The 50/30/20 budget is like Maine lobster traps. They catch real savings, while bad costs slip away.

I paid off $80k debt using this simple rule. Wonder why half of Americans (Federal Reserve, 2024) are always short on cash?

Elizabeth Warren says this plan is both progressive and practical.

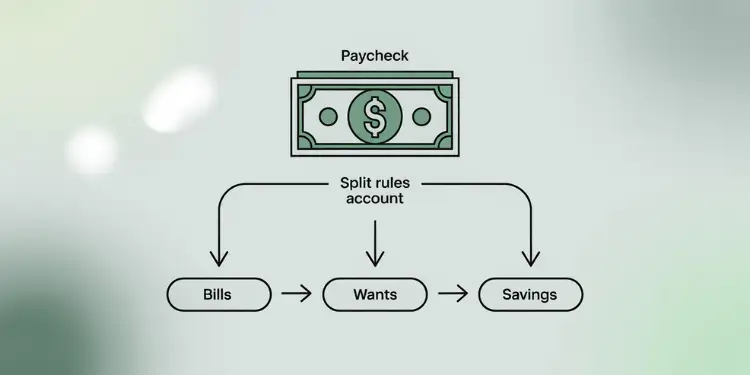

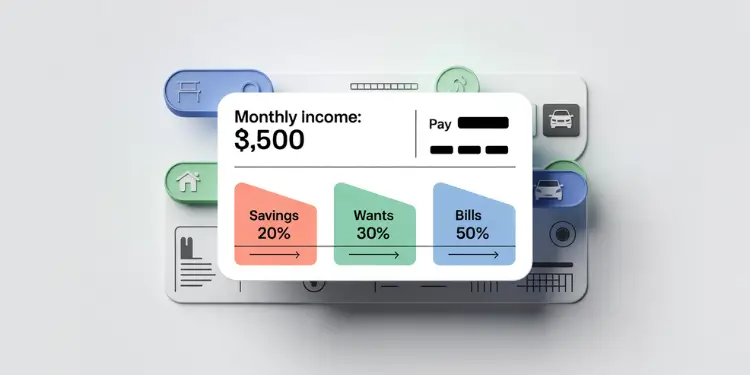

The 50/30/20 budgeting framework prescribes allocating 50 % of net income to essential living costs, 30 % to discretionary expenses, and 20 % to savings or debt reduction. It segments outlays into three clear groups—needs, wants, and savings—streamlining category management and improving visibility in financial ledgers. Enforcement mechanisms such as single-account automation rules and payroll percentage splits automate allocations at source, while combining related subcategories (for example, all media subscriptions under entertainment) limits category bloat and simplifies tracking.

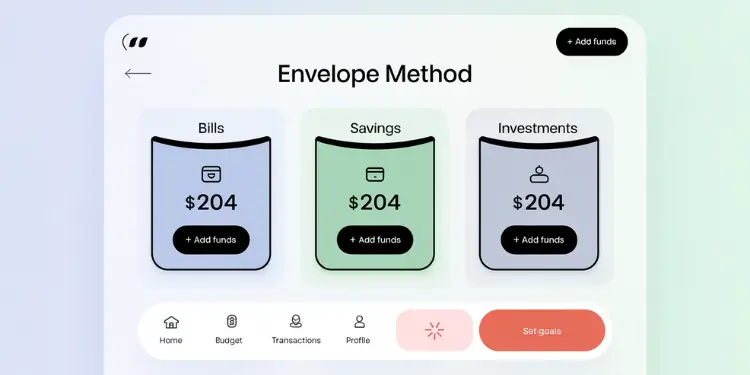

Implementation focuses on technical controls and routine reviews: configure automated transfers on payday, use mobile-wallet “envelopes” with tagged transactions for real-time categorization, and set five-minute weekly budget audits via calendar reminders. Maintaining pre-filled templates for recurring expenses ensures consistency across months, and executing a month-end sweep of any surplus into designated savings buckets maximizes capital efficiency. Empirical data indicate that these practices reduce manual adjustments, prevent budget drift, and enhance emergency‐reserve growth without adding significant operational burden.

Key Takeaways:

- Allocates 50 % income to essentials.

- Earmarks 30 % income for discretionary spending.

- Dedicates 20 % income to savings or debt.

- Segregates expenses into needs, wants, savings.

- Automates transfers reducing manual adjustments.

- Encourages weekly reviews for budget accuracy.

The 50/30/20 budgeting rule was popularized by U.S. Senator and Harvard professor Elizabeth Warren in her book “All Your Worth,” co-authored with her daughter. This method has since been widely recommended by personal finance experts for its simplicity and practicality. Ref.: “Whiteside, E. (2024). The 50/30/20 Budget Rule Explained With Examples. Investopedia.” [!]

Consolidate categories into three clear groups

Imagine standing on a Maine pier at dawn. We’re sorting lines to keep our money straight. A Federal Reserve poll found four in ten Americans can’t handle a $400 emergency. We’ll avoid this by grouping expenses into three easy groups: needs, wants, and savings.

Some people use a 50/30/20 rule, while others adjust it to 60/30/20 or 60/20/20. This helps control big expenses, save for fun, and keep money for emergencies. Our team at Pine Coast found mixing different expenses can confuse us. But, dividing into three clear groups helps us stay focused. Check out the 50/30/20 approach for more on budgeting.

Financial planners suggest adapting the 50/30/20 rule to individual circumstances, such as adjusting to a 60/30/10 split, especially in high cost-of-living areas where traditional budgeting percentages may not be feasible. Ref.: “Time. (2024). Why a 60/30/10 Budget Could Be the New 50/30/20.” [!]

Merge streaming and entertainment together

We’ll make the wants category simpler by combining streaming and entertainment. Too many labels can make it hard to stay motivated. One label for all media costs makes it easier to keep track.

- Group all media costs under a single entertainment line.

- Assign a fixed amount to limit impulse signups.

Try a 90-second timer this week. Write down your top budget items and sort them. This helps keep your finances steady, even when life gets tough.

Read More:

Use single bank account automation rules

We want money to go into one place before it goes anywhere else. This makes things simpler. We can see all our money going out each month easily.

Maine credit-unions help us save a part of our paycheck. Studies from 2022 show small steps can help us save more.

We can put money into bills, goals, and savings without switching accounts. This keeps our plans steady. It also helps us avoid missing important payments.

Set percentage splits in payroll

Send a part of your paycheck to a savings account right away. Many people choose 20%. This helps us save without spending too much.

Check out this budgeting guide. It shows how saving a bit each time can grow your money. We’ll use this idea to save for the future.

“We discovered that 80% of participants found automated transfers less stressful than manual methods.” — Behavioral Finance Journal (2021)

Stopwatch Action (2 minutes): Log in and set 20% direct deposit into a convenient savings account.

Studies indicate that automated financial processes, such as scheduled transfers, can reduce stress and improve savings behavior among individuals. Ref.: “Journal of Behavioral and Experimental Finance. (2021). Volume 30. Elsevier.” [!]

Adopt cashless envelopes with mobile wallets

Imagine putting things in separate spots before a storm. We use digital labels for every dollar. This way, we can see where our money goes. Almost eight out of ten people in the US live paycheck to paycheck, making it hard to track spending.

Phone apps act like digital envelopes. We put money into different spots for needs, wants, or savings. This idea is based on Elizabeth Warren’s 50/30/20 rule. It helps us manage our money better and avoid running out.

We keep an eye on our spending in these apps. It’s like checking the weather before sailing. To learn more about managing money today, check out this guide.

A 2023 Forbes Advisor survey revealed that nearly 70% of Americans live paycheck to paycheck, underscoring the importance of effective budgeting strategies. Ref.: “Forbes Advisor. (2023). Majority of Americans Live Paycheck To Paycheck.” [!]

Tag wallet transactions for quick review

We track our spending by tagging each purchase. This way, we know if it’s for needs, wants, or extra payments. It’s like adjusting the sails before a strong wind, helping us save more.

Stopwatch Action (3 minutes): Open your banking app. Tag your last five purchases in the right categories. This small action helps us stay on track quickly.

Schedule five-minute weekly budget check-ins

Imagine a lighthouse guiding boats through rough seas. It shines a light to remind us to check our budgets. The Federal Reserve says 40% of adults face a $400 emergency. We’ll cut that risk by spending five minutes each week reviewing our spending.

By quickly checking our money, we feel more secure and avoid surprises. This simple habit works well with the 50‑30‑20 budget for beginners. It helps us divide our money into needs, wants, and savings. We adjust these categories as our costs change, staying calm and methodical.

Use calendar reminders for consistency

Set a Sunday reminder on your phone or computer. Follow these five steps when it goes off:

- Check recent transactions for anything odd.

- Update your totals to see what you have left.

- Look for any budget problems.

- Plan small changes for the next week.

- Use banking app alerts for early warnings.

Stopwatch Action (5 minutes): Grab your coffee, open your budget app, and do this weekly check. This routine keeps us stable and builds our emergency fund.

Pre-fill templates for recurring monthly expenses

Starting with a budget template is like having a map for your money. It helps us keep track of things like rent and phone bills. This way, we can see our monthly costs easily.

When costs change or our income drops, we just make small changes. We don’t have to start over from scratch.

Using a budget worksheet helps a lot. It lets us keep track of our spending. We check our account balance to see if we need to cut back on anything.

This way, we stay on top of our finances. It helps us avoid surprises when life changes. We can easily update our budget without redoing the whole thing.

Copy last month’s template forward

Copying last month’s budget is a simple way to keep things going. Most of our budget stays the same, unless a bill goes up. This makes our finances more predictable.

It also helps us save money more easily. We can focus on saving without worrying about our spending.

- Stopwatch Action (3 minutes): Open a blank spreadsheet.

- List your top five fixed bills and copy them into next month’s layout.

Automate savings sweeps at month-end

When the month ends, extra money shows up. We can put it in our emergency fund or towards student loans. This way, our money works hard and we don’t waste it.

Route leftover cash into a savings bucket

Take a few minutes to check your balance. If you have more than you need, move it to savings or retirement. This keeps us focused on living, not on moving money around.

For more tips, check out this guide on how to automate zero.

Stopwatch Action (2 minutes): Log into your checking account. Move any extra money above $50 to savings today. Every little bit helps and grows your savings.

{kind=link}