What if the budgeting approach you’ve trusted for years is actually holding you back? Millions of Americans feel stuck financially—despite budgeting. The solution might be simpler than you think.

As of 2024, nearly 40% of Americans still can’t cover a $400 emergency without borrowing. This shows why managing your after-tax income is key.

Financial expert Dave Ramsey says, “A budget is telling your money where to go instead of wondering where it went.” This wisdom shows why percentage-based budgeting is popular.

I once felt frustrated trying to track every dollar. Then I discovered two budgeting systems that actually worked. They are simple and don’t need complex spreadsheets or tracking every receipt.

These systems divide your take-home pay into simple percentages into categories. One uses three categories: necessities, discretionary expenses, and savings. The other has just two: living costs and savings/investments.

Learning about these frameworks can change how you manage money. It can bring stability to your budget. Let’s see which method fits your lifestyle and goals better.

- Comparing Percentage-Based Budgeting Frameworks

- These percentage-based approaches help ensure consistent saving while maintaining realistic spending expectations

- The right budgeting method depends on your personal financial situation and goals

50/30/20 vs 80/20 Mindsets

When I started helping neighbors with money, I saw a big difference. People choose budgeting styles based on their beliefs, not just math.

The 50/30/20 rule is about balance. It says you should spend on needs, enjoyments, and savings. It’s like eating a meal with all parts: proteins, veggies, and dessert.

The 80/20 method is radically simple. It focuses on saving a lot. It’s for those who don’t like to track every expense. It’s like saying, “Save first, ask questions later.”

The way you budget reflects your values more than your math skills.

The 50/30/20 rule helps with spending. It lets you spend 30% on fun. This way, you don’t feel guilty about enjoying life.

The 80/20 rule is good for those who save easily. It lets you save more without worrying about small expenses.

| Philosophical Aspect | 50/30/20 Approach | 80/20 Approach |

|---|---|---|

| Core Belief | Balance leads to sustainability | Simplicity leads to consistency |

| Decision Framework | Categorize then spend | Save first, spend remainder |

| Mental Load | Higher tracking requirements | Lower tracking requirements |

| Ideal For | Those needing spending guardrails | Naturally frugal individuals |

These views change how you see money. A 50/30/20 person might pick an apartment based on cost. An 80/20 person might choose the cheapest option.

I’ve seen these views in everyday choices. A 50/30/20 person might buy organic food. An 80/20 person might save more by spending less.

Neither way is better. They just show different ways to manage money. The 50/30/20 rule gives structure. The 80/20 rule offers simplicity.

Knowing these differences helps you pick a budget that fits you. The best budget is one you’ll stick to every month.

“Related Articles: How to stick to 50/30/20 budget without constant willpower battles“

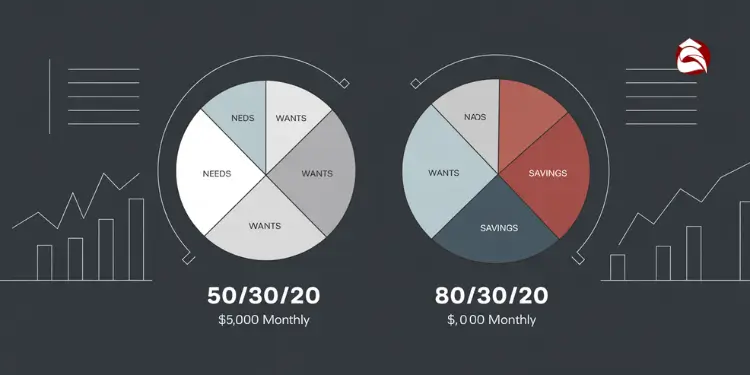

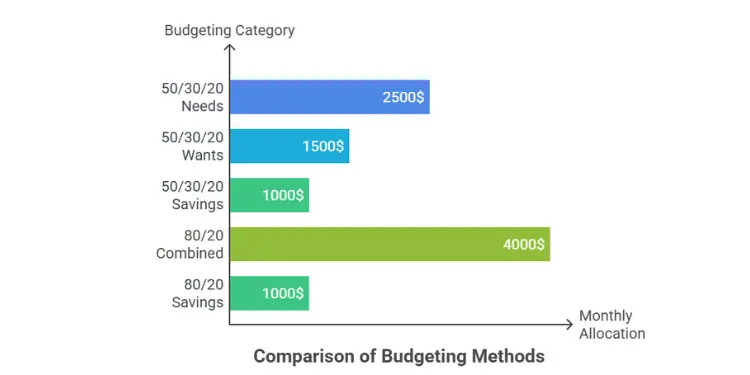

How Each Budget Splits a $5,000 Monthly Income

Both budgeting methods say save 20% of your income. But they handle the rest differently. This affects how you spend money. Knowing these differences helps you pick the best method for you.

Let’s see how each method would spend a monthly income of $5,000:

| Category | 50/30/20 Rule | 80/20 Rule | Key Difference |

|---|---|---|---|

| Needs/Essentials | $2,500 (50%) | Combined $4,000 (80%) | Strict separation vs. flexible allocation |

| Wants/Nonessentials | $1,500 (30%) | Part of the $4,000 | Defined budget vs. discretionary spending |

| Savings/Investments | $1,000 (20%) | $1,000 (20%) | Identical savings goals |

The 50/30/20 rule sets clear spending limits. With $5,000 a month, you spend $2,500 on needs like rent and food. You also have $1,500 for wants and $1,000 for savings.

The 80/20 rule mixes all spending into one pool of $4,000. You decide how to split it between needs and wants, saving $1,000. It’s more flexible but needs discipline in tracking spending.

Daily Spending Behavior Under Each Budget

Your budget affects your daily choices. The 50/30/20 rule sets clear limits for wants. The 80/20 rule lets you decide more.

With the 50/30/20 rule, your $1,500 for wants is about $50 a day. This helps you decide on small treats. You might spend $150 on dining out, $50 on streaming, and $200 on fun each month.

The 80/20 rule is different. You have $4,000 for all expenses. You must balance needs and wants. It’s good if you like flexibility and can resist buying things on impulse.

- Prefer flexibility over rigid category limits

- Have predictable essential expenses

- Can resist impulse purchases without explicit boundaries

- Enjoy adjusting spending priorities throughout the month

- Focus mainly on meeting your savings target

Think about your daily coffee habit. Under the 50/30/20 rule, a $5 coffee is from your wants budget. It’s 10% of your daily discretionary money. You know it fits your plan.

With the 80/20 rule, that coffee is part of your total spending. You might spend more on coffee one week and less the next. As long as you pay bills and save, it’s okay.

The 50/30/20 rule gives structure, reducing spending guilt. You’ve already decided on your wants budget. Daily purchases feel okay.

The 80/20 method lets you adjust spending as life changes. If you have an unexpected car repair, you might cut back on dining out. It feels less like breaking rules.

I switched from the 80/20 to the 50/30/20 rule last year, and the biggest difference was feeling okay to enjoy my ‘wants’ spending without guilt. That 30% is there for a reason – to enjoy life while being responsible.

Both methods aim to save the same amount. The main difference is in daily spending choices. You might prefer clear rules or more flexibility.

“You Might Also Like: 50/30/20 budget example for a typical monthly income“

Using Apps and Automation to Simplify Budgeting

Modern banking tools have made budgeting easy. No more spreadsheets or envelope systems. Today, digital tools automate much of the work.

Apps like Mint, YNAB, and Personal Capital help with the 50/30/20 rule. They sort your spending into needs, wants, and savings. They update your spending in real-time, making tracking easy.

To start the 50/30/20 system, first, find out your take-home pay. Then, decide how much to save and spend. Lastly, set up automatic payments to save money on payday.

Many banks offer free savings accounts. You can have one for daily spending and another for savings. This helps you save for different goals.

- A checking account for daily expenses (needs and wants)

- A high-yield savings account for your emergency fund (part of your 20%)

- A retirement account for long-term savings (another part of your 20%)

The 80/20 rule is even simpler. Just set up automatic transfers to save 20% of your income. This way, you save before you spend.

Financial advisor Maria Chen says, “Automating my savings changed my life. Now, I save 20% before I spend, and I’m more secure than ever.”

Digital banking features like round-up savings can boost your savings. They add small amounts to your savings. For example, if you spend $3.50 on coffee, $0.50 goes to savings. This helps you save more without feeling it.

Both rules work for people with irregular income. Use your average income over six months to set your percentages. Save extra in good months and use your reserves in tough months.

| Implementation Feature | 50/30/20 Rule | 80/20 Rule | Recommended Tools |

|---|---|---|---|

| Account Structure | Multiple accounts recommended (needs, wants, savings) | Two accounts sufficient (spending, savings) | Online banks with free multiple accounts |

| Automation Complexity | More complex (three categories to track) | Simpler (two categories to track) | Automatic transfers on payday |

| Expense Tracking | Detailed tracking needed across categories | Less detailed tracking required | Mint, YNAB, Personal Capital |

| Time Investment | 15-30 minutes weekly to review categories | 5-15 minutes weekly for basic review | Mobile banking apps with alerts |

| Flexibility for Changes | Requires adjustments across three categories | Simpler adjustments between two buckets | Budgeting apps with adjustment features |

Choose a budgeting method that fits your lifestyle. If you like detailed tracking, the 50/30/20 rule might be for you. If you prefer simplicity, the 80/20 rule could be better.

Your budget should make your life easier, not harder. Modern tools aim to simplify your finances. Start simple and add more features as you get more comfortable.

Adapting Your Budget When Income Drops

When your income changes or you face unexpected costs, your budget is tested. Some people panic when their hours are cut. Others adjust their spending calmly because they have a flexible budget.

The 50/30/20 rule helps when your income drops. For example, if you earn $5,000 a month and it drops to $4,000, your spending changes. You spend less on wants and save more.

The 80/20 approach is simple. You save 20% of your income and spend the rest. This is easy when money is tight.

But, the 80/20 rule can be hard. It doesn’t tell you which expenses to cut first. The 50/30/20 rule helps by separating needs from wants.

“Discover More: 50/30/20 budget breakdown of needs, wants, and savings“

How to Keep Saving Even When Money’s Tight

When money is tight, saving is hard. It’s tempting to stop saving. But, saving a little is better than nothing.

Instead of saving 20%, try saving 10% or 5%. This keeps you saving while being realistic.

When your income drops, save for emergencies first. For long-term stress, balance saving for emergencies and retirement.

One client faced a 30% income drop. She didn’t give up on saving. She adjusted her budget to cover costs while saving a little.

| Financial Challenge | 50/30/20 Adaptation | 80/20 Adaptation | Savings Priority |

|---|---|---|---|

| Temporary income drop (1-3 months) | Shift to 60/25/15 temporarily | Maintain 20% savings if possible | Emergency fund first |

| Major expense (medical, home repair) | Reduce wants to 20%, increase needs to 60% | Reduce to 85/15 temporarily | Debt repayment |

| Long-term income reduction | Permanently adjust all percentages | Consider 90/10 until stabilized | Balance emergency and retirement |

| Job loss | Shift to emergency budget (70/20/10) | Reduce to minimal savings (95/5) | Immediate needs only |

An emergency fund is key when income changes. Aim for 3-6 months of expenses. This helps when money is tight.

Both budgeting systems help with debt. In the 50/30/20 rule, debt repayment is part of savings. The 80/20 rule uses the 20% for debt.

When money is very tight, you might pause retirement savings. One family paused 401(k) contributions during a furlough. They started again when income returned.

Financial resilience is about confidence in tough times. Both 50/30/20 and 80/20 rules can adjust. The key is to make smart changes, not give up.

“Further Reading: Should I use 50/30/20 budget or another budgeting method“

What Drives Budgeting Success Willpower or Simplicity?

Good budgeting is more than just numbers. It’s about making your financial plan fit how your brain works. Many friends start with great budgets but give up because they ignore the mind’s role in money.

The 50/30/20 rule helps by making clear mental lines. It stops you from thinking every want is a need. This clear thinking stops small excuses that can ruin budgets.

Every money choice you make uses up your brain power. The 50/30/20 rule makes these choices easier by dividing them into clear groups.

As one financial coach said,

“Most budgets fail not because the math doesn’t work, but because people underestimate how quickly their willpower depletes when facing constant financial decisions.”

The 80/20 rule is simple and helps avoid budget burnout. It’s easy to track just one number, your savings rate. This makes budgeting less stressful.

For those who hate detailed tracking, the 80/20 rule is a lifesaver. Friends who couldn’t stick to zero-based budgeting found success with 80/20. They focused on saving 20% for big goals like retirement or paying off loans.

“Related Topics: Zero budgeting vs percentage budgeting deciding the better fit“

Gamifying Savings Milestones for Engagement

Turning savings into a game can make budgeting fun. Research shows games tap into our brain’s reward system. This makes sticking to habits easier.

For 50/30/20, use a visual tracker for each area. A chart for your savings can give you a boost when you reach your goal. Reward yourself when you hit 20% savings for the month.

When paying off loans, celebrate each milestone. Treat yourself when you pay $1,000 off your debt. This positive feedback helps keep you on track.

The 80/20 rule is easy to gamify. Track your savings streaks and reward yourself for each month. Many apps now offer features for tracking and rewarding these habits.

| Gamification Strategy | 50/30/20 Application | 80/20 Application | Psychological Benefit |

|---|---|---|---|

| Visual Trackers | Separate charts for needs, wants, savings | Single savings progress bar | Provides visual feedback on progress |

| Milestone Rewards | Celebrate when all three categories hit targets | Reward reaching savings percentage | Creates positive reinforcement loop |

| Streak Challenges | Track consecutive months in balance | Count months hitting 20% savings | Builds consistency through commitment |

| Social Sharing | Share balanced budget wins with friends | Celebrate savings milestones publicly | Adds accountability and recognition |

Digital tools make gamifying easy. Apps can track your spending and show your progress in fun ways.

The envelope system can also be made into a game. I’ve seen families use “victory envelopes” for rewards after budget wins.

Everyone is different when it comes to motivation. Some like competition, others like progress bars. Find what works for you.

The best budget isn’t perfect math. It’s one you can stick to. We’re not always rational with money. Choose a budget that fits your mind for lasting success.

“Read More: 50/30/20 vs zero based budgeting complete comparison guide“

Choosing the Budgeting Method That Works for You

Choosing between the 50/30/20 and 80/20 budgeting methods depends on your financial situation. If you have a big mortgage or rent, the 50/30/20 rule helps balance costs. It makes sure you have enough for other needs.

Ask yourself these questions to find the budget that works for you:

Do you enjoy tracking every purchase or prefer automation? The 50/30/20 method helps you keep an eye on spending. It includes debt payments and housing costs.

Is saving for retirement your main goal? The 80/20 rule saves 20% for retirement first. Then, you can spend on other things.

Read More:

Your income stability is important. If your income changes a lot, the 80/20 rule might be easier. It helps you save during tough times.

Think about your housing costs too. If rent or mortgage is more than 30% of your income, you might need to adjust. This way, you can reach your financial goals.

Personal finance is different for everyone. The best plan is one you can follow every day. Test each method for 90 days and track which one supports your lifestyle and savings habits better. See which one helps you reach your goals, like paying off debt or saving for retirement.

{kind=link}