The 50/30/20 budget is easy to follow and can change how teens handle money. It splits income into three parts. This makes planning finances simple, even without using spreadsheets.

Did you know 70% of teens worry about money? A 2023 survey found only one in three teens learn about money in school. Most have to figure it out by themselves.

Elizabeth Warren created this budget. She said, “A budget tells your money where to go instead of wondering where it went.” Teens who use this budget feel more confident with money years before others.

Unlike old-school budgets, the 50/30/20 method is flexible yet structured. It’s based on simple math. You just split your income into needs, wants, and savings.

Quick hits:

- Works with any income amount

- Requires only basic math skills

- Builds lifelong financial discipline

- Adapts as circumstances change

- Prepares for financial independence

Get a notebook or open your notes app. You’ll want to write down these percentages as we dive into each part.

Understand income sources like allowance or jobs

The first step in mastering the 50/30/20 budget as a teen is identifying and recording all your income streams. Unlike adults with steady paychecks, your money likely comes from various sources at irregular intervals. This makes tracking very important for teen budgeting success.

Most teens receive money from multiple channels. You might get a weekly allowance from parents, earn from a part-time job, or collect cash gifts during holidays. Some of you might babysit, mow lawns, or sell items online. Each dollar counts when creating a budget that works for your lifestyle.

“The habit of tracking every dollar you earn now will build financial literacy skills that benefit you for decades to come.”

I once made the mistake of ignoring small income sources when I was a teen. Those $5 birthday cards from grandma and $10 for helping neighbors with chores seemed too minor to track. By year’s end, I realized I’d missed recording over $300 – money that could have grown in savings!

Record Every Dollar From Gifts or Gigs

Developing strong money habits starts with awareness. When you keep a record of all incoming cash, you gain a clear picture of your financial reality. This awareness becomes the foundation for all your future money decisions.

Start by listing every way you receive money. Include regular sources like allowance and part-time work, plus occasional windfalls like birthday money or one-time gigs. Here’s a simple way to categorize your income:

- Regular income: Allowance, part-time job paychecks, weekly chores

- Occasional income: Babysitting, lawn mowing, seasonal work

- Gift money: Birthday, holidays, graduation, achievements

- Unexpected money: Contest winnings, rebates, refunds

Nearly 70 % of U.S. teens say financial worries influence their education plans, underscoring why early budgeting skills matter. Ref.: “Junior Achievement & Citizens (2023). 2023 JA Teens & Personal Finance Survey. Junior Achievement USA.” [!]

The key is recording everything immediately. Got $20 for watching your neighbor’s dog? Write it down before that bill disappears into your pocket. Received $50 from grandma? Log it before spending a cent.

Many teens find that money slips through their fingers because they never truly knew how much they had to begin with. When figuring out how much you earn monthly, include everything – even small amounts add up quickly.

Create Simple Spreadsheet for Income Tracking

You don’t need fancy tools to track your income effectively. A basic spreadsheet or even a notebook can work perfectly as you build this habit. The important part is consistency, not complexity.

For tech-savvy teens, a simple spreadsheet offers the advantage of automatic calculations. You can create one using free tools like Google Sheets or Microsoft Excel. Here’s a basic structure to get you started:

| Date | Source | Amount | Category | Notes |

|---|---|---|---|---|

| May 1 | Allowance | $25 | Regular | Weekly payment |

| May 5 | Babysitting | $40 | Occasional | 4 hours for neighbors |

| May 12 | Birthday gift | $75 | Gift | From Aunt Sarah |

| May 15 | Part-time job | $120 | Regular | Weekend shifts |

If you prefer pen and paper, dedicate a small notebook exclusively to income tracking. The physical act of writing down earnings can make the money feel more real and help you think twice before spending.

When your income fluctuates month to month, calculate a three-month average to use for planning your spending. This gives you a more realistic baseline for your budget calculations.

Only 26.3 % of U.S. public-high-school students are guaranteed a personal-finance course, so most teens must master budgeting without formal classroom support. Ref.: “Next Gen Personal Finance (2024). State of Financial Education Report. NGPF.” [!]

One common challenge is forgetting to record cash transactions. Set a weekly reminder on your phone to update your tracker. Sunday evenings work well for many teens – just five minutes of maintenance can keep your system running smoothly.

“The most effective budget tracker is the one you’ll actually use consistently. Choose a method that fits your lifestyle and stick with it.”

For those who prefer digital solutions, several free apps are designed for teen budgeting. These can sync across devices and send helpful reminders when you haven’t logged income for several days.

Remember that tracking is just the first part of budgeting. Once you know how much money comes in, you can make informed decisions about how to divide it using the 50/30/20 rule. This foundation makes the rest of your budget plan your spending much easier to implement.

Before moving to the next section, take action now: List all your income sources from the past month and calculate your average monthly income. This number becomes your starting point for applying the 50/30/20 budget framework.

Allocate 50 percent toward must-have school needs

The biggest part of your budget is for things you really need. This is 50 percent of your money. For teens, this means school stuff and daily needs.

As a teen, your needs are about school and everyday life. You can’t skip these to do well in school. Learning to budget is a big skill.

What’s a necessity? It’s things for school and daily life. This includes school supplies, how you get to school, and food.

Budget Supplies Snacks Transport Pass Costs

School supplies are a big part of your budget. Figure out how much you spend on them each month. This way, you won’t run out when you need it.

Getting to school costs money too. It might be bus passes or gas. A monthly pass can be $30-60, which is a lot for a teen.

Food is also a need. If you buy lunch or snacks, keep track of how much. A school lunch is $3-5 a day, which is $60-100 a month.

Deciding what’s a need can be hard. Ask if you really need something. A basic notebook is a need, but a fancy one is a want.

“The hardest part of budgeting isn’t math—it’s being honest with yourself about needs versus wants.”

To figure out your needs budget, multiply your monthly income by 0.5. For example, if you make $200, your needs budget is $100. Then, list all your must-haves to see if they fit.

- School supplies: $20/month

- Transportation: $40/month

- Lunch money: $30/month

- Phone bill contribution: $10/month

Friends might say you need expensive things. But, being smart with money now helps you later. Waiting to buy expensive items is good for your money skills.

Plan for big expenses like science fair projects. If you need $50 in three months, save $17 monthly. This avoids last-minute money problems.

Try this: Take your monthly income and find 50% of it. List your must-haves. If they cost more than that, think about what you can cut back on.

Assign 30 percent for hobbies and social outings

The wants category is 30% of your teen budget. It’s for hobbies and social activities. This part of your money is for things that make you happy but aren’t needed to live.

When I was a teen, I spent all my money on weekend fun. The 30% rule would have helped me save money. It lets you spend on fun but keeps spending in check.

For most teens, “wants” include video games, movie tickets, and trendy clothes. It also includes streaming services and snacks with friends. Knowing the difference between needs and wants is key.

Different budget methods might change these numbers. But the idea is the same: enjoy today while saving for tomorrow.

Plan Low-Cost Hangouts Like Park Days

Having fun with friends doesn’t have to cost a lot. Budget-friendly activities are often the most fun. Instead of expensive outings, try these:

- Host a potluck movie night where everyone brings a snack

- Plan a park picnic with games

- Take advantage of free community events

- Explore student discounts at local attractions

- Organize a game tournament at someone’s home

Last summer, I helped my nephew have a backyard camping night. They made s’mores and told stories. It was cheaper than going to the movies. The cost? Less than $10 per person.

When friends want you to spend too much, try these ideas: “I’m saving for something big, but let’s go to the park instead.” Or, “Let’s find something free to do, like a concert downtown.”

Setting short-term goals for your wants budget helps you focus. Maybe you’re saving for concert tickets or a new game. Tracking your short term savings in your 30% makes it more rewarding.

Here are ways to stretch your wants budget:

- Look for student discounts everywhere you go

- Plan activities around sales and promotions

- Share subscriptions with family members

- Wait 48 hours before making impulse purchases

- Use cash instead of cards to feel the spending more directly

Remember, budgeting is about making choices, not restrictions. The 30% category lets you have fun while learning to manage money.

Learning to enjoy life while living within your means is one of the most valuable skills you can develop as a teenager.

Want to try something practical? List your five favorite activities with friends. Then, think of ways to do them without breaking the bank. This simple step makes budgeting real.

| Activity Type | Typical Cost | Budget-Friendly Alternative | Potential Savings |

|---|---|---|---|

| Eating Out | $15-25 per person | Potluck meal at home | $10-20 per person |

| Movies | $12-15 ticket + snacks | Movie night with streaming service | $8-12 per person |

| Shopping Trip | $30-50+ for clothes/items | Thrift store treasure hunt | $15-40 per trip |

| Gaming | $60 for new release | Game swap with friends | $40-60 per game |

| Sports Event | $25-40 for ticket | Playing the sport at local park | $20-35 per event |

Save 20 percent toward future education expenses

Learning to save 20% of your income as a teen is very important. It helps you for many years. This part of the 50/30/20 budget might seem boring, but it’s where the magic happens.

Adults often save this 20% for retirement. But teens can save for things they need now. This helps them learn good money habits.

The power of starting early is huge. Saving as a teen means you get to use compound interest. This is like money making more money for you while you sleep or have fun.

Think about this: saving $20 a week from age 15 could mean over $12,000 by age 25. But if you start saving at 25, you won’t have as much by 35. Starting early means more money over time.

Starting to save in your teens harnesses compound growth—“the power of compound interest can drive life-changing results over long periods of time.” Ref.: “Schock, L. (2025). Ten Building Blocks to Building Wealth. U.S. Securities and Exchange Commission.” [!]

“Further Exploration: 50/30/20 budget for college students easy campus money management plan“

Open High-Yield Teen Savings Account Early

Not all savings accounts are the same. High-yield accounts grow your money faster. Many banks have special teen accounts with no fees or minimums.

When looking for an account, ask these questions:

- What interest rate does the account offer?

- Are there any fees or minimum balance requirements?

- Can I access the account online and through a mobile app?

- Does the account offer automatic transfers to help with saving?

Most teen accounts need a parent or guardian until you’re 18. This helps you stay on track and learn about saving. It’s a chance to talk about different saving strategies like the “pay yourself first” method.

Having separate savings for different goals helps you stay focused. You might save for emergencies or for college. Digital banks let you create “buckets” for different goals.

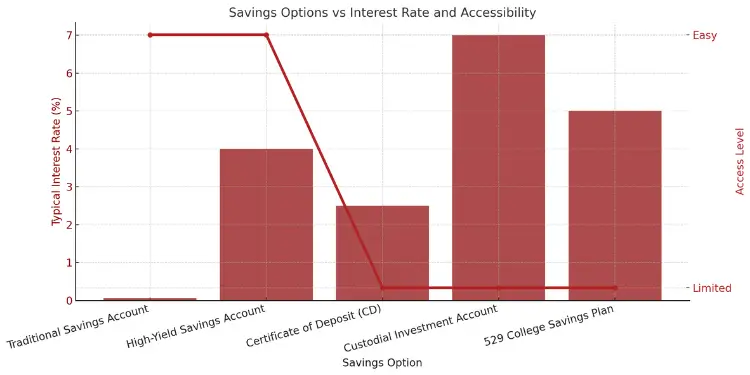

| Savings Option | Best For | Typical Interest Rate | Access to Funds | Parental Involvement |

|---|---|---|---|---|

| Traditional Savings Account | Emergency fund | 0.01% – 0.1% | Easy access | Required until age 18 |

| High-Yield Savings Account | Short-term goals (1-3 years) | 3% – 5% | Easy access | Required until age 18 |

| Certificate of Deposit (CD) | Known future expenses | 1% – 4% | Limited until maturity | Required until age 18 |

| Custodial Investment Account | Long-term growth (college) | Varies (potentially 7%+) | Limited until age 18/21 | Required (custodian) |

| 529 College Savings Plan | Education expenses | Varies (potentially 5%+) | Education expenses only | Account owner (parent) |

It’s hard for teens to save money because they want to spend it right away. To beat this, set up automatic transfers. This way, you save money without even thinking about it.

High-yield savings accounts are paying up to 4.35 % APY as of June 2025—far above traditional accounts and ideal for emergency or short-term teen savings goals. Ref.: “Jackson, S. (2025). Best High-Yield Savings Accounts — June 2025. Kiplinger.” [!]

Start with small savings goals to build confidence. Maybe save $100 for emergencies, then $500 for a new phone. Each goal you reach helps you save more for the next one.

Saving money is not just about the money. It’s about learning to delay gratification. Every dollar you save is a choice to think about your future first.

Take action today: Figure out 20% of your monthly income and set up automatic transfers. Even saving a little bit, like $5 or $10, is important. Your future self will be grateful for every dollar you save.

“Read Also: 50/30/20 budget for families tackling kids expenses and monthly bills“

Use cash envelopes or apps to stay organized

Teens who budget well know the secret. They use cash envelopes or apps to stay on track. This makes money management real and easy to follow.

Having a system helps you reach your goals. It doesn’t matter if you like paper or tech. What’s important is finding something you’ll use every day.

Label Envelopes for Needs, Wants, and Savings Categories

The cash envelope system is great for hands-on learners. It uses physical envelopes for spending categories. Start with sturdy envelopes and a marker.

Label three main envelopes for your 50/30/20 budget. You’ll need “Needs,” “Wants,” and “Savings” envelopes. For better organization, make sub-envelopes within these categories.

When you get money, divide it into the right envelopes. This stops you from spending your savings on impulse buys.

“Using cash envelopes completely changed my relationship with money. Seeing my ‘wants’ envelope empty halfway through the month was the wake-up call I needed to improve my spending habits.”

This system is simple. When an envelope is empty, you stop spending in that category. This builds discipline and helps you wait for what you really want.

For teens with debt, this system helps a lot. Set aside money for debt in your “Needs” envelope. This keeps you on track with payments and your credit score.

“Discover Insights: 50/30/20 needs vs wants categories for confident everyday spending choices“

Try Gamified Budget Apps for Motivation

If you prefer tech, many budget apps make money management fun. These apps are great for teens who always have their phones.

These apps use games and rewards to track your money. Many teens find it motivating to earn badges and see their progress. It helps them stick to their 50/30/20 budget breakdown.

| App Feature | Benefit for Teens | 50/30/20 Compatibility | Privacy Level |

|---|---|---|---|

| Spending Challenges | Makes saving feel like a game | High – tracks percentage goals | Medium – shares basic stats |

| Visual Progress Bars | Shows real-time category status | Perfect – shows category percentages | High – only you see details |

| Achievement Badges | Rewards consistent budgeting | Medium – not percentage-focused | Low – often shares on social |

| Automated Sorting | Categorizes expenses automatically | High – sorts into 50/30/20 buckets | Medium – requires transaction access |

When picking a budgeting app, choose one that’s safe. Look for apps that don’t ask for your full banking info. Many apps let parents check in without seeing everything.

CFPB guidance (2024) flags “phantom” overdraft fees—charges applied without documented consent. Teens should review account settings and consider opting out of overdraft programs. Ref.: “Consumer Financial Protection Bureau. (2024). CFPB Takes Action to Stop Banks from Harvesting Overdraft Fees Without Consumers’ Consent. CFPB.” [!]

Don’t keep switching apps. This messes up your tracking and makes it hard to see spending patterns. Pick one app and use it for at least three months before changing.

Set up alerts to help you stay on track. A weekly summary and alerts when you’re close to spending limits are good. They keep you aware without being too much.

Whether you use envelopes or apps, being consistent is key. The best system is one you’ll use every day. Many teens mix methods, using envelopes for daily spending and an app for savings.

Ready to start? Pick one method and set it up today. If you’re going digital, download an app and set up your 50/30/20 categories tonight. For envelope users, label your first three envelopes and divide your next income right away. Taking this step now helps build lasting financial habits.

“Explore This: How to make 50/30/20 budget with clear practical step by step“

Evaluate spending monthly and tweak categories

Regular review is key to the 50/30/20 for teens. Spend 15 minutes each month to check your spending. This habit helps you manage money well for life.

Ask yourself: “Did I stay within my categories?” and “What unexpected expenses came up?” Tracking your spending for two months helps spot patterns. Then, you can adjust your budget.

If you spend more than 50% on needs, find ways to cut costs. Some “needs” might be “wants.” Making these decisions gets easier with time.

“You Might Also Like:

Celebrate improvements and reset next month

Don’t aim for perfection with your budget. Small savings are worth celebrating. Saving $5 extra is a big deal!

Keep track of your progress to stay motivated. Many teens use the 50/50 rule for extra money. Save half and spend the other half on fun.

Start each month with a new budget. You’ll get better at managing money as a teen. Each month, you’ll grow more confident with your finances.

{kind=link}