Product liability insurance keeps businesses safe from expensive lawsuits. It helps when their products cause harm. This insurance protects many, including makers, sellers, and distributors.

Why do smart business owners worry about one bad item? A shocking fact is that U.S. businesses face over 15,000 new liability claims every year. These claims often cost around $2.3 million to settle.

“I’ve seen families lose everything because they thought they didn’t need this insurance,” says an Idaho Falls agent. “Just one claim about an allergic reaction can ruin a business fast.”

In my 10 years helping families, I’ve seen how this insurance saves businesses. It doesn’t matter if you make furniture or sell things from other countries. This insurance is like a safety net for your money. It pays for legal fees, medical bills, and settlements if someone says your product hurt them.

Product liability insurance enables businesses to transfer financial risk associated with design, manufacturing, or labeling defects. Coverage encompasses legal defense costs, settlements for bodily injury and property damage claims, and expert witness fees. Annual claim frequency in the U.S. exceeds 15,000, with average settlement costs around $2.3 million. Policies protect manufacturers, distributors, and retailers regardless of prior knowledge of defects.

Contractual obligations often mandate coverage limits between $1 million and $2 million and inclusion of additional insured endorsements. Policies fund court costs, medical expenses, and damage awards to preserve assets and maintain operations. Regular review of policy limits ensures adequacy against potential high-cost judgments and alignment with distributor or retailer requirements.

Quick hits

- Covers lawsuits from defective goods

- Protects against medical expense claims

- Handles legal defense costs automatically

- Essential for all manufacturers nationwide

Protection against defective product lawsuits

Product liability insurance helps your business when customers say your products hurt them. It keeps you safe from three main types of product defects. These can lead to costly lawsuits.

Let’s say you sell a coffee maker. If it overheats and catches fire, that’s a design defect. It’s dangerous, even if customers use it right.

Manufacturing defects occur during making. Your coffee maker is fine, but one has bad wiring. This can start a lawsuit, even if your design is good.

Marketing defects happen when warnings or instructions are missing. You sell the coffee maker without telling customers to avoid water. This can hurt them because they didn’t know the risks.

“Businesses can face liability even when they had no knowledge that they were selling a defective product. The law doesn’t require intent—just that the product caused harm.”

What surprises many is that liability insurance protects you even if you didn’t know about the defect. You’re responsible, even if you didn’t know about the problem.

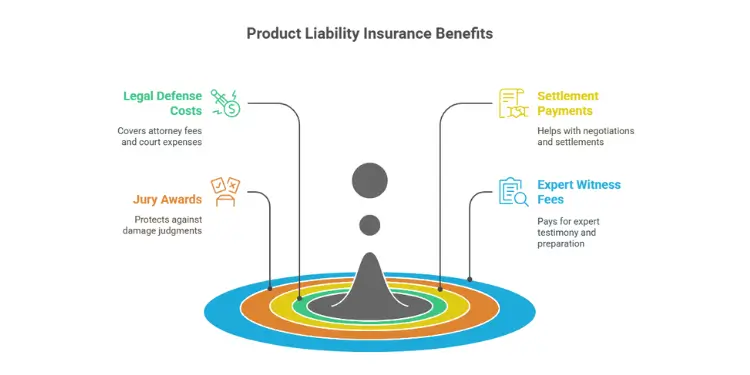

This insurance helps with many costs if someone sues you for a defective product:

- Legal defense costs and attorney fees

- Court costs and filing expenses

- Settlement negotiations and payments

- Jury awards and damage judgments

- Expert witness fees and case preparation

Without insurance, one lawsuit can use up all your savings. I’ve seen small businesses face huge legal bills before trial. This can force them to close.

Product liability insurance moves these risks to your insurance company. If someone says your product hurt them, your insurer will defend you. They also pay for damages.

The important thing is you don’t have to be careless to face a lawsuit. Just selling a product that later causes harm can lead to a lawsuit. Your insurance helps protect your business and keeps it running while you deal with legal issues.

Remember, insurance covers all three defect types the same. It doesn’t matter if the problem is in design, making, or warnings. Your policy helps the same way. This gives you peace of mind when selling products, knowing you’re not at risk of losing everything to a lawsuit.

Read More:

Coverage for bodily injury claims

When someone gets hurt using your product, you face big medical bills and legal trouble. Bodily injury claims are the biggest risks for manufacturers. I’ve seen small businesses get bills over $100,000 for injuries caused by their products.

Product liability insurance helps cover these huge costs. Without it, one injury claim could bankrupt you. Your policy helps with both immediate medical costs and long-term legal issues.

Medical Expenses for Injured Consumers

Liability insurance pays for medical treatment when someone is hurt by your product. These costs start right away and can grow fast. Your coverage includes many types of medical costs:

- Emergency room visits and ambulance transportation

- Surgical procedures and hospital stays

- Physical therapy and rehabilitation services

- Ongoing treatment for permanent disabilities

- Prescription medications and medical equipment

Medical costs from product injuries can surprise business owners. A small cut might cost $2,000. But serious injuries can cost $50,000 or more.

Your insurance pays for these medical bills, no matter who’s at fault. This helps injured people while legal issues are sorted out. It’s important to act fast on product liability claims to avoid more problems.

Supplemental Payments Like Legal Judgments

Product liability insurance also covers big legal judgments. These payments can be much more than medical costs. Your coverage includes several types of legal awards:

- Compensatory damages for pain and suffering

- Punitive damages when courts find negligence

- Lost wages during recovery periods

- Future earning capacity for permanent disabilities

Legal judgments in injury claims can be hundreds of thousands of dollars. Courts give compensatory damages for emotional pain and lower quality of life. Punitive damages punish for safety mistakes or bad design.

Insurance covers these judgments to protect your personal stuff. Without it, creditors could take your home, savings, and business stuff. One big judgment can wipe out years of hard work and planning.

“You Might Also Like: What is the purpose of mortgage life insurance?“

Property damage resulting from product faults

Product liability insurance helps protect your business. It covers damage to customers’ homes or workplaces from faulty items. Many overlook how product malfunctions can harm buildings, vehicles, and belongings.

I’ve seen how costly this oversight can be. A client sold space heaters that had a faulty thermostat. This caused a house fire that damaged the kitchen and other rooms. The repair costs were over $75,000, paid out of the business owner’s own money.

Your insurance covers two types of damage. Direct damage is when your product breaks something. Consequential damage is when your product causes more damage after the initial problem.

Examples include electrical items starting fires, tools damaging surfaces, or appliances leaking and flooding basements. These situations can cost a lot and threaten your business.

- Electrical products shorting out and starting fires

- Heating devices overheating and melting nearby materials

- Appliances leaking water and flooding homes

- Tools malfunctioning and damaging expensive equipment

- Chemical products corroding surfaces or structures

Claims for property damage can be big surprises. Home repairs, business interruptions, and replacement costs add up fast. One incident can cost tens of thousands of dollars.

| Damage Type | Common Causes | Typical Costs | Coverage Response |

|---|---|---|---|

| Fire Damage | Electrical shorts, overheating | $25,000-$150,000 | Repairs, temporary housing |

| Water Damage | Appliance leaks, pipe bursts | $5,000-$50,000 | Cleanup, restoration, mold |

| Structural Damage | Explosions, chemical reactions | $50,000-$300,000 | Rebuilding, engineering costs |

| Equipment Damage | Tool malfunctions, power surges | $10,000-$75,000 | Replacement, lost productivity |

Without product liability insurance, you’d have to pay these costs yourself. This could mean losing your home, retirement savings, or business equity. The financial burden often forces small manufacturers out of business.

Your insurance helps by covering repair costs, replacement expenses, and temporary relocation fees. This lets you focus on fixing the product issue instead of worrying about huge bills.

Check your policy limits every year. Property damage from defective products can be more than your basic coverage. This is true, even in commercial settings where equipment values are high.

“Check Out: The purpose of homeowners insurance coverage“

Legal defense and settlement costs

Product liability lawsuits can surprise businesses more than the damages. Many think they only pay if they lose. But legal liability is different in real life.

Your liability coverage starts when someone files a claim. Even silly lawsuits cost tens of thousands of dollars. The policy covers these costs, keeping your money safe during tough times.

Product liability insurance helps with big legal bills, no matter the case’s worth. I’ve seen companies spend $15,000 just to prove they’re not guilty. Your coverage pays these costs right away, so you don’t lose money waiting for the case to end.

Settlement talks are also covered by your policy. If your lawyer suggests settling to avoid a big trial loss, your insurance helps with that too. This lets you focus on your business, not worrying about legal costs.

Attorney Fees and Court Costs

Legal costs add up quickly in product liability cases. Lawyers charge $300 to $500 an hour, and cases can last a long time. Your policy covers these costs automatically.

There are more costs than just lawyer time. Filing fees, expert witness costs, and document prep are all covered. I’ve seen these costs go over $25,000 before a trial even starts.

Your policy also covers special legal needs. This includes hiring experts to explain your product’s design or how it’s made. These experts can charge $200 to $400 an hour for their time.

Next, check your policy limits to make sure they cover your legal costs. If you make high-risk products, you might need more coverage to handle complex cases.

“Dive Deeper: Why is car insurance important to have?“

Compliance with retailer and distributor contracts

Your product liability insurance is key for partnerships with big stores and distributors. Many find out when they’re ready to sign big contracts. Stores won’t sell your products without proof of insurance.

I’ve helped many manufacturers meet these needs. They usually need $1 million to $2 million in product liability coverage. It’s not just a suggestion, it’s a must.

Retailers can face lawsuits even if they just sell the product you sold without changing it. They need insurance to protect themselves from future claims. Your insurance helps keep them safe.

Distributors also face risks, even if they don’t make the products. They move products but can get sued. The liability insurance is designed to protect everyone in the chain.

Without the right insurance, you can’t sell to big stores or many retailers. You’ll only be able to sell directly or to small stores. This limits your business and how much money you can make.

Having insurance shows you’re professional and know about risks. It opens doors to bigger opportunities.

When looking at contracts, check the coverage amounts and who needs to be added to your policy. Your policy must match these details. The product liability insurance is designed to meet these needs and protect your business.

| Retailer Type | Typical Coverage Requirement | Additional Insured | Contract Timeline |

|---|---|---|---|

| Big Box Stores | $2 Million | Required | Annual Review |

| Online Marketplaces | $1 Million | Sometimes Required | Ongoing Verification |

| Wholesale Distributors | $1-2 Million | Required | Contract Renewal |

| Specialty Retailers | $500K-1 Million | Varies | Case by Case |

Get coverage before talking to big retailers. Having insurance speeds up talks and shows you’re serious. The insurance is designed to help you reach more customers.

These rules protect the whole supply chain. When everyone has the right coverage, risks are shared fairly. This helps everyone in the chain and gives consumers a way to get help if needed.

“Further Reading: Do I need life insurance for my family?“

Business reputation and customer trust protection

Your business reputation is built over years. It’s about the trust you’ve earned from customers. Product liability insurance helps protect this trust when problems arise.

I’ve seen how it works. Companies with the right insurance keep their customers loyal, even in tough times. Without it, businesses find it hard to get back their reputation.

Crisis management during product incidents

When a product is linked to harm, your insurance helps. They offer crisis management tools. These tools help you respond fast and well.

Product liability insurance covers legal costs. It lets you focus on keeping customers safe. Most policies don’t cover recall costs, but they do cover legal defense.

Professional communication strategies

Good communication is key during product issues. Liability insurance shows you’re responsible. It helps you keep the public’s trust.

Your insurer’s PR support helps you respond right. This shows customers you’re ready for anything. It’s a sign of financial strength.

This lets you fix problems without worrying about money. You can focus on safety, not just saving money. Next, talk to licensed agents to find the right insurance for your products and budget.

{kind=link}