Knowing when you’re not ready to buy a house can save you a lot of trouble. I’ve seen many people buy a house too soon. They face big problems because of it.

A 2021 Bankrate survey found 63% of young homeowners regret their choice. I tell my clients, “The house might end up owning you, not the other way around.”

Renting isn’t always a bad deal, unlike what many think. First-time buyers often don’t see the hidden costs of owning a home. These costs can turn a dream into a financial nightmare.

In my nine years helping people in Greenville with real estate, I’ve found five key signs to wait. These signs help figure out if you’re ready for such a big step.

Quick hits:

- Unstable income spells mortgage payment trouble

- High debt ratios restrict purchasing power

- Minimal savings can’t cover unexpected repairs

- Uncertain location plans limit investment

- Market timing affects long-term financial outcomes

Insufficient savings for down payment

Starting to buy a home needs a lot of savings for the down payment. Many people don’t realize this. In Greenville, I’ve seen many dreams delayed because of this.

Most loans need 3-5% down. FHA loans need 3.5%. Putting down less than 20% means you’ll pay PMI every month. This is extra money for the lender, not you.

Last year, a couple saved just enough for a 5% down payment. They got the loan but had to pay $180 extra each month for PMI. This cut their buying power by almost $40,000.

Conventional mortgages impose monthly Private Mortgage Insurance (PMI) whenever the down payment is below 20 %, increasing housing costs until you build sufficient equity.Ref.: “Johnson, K. (2025). Current Mortgage Rates by Credit Score. The Mortgage Reports.” [!]

Emergency Fund Lacks Six Month Cushion

Your down payment and emergency fund must be separate. This is very important. An emergency fund of 3-6 months of expenses is your safety net.

I remember Michael, a software developer who bought his first home in 2021. He lost his job three months later. But he had a six-month emergency fund. This let him keep making mortgage payments while he looked for a new job.

To figure out your emergency fund, use this formula:

| Monthly Expense | Typical Amount | Your Amount | 6-Month Total |

|---|---|---|---|

| Mortgage/Rent | $1,500 | $_____ | $_____ |

| Utilities | $300 | $_____ | $_____ |

| Food/Groceries | $600 | $_____ | $_____ |

| Transportation | $400 | $_____ | $_____ |

| Insurance/Medical | $350 | $_____ | $_____ |

Add your monthly expenses and multiply by six. This is the minimum emergency fund you should have in addition to your down payment.

Federal regulators advise building an emergency fund that covers at least six months of essential expenses before taking on a mortgage, safeguarding you against sudden income loss or major repairs.Ref.: “Federal Deposit Insurance Corporation. (2024). Starting Small Can Lead to Big Savings. FDIC Consumer News.” [!]

Closing Costs Remain Unfunded Reserve

The down payment is just the start of what you’ll need at closing. Many first-time buyers are surprised by closing costs. These costs add 2-5% to the home price.

For a $300,000 home, that’s $6,000-$15,000 in cash. Here’s what you can expect:

- Loan origination fees: 0.5-1% of loan amount ($1,500-$3,000 on a $300,000 home)

- Appraisal fee: $300-$500

- Home inspection: $300-$500

- Title insurance: $500-$1,000

- Attorney fees: $500-$1,500

- Prepaid property taxes and homeowners insurance: Often 2-3 months’ worth

- Mortgage points (optional): Each point costs 1% of your loan amount but lowers your interest rate

Last month, a family saved $40,000 for a $250,000 home. But their Loan Estimate showed nearly $8,000 in closing costs. Without more savings, they had to choose between a smaller down payment or wait to buy.

The biggest mistake first-time buyers make is using all their savings for the down payment and closing costs. They forget about moving expenses and home repairs.

Also, save $3,000-$5,000 for moving, home repairs, and improvements. The water heater or HVAC system won’t wait for you to save more.

If you’re short on savings, you’re not ready to buy a house yet. Keep saving and watch the housing market. Being financially ready is key when you’re ready to buy.

High debt impacts loan qualification chances

Carrying a lot of debt while looking for a house is a big problem. It makes it hard to save for a down payment. It also affects if lenders will give you a mortgage.

Lenders look at your debt-to-income ratio (DTI) when you apply for a loan. This ratio shows how much of your income goes to debt. It helps them see if you can handle a mortgage payment.

Most loans want your DTI to be under 43%. This means your total debt payments can’t be more than 43% of your income. This includes your future mortgage payment.

FHA loans might let you go up to 50% in some cases. But, it’s not smart to go that high. If you try buying a house with a lot of debt, saving for a down payment is tough. Most of your extra money will go to debt.

To find your DTI, add up all your debt payments, then divide by your income. Multiply by 100. For example, if you pay $2,000 in debt and make $6,000 a month, your DTI is 33%.

Debt to Income Ratio Exceeds Lender Limits

Even if a lender says you qualify, being close to the limit is risky. I helped a client who was approved for a mortgage that would have pushed their DTI to 42%. They would have had only $400 a month for everything else.

Experts say your housing payment should be no more than 25% of your income. This leaves room for saving and other expenses.

Many small debts can add up to a big problem. A $300 car payment, $250 in student loans, and $150 in credit card payments can take up $700 of your income. This leaves little room for a mortgage.

High-interest debt, like credit cards, needs your focus. Paying off these debts can save you money. It also makes you more likely to qualify for a mortgage.

Make a plan to pay off your debt before you start looking for a house. Track your debt and make a timeline to pay it off. This might delay your home purchase, but it will help you qualify for better loans and reduce stress.

Remember, owning a home has unexpected costs. If you’re not already stretched thin by debt, you can handle these surprises. The goal is to enjoy your home without constant worry about money.

“Read More: Must have home buying budget tools for buyers”

Unstable employment or income history patterns

Your income history tells lenders a lot about your mortgage application. They usually want to see two years of steady work in the same field. It’s not about working for the same company, but job changes can worry them.

I’ve helped many first-time buyers, and employment checks often block them. Lenders need proof you can pay your mortgage for 15-30 years.

Changing jobs in the last two years might slow down your home buying. The same goes for gaps in work or recent graduation. Lenders look for stability before giving a big loan.

Fannie Mae underwriting generally demands two full years of verified self-employment income, which can delay purchases for newly launched businesses.Ref.: “Fannie Mae. (2024). Underwriting Factors and Documentation for a Self-Employed Borrower. Selling Guide B3-3.2-01.” [!]

Income from commissions is tricky. Lenders average your income over two years if it’s from commissions. This can make your qualifying income lower if you’ve recently earned more.

Your employment history isn’t just a checkbox for loan approval—it’s a practical safeguard against taking on a financial commitment you might struggle to maintain.

Self-employed buyers get extra checks. I’ve helped many entrepreneurs buy homes. Lenders often need:

- Two years of business tax returns

- Personal tax returns showing consistent income

- Year-to-date profit and loss statements

- Business bank statements

The gig economy makes things harder. Uber drivers, freelancers, and those with multiple jobs face income verification challenges. Lenders want a longer income history.

Mortgage payments are fixed, unlike rent. This makes stable income a must for homeownership.

If you’re facing job instability but want to look at houses, here’s what to do:

- Stay in your current job for at least 12 more months if you can

- Keep detailed records of all income, if self-employed

- Avoid changing industries, even if changing employers

- Save up for a bigger down payment to help with job worries

- Talk to a lender about what you need for your situation

Those with recent job gaps might want to wait to buy. Lenders often want you to work for six months before counting your income. Self-employed people need two years of tax returns showing enough income.

Waiting to build a stronger job record is smart. It’s not just for loan approval. It’s for affording your home without stress. The stability lenders want helps you build equity without worry.

If unsure about your job history, get pre-qualified with a lender. This shows how much your payments will be and if now is the right time to buy.

“Check This Out: How to buy house on low income successfully”

Low credit score increases borrowing costs

A fair credit score can save you nearly $100,000 on your mortgage. As a realtor, I’ve seen this truth at closing tables many times. Your credit score is key for lenders to set your interest rate.

Even a small rate difference adds up over 30 years. Let’s see how it affects your money.

For a $300,000 mortgage, a 620 score might mean 1.5% higher interest than a 740+ score. This means about $250 more each month. Over 30 years, you’ll pay an extra $89,000 in interest. That’s enough for college or a big retirement fund.

If your credit score is lower than the mid-600 range, you’ll only be eligible for crappy, high-interest loans. So, before you buy a house, buckle down and knock out your debt as fast as possible using the debt snowball.

Loan types have different credit score needs. Conventional loans need 620+, FHA loans accept 580, and VA loans range from 580-620. But, even meeting these minimums often means high rates.

Raising a credit score from 620 to 740 on a $300 k 30-year loan can trim payments by ≈$291 per month—saving about $104,760 in lifetime interest.Ref.: “Johnson, K. (2024). How Credit Scores Impact Mortgage Rates. Refi.com.” [!]

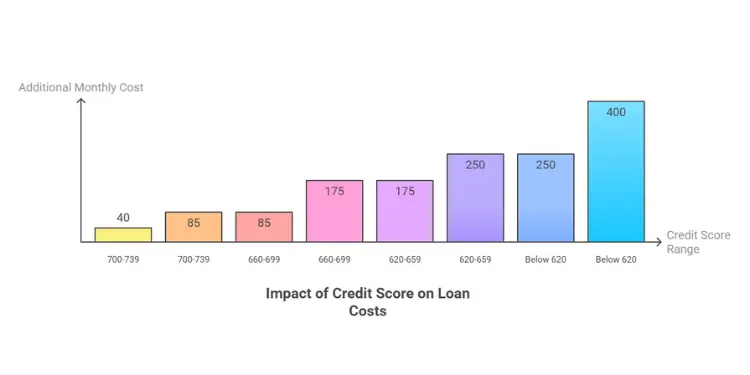

| Credit Score Range | Loan Eligibility | Typical Rate Increase | Monthly Impact ($300K) | 30-Year Added Cost |

|---|---|---|---|---|

| 740+ | All loan types | Best available rates | Baseline | Baseline |

| 700-739 | All loan types | 0.25-0.5% higher | $40-$85 more | $14,400-$30,600 |

| 660-699 | All loan types | 0.5-1.0% higher | $85-$175 more | $30,600-$63,000 |

| 620-659 | Limited options | 1.0-1.5% higher | $175-$250 more | $63,000-$90,000 |

| Below 620 | FHA/VA only | 1.5-2.5%+ higher | $250-$400+ more | $90,000-$144,000+ |

A low credit score means higher interest rates and more costs. You might pay more for private mortgage insurance and need a bigger down payment. These can make your monthly payments higher and reduce what you can buy.

Many first-time buyers are surprised by how much interest rates affect affordability. A buyer with excellent credit might qualify for a $300,000 home. But someone with poor credit might only qualify for $225,000, even with the same income.

“Related Topics: House price to income ratio rule for buyers”

Time Needed To Repair Credit Profile

Credit repair takes time, but it’s worth it. Most improvements take 3-12 months of consistent effort. This time is perfect for saving for a down payment, too.

Negative items like late payments stay on your report for 7 years. But, their impact lessens over time. Recent good behavior helps more than past mistakes. So, you can see big improvements in 6-9 months with a good credit plan.

If you’re wondering how to get a home loan with bad credit, start by improving your score. Here are some steps:

- Check your credit reports for errors (available free at AnnualCreditReport.com)

- Reduce credit card balances below 30% of your limits

- Make all payments on time, every time

- Avoid opening new credit accounts

- Keep old accounts open to maintain credit history length

I helped a client raise her score from 580 to 680 in nine months. This saved her $217 monthly. That’s $78,120 over 30 years. She paid down debt, fixed errors, and made all payments on time.

Improving your credit score takes patience and discipline. If your score is low, wait until it improves. The savings will be worth it.

Lenders look at more than just your score. They check your payment history, credit types, and recent applications. A score that’s getting better shows you’re managing your money well.

Emotional readiness and lifestyle factors misaligned

Numbers only tell part of the story about being ready to buy a home. Your feelings and lifestyle plans are just as important. Even with great credit and savings, buying a home might not fit your life right now.

Think about this: Are you ready to stay in one place for a long time? The average American stays in their “forever home” for just 13 years. Selling a home too soon can cost you money because of closing costs and early mortgage interest.

“Explore More:

Uncertain Plans About Career or Location

If you’re thinking about going back to school or moving for a job, now might not be the best time to buy a home. Homeownership can limit your flexibility when you’re changing careers or moving around.

Also, think about your lifestyle. Do you like being able to move easily? Do you hate doing home repairs? It’s important to know if you’re ready to stay in one place and handle home duties.

Remember, having extra money in your budget is not just for the mortgage. Homeowners spend about 1-4% of their home’s value on maintenance each year. This can be a lot of time and money, depending on your lifestyle.

It’s okay if you’re not ready to buy a home yet. It’s actually smart to wait until you’re financially and emotionally ready. When your career and location plans are clear, you’ll find the perfect home for you.

{kind=link}