Choosing between a big or small down payment changes your whole home buying journey. The amount you put down affects your monthly costs and your financial future. Did you know it can save you tens of thousands of dollars in interest?

The National Association of Realtors® 2022 Profile shows first-time buyers often pay just 6% down. This is much less than the old 20% rule. Housing prices have gone up a lot, making 20% seem hard to reach for many.

“The right payment amount isn’t about following rules—it’s about matching your financial situation to your housing goals,” I tell my clients. I’ve helped hundreds of buyers make this choice. It affects every part of buying a home.

Your choice affects whether you’re buying a starter home or forever home. Each path needs a different financial plan. Neither is always better—it depends on your situation and the market.

Quick hits:

- Lower upfront costs mean higher monthly payments

- Twenty percent down eliminates mortgage insurance

- Market conditions influence optimal strategy

- Emergency savings should remain untouched

- Lenders offer various payment requirement options

Initial savings requirement comparison and timeline

The size of your down payment goal is key. It decides how fast you can move from renting to owning a home. This time difference is often overlooked by buyers debating down payment sizes.

A 20% down payment on a $300,000 home means you need $60,000. But a 3% down payment is just $9,000. This $51,000 difference means more years of saving for most families.

In Greenville, buyers save about $450 a month toward their down payment. Saving for 20% takes 11 years. But saving for 3% takes only 20 months.

Home prices go up 3-5% a year. So, a $300,000 home today might cost $345,000 in three years.

Many first-time buyers find saving for a down payment hard. Over a quarter say it’s the hardest part of buying a home. This is why many choose lower down payments, even if they cost more in the long run.

Down payment help can speed up your savings. In South Carolina, first-time buyers can get up to $10,000. This can save months or years.

Every month you rent, you build equity for someone else. But if you buy with 3% down, you build $450 in equity right away.

Your savings plan should think about market growth and your rent vs. own choice. Let’s look at how different down payments affect your timeline:

| Down Payment Option | Amount Needed ($300K Home) | Months to Save ($450/month) | Home Value After Saving Period* | Rent Paid During Saving Period |

|---|---|---|---|---|

| 3% Down | $9,000 | 20 months | $315,000 | $25,000 |

| 5% Down | $15,000 | 33 months | $324,500 | $41,250 |

| 10% Down | $30,000 | 67 months | $348,000 | $83,750 |

| 20% Down | $60,000 | 133 months | $399,000 | $166,250 |

*Assumes 3% annual home price appreciation

Assumes $1,250 monthly rent

U.S. home prices climbed 4.5 % between Q4 2023 and Q4 2024; waiting years to save a larger down payment means chasing a market that may outpace your savings rate. Ref.: “Federal Housing Finance Agency. (2025). U.S. House Prices Rise 4.5 Percent Over the Prior Year: House Price Index Report Q4 2024.” [!]

This table shows a key point: waiting for 20% down changes the financial picture. The home you can afford with 3% down might be too expensive by the time you save 20%.

Many clients are surprised by payment help options. For example, an FHA loan with 3.5% down might get you $5,000 in help. This means you only need $5,500 for a $300,000 home.

The real question is “how soon?” Your choice should weigh immediate benefits against long-term costs. We’ll look at this more in the next section.

Monthly mortgage payment differences modeled

Your down payment choice affects your monthly mortgage payment. It also changes your financial journey. Let’s look at how different down payments impact your monthly budget and long-term finances.

I’ve used today’s market to model a $350,000 home purchase. With a 20% down payment ($70,000), your monthly payment is $1,767. If you choose 5% down ($17,500), your payment jumps to $2,107. That’s a $340 difference every month.

This monthly payment gap adds up over time. With 20% down, you save $4,080 a year. This money can fund a vacation, boost retirement, or cover home repairs. Over five years, you’d save $20,400.

But it’s not just about the payment size. With 5% down, you borrow $52,500 more. At 6.5% interest, you pay about $115,000 more in interest. This is a lot of money that could grow your net worth.

| Down Payment | Loan Amount | Monthly P&I | Monthly Savings | 5-Year Savings |

|---|---|---|---|---|

| 5% ($17,500) | $332,500 | $2,107 | $0 | $0 |

| 10% ($35,000) | $315,000 | $1,995 | $112 | $6,720 |

| 15% ($52,500) | $297,500 | $1,881 | $226 | $13,560 |

| 20% ($70,000) | $280,000 | $1,767 | $340 | $20,400 |

Many first-time buyers don’t see how down payment affects their monthly payments. When I talk to clients, I show them these numbers. They see how their down payment choice changes their monthly payments.

Amortization Schedule Effects on Equity

Your down payment choice changes your monthly payment and how fast you build equity. This is where the long-term impact really shows.

With a 20% down payment on a $350,000 home, you build about $4,800 in equity in the first year. With 5% down, you build about $3,900 in equity. This is because more of your payment goes to interest with a smaller down payment.

This equity gap grows over time. By year five, the 20% down payment gives you about $17,000 more equity. This advantage grows as you own the home longer.

The reason is simple: with a smaller loan, more of your payment goes to principal from the start. For example, with 20% down, about 31% of your first payment reduces principal. With 5% down, only 24% does.

When I show clients their side-by-side amortization tables, they’re often shocked to see how much more of their payment goes to interest with a smaller down payment. That visualization makes the abstract concept of amortization suddenly very real.

Remember, equity building speeds up as your principal balance goes down. The early years of your mortgage are mostly interest payments. But this effect is bigger with smaller down payments.

For many clients, seeing these numbers helps them make better decisions about down payments. Some wait to save more, while others prefer the higher monthly payment to get into the market sooner.

The key is understanding that your down payment choice is about your future finances. By looking at these payment and equity differences upfront, you can choose a down payment that fits your short-term budget and long-term goals.

Private mortgage insurance triggers and costs

Understanding PMI is key when choosing down payments. PMI is needed for loans under 20% to protect lenders. It doesn’t help you, but the lender.

PMI costs range from 0.5% to 1.5% of your loan yearly. This depends on your credit and down payment. It’s a big monthly cost that affects your budget.

Let’s say you buy a $350,000 home with 5% down. Your loan is $332,500. You’ll pay $138 to $415 monthly for PMI, plus your mortgage.

| Down Payment | Loan Amount | PMI Rate | Monthly PMI Cost | Annual PMI Cost |

|---|---|---|---|---|

| 5% ($17,500) | $332,500 | 0.5% | $138 | $1,662 |

| 5% ($17,500) | $332,500 | 1.0% | $277 | $3,325 |

| 5% ($17,500) | $332,500 | 1.5% | $415 | $4,987 |

| 10% ($35,000) | $315,000 | 0.5% | $131 | $1,575 |

| 15% ($52,500) | $297,500 | 0.5% | $124 | $1,487 |

Your credit score affects PMI rates. Scores above 760 might get lower rates. Improve your credit score before applying for a mortgage.

PMI Cancellation Thresholds Across Lenders

PMI can be canceled when your loan balance is 78% of the original price. You can also ask for cancellation at 80% through payments and home value increase.

Lenders have different rules for canceling PMI. Some need an appraisal, while others use computer models. Most want at least two years of on-time payments.

- Some lenders require a new professional appraisal ($300-500) to verify your home’s current value

- Others use automated valuation models to estimate your home’s worth without an in-person appraisal

- Most require at least two years of on-time payments before considering early termination

- Some have minimum equity thresholds higher than 20% for certain property types or loan programs

The Homeowners Protection Act mandates automatic PMI termination at 78 % LTV and allows borrowers in good standing to request cancellation at 80 % LTV—often shaving years off PMI payments. Ref.: “Consumer Financial Protection Bureau. (2023). When Can I Remove Private Mortgage Insurance (PMI) from My Loan? CFPB.” [!]

I’ve helped clients cancel PMI in 2-3 years in good markets. One client in Greenville had a 15% increase in their home’s value by 2022. They removed PMI, saving $189 monthly.

Document your home’s value increase and ask for PMI cancellation. Don’t wait for your lender to tell you. Check your equity yearly.

“read more: Rent to own home basics for budget constrained buyers“

Impact on Cash Reserves Post Closing

Keeping more cash after closing is a big plus of smaller down payments. It gives you financial freedom for repairs and emergencies.

With a 5% down payment on a $350,000 home, you keep $52,500. This is a big safety net for repairs, job loss, and emergencies.

- Unexpected home repairs (new HVAC systems average $5,000-$10,000)

- Job loss or income reduction (3-6 months of mortgage payments)

- Medical emergencies not covered by insurance

- Home improvements that increase your property value

Don’t stretch to make a 20% down payment. It can leave you with no cash for emergencies. One client used credit cards for a $7,800 plumbing emergency after depleting their savings.

Consider PMI costs and how long you’ll pay them. In fast-appreciating markets, you might only pay PMI for 2-4 years, making smaller down payments more attractive.

PMI is tax-deductible for many homeowners with incomes under $100,000. This can lower its cost. Talk to your tax advisor to see if you qualify.

Investment opportunities for leftover capital

Choosing a small down payment lets you keep money for other things. This is smart for home buyers. It’s not about spending less on your home. It’s about using your money wisely.

For example, on a $350,000 home, a 5% down payment leaves you with $52,500. This is money you can use for other things. Your lender might want you to put down more. But think about your other goals.

This money can be used for other investments. Even if your mortgage is 6%, other investments might give you more returns.

I always tell my clients: “Your home is both a place to live and an investment, but it shouldn’t be your only investment.”

Many first-time buyers are surprised by how this money can grow. If you put it in a mix of investments, it could grow to $73,500 in five years. Your home will also gain value.

Using a small down payment lets you build wealth in many ways. Clients have used their money for:

- Home improvements that increase value

- Starting retirement accounts

- Creating emergency funds

- Starting side businesses

- Investing in education

Qualifying for a loan with a small down payment means you keep your money flexible. This is great for first-time buyers who haven’t built a big investment portfolio yet.

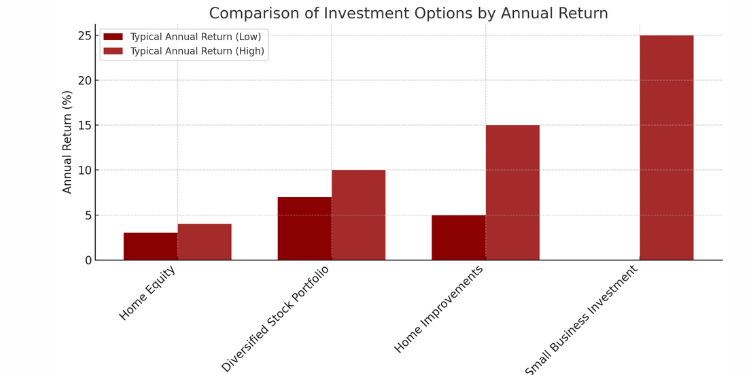

Here’s a look at how your money could grow in different ways:

| Investment Option | Typical Annual Return | Liquidity Level | 5-Year Growth on $50,000 | Risk Level |

|---|---|---|---|---|

| Home Equity (Additional Down Payment) | 3-4% (Historical Home Appreciation) | Low | $58,000-$61,000 | Moderate |

| Diversified Stock Portfolio | 7-10% | High | $70,000-$80,500 | Moderate-High |

| Home Improvements (Strategic) | 5-15% (In Home Value) | Low | $63,000-$100,000 | Varies |

| Small Business Investment | 0-25%+ | Low | Varies Widely | High |

DATA-BACKED STRATEGY:

A diversified stock portfolio has historically returned about 10 % per year, far outpacing the average 4–5 % annual rise in home values—so investing surplus cash instead of locking it all in equity can accelerate long-term wealth. Ref.: “Investopedia Staff. (2015). Has Real Estate or the Stock Market Performed Better Historically? Investopedia.” [!]

Last year, a client put down 10% on a $300,000 home. She used the $30,000 for investments and home improvements. In 18 months, her investments grew 12% and her home’s value went up 5%.

Your lender only looks at the loan, not your whole financial picture. They want you to put down more to reduce their risk. But think about your whole financial situation, not just the loan.

First-time buyers often choose a 6-7% down payment. They know keeping money flexible is important. It’s not always best to put down as much as you can.

The right down payment is the one that helps you financially. Some of my clients put down just enough to get good loan terms. Then they use their money for other things.

Risk tolerance and emergency fund sizing

Knowing how much to save for a down payment is key. It depends on how you feel about risk. I’ve helped many first-time buyers make this choice, and it’s different for everyone.

Choosing a down payment shows how you feel about risk. Some like to keep their payments low. Others want to save for emergencies.

One client put 20% down to avoid PMI. But then their HVAC broke, costing $7,800. They had to use credit cards, causing financial trouble for years.

Homeowners need more savings than renters. Renters can count on their landlord for big repairs. Homeowners can’t.

“read also: House hacking first home guide for new buyers”

Emergency Fund Guidelines for Homeowners

Experts say keep 3-6 months of expenses in savings. But homeowners might need more. Think about these things when deciding:

- Home age and condition

- Expected lifespan of major systems

- Property risks like flooding

- Job stability and income

- Other income sources

First-time buyers usually put down 6-7% of the home price. This is often a choice to keep money liquid, not a limit.

Every dollar for a down payment is one you can’t use for emergencies or other goals. Think about this when deciding.

Stress Testing Budget Against Income Shocks

Test your budget with different scenarios before deciding on a down payment. This shows how strong you are financially.

Ask yourself these questions:

- Can you pay your mortgage if you lose income for 90 days?

- What if property taxes go up 15%?

- How would a $5,000 home repair affect you?

- Can you handle a big increase in homeowner’s insurance?

- What if utility costs go up a lot?

Understanding loan options helps match your down payment to your risk level. Loans have different down payment needs:

| Loan Type | Minimum Down Payment | Key Eligibility Factors | Best For |

|---|---|---|---|

| Conventional | 3-5% | Credit score 620+, stable income | Buyers with good credit and steady employment |

| FHA | 3.5% | Credit score 580+, debt-to-income ratio limits | Buyers with lower credit scores or higher debt ratios |

| VA | 0% | Military service eligibility | Qualified veterans and service members |

| USDA | 0% | Rural property location, income limits | Moderate-income buyers in qualifying rural areas |

Many states have programs to help first-time buyers. These can give grants or low-interest loans for down payments.

Government-backed mortgages—such as VA loans with 0 % down and no PMI—let qualified buyers enter the market sooner while preserving cash for repairs and reserves. Ref.: “U.S. Department of Veterans Affairs. (2025). VA Home Loans – No Downpayment Required.” [!]

Make a risk assessment matrix for yourself. Consider your job, extra money, and support networks. Also, think about your home’s maintenance needs. This helps you decide on a down payment.

Remember, the down payment you can get from a bank isn’t always what you can afford. It’s about balancing your monthly payment and keeping enough money for emergencies.

Read More:

Break even analysis for down payment choices

When picking down payment options, knowing your break-even point helps. Let’s say you’re buying a $350,000 home. The difference between 5% and 20% down is $52,500.

This bigger down payment means saving about $340 a month. That’s $4,080 a year. To find out when you break even, divide your extra down payment by your yearly savings: $52,500 ÷ $4,080 = 12.9 years.

The type of mortgage you choose and current rates change this time a lot. At 4% interest, it takes 17 years to break even. At 8%, it’s only 10 years.

If you have equity in your current home, you can use it for a bigger down payment. First-time buyers should look into payment assistance programs. These can lower upfront costs and keep monthly payments low.

With less than 20% down, your higher monthly payment can help build equity faster. This is true if you stay longer than the break-even point. Remember, the price of the home affects all these calculations.

This choice isn’t forever. You can always make extra payments later when you can. I give clients special calculators. They consider their taxes, how much the home might grow, and other investments.

The best choice is one that fits your life and money situation. It’s about your comfort with debt, your cash flow, and how long you’ll live in the home.

{kind=link}