of income. Families in San Francisco and New York often struggle to stay under 65% without big lifestyle changes.

“I tried forcing our family into the 50/30/20 model for six months, but with Bay Area housing costs, we were constantly stressed and felt like failures. Switching to 70/20/10 brought immediate relief and we actually stuck with it.”

The 70/20/10 method works well in high-cost areas. It lets you keep more money for essentials, reducing stress. It’s good for those with big fixed costs like housing or childcare.

But, 70/20/10 saves less, slowing down your financial growth. You might face more unexpected costs and need to work longer for retirement.

Often, the best budgeting method changes as your finances do. Many start with 70/20/10, then move to 60/25/15 or 50/30/20 as they earn more or pay off debt.

| Budget Model | Long-Term Strengths | Long-Term Challenges | Best For |

|---|---|---|---|

| 50/30/20 | Faster wealth building, stronger emergency fund, balanced lifestyle | Difficult in high-cost areas, may require lifestyle downsizing | Moderate cost-of-living areas, debt reduction focus |

| 70/20/10 | Less daily budget stress, accommodates higher fixed costs | Slower progress to financial goals, less emergency capacity | High cost-of-living areas, early career stages |

| Evolving Approach | Adapts to changing circumstances, grows with your journey | Requires regular reassessment, adjustment periods | Long-term financial growth, changing life stages |

The key to lasting success is not sticking to one plan but making steady progress. Your budget should grow with you. Many use budgeting apps to track and adjust as needed.

Remember, these are tools, not strict rules. The best plan is one you can keep up with and reach your financial goals. Sometimes, starting with 70/20/10 and moving to 50/30/20 is the best way to go.

How to Choose the Right Budget Ratio for Your Goals

I’ve learned that the right budget split depends on your life. Your budget should match your current situation, not just follow a formula.

Financial experts emphasize that no single budget rule fits all—adaptation based on income, goals, and cost of living improves adherence and outcomes. Ref.: “How the 70/20/10 Budget Rule Works | U.S. News.” [!]

If you’re fighting debt hard, the 50/30/20 rule helps. It lets you save 20% for savings and extra payments. This is great for saving for a house or growing your retirement.

In expensive cities, the 70/20/10 rule is better. It gives you room to breathe. You save 20% for the future and enjoy 10% of your income.

Your income level also plays a part. If you earn more, 50/30/20 might work for you. But if money is tight, you might need to save 70% for basics first.

The key is to start with a method that feels right. Then, track your spending for two months and tweak as needed. You might end up with 55/25/20 or 65/15/20. What’s important is saving regularly and enjoying life too.

Remember, these are just guidelines. The best budget is one you can stick to every month. It helps you build the future you dream of.

{kind=link}