Nearly 65% of Americans don’t know where their money goes each month. I was one of them until I found a powerful way to change my spending habits. It’s simple: give every dollar a job before you spend it.

A zero-based budget changes how you see money. It makes sure your income minus expenses equals zero. This doesn’t mean you’re broke. It means every dollar has a purpose.

Whether it’s for groceries, savings, or your morning coffee, each dollar has a role. This method is different from traditional budgeting. You don’t just set vague spending limits.

Instead, you make intentional choices about your whole monthly income. The system helps you track your spending after bills and necessities are paid.

By giving funds a purpose, you’ll stop making impulse buys. You’ll also understand your true spending habits. This method is flexible and helps you avoid wondering where your money went at the end of the month.

- A zero-based budgeting system assigns a purpose to every dollar you earn

- This method helps eliminate mystery spending and builds financial awareness

- The approach works for any income level and adapts to your personal priorities

- You’ll gain control over your allowance while enjoying your money

Why giving every allowance dollar a job prevents sneaky overspends

Preventing overspending starts with giving each dollar a job. When I first tried managing my money, cash would disappear without a trace. This is because money without a purpose can easily slip away.

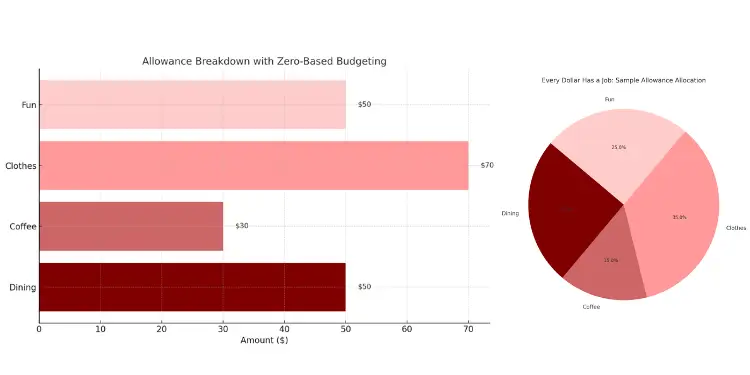

Zero-based budgeting changes how you see money. Instead of saying, “I have $200 to spend,” you say, “I have $50 for dining, $30 for coffee, $70 for clothes, and $50 for fun.” This way, you control your money, not the other way around.

Pre-allocating funds to specific categories in ZBB enhances financial awareness and reduces impulsive purchases by creating a clear spending plan. Ref.: “Mindfully Money. (2022). What is Zero-Based Budgeting and How Does It Work? Mindfully Money.” [!]

Every dollar in your budget should have a name before the month begins. This intentionality is what transforms your financial life from chaotic to controlled.

This method creates barriers against buying things on impulse. If you see something online for $40, you know which budget line it will affect. This pause helps you spend wisely, focusing on what’s truly important.

Following a zero-based budget means every expense must be justified. You decide where your money goes based on your needs, not just habit.

“You Might Also Like: How to Create Zero Budget for Absolute Beginners“

Key Benefits of Assigning Jobs to Your Dollars

- Increased awareness – You notice exactly where your money goes

- Reduced impulse spending – Each purchase requires a category adjustment

- Better alignment with goals – Your money supports what truly matters to you

- Elimination of financial leaks – Those mysterious disappearing funds become visible

- Greater financial confidence – You know exactly what you can afford

Many people spend on things that don’t improve their lives. Zero-based budgeting shows these patterns clearly. One client cut $75 monthly on unused subscriptions, saving for emergencies instead.

| Traditional Budgeting | Zero-Based Budgeting | Impact on Spending |

|---|---|---|

| Starts with income, sets aside some savings | Assigns every dollar a specific purpose | Eliminates the “leftover” money that often disappears |

| Based on previous spending patterns | Based on current needs and priorities | Prevents carrying forward unnecessary expenses |

| Often leaves money unassigned in checking account | Every cent has a job (even saving) | Creates clear boundaries for spending categories |

This method is effective because every dollar must justify its place. Being selective about where your money goes doesn’t mean being cheap. It means spending on what truly adds value to your life.

Your checking account becomes a place of control, not mystery. Every transaction is a choice, not a habit. This shifts you from reacting to money to managing it proactively.

This approach is great for allowance money. By assigning jobs to these dollars, you enjoy your money without regret. You avoid wondering where it all went.

Set allowance amount based on income goals and spending history

Figuring out how much allowance to give needs careful thought. You must look at your income goals and how you spend money. When I first tried zero-based budgeting, I picked a random number. But it didn’t work because it wasn’t based on real numbers.

First, add up all your monthly income. This includes paychecks, side jobs, and benefits. Then, subtract your fixed costs like rent and bills.

What’s left should be split for savings and fun money. ZBB helps you decide how to split it. Experts say 5-15% for fun is good, but you might need more or less.

Zero-based budgeting is special because it makes you justify every expense. It doesn’t just add a little more each month. It looks at each expense from the start.

“Related Articles: What is Zero Based Plan Explained for Novice Budgeters“

Past Three Month Debit Card Review Shows Realistic Figure

The best way to figure out your allowance is to look at your spending history. Check your bank and credit card statements from the last three months. This shows what you really spend, not what you wish you spent.

When I looked at my spending, I was surprised. I was spending almost twice as much on food out and convenience store items. My idea of my spending was way off until I saw the numbers.

Look closely at things like dining out, movies, clothes, and coffee. Add up these costs for each month. Then, find the average. This gives you a clear picture of your spending.

Next, compare this average to your financial goals. If you want to save more or pay off debt, you might need to spend less. If your spending is already low and matches your goals, you might not need to change it.

This method helps you avoid spending more than you need to. Every dollar in your allowance is justified by real data. This helps you make smart choices instead of falling back into old habits.

“The most dangerous budget is the one you set and forget. Zero-based budgeting forces you to question every dollar, every month.”

Your allowance amount can change as your income or goals do. The important thing is to make these changes on purpose. Don’t let your spending grow without thinking about it.

Separate allowance funds from bills using dedicated wallet or app

Starting with a simple step can bring big changes. It’s about keeping your fun money separate from bills. I learned this the hard way, mixing everything in one account and spending too much.

This idea is like having a fence for your spending money. It keeps it from getting mixed up with other money.

The envelope system is a classic way to do this. You put cash in different envelopes for different things. When an envelope is empty, you can’t spend in that category until you get paid again.

Today, you have many ways to keep your money separate, whether you like cash or digital:

- Physical cash envelopes labeled for different categories

- A separate checking account with its own debit card

- Prepaid debit cards loaded with exactly your allowance amount

- Budget-specific apps that digitally recreate the envelope system

This method helps you think more about your spending. It also makes tracking easier because you only need to watch one account.

Utilizing tools like cash envelopes, separate accounts, or budgeting apps effectively enforces spending limits and enhances control over discretionary funds. Ref.: “Ramsey Solutions. (2025). Zero-Based Budgeting: What It Is and How to Use It. Ramsey Solutions.” [!]

“Explore More: How Zero Budget Tracking Works to Stop Random Spending“

Prepaid Debit Cards Work Well For Teens And Adults

Prepaid debit cards are great for both teens and adults. They help you stick to your budget because you can’t spend more than you have. This is perfect for allowance money.

For teens, cards like Greenlight let parents see how they’re doing. It’s a safe way for them to learn about money. Parents can control how much money is loaded and where it can be spent.

Adults can use cards like Chime or Bluebird for the same reason. I switched to one and started making better choices. It’s powerful to see your money go down with each purchase.

These cards also send you updates on your spending. This way, you know right away if you’ve spent too much.

| Separation Method | Best For | Pros | Cons |

|---|---|---|---|

| Cash Envelopes | Visual learners, cash spenders | Tangible, impossible to overspend, no fees | Risk of loss/theft, inconvenient for online purchases |

| Separate Checking Account | Digital spenders who want flexibility | Works everywhere, tracks spending history | Potential bank fees, overdraft possibility |

| Prepaid Debit Cards | Those needing strict spending limits | No overdraft possible, works for online shopping | May have loading fees, limited rewards |

| Budgeting Apps | Tech-savvy budgeters | Real-time tracking, category management | Requires consistent monitoring, some have subscription costs |

Starting with zero-based budgeting? Try different ways to separate your money. Many found success by keeping their allowance separate from bills.

Apps like You Need A Budget (YNAB), EveryDollar, and Mint can help if you don’t like cash or separate accounts. They let you put every dollar into specific categories and track your spending.

The most important thing is to have a clear line between your allowance and bills. This way, your fun money stays safe from being used for emergencies or bills.

Remember, your short-term savings goals can also benefit from this approach. Many budgeters have special spaces for things like vacation funds or holiday gifts.

“For More Information: How Zero Budget Planner Works for Planners Who Iterate“

Track allowance purchases immediately to watch balance shrink responsibly

Recording purchases right away is key to zero allowance budgeting. It makes you aware of your spending. When you buy that $5 coffee, write it down right then.

This way, you don’t waste money on small things. Those $3 snacks and $4 coffees add up. By tracking, you use your money wisely, not wondering where it went.

Seeing your money go in real-time helps you spend smarter. It makes you think twice before buying. Watching your “dining out” money go down shows how fast money can disappear.

While immediate tracking of expenses enhances budget adherence, it requires diligent effort and may be challenging to maintain consistently over time. Ref.: “Fidelity Investments. (n.d.). What is zero-based budgeting and how does it work? Fidelity Investments.” [!]

Daily Check Helps You Decide Whether Coffee Fits Budget

Checking your balance daily turns budgeting into a smart choice. If you’ve spent $35 of your $50 for restaurants, you can plan better. This helps you decide on social plans.

This isn’t about cutting back. It’s about knowing what you’re doing with your money. Many people struggle because they don’t see their spending. Daily checks help you make better choices, like choosing coffee at home.

Make tracking easy so it becomes a habit. Choose something that fits your life. The goal is to track every purchase, big or small.

| Tracking Method | Pros | Cons | Best For |

|---|---|---|---|

| Budgeting Apps (YNAB, Mint) | Automatic import, real-time balance, category tracking | May cost money, requires smartphone | Tech-savvy users who prefer automation |

| Notes App | Free, always with you, simple to use | Manual entry, limited reporting | Casual trackers who want minimal friction |

| Pocket Notebook | Works offline, creates physical awareness | Easy to forget, manual calculations | Visual learners who prefer writing things down |

| Spreadsheet | Highly customizable, detailed reports | Less convenient on-the-go | Detail-oriented people who love data analysis |

Tracking right away helps you spend less on impulse. Seeing your money go down makes you think more about what you buy. This way, you spend on what you really need, not just want.

Checking your budget daily also helps you adjust. You can move money between categories as your needs change. This keeps your long-term goals safe while letting you adapt to life.

Tracking your money also changes how you feel about it. Instead of feeling trapped, you feel in control. This makes spending a thoughtful choice, not just a habit.

“Check This Out: Best Zero Budgeting Tools for Hassle Free Planning“

Use midweek balance check to decide spend save or pause

Your zero allowance budget needs a midweek check. This check helps you decide how to spend your money. I suggest doing it on Wednesday.

Wednesday is great because it’s between weekends. This way, you can see your spending patterns. And you can make changes before the weekend.

When you check your balance, you might face three choices. Each choice needs a different action. Let’s look at what to do in each case:

When You’re On Track

If your balance is good, you have choices. You can keep spending as planned. Or, you can save some money or treat yourself.

Checking your balance helps you make smart choices. It stops you from buying things on impulse. This way, every dollar is used wisely.

When Funds Are Running Low

If your balance is low on Wednesday, you can make changes. You might eat lunch at home or have a movie night in. These small changes can help you stretch your money.

Being flexible with your budget is important. If you spent more on dining out, you can cut back on other things. This way, you use every dollar wisely.

“Learn More About: How Zero Budgeting Reset Works for Monthly Money Sanity“

When a Category Is Depleted

Sometimes, you might find you’ve spent all your money in a category. You have to decide what to do. You can pause spending in that category or move money from another category.

This system is like the cash envelope system but more flexible. If you move money, do it on purpose. For example, you might take money from your clothing budget to your dining budget.

“The midweek check prevents the all-too-common problem of realizing on the 25th that you spent your entire month’s allowance in the first three weeks.”

Keeping a small “buffer” category for unexpected things is helpful. This way, you can handle emergencies without breaking your budget.

This approach makes budgeting empowering. It’s not just about cutting back. It’s about making choices that matter to you. Whether it’s saving for a trip, paying off debt, or enjoying a special dinner.

If you find some spending categories hard, your midweek check can help. Maybe you need to adjust your coffee budget or spend more on social activities. Use this information to improve your budget next time.

“Read More:

Reset allowance at chosen interval and reflect on spending choices

The last step in your zero allowance budget is setting a regular reset day. Most people choose this day to match their paychecks. This could be weekly, bi-weekly, or monthly.

On this reset day, you get to learn from your spending habits. Look at which spending categories ran out first and which had leftovers. The cash envelope system works best when you adjust based on real patterns.

Did you need more for groceries but had extra in your entertainment fund? Your next budget can reflect that. This way, you make sure every dollar you earn works harder.

Ask yourself: “Did my spending match what I truly value?” This honest check keeps you free from broke periods between paychecks.

For those with irregular income from a side hustle or freelance work, try using last month’s earnings to fund this month’s allowance. You’ll need a one-month buffer first, but it creates stability.

Building a budget this way might seem challenging to implement at first. The payoff comes when you’re confidently paying off a credit card or watching savings grow. Each reset gets easier as you learn exactly what you want to allocate for each category.

Zero-based budgeting, originally developed for corporate financial planning, has been adapted for personal finance, helping individuals assign purpose to every dollar and gain control over their spending habits. Ref.: “The Guardian. (2024). ‘Every penny has a purpose’: the rise of zero-based budgeting. The Guardian.” [!]

Your money or spending plan becomes more accurate with each cycle. The zero allowance system encourages you to use every dollar intentionally – not perfectly, but purposefully. That’s the real win.

{kind=link}