Many people face a tough choice: pay off debt or save for a house. This choice greatly affects how much house you can buy. A small change in mortgage rates can mean thousands more for your home.

43% of Americans find it hard to balance paying loans and saving. Many first-time buyers wait years because of this. The effect on your future wealth is big.

“The smartest path isn’t always the obvious one,” my mentor said. I’ve helped hundreds of first-time buyers. I’ve seen how choosing wisely between debt and savings can greatly change things. Some clients spent thousands more than they had to.

This guide will help you make a plan that works for you. You’ll learn what lenders look at and how your choices today affect tomorrow.

Quick hits:

- Higher credit scores unlock better rates

- Lower monthly payments mean more buying power

- Twenty percent down means no mortgage insurance

- Comparing interest rates shows what’s important

- Your timeline helps decide the best strategy

Current debt burden impact on qualifying

The debt you carry today affects how much house you can buy tomorrow. Many first-time buyers don’t understand this. When I meet with clients, they often focus only on saving for a down payment.

But, their current debt payments can cut their buying power by tens of thousands of dollars. This is something they don’t see coming.

Your debt payments, like credit cards and car loans, are key in deciding if you can get a mortgage. Lenders look at your income and credit score. But they also check how much of your income goes to debt.

I worked with a couple making $8,500 a month. They were shocked to find their $850 in monthly debt payments cut their home buying power by nearly $95,000. This made them wait six months to buy a house while they paid down their debt.

Debt to Income Ratio Benchmarks Explained

Your debt-to-income (DTI) ratio shows how much of your income goes to debt. This ratio decides if you can get a mortgage and how much you can borrow. Lenders look at two DTI figures: housing costs and all debt.

For most loans, a DTI below 43% is best. But, some loans offer more flexibility. Here’s what different DTI levels mean for your mortgage:

- 36% or lower: Ideal DTI for most loan programs with the best rates

- 43% or lower: Maximum for most conventional loans

- 45-50%: May qualify for FHA loans or other programs

- Above 50%: Fewer mortgage options and may need more to qualify

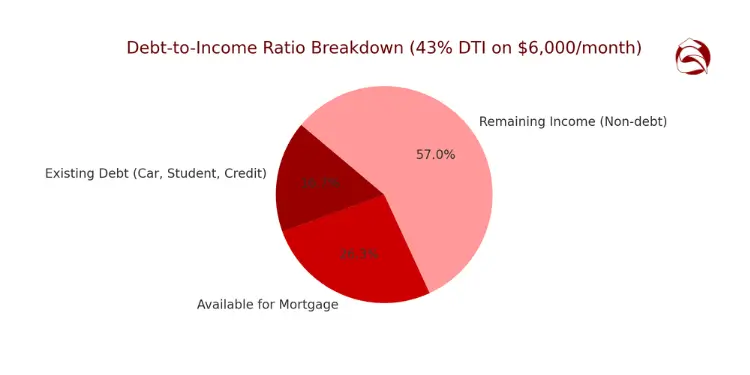

If you make $6,000 a month, a 43% DTI means your total debt payments shouldn’t be more than $2,580. If you already pay $500 for a car loan, $300 for student loans, and $200 for credit cards, that’s $1,000 for debt. You’d have only $1,580 for your mortgage.

Credit utilization also affects your mortgage. Keeping credit card balances low can improve your score. This can qualify you for better rates, saving you money over time.

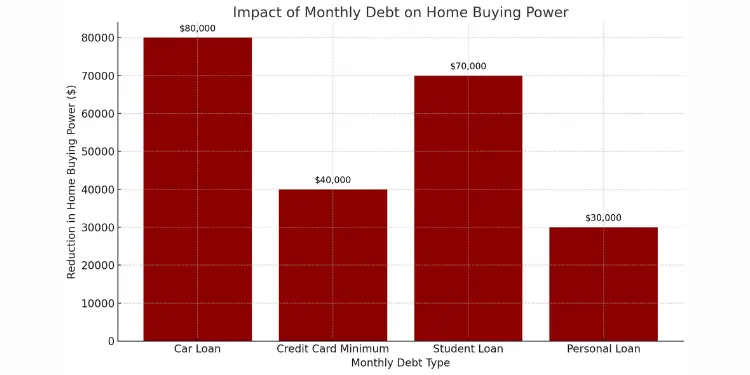

For example, every $100 in monthly debt payments means you can buy $20,000 less house. A $400 car payment cuts your home buying budget by $80,000. This changes how clients manage their debt.

| Monthly Debt Type | Typical Amount | Reduction in Home Buying Power | Better Use of Funds |

|---|---|---|---|

| Car Loan | $400 | $80,000 | Consider a less expensive vehicle |

| Credit Card Minimum | $200 | $40,000 | Pay down to below 30% utilization |

| Student Loan | $350 | $70,000 | Explore income-based repayment |

| Personal Loan | $150 | $30,000 | Prioritize payoff before house hunting |

Buyers often face a choice: save for a down payment or pay off debt? For those with high-interest debt, like credit cards, paying it off can give you more buying power than saving for a down payment.

If your credit utilization is over 30%, focus on paying off debt. This will improve your DTI ratio and boost your credit score. A better credit score can qualify you for lower interest rates, saving you thousands over your mortgage’s life.

Remember to keep emergency savings separate from your down payment fund. Aim for 3-6 months of essential expenses. This prevents new debt if unexpected expenses come up after buying a house.

Down payment size and mortgage insurance

Knowing how your down payment affects mortgage insurance can save you a lot. Buyers often rush into homes without thinking about the long-term effects. Your down payment can change your finances for years.

The down payment size affects two big things: mortgage insurance and how much equity you get right away. These factors can change your monthly budget and how much wealth you build over time.

Loan to Value Thresholds for Premiums

Mortgage insurance helps lenders when you put down less money. The cost of this insurance depends on your loan-to-value ratio (LTV). This is how much of the home’s value you’re borrowing.

For conventional loans, there are clear rules:

- 20% down payment – No private mortgage insurance (PMI)

- 10% down payment – Lower PMI rates and faster removal

- 5% down payment – Most conventional loans with higher PMI costs

- 3% down payment – For first-time buyers with the highest PMI rates

Let’s look at real numbers. On a $300,000 home with 5% down, PMI costs $142-$425 monthly. This goes on until you have 20% equity.

The Homeowners Protection Act requires automatic PMI termination at 78 % LTV and lets borrowers request cancellation at 80 %—plan extra principal payments to hit these triggers sooner. Ref.: “Consumer Financial Protection Bureau. (2012). Homeowners Protection Act (PMI Cancellation Act) Guide. CFPB.” [!]

FHA loans have different rules. They always need mortgage insurance, no matter the down payment. This includes 1.75% upfront and 0.55-1.05% annually. With down payments under 10%, this insurance lasts the life of the loan.

I had clients last year who were $8,000 short of a 20% down payment. By delaying their purchase three months to reach that threshold, they saved over $24,000 in mortgage insurance costs over five years.

Building Equity Speed Versus Liquidity

Choosing a down payment isn’t just about monthly costs. It’s also about building equity versus keeping money liquid. A bigger down payment means more equity but less cash.

Deciding between debt and down payment is strategic. Paying off high-interest debt often gives better returns than increasing your down payment.

Here’s a comparison table:

| Financial Choice | Immediate Benefit | Long-Term Impact | Risk Level |

|---|---|---|---|

| Eliminating debt at 18% interest | 18% guaranteed return | Improved debt-to-income ratio | Low risk |

| Larger down payment | Reduced/eliminated PMI | More initial equity | Medium risk |

| Building an emergency fund | Financial security | Prevents future high-interest debt | Low risk |

| Minimum down payment | Preserves cash reserves | Higher monthly costs | High risk |

If you’re paying high interest on debt, pay that off first. For example, paying off a $5,000 credit card balance at 18% saves $900 a year. This is more than the PMI savings from a bigger down payment.

Qualified Veterans can use VA home loans with 0 % down and no monthly mortgage insurance, preserving cash reserves while maintaining affordability. Ref.: “U.S. Department of Veterans Affairs. (2025). VA Home Loans Overview. VA.” [!]

But, if you’re close to key down payment amounts (5%, 10%, or 20%), aim for those. This can cut or eliminate mortgage insurance costs. This is true if your debt has lower interest rates.

I tell my clients to compare debt interest rates to PMI savings. The higher number shows where to put your money first.

Building equity comes from paying off debt and property appreciation. Sometimes, getting into the market sooner with less down payment is faster. This is true in areas with rising home prices.

Your mortgage application will be stronger with less debt. This can qualify you for better loan terms. This often means a lower monthly payment, even with less down.

“read also: Rent to own home basics for budget constrained buyers“

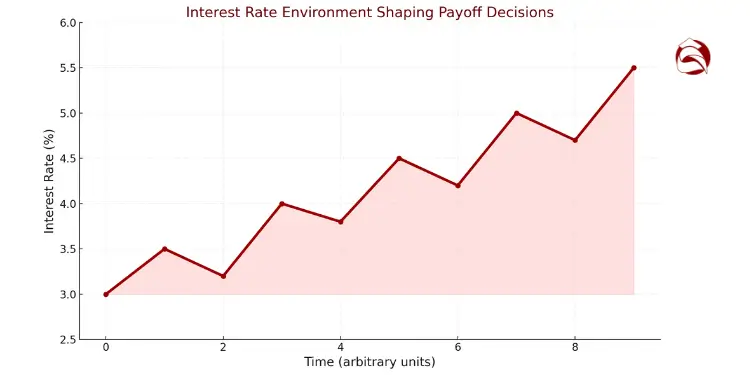

Interest rate environment shaping payoff decisions

When you’re buying a home, interest rates are very important. They can change a lot. This affects how you use your money.

Your credit score affects your mortgage rate. I’ve helped clients improve their scores by 40+ points in 90 days. This saved them tens of thousands in interest.

A 1% difference in mortgage rate on a $300,000 loan means $180 more a month. That’s $64,800 over 30 years. It’s enough for college or retirement.

Interest rates won’t fall fast enough to bail borrowers out of a bad situation. Continue to prioritize aggressive debt repayment.

The Federal Reserve’s policy adds complexity. In rising rates, paying off variable debt is urgent. Credit card rates can go up fast, while mortgage rates move slower.

Zero-percent balance transfer offers can help pay off debt. These rates protect you from high interest. Just watch out for fees and when the offer ends.

Track the difference between your highest debt rate and mortgage rates. If it’s over 5%, pay off debt first. For example, if you have 18% credit card debt and mortgage rates are 7%, focus on the high-interest debt.

Eliminating credit-card balances averaging 21.58 % APR yields a risk-free “return” more than triple today’s 6.81 % 30-year mortgage rate, freeing cash flow and boosting mortgage eligibility. Ref.: “Board of Governors of the Federal Reserve System. (2025). Consumer Credit (G.19) Statistical Release.” [!]; “Freddie Mac. (2025). Primary Mortgage Market Survey – June 18 2025.” [!]

Mortgage interest is tax-deductible, but consumer debt isn’t. This makes paying off high-interest debt even more important. A 7% mortgage might cost you less than 5.5% after taxes.

In falling rate environments, buying a home sooner might be good. But, avoid new debt after buying. I’ve seen clients undo their progress by using credit cards too much.

| Interest Rate Scenario | Debt Payoff Priority | Down Payment Strategy | Long-term Impact |

|---|---|---|---|

| Rising Rates | High-interest variable debt first | Minimum needed for approval | Protects against payment shock |

| Stable High Rates | Any debt above mortgage rate | 20% to eliminate PMI if possible | Maximizes monthly affordability |

| Falling Rates | Debt exceeding 10% interest | Consider smaller down payment | Enables earlier purchase with refinance |

Don’t wait for perfect interest rates. I’ve seen clients wait too long, only to face higher prices. Focus on paying off high-interest debt to improve your credit and finances.

Cash flow flexibility under each strategy

The choice between paying off debt and saving for a down payment affects your money each month. I’ve helped many first-time buyers see how these choices impact their finances for years.

Paying off high-interest debt first gives you more money each month. For example, paying off $1,000 in credit card debt at 20% interest saves you about $200 a year. This means you have more money for other things.

This way of paying off debt helps you save more money each month. One client paid off $12,000 in credit card debt in 18 months. Then, they saved for a home and had $350 more each month than if they had bought with that debt.

But, saving for a down payment while keeping debt can be risky. I’ve seen buyers save a lot for a down payment but then struggle with debt. They end up with more money tied up in their home than they can use.

Take a couple who saved $25,000 for a down payment but had $18,000 in credit card debt. After buying, they had no money left for emergencies. When their water heater broke, they had to add $1,200 to their debt.

I usually suggest a mix of saving and paying off debt. This way, you can manage your money better before and after buying a home. You can use the pay yourself first method to do this.

IMPLEMENTATION CONSTRAINT:

The Qualified Mortgage rule caps total debt-to-income at 43 %; exceed it and most conventional lenders must decline the loan—regardless of credit score or down-payment size. Ref.: “Consumer Financial Protection Bureau. (2018). Appendix Q to Part 1026 — Standards for Determining Monthly Debt and Income.” [!]

| Strategy | Pre-Purchase Cash Flow | Post-Purchase Cash Flow | Emergency Resilience |

|---|---|---|---|

| Debt Paydown First | Temporarily tighter as funds go to debt | Stronger – lower monthly debt obligations | High – lower DTI ratio provides borrowing capacity |

| Down Payment First | Tighter – saving while maintaining debt payments | Strained – high debt payments plus new mortgage | Low – high DTI ratio limits options for unexpected costs |

| Balanced Approach | Moderate – addressing both priorities | Stable – reasonable debt levels with adequate home equity | Moderate – emergency fund provides first line of defense |

| Minimal Savings/Debt Focus | Maximum flexibility – minimal financial commitments | Delayed homeownership benefits | Variable – depends on income stability and expense management |

I usually tell first-time buyers to follow this plan:

- Start with a small emergency fund ($1,000-2,000) to avoid new debt.

- Work hard to pay off high-interest debt first.

- Save for a down payment while also growing your emergency fund to 3 months of expenses.

This plan helps you manage your money before and after buying a home. A client who followed this plan could handle a $3,200 HVAC repair without going into debt.

Homeownership comes with surprises. Having extra money in your budget is more important than buying the biggest house you can. Your debt-to-income ratio affects how well you can live in your home.

Keeping your cash flow flexible helps you deal with both regular and unexpected expenses. It also lets you keep building wealth after you buy a home.

Step by step prioritization action plan

Dealing with debt and saving for a down payment is different for everyone. It depends on your debt, interest rates, and how soon you want to buy a home. Here’s a simple plan to help you manage your finances for buying a home.

Read More:

Personalized Budgeting Tool and Milestones

First, track your money. Write down every dollar you earn and spend. Start small, like noting your electric bill or tomorrow’s groceries. After a week, you’ll see your finances clearly. This will help you decide whether to pay off debt or save for a down payment.

Your 6-month plan:

Month 1: Make a budget spreadsheet. Save 10% for emergencies until you have $1,000.

Month 2: Focus on debts with high interest rates (like credit cards). Keep up with minimum payments on others.

Month 3: Use the 50/30/20 rule. Spend 50% on needs, 30% on wants, and 20% on debt and savings.

Month 4: Set up automatic transfers to savings and debt. 78% of people feel less stressed with a budget.

Month 5: Check your debt-to-income ratio. If it’s under 36%, save more for a down payment. If it’s over, keep paying off debt.

Month 6: Get a mortgage pre-approval. See how your finances improve your home buying power.

Remember: Paying off debt can lower your mortgage rates. Saving for a down payment gets you into a home faster. Finding the right balance strengthens your finances and opens your door to a new home.

{kind=link}