A 401k plan is a powerful retirement tool. Did you know Americans hold over $7 trillion in 401k assets? To understand How to set up 401k is crucial for self-employed individuals and small business owners. How can you maximize this retirement savings vehicle?

Establishing a 401k plan, evaluating available options, and implementing effective strategies will help you leverage tax advantages and compound growth to build substantial wealth for your retirement years.

- 401k plans offer significant tax advantages for retirement savings

- Solo 401k allows self-employed to contribute as both employer and employee

- Choose between traditional and Roth options

- Automate contributions and rebalancing for consistent growth

- Diversify investments beyond company stock to manage risk

- Maintain compliance with IRS regulations to preserve tax benefits

What is a 401k Plan?

A 401k plan is a retirement account that allows employees and self-employed individuals to save for retirement with tax advantages. It’s a type of defined contribution plan, where retirement savings depend on the plan contribution and the earnings on those contributions. There are different types of 401k plans, including traditional 401k and Roth 401k options.

Types of 401k Plans for Self-Employed Individuals

Self-employed individuals have several 401k plan options designed to maximize retirement savings while offering tax advantages. The main types of 401k plans available include:

- Solo 401k (Individual 401k)

- Traditional Solo 401k

- Roth Solo 401k

- Self-employed 401k with profit sharing

- Individual 401k with Roth option

Advantages of Opening a 401k

Opening a 401k plan offers numerous benefits that can significantly enhance your retirement savings strategy and financial security. The following table outlines the key advantages for each type of 401k plan:

| Advantage | Traditional 401k | Roth 401k | Solo 401k |

|---|---|---|---|

| Tax Treatment | Pre-tax contributions reduce current taxable income | After-tax contributions with tax-free withdrawals in retirement | Can be structured as either traditional or Roth for flexible tax planning |

| Contribution Limits | High annual limits with catch-up contributions for those 50+ | Same high limits as traditional with catch-up options | Highest contribution potential as both employee and employer |

| Employer Contributions | Available through employer match or profit sharing | Available through employer match or profit sharing | Self-employed can contribute as both employee and employer |

| Investment Growth | Tax-deferred growth until withdrawal | Tax-free growth if qualified distribution rules are met | Tax-deferred or tax-free growth depending on plan type |

| Withdrawal Flexibility | Required minimum distributions at age 73 | No RMDs during account owner’s lifetime | Flexible withdrawal options with RMDs for traditional portion |

| Loan Options | May allow loans against account balance | May allow loans against account balance | Typically allows loans when plan permits |

The IRS has officially set the 2024 employee contribution limit for 401k plans at $23,000, with an additional $7,500 catch-up contribution allowed for those aged 50 and older. For solo 401k plans, the total combined employer and employee contribution limit is $69,000. Ref.: “Internal Revenue Service. (2023). 401(k) limit increases to $23,000 for 2024, IRA limit rises to $7,000. IRS Newsroom.” [!]

How to set up 401k?

Opening a 401k involves several steps, including the following:

- Choose the right 401k provider by comparing fees, investment options, and customer service.

- Gather required documents including identification, Social Security number, and business registration if applicable.

- Complete the application process either online or via paper forms with personal and financial information.

- Designate beneficiaries and select your initial investment options.

- Review and sign the plan adoption agreement outlining the plan’s rules and regulations.

- Establish contribution methods such as payroll deductions or automated bank transfers.

- Set up ACH withhold authorization for automatic contributions to your retirement account.

- Design your initial investment allocation based on your retirement goals and risk tolerance.

- Complete any required IRS filings and ensure compliance with all regulatory requirements.

- Begin making contributions and regularly monitor and adjust your plan as needed.

Choosing the Right 401k Provider

Selecting the right 401k provider is a crucial decision that impacts your retirement savings for years to come. The provider you choose will affect everything from investment options and fees to customer service quality and plan administration. Making an informed choice ensures your retirement plan operates efficiently and aligns with your long-term financial goals.

Critical factors to consider when evaluating 401k providers:

- Fee structure and expense ratios

- Range and quality of investment options

- Customer service availability and expertise

- Plan administration tools and technology

- Ease of account management and reporting

- Educational resources and retirement planning tools

- Reputation and financial stability of the provider

- Flexibility in plan design and customization options

- Compliance support and regulatory updates

- Integration capabilities with existing business systems

Required Documents to Open a 401k

Opening a 401k plan requires gathering specific documentation to ensure compliance and proper setup. Having these documents ready will streamline the application process and help avoid delays in establishing your retirement account.

Required documents typically include:

- Social Security Number or Tax ID Number

- Government-issued photo identification (driver’s license or passport)

- Proof of address (utility bill or bank statement)

- Business registration documents (for business owners)

- Employer Identification Number (EIN)

- Plan adoption agreement

- Participant information (if applicable)

- Banking information for funding the account

- Beneficiary designation forms

- Previous retirement plan documentation (if rolling over funds)

How to Complete the Application Process

The application process usually involves completing an online or paper form with your personal and financial information. You’ll need to designate beneficiaries and choose your initial investments. If opening a Roth 401k, you’ll need to specify your Roth contribution amounts. Ensure all information is accurate to avoid delays, as this is critical for setting up your retirement plan with the Internal Revenue Service.

Making Contributions to Your 401k

Making contributions to your 401k is essential for building retirement wealth. Understand the contribution limits set by the IRS and consider maximizing your contributions each year. For those aged 50 and over, catch-up contribution options are available. Whether you choose elective deferrals or employer profit sharing, consistent contributions are key to a secure retirement.

“For More Information: Ten Smart Ways to Cut Expenses to Afford House Faster”

Managing Your 401k Plan

Effectively managing your 401k plan is crucial for a secure retirement. Regularly review your investment options and understand the fees associated with your 401k. Consider rebalancing your portfolio periodically to align with your risk tolerance and retirement goals. Stay informed about changes in the 401k plan rules and regulations from the Internal Revenue Service to maximize your retirement savings. The plan document serves as the complete guide to your retirement plan.

Open employer sponsored or solo 401k plan

When establishing a retirement savings strategy, individuals can choose between employer-sponsored 401k plans and solo 401k plans, depending on their employment status and business structure. Employer-sponsored plans are offered by companies to their employees, while solo 401k plans are designed specifically for self-employed individuals with no employees other than a spouse. Understanding the key differences between these options is essential for selecting the most suitable retirement savings vehicle for your specific situation.

| Feature | Employer-Sponsored 401k | Solo 401k |

|---|---|---|

| Eligibility | Employees of companies offering the plan | Self-employed individuals with no employees (or only spouse) |

| Plan Administration | Managed by employer and third-party administrator | Self-administered by the business owner |

| Contribution Types | Employee deferrals, employer match, profit sharing | Employee deferrals + employer contributions (as both roles) |

| 2024 Contribution Limit | $23,000 employee + $7,500 catch-up | $69,000 total ($23,000 employee + $46,000 employer) |

| Setup Costs | Typically covered by employer | $0-$500+ depending on provider |

| Administrative Burden | Minimal for employees | Higher for business owner |

| Loan Provisions | Varies by plan | Typically available |

| Roth Option | Available in many plans | Available with most providers |

| Required Testing | Non-discrimination testing required | No testing required |

| Deadline to Establish | Year-end for effective date | Year-end for effective date |

Compare traditional 401k and Roth solo

Choosing between a traditional 401k and Roth solo 401k requires understanding their fundamental tax differences and how each aligns with your financial situation. The primary distinction lies in when you pay taxes—now with Roth contributions or later with traditional withdrawals. Your current tax bracket, expected retirement income, and future tax rate projections all play crucial roles in determining which option provides greater long-term benefits for your retirement savings strategy.

Traditional 401k plans allow pre-tax contributions, reducing current taxable income, but withdrawals are taxed as ordinary income in retirement. Roth 401k plans use after-tax contributions with no current tax deduction, but qualified withdrawals in retirement are completely tax-free, including all investment earnings. Ref.: “Investor.gov. (n.d.). Traditional and Roth 401(k) Plans. U.S. Securities and Exchange Commission.” [!]

“Explore More: Zero Budgeting vs Percentage Budgeting: Deciding the Better Fit”

Employer of one eligibility requirements

As a self-employed individual or sole proprietor, you may qualify for a solo 401k plan if you meet specific eligibility criteria. These requirements ensure that the plan is designed for those who truly operate as an employer of one, allowing them to maximize retirement savings while maintaining compliance with IRS regulations.

Eligibility requirements for a solo 401k plan include:

- Your business must have no employees besides yourself (and optionally your spouse).

- Can include a spouse as the only other employee

- Must have earned income from self-employment

- Business can be structured as partnership, sole proprietorship, LLC, S-corp, or C-corp

- Must have a valid Employer Identification Number (EIN)

- Cannot have any common law employees who work more than 1,000 hours per year

- Must intend to contribute to the plan in the current year

- Must establish the plan by your business’s tax filing deadline (typically December 31)

To qualify for a solo 401k plan, you must be self-employed with no full-time. Your business can be structured as a sole proprietorship, partnership, LLC, S-corp, or C-corp, and you must have earned self-employment income and a valid Employer Identification Number (EIN). Ref.: “Internal Revenue Service. (n.d.). Retirement plans for self-employed people. IRS.gov.” [!]

“Related Articles: Best Zero Budgeting Tools for Hassle Free Planning”

Complete plan adoption agreement paperwork

Once you’ve chosen a 401k provider, you’ll need to complete the plan adoption agreement paperwork to officially establish your retirement plan. This critical step involves providing detailed information about your business structure, contribution strategy, and designated beneficiaries. Thoroughly reviewing the plan document ensures you understand all terms and conditions, while accurate completion of this paperwork is essential for properly setting up your retirement plan with the financial institution.

Key components of the plan adoption agreement include:

- Business information (legal name, address, EIN)

- Plan effective date and fiscal year

- Eligibility requirements for participants

- Contribution formulas and limits

- Vesting schedules for employer contributions

- Distribution rules and loan provisions

- Designated beneficiary information

- Plan administrator designation

- Signature blocks for authorized representatives

Establish payroll deduction or bank transfers

To contribute to your 401k plan consistently, you’ll need to establish reliable contribution methods that align with your business structure and cash flow. For self-employed individuals, automated systems are particularly valuable for ensuring regular contributions and maximizing your annual retirement savings potential. The right contribution system should seamlessly integrate with your income patterns while making it easy to maintain consistent retirement funding.

| Contribution Method | Best For | Setup Process | Frequency | Advantages |

|---|---|---|---|---|

| Payroll Deduction | Businesses with formal payroll systems | Coordinate with payroll provider | Per pay period | Automatic, consistent, easy to scale |

| Bank Transfer | Self-employed, sole proprietors | Set up with financial institution | Weekly, bi-weekly, monthly | Flexible, control timing, no payroll required |

| ACH Authorization | All business types | Complete authorization form | Custom schedule | Automated, reliable, reduces manual effort |

| Manual Contributions | Irregular income situations | Initiate transfers as needed | Variable | Maximum flexibility, pay when able |

| Check Deposits | Traditional preference | Mail or deliver checks | Variable | Tangible, some prefer paper trail |

Setting up ACH withhold authorization

Setting up Automated Clearing House (ACH) withhold authorization streamlines the process of making contributions to your 401k plan by enabling automatic transfers from your bank account to your retirement account on a predetermined schedule. This automation eliminates the need for manual transfers and ensures consistent funding of your retirement savings. For small business owners and self-employed individuals, ACH authorization provides a reliable way to maintain regular contributions without the administrative burden of manual processing.

Key steps in setting up ACH contributions:

- Complete the ACH authorization form with accurate banking information

- Specify contribution amount and frequency (weekly, bi-weekly, monthly)

- Designate start date for automatic transfers

- Verify bank routing and account numbers to prevent delays

- Set up notifications to confirm successful transfers

- Establish process for updating contribution amounts as needed

- Maintain records of all ACH transactions for tax reporting

- Review quarterly to ensure contributions align with retirement goals

Design investment allocation to match goals

One of the most critical aspects of a 401k plan is the strategic allocation of investments to align with your retirement goals. This involves carefully considering various investment options within your 401k plan assets, such as stocks, bonds, and mutual funds, to create a diversified portfolio.

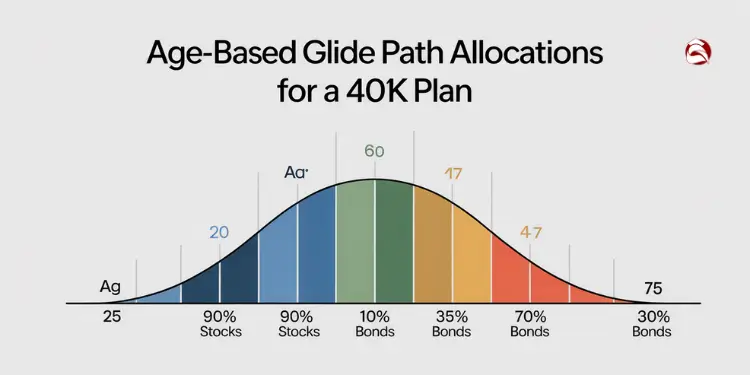

Age based glide path examples explained

Age-based glide paths implement a dynamic investment strategy that progressively modifies your asset allocation as you advance toward retirement. These systematic models transition your portfolio from growth-focused investments with higher volatility to more stable, income-generating assets as you age. This approach strategically reduces investment risk by minimizing exposure to market fluctuations during periods when your timeline for recovering from potential financial setbacks becomes shorter.

Examples of age-based glide path allocations:

- Age 25: 90% stocks, 10% bonds – Maximizing growth potential with a long time horizon

- Age 35: 85% stocks, 15% bonds – Slightly more conservative while still prioritizing growth

- Age 45: 75% stocks, 25% bonds – Beginning to reduce risk as retirement comes into view

- Age 55: 60% stocks, 40% bonds – Balanced approach protecting accumulated savings

- Age 65: 40% stocks, 60% bonds – Conservative allocation focused on capital preservation

- Age 75: 30% stocks, 70% bonds – Income-focused with minimal growth exposure

A glide path is a formula that determines the asset allocation of a target-date retirement fund based on your target retirement age. It automatically shifts from aggressive growth-oriented investments to conservative income-focused assets as you approach retirement, typically reaching its final allocation around age 72. Ref.: “Vanguard. (n.d.). Target-date fund glide path. Vanguard Institutional.” [!]

Avoid concentration in company stock

Automate rebalancing and periodic contribution increases

Automating your 401k management processes helps maintain optimal investment performance and steadily grow your retirement savings. By implementing automated rebalancing and contribution increases, you can ensure your portfolio stays aligned with your financial goals while taking advantage of compound growth opportunities without requiring constant manual intervention.

| Rebalancing Frequency | Best For | Advantages | Considerations |

|---|---|---|---|

| Quarterly | Active investors | Frequent alignment with targets | May trigger unnecessary trades |

| Semi-annually | Most investors | Good balance of responsiveness and stability | Market timing concerns minimized |

| Annually | Long-term investors | Lower transaction costs, tax efficiency | May drift from targets between adjustments |

| Threshold-based (5% drift) | Target-focused investors | Rebalances only when needed | Requires monitoring systems |

Review plan documents for compliance deadlines

Staying compliant with IRS regulations requires diligent attention to your 401k plan documents and their associated deadlines. Regular reviews help ensure your plan maintains its tax-advantaged status and avoids costly penalties that could impact both your business and retirement savings. Critical compliance deadlines to monitor:

| Deadline | Requirement | Consequence of Missing |

|---|---|---|

| January 31 | Distribute Form W-2 to employees | $50 per form penalty, increases with time |

| April 15 | File Form 5500 for small plans | $25 per day penalty, up to $15,000 |

| July 31 | File Form 5500 for large plans | $25 per day, up to $15,000 |

| December 31 | Plan amendments for regulatory changes | Plan disqualification risk |

| Quarterly | Deposit employee deferrals | Excise taxes, plan disqualification |

Annual compliance testing checklist overview

Annual compliance testing is a fundamental responsibility for 401k plan administrators, ensuring the plan meets IRS requirements and maintains its qualified status. These tests verify that your plan doesn’t disproportionately benefit highly compensated employees and that all contributions remain within regulatory limits.

Required compliance tests for 401k plans:

| Test Type | Purpose | Frequency | Correction Deadline |

|---|---|---|---|

| Actual Deferral Percentage (ADP) | Ensures highly compensated employees’ deferrals don’t exceed non-HCEs by specified limits | Annually | 2.5 months after plan year-end |

| Actual Contribution Percentage (ACP) | Tests employer matching and after-tax contributions for fairness | Annually | 2.5 months after plan year-end |

| Top Heavy Test | Determines if key employees own more than 60% of plan assets | Annually | 2.5 months after plan year-end |

| Coverage Test | Verifies plan benefits appropriate percentage of non-highly compensated employees | Annually | 2.5 months after plan year-end |

| Nondiscrimination Test | Ensures plan doesn’t favor highly compensated employees | Annually | 2.5 months after plan year-end |

Setting up a 401k plan is a powerful step toward securing your financial future, whether you’re self-employed or a small business owner. Understanding how to set up a 401k gives you access to significant tax advantages and the opportunity to build substantial retirement savings through options like the solo 401k, traditional 401k, and Roth 401k.

By carefully selecting the right plan, automating your contributions, and staying compliant with regulations, you can maximize your retirement savings potential and create a more secure financial foundation for your golden years. Take action today to leverage these valuable retirement planning tools and build the wealth you’ll need for a comfortable retirement.

A 401k plan is a powerful retirement savings vehicle offering significant tax advantages for both employees and self-employed individuals. Understanding how to set up a 401k is essential for maximizing retirement wealth, with options including traditional, Roth, and solo 401k plans designed to meet different financial situations and goals.

Self-employed individuals can leverage solo 401k plans to contribute as both employer and employee, potentially reaching higher contribution limits. The choice between traditional (tax-deferred) and Roth (tax-free withdrawals) options depends on current versus expected future tax brackets, with proper management and compliance being crucial for maintaining the plan’s tax-advantaged status.

{kind=link}