Controlling your money starts with one powerful shift: putting every dollar to work before the month begins. The 2025 Charles Schwab Modern Wealth Survey reveals that 97% of Americans with a written financial plan feel confident about their financial goals—yet only 38% maintain one.

Digital apps left me overwhelmed. A simple notebook changed the game—tangible, durable, and effective. It’s thick and durable, perfect for carrying around.

Give every dollar a mission before the month starts. It’s a hands-on way to start with personal finance.

The idea is simple: use every dollar for something until you’re at zero. This way, you see your money differently and cut down on waste.

For beginners, a real notebook helps you connect with your money. It’s different from apps that hide behind screens. Writing down your finances makes you face your money head-on.

- A physical budgeting system increases accountability and mindfulness

- Zero-based budgeting helps eliminate “mystery spending” by assigning purpose to every dollar

- The right notebook makes financial organization simple and portable

- Building this habit takes about 90 days but delivers lasting financial clarity

Why Beginners Choose Zero-Based Budgeting

Newcomers to money planning love zero-based budgeting. It’s clear and helps manage money well. When I talk to neighbors, they often say, “I don’t know where it all goes.” This is why zero-based budgeting is great for beginners.

Zero-based budgeting is different from other methods. It makes sure your income minus expenses equals zero. This doesn’t mean you spend everything. It means every dollar has a job, like paying bills or saving.

“You Might Also Like: How zero budget tracking works to stop random spending”

Every Dollar Gets a Mission

The key to zero-based budgeting is giving every dollar a job. Think of each dollar as an employee. Would you pay workers to do nothing? No.

When I started using this system, my finances improved fast. I knew where my money went. Some dollars paid bills, others saved money, and some even bought weekend hobby supplies.

This method makes money management intentional. Before the month starts, you decide what each dollar will do. This simple change makes you proactive with money, not reactive.

“Zero-based budgeting changed everything for me. For the first time, I felt in control of my money instead of my money controlling me.”

“Discover More: How zero based budgeting works for first time savers”

Builds Awareness and Reduces Impulse Buying

Beginners love this method because it makes them aware of spending. When you decide where every dollar goes, you think twice before buying things. This stops impulse purchases.

This awareness can save a lot of money. I’ve seen neighbors cut down on restaurant spending by half. It’s very clear.

Tracking spending helps find problem areas. That $5 daily coffee adds up to $150 a month. It’s not about feeling guilty. It’s about making smart choices.

| Budgeting Method | Dollar Assignment | Spending Awareness | Flexibility | Beginner Friendly |

|---|---|---|---|---|

| Zero-Based | Every dollar has a specific purpose | Very High | Adjustable monthly | Excellent |

| 50/30/20 Rule | Broad category allocation | Moderate | Limited adjustment | Good |

| Pay Yourself First | Savings prioritized, rest unplanned | Low | High for spending | Fair |

| Envelope System | Cash assigned to categories | High | Requires physical transfers | Good |

Zero-based budgeting is simple yet effective for beginners. You don’t need fancy spreadsheets or degrees. Just assign every dollar a purpose and make sure your income minus expenses equals zero.

As you use this method, you’ll get clearer about your finances. Your spending categories will mean more. You’ll make choices based on what’s important, not just on impulse.

I tell neighbors starting out to focus on progress, not perfection. Your first budget won’t be perfect, and that’s okay. Each month, you’ll get better at managing your money and spending on what matters most.

Must-Have Features in a Beginner Budget Planner

My first try at using a budget planner was a disaster. I spent $35 on a fancy planner but gave up after two weeks. It was too hard to use. Don’t make the same mistake I did.

After helping many neighbors pick their first budget planner, I found three key features for beginners. These features help you succeed.

“Explore More: How to create zero budget for absolute beginners”

Pre-Filled Budget Category Prompts

When you start with a monthly budget, you don’t know all the categories. Pre-filled prompts are very helpful. A good planner should have common spending categories already listed.

Look for planners with these categories:

- Housing (rent or mortgage)

- Utilities (water, electric, gas)

- Groceries and household items

- Transportation (car payment, gas, insurance)

- Entertainment and dining out

For bleed-free pages and durability, opt for notebooks with 140 gsm paper and reinforced spines—standards validated in Wirecutter’s 2025 assessment of best paper journals.Ref.: “Gilbertson, S. (2024). The Best Paper Notebooks and Journals. WIRED.” [!]

These prompts help you avoid forgetting important expenses. I’ve seen friends give up because they forgot to include some costs.

“Further Reading: What is zero based budgeting explained simply for beginners”

Easy-to-Use Monthly Totals Page

The second key feature is a simple monthly totals page. This page should show your income minus expenses clearly. It should also have a spot to check if you’ve reached zero in your zero based budget planner.

Stay away from planners with too many details. They can confuse you and make you quit. The best planners have a simple overview that’s easy to understand.

A good totals page should:

- Show total income at the top

- List category subtotals clearly

- Calculate remaining funds (which should equal zero)

- Use simple math that’s easy to double-check

This feature lets you manage your money with confidence. You can quickly see if you need to adjust your spending. When you know every dollar is accounted for, you’re more likely to stick with your plan.

Affordable Price Under Twenty

The final key feature is the price. Keep your first budget template under $20. This is because your first planner is for learning.

You’ll learn what you like and need with this first planner. Do you prefer weekly or monthly layouts? Do you like digital or paper tracking? These choices will help you in the future.

I’ve seen friends buy expensive planners and feel guilty. This guilt often makes them stop using their expense tracker.

“Start with training wheels before buying a racing bike. Your first budget planner should be simple enough to use consistently but have enough features to teach you the basics.”

An affordable starter planner lets you budget every month without feeling guilty. You can try different things, make mistakes, and start over without wasting money.

These three features—pre-filled categories, simple totals pages, and an affordable price—make the perfect beginner budgeting setup. They help you avoid common problems and start a good budgeting habit that can change your financial life.

“Related Topics: How to do zero budgeting with clear examples”

Best Budget Planners for Beginners in 2025

Choosing your first budget planner is important. Not all are good for beginners. I tested over a dozen with my finance group. Three stood out for helping beginners stick to their budget.

Digital tools like Rocket Money (2025’s top-rated app) offer automation, though physical planners build deeper habit formation. But, physical planners help beginners form habits better. This is what I’ve seen teaching budgeting classes.

These top picks have special features for first-time budgeters. They offer structure without being too complex. This makes zero-based budgeting easy, even if you’ve never tracked expenses before.

Clever Fox Starter Edition

The Clever Fox Starter Edition is our top pick for beginners. It has the right mix of structure and simplicity. It covers all major expense areas and lets you add your own touches.

The coil binding is a big plus. It lets the book lay flat, making it easier to use every day. The monthly summary pages use simple math that won’t scare off newcomers.

The included sticker set adds fun. It makes budgeting feel like a fun activity, not a chore. Many students who failed with other systems found success with Clever Fox.

Budget Mom Paycheck Workbook

The Budget Mom Paycheck Workbook is great for those paid bi-weekly. It’s designed for managing money in two-week chunks. This helps beginners stretch their paycheck across the month.

Each paycheck has its own planning section. This makes it easy to see which bills get paid with which check. It helps avoid the cash crunch that often happens mid-month.

The cash envelope tracking system is also helpful. It’s good for categories where overspending is common, like groceries and dining out. Unlike digital tools, the physical envelopes help control spending better.

“Read More: How to start zero budgeting with simple step by step guide”

Happy Planner Budget Edition

The Happy Planner Budget Edition is all about customizability and looks. Its disc-bound system lets you add or remove pages as you like. This is perfect for beginners figuring out what works for them.

The colorful layouts and inspirational quotes make it fun to use. They’re great for visual learners. The built-in bill tracker and debt tracker keep you on track and motivated.

This planner stands out because it fits well with other planning systems. If you already use a Happy Planner, you can add your budget pages. This makes it easier to keep up with your budget.

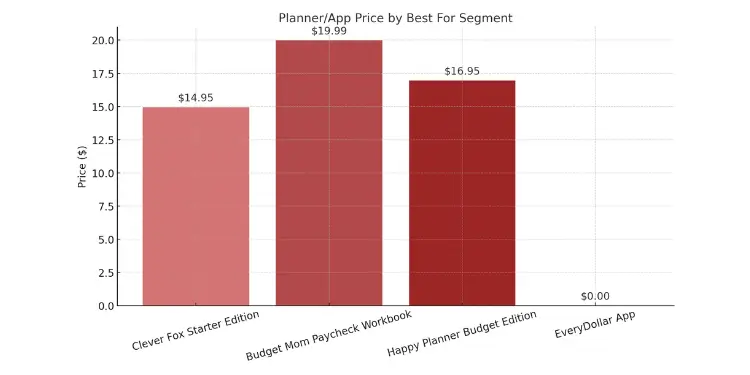

| Planner | Price | Best For | Standout Feature | Binding Type |

|---|---|---|---|---|

| Clever Fox Starter Edition | $14.95 | First-time budgeters | Perfect balance of structure and simplicity | Coil (lays flat) |

| Budget Mom Paycheck Workbook | $19.99 | Bi-weekly paid workers | Paycheck-to-paycheck planning sections | Spiral bound |

| Happy Planner Budget Edition | $16.95 | Visual learners | Customizable disc-bound system | Disc-bound (removable pages) |

| EveryDollar App (Digital Alternative) | Free basic version | Tech-savvy beginners | Automatic calculations | N/A (digital) |

Apps like YNAB (2025) sync across devices but lack tactile accountability. But, physical planners help beginners see their spending better. Writing down expenses by hand connects you to your money more than tapping on a screen.

Choose a planner that fits your payment schedule and style. The best planner is the one you’ll use every day. For most students, starting with one of these three options is best before switching to digital tools.

How to Set Up Your First Monthly Budget

Starting your first monthly budget is easy if you follow a few simple steps. I used to make it too hard and got really frustrated. But, I’ve helped many beginners with a simple method that works great.

List Your Income First

First, list all the money you’ll get in the month. This is key to the “pay yourself first” method. Include your regular paycheck, side hustle, and any other money coming in.

If your income changes, use the lowest amount you’ve made recently. This way, you won’t be disappointed when you can’t spend as much. You can only spend money you have or will get.

Many beginners skip listing their income first. This can lead to frustration when the numbers don’t add up. Use free budget spreadsheets and templates to track your income easily.

Allocate Buffers For Irregulars

Planning for unexpected expenses is key. These are costs that don’t come every month but will eventually. Think car registration, insurance, or holiday gifts.

Set aside a little money each month for these expenses. Even $20-30 can help avoid big surprises. Here are some important categories to consider:

- Car maintenance and repairs

- Medical co-pays and deductibles

- Annual subscriptions and memberships

- Seasonal expenses (holidays, back-to-school)

- Emergency fund contributions

I learned the hard way about planning for big expenses. A $600 car insurance bill ruined my third budget. If I had saved just $50 monthly, I’d have been ready.

This method also helps with saving for big goals. Small, regular savings add up quickly, whether for a vacation or emergency fund.

Highlight Due Date Clusters

Most bills come due around the same time, causing cash flow problems. Highlight these dates in your calendar. This helps you know when to be careful with spending.

For example, if rent, car payment, and internet bill all come between the 1st and 5th, mark those dates. This way, you avoid spending too much before big payments are due.

Group your bills into payment groups:

- Early Month (1st-10th): Typically housing, car payments

- Mid-Month (11th-20th): Often utilities, phone bills

- Late Month (21st-31st): Usually credit cards, streaming services

If many big expenses fall together, ask service providers to change your due dates. Many companies will help you manage your money better.

Don’t worry if your first month isn’t perfect. It’s okay. The goal is to get better each month and manage your money with confidence.

Common Budgeting Mistakes Beginners Make

Starting with zero-based budgeting can be tricky. Many people face the same problems. Knowing these can save you a lot of trouble.

Forgetting Yearly Subscription Renewals

Annual subscriptions can surprise you and hurt your budget. They can mess up your zero budget plan.

I forgot my Amazon Prime renewal and it cost me $119. Streaming services and memberships can also surprise you.

To avoid this, try these tips:

- Make a “Subscriptions” page in your planner

- Write down each subscription and its cost

- Split the yearly cost by 12 and save that monthly

- Set reminders 30 days before renewals

This makes yearly costs easier to handle. It’s key for those with irregular income.

Ignoring Small Cash Purchases

Small daily buys can also hurt your budget. A $3.50 coffee or $5 at the store adds up fast.

A family lost $400 a month without realizing it. They found out by tracking every cash buy. This habit cost them $5,000 a year!

Here’s how to track small buys:

- Always carry your planner

- Use a notepad or app for buys

- Update your planner every night

- Use envelopes for small buys

The envelope system is great for small buys. Just put cash in labeled envelopes at the start of the month. When it’s gone, you’re done spending.

Tracking subscriptions and small buys can save thousands. Every dollar counts in a zero-based budget. It makes your money go further than you think.

The biggest budget leaks are the ones you don’t see. It’s the small daily buys that hurt, not the big ones.

Your budget planner only works if you fill it with good info. Avoid these common mistakes to make your zero-based budget work well.

Staying Motivated Through First Year

The real challenge with zero-based budgeting isn’t learning it—it’s sticking with it long enough to see results. I fixed my finances and helped neighbors too. Two key strategies help people stay motivated when the excitement fades.

Celebrate Monthly Surplus Wins

Your brain needs positive reinforcement to build lasting habits. When you spend less than planned, mark it! I circle surpluses in green or add stickers to my budgeting system.

Try setting aside 10% of any surplus for something fun—a coffee date or movie night. The other 90% goes toward money goals like savings and debt repayment. That little reward creates powerful motivation to continue.

Track Progress Visually Graphs

Numbers alone rarely inspire, but visual progress markers do. Reserve space in your spreadsheet or budgeting notebook for simple graphs. My neighbor Lisa created a debt payoff thermometer in her zero-based budget planner and colored it in monthly.

This visual reminder helped her eliminate $42,000 in debt in just 18 months. Track what matters most—emergency fund growth, debt reduction, or spending in problem categories.

Meta-analysis of 19,951 participants found that frequently recording visible progress (e.g., colouring a debt-payoff thermometer) significantly boosts goal attainment—especially when updates are written down or shared publicly.Ref.: “Harkin, B. et al. (2015). Does Monitoring Goal Progress Promote Goal Attainment? Psychological Bulletin / APA-ScienceDaily.” [!]

Remember that zero-based budgeting is important because it builds awareness. You’ll need to create a new budget every month to handle irregular expenses and changing monthly income. The system gets easier with practice, and tracking your wins will keep you motivated through the ups and downs of your first year with ZBB.

{kind=link}