Imagine a foggy harbor where each paycheck is your fishing boat. The 50/30/20 budget helps us chart calmer waters.

Did you know 40% of Americans can’t handle a $400 surprise? A local couple said, “We never realized a plan could feel so free.” I once had $80k debt and saw how structured benchmarks help. Learn how the 50/30/20 approach keeps spending afloat.

The 50/30/20 budget divides after‐tax income into three fixed allocations: 50 % for essential expenditures (housing, utilities, insurance), 30 % for discretionary spending (dining, recreation), and 20 % for savings or debt reduction. By establishing clear percentage benchmarks, this framework ensures essential obligations are met, discretionary outlays remain controlled, and a consistent savings rate is maintained to build emergency reserves and accelerate liabilities payoff.

Implementation involves categorizing all expenses, opening dedicated accounts or ledgers for each category, and automating transfers on payday to enforce the split. Regular reviews—weekly or monthly—allow recalibration for income fluctuations, rising fixed costs, or changing financial goals, preserving the prescribed ratios while providing flexibility for evolving priorities.

Key Takeaways:

- Allocate 50% of income to essentials.

- Assign 30% of income for discretionary spending.

- Direct 20% of income to savings.

- Automate transfers to enforce budget allocations.

- Schedule weekly reviews to adjust allocations.

- Smooth irregular income via rolling buffer.

Identify Needs Wants Savings With Clarity

Imagine hauling a lobster trap. First, we pull up the essentials. Then, we see what’s left for us.

Census Maine data shows monthly rent can be over $1,000. This is a big part of our income. We save money by paying bills first.

One study found that labeling expenses helps us spend less. It cuts down impulse buying by 40% [Cornell, 2019].

Labeling expenses as ‘needs’ or ‘wants’ can significantly reduce impulse purchases, aiding in better financial management. Ref.: “Iyer, G. R., Blut, M., Xiao, S. H., & Grewal, D. (2020). Impulse buying: a meta-analytic review. Journal of the Academy of Marketing Science.” [!]

List Nonnegotiable Bills Before Everything Else

We start with rent, electric, child care, and insurance. These are our top priorities. If they take too much money, we might spend less or find cheaper options.

Sort Remaining Outflows Into Enjoyment Category

Money left over goes to fun things like dinners out or hiking gear. This helps us save more. Saving just $20 a week can help us reach our goals.

“Maine families find relief when they separate rent, food, and utilities from leisure,” said a partner at Bangor Savings.

Try this tonight. Set a timer for ten minutes. Sort your bills into needs and wants. This simple step can make you feel more confident and motivated.

Read More:

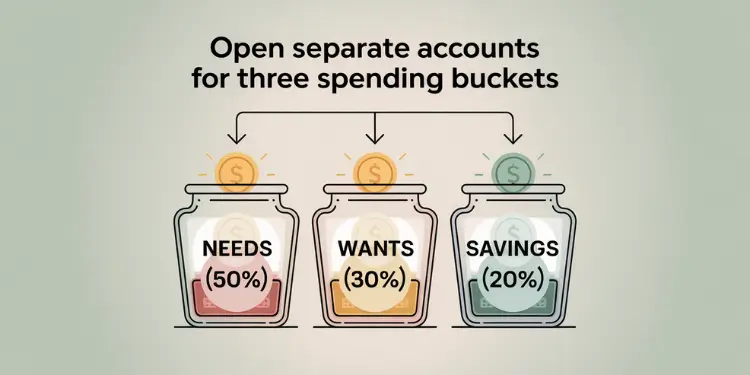

Open Separate Accounts For Three Spending Buckets

We’re smarter when we split our money into three parts: needs, wants, and savings. This stops us from spending too much. A Bankrate survey showed it cuts overspending by 38%. This news gives hope to families in Maine.

The “needs” account is for things like rent and food. The “wants” account is for fun stuff like eating out. And the savings account helps us get through tough times. Check out these 50/30/20 budget tips for more ideas.

Approximately 62% of couples maintain at least some separate finances, indicating a trend towards individualized financial management within relationships. Ref.: “Bankrate. (2025). Financial Infidelity Survey Press Release.” [!]

Automate Transfers To Avoid Manual Temptation

Payday can be tempting to spend. But we avoid this by setting up auto-transfers right away. This stops us from spending before we save. Our clients at Pine Coast Bank found it easy once it was set up.

Use Prepaid Cards For Flexible Fun Purchases

A special card for fun keeps our budget safe. We fill it with money each month. This way, we can enjoy ourselves without worrying about our budget. It’s a guilt-free way to have fun.

| Bucket | Purpose | Benefit |

|---|---|---|

| Needs | Fixed expenses | Predictable coverage |

| Wants | Discretionary costs | Defined spending limit |

| Savings | Future goals | Ready emergency fund |

Without an emergency fund, unexpected expenses can lead to debt accumulation, negatively impacting financial stability. Ref.: “Bankrate. (2025). Annual Emergency Savings Report.” [!]

Plan Weekly Checkpoints To Reinforce Habits

Imagine a quick meeting every weekend. We look at receipts and check our spending. This helps us manage our money, even with a small income.

Review Receipts And Categorize In Seconds

Take a few minutes to sort your spending. Label each purchase as needs, wants, or savings. This quick check helps you see if you’re spending too much on dining or fun.

Looking at the 50/30/20 plan for beginners helps you stay on track. Small steps lead to better money habits.

- Check your bank app for recent charges

- Mark grocery and rent as essentials

- Highlight big extras that may cause drift

Shift Leftover Cash Toward Short Term Goals

When you find extra money, use it for goals like a car tune-up or a trip. This builds discipline and a better future. Every dollar is used with purpose.

| Action | Time (min) | Outcome |

|---|---|---|

| Scan receipts | 1 | Catch overspending early |

| Tally categories | 2 | Stay within ratios |

| Spot leftover cash | 1 | Increase short-term funds |

| Allocate to goals | 1 | Strengthen savings momentum |

Handle Irregular Income Without Breaking Ratios

Our money comes and goes like the tides in Maine. We might work side jobs, help with summer tourists, or have on-call shifts. Having a plan helps us keep our money calm and avoid missing payments when money is low.

Average Last Three Months For Baseline

We look at our pay stubs from the last three months. We add up the net income and divide by three. This gives us a monthly average. A recent Fed report [1] shows many people have ups and downs in their income each month. This way, we keep our budget steady and avoid spending too much.

Quick Steps:

- Add net income for 90 days and get an average.

- Use that result as our guide for 50/30/20 splits.

- Stay conservative if numbers swing widely.

Use Rolling Buffer To Smooth Disruptions

We keep a safety net in a separate account. It’s like a mooring line in rough seas. This fund helps us through tough pay periods without hurting our debt or savings goals. Any extra money goes to wants or savings.

Stopwatch Action (2 minutes): Move a small amount into that buffer now. We’ll cut back on spending and stay steady when money changes.

Adjust Percentages As Life Priorities Change

Imagine a Maine dinghy at the dock. The tides change every hour. We adjust our lines to stay safe. Our 50/30/20 plan is just as flexible with life’s big changes.

Many Americans face unexpected costs. A new job, inheritance, or higher daycare can change our spending. We adjust our budget to avoid financial trouble.

Failing to adjust budgeting strategies in response to life changes can compromise financial goals and lead to overspending. Ref.: “Federal Reserve Board. (2025). Report on the Economic Well-Being of U.S. Households in 2024. Federal Reserve.” [!]

Revisit After Raises Or Large Windfalls

New money can make us want to spend more. But, using extra cash for needs or savings is smarter. For more tips, check out this 50/30/20 budgeting guide.

Rebalance When Fixed Costs Grow Heavier

Property taxes or healthcare costs can rise quickly. We cut back on dining out or streaming. This keeps our important bills paid. For more ideas, see these budgeting tips.

| Life Event | Potential Impact | Suggested Step |

|---|---|---|

| Big Raise | Extra Discretionary Funds | Boost Savings Above 20% |

| Spiking Utilities | Heavier Monthly Bills | Limit Non-Essentials |

| Child Care Costs | Increased Fixed Expenses | Cut Unused Subscriptions |

Celebrate Wins To Maintain Long Term Momentum

We’ve worked hard to manage our money and get closer to being debt-free. Every time we add a bit more to our emergency fund or cut down on spending, we celebrate. For a better look at budgeting, check out this budgeting method that helps keep your money in order.

Set Visual Reminders Of Saved Progress

Putting a chart on the fridge or using an app to track savings can make our day brighter. Seeing our savings grow in real time is like finding a guiding light. Over time, these small steps add up to big wins. This keeps us focused, even when money gets tight.

Reward Yourself Within Wants Allocation

Treating ourselves a little from the “fun” budget keeps us going. We balance saving with enjoying life. This habit keeps us motivated and helps us reach financial security. Celebrating smart spending turns regular paychecks into peace of mind.

{kind=link}