When you buy a house, the price you see is just the start. Many first-time buyers only think about mortgage payments. But, they forget about thousands in extra costs. Did you know 63% of new homeowners spend more than they expected in their first year?

“Understanding total costs before buying is key,” I tell my clients. I’ve helped over 200 first-time buyers buy their homes successfully.

The 30/30/3 rule is a good guide for your budget. Housing costs should not be more than 30% of your monthly income. Save 30% for down payment and closing costs. And, keep the home price under 3 times your yearly income.

Many buyers don’t see how fast hidden costs of homeownership add up. Inspection fees and annual maintenance can turn dream homes into financial problems if not planned for.

I’ve seen many buyers stretch their budgets too far. Then, they face unexpected repairs months later. Smart homeownership means planning for both the purchase and ongoing costs.

Quick hits:

- Budget for more than mortgage payments

- Calculate all closing costs upfront

- Plan for ongoing maintenance expenses

- Consider property taxes and insurance

- Maintain emergency home repair funds

Analyze market prices and value trends

Knowing the difference between paying too much and getting a good deal is key. In my nine years helping Greenville buyers, I’ve seen many save thousands by doing their homework. It’s not just about looking at online listings. It’s about understanding how to value properties well.

Begin by asking your real estate agent for a Comparative Market Analysis (CMA). This document shows recent sales in your area. It’s important to look at homes within a mile to get accurate prices. Remember, prices can change a lot even in the same zip code.

Don’t just look at listing prices. These are what sellers hope to get, not what buyers pay. Look at closed sales data instead. This shows what buyers really paid. Homes often sell for 3-7% less than the asking price, which helps in negotiations.

Compare Similar Recent Neighborhood Sales

When comparing homes, look at square footage, bedroom count, and lot size. These things affect prices a lot. Last month, I helped a couple avoid overpaying by $15,000. They saw three similar homes sell for less, just two blocks away.

Days-on-market stats are also important. If homes in your area sell fast but the one you’re looking at has been listed long, it might be overpriced. Use this info when making your offer.

First-time buyers might want to start with a smaller home. This can be a smart move. It meets your needs now and builds equity for later. In today’s market, it’s often better than stretching your budget too far.

| Property Comparison Factor | High Impact on Value | Medium Impact | Low Impact |

|---|---|---|---|

| Square Footage | Within 200 sq ft | Within 400 sq ft | Greater variance |

| Sale Timeframe | Last 30 days | 31-90 days | 91+ days |

| Distance from Target | Same neighborhood | Within 1 mile | 1-3 miles |

| Property Condition | Similar updates/age | Minor differences | Major differences |

When deciding how much to spend, think about the price and how much it might go up. Some areas keep their value better than others. Look at 5-year trends to find safe investments.

Online tools can help, but they miss important details. Nothing beats real research and advice from a local agent. They know the market well.

Buying a home is more than finding a place to live. It’s a smart financial move. By studying market trends, you make informed choices. This way, you avoid overpaying and build wealth through real estate.

“You Might Also Like: How to avoid overspending on house purchase budget“

Set firm ceiling before negotiations begin

Starting your homebuying journey means knowing your budget first. It’s not just about what your lender says you can borrow. It’s about finding a price that keeps your housing costs low for years.

Make sure your monthly mortgage payment is less than 28% of your income. This includes the loan, property taxes, insurance, and HOA fees. Use a mortgage calculator that includes all these costs, not just the loan payment.

Lenders generally cap the front-end debt-to-income ratio at 28 %; exceeding it can jeopardize loan approval and future refinancing options. Ref.: “Hayes, A. (2025). Front-End Debt-to-Income (DTI) Ratio: Definition and Calculation. Investopedia.” [!]

Make a budget worksheet with three numbers: your ideal price, your stretch price, and your walk-away number. Share it with your agent before you start looking. Ask them to stick to your budget, even if you fall in love with a house.

“The difference between financial freedom and financial stress often comes down to one decision: buying a house that fits your budget versus stretching for one that exceeds it. The former builds wealth; the latter depletes it.”

Include Inspection Repair Cost Estimates

Inspections can reveal costly surprises. Add $5,000-$10,000 to your budget for repairs. This way, you won’t have to choose between walking away or spending your emergency fund.

I helped a couple find a 1940s bungalow for $285,000. But the inspection found $8,200 in repairs. They had to decide whether to walk away or spend their savings.

Your credit score affects your mortgage payments. A score over 740 gets you the best rates. Every 20-point drop below 740 means higher payments.

| Budget Planning Approach | Advantages | Disadvantages | Long-term Impact |

|---|---|---|---|

| Pre-set Budget Ceiling | Prevents emotional overspending; maintains financial discipline | May limit options in competitive markets | Greater financial stability; lower risk of payment stress |

| Flexible Maximum | More property options; adaptability to market conditions | Risk of budget creep; possible financial strain | Possible reduced savings; higher monthly stress |

| No Budget Limit | Maximum property choice; emotional satisfaction | Significant financial overextension risk | Potential foreclosure risk; limited future opportunities |

Resist Last Minute Price Escalations

The final negotiation is the toughest test of your budget discipline. It’s easy to want to add more to get the house. But remember your budget ceiling.

When sellers make counter-offers, compare them to your maximum budget. Every $10,000 increase adds $50-60 to your monthly payment.

Don’t justify extra costs with “we’ll make it work.” The extra debt adds up over 30 years. Sticking to your budget keeps you financially healthy.

Get a budget accountability partner. Someone who can remind you of your goals when emotions get high. This could be a friend, family member, or financial advisor.

Homeownership costs more than just the price. Set firm budgets, include repair funds, and avoid emotional spending. This way, you can enjoy homeownership without financial stress.

“Discover More: Rent vs mortgage payment budgeting for the switch“

Negotiate concessions to reduce closing costs

When you buy a home, don’t forget to ask for concessions to lower your closing costs. Closing costs can add 2-5% to your home’s price. This means $6,000-$15,000 on a $300,000 home. This extra cost can make it hard to afford moving and settling in.

In Greenville, I’ve helped many buyers save money by negotiating. It’s all about knowing which costs can be lowered and how to talk to sellers about it.

CoreLogic data show average U.S. closing costs of $6,905—or roughly 2 %-5 % of a home’s price—highlighting the need to review the Loan Estimate early and request seller credits to offset these fees. Ref.: “McMillin, D. (2024). Average closing costs on a house in 2024. Bankrate.” [!]

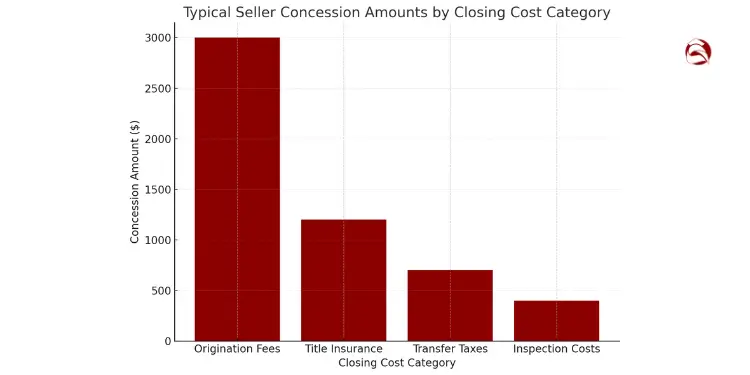

First, ask your lender for a Loan Estimate. This document lists all the fees you’ll pay at closing. Look closely to find areas where sellers might help, like:

- Loan origination fees

- Title insurance premiums

- Transfer taxes

- Recording fees

- Home inspection costs

When you make an offer, be clear about what you want. Instead of saying “3% toward closing,” say “$6,500 toward closing costs.” This makes it clear to sellers what you’re asking for.

The market affects how much you can negotiate. In balanced or buyer’s markets, I’ve helped clients get $3,000-$8,000 in concessions. Even in seller’s markets, you can negotiate if you talk well with the seller’s agent about your needs.

If sellers don’t want to give money, ask for other things that help you. For example:

| Alternative Concession | Typical Value | Benefit to Buyer |

|---|---|---|

| Home warranty | $400-$600 | Covers major systems/appliances for first year |

| Pre-paid HOA dues | $300-$1,200 | Reduces immediate post-purchase expenses |

| Interest rate buydown | $2,000-$5,000 | Lower your monthly mortgage payments |

Another good idea is to ask sellers to pay for specific costs. For example, ask them to cover the title insurance policy or the home inspection. This can be easier for sellers and saves you money.

But, remember, lenders have rules about concessions. Conventional loans usually allow 3-6% of the purchase price, while FHA loans allow 6%. Your lender can tell you the exact rules for your loan.

Every dollar saved on closing costs is a dollar you can put toward new furniture, immediate repairs, or building your emergency fund.

When you ask for concessions, do it in your initial offer. This makes it part of your whole offer, not just an extra request.

Don’t hesitate to ask for concessions. They’re a normal part of buying a home. Knowing how closing costs work can help you save money. With smart planning, you can make a strong offer without using up all your savings.

Buyers who negotiate closing costs start their new life with more money and less stress. Having extra money in your budget can make moving easier and less stressful.

Avoid emotional bidding during auctions

Auctions can make you spend more than you want. In Greenville, I’ve seen people make bad money choices. One person spent $25,000 more than they planned to.

Psychologists call this “auction fever.” It makes people forget about money. This can lead to big problems later.

To avoid spending too much, do these things:

- Write down your maximum price on paper before the auction begins

- Share your limit with a trusted friend who isn’t emotionally invested in the purchase

- Calculate your true affordability using post-purchase expenses, not just the mortgage

- Practice saying “I’m done” out loud before attending

- Attend an auction as an observer first before participating as a bidder

I tell clients to skip auctions if they can’t handle the pressure. Buying in a normal sale is safer.

“Further Reading: Essential single income home buying budget strategies“

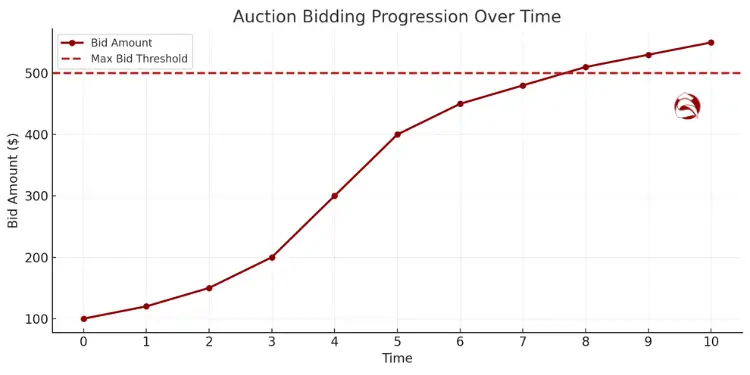

Set Bidding Walk Away Threshold

Setting a “walk away threshold” is key. It’s not just your max budget. It’s 10% less than that.

For example, if you can spend $300,000, set your threshold at $270,000. This helps you avoid bidding too much.

Here’s how to stay on track:

- Step away physically for 10 minutes to regain perspective

- Ask yourself: “If this house needed a $15,000 roof repair tomorrow, would I feel comfortable at this price?”

- Calculate the actual monthly payment increase for each $5,000 bid increase

- Remember that another suitable property will eventually become available

Walking away from a bid is never regretted. The disappointment of losing fades fast. But overpaying lasts for years.

“The most expensive houses I’ve ever sold weren’t the highest-priced properties—they were the ones where buyers paid 15% above market value in emotional bidding wars, then struggled with buyer’s remorse for years afterward.”

Auctions aim to make you feel something strong. Knowing this helps you stay safe. Your future self will be grateful for your caution.

Evaluate long term maintenance expenses realistically

Homeownership comes with more than just a mortgage. In Greenville, I’ve seen many struggle with unexpected costs. Owning a home means always being ready for expenses.

Set aside 1-3% of your home’s value each year for upkeep. For a $300,000 home, that’s $3,000 to $9,000 yearly. This helps avoid financial strain.

Building scientists recommend reserving 1 %–4 % of a property’s value annually for maintenance—older or climate-exposed homes should budget at the upper end of this range. Ref.: “Wentland, M. (2023). Solved! Here’s How Much to Budget for a Home Maintenance Fund. Bob Vila.” [!]

The difference between a home maintenance emergency and a home maintenance plan is simply preparation. When you budget for the inevitable, you transform possible crises into manageable events.

Predict Utility Bills Seasonal Variation

Utility costs change with the seasons. This can surprise homeowners. Ask for the seller’s last year of bills before buying.

In southern states, cooling costs can be much higher in summer. Northern homes see higher heating costs in winter. Knowing this helps budget better.

Use a utility averaging system. Save the same amount each month based on the yearly total. For example, if yearly utilities are $3,600, save $300 monthly.

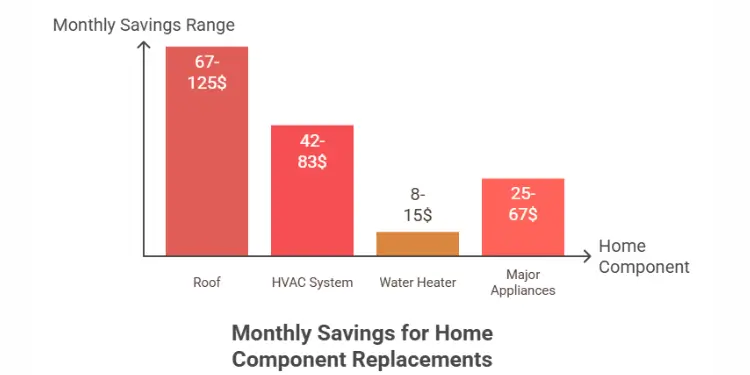

Budget for Roof and Appliance Replacement

Big home parts have set lifespans. Knowing this helps plan for replacements. Use a simple formula to save each month.

| Component | Typical Lifespan | Average Replacement Cost | Monthly Savings (10 Years Left) |

|---|---|---|---|

| Roof | 20-30 years | $8,000-$15,000 | $67-$125 |

| HVAC System | 15-20 years | $5,000-$10,000 | $42-$83 |

| Water Heater | 8-12 years | $1,000-$1,800 | $8-$15 |

| Major Appliances | 10-15 years | $3,000-$8,000 (all) | $25-$67 |

For example, a 10-year-old roof with 15 years left and a $12,000 replacement cost means saving $67 monthly. This makes big costs easier to handle.

Plan Annual Property Tax Increases

Property taxes often go up each year. But many homeowners don’t plan for this. Look at your county’s tax history to plan better.

A $3,000 tax bill growing 3% yearly becomes $3,472 in five years and $4,026 in ten. This increase might seem small but can add up.

ATTOM reports property-tax revenues rose 6.9 % in 2023; budgeting for at least a 3 %-5 % yearly increase protects cash flow as assessments climb. Ref.: “Miller, P. (2024). The New Affordability Crisis: Homeowners Forced Out by Higher Costs. ATTOM.” [!]

Always review your property tax assessments and budget for at least a 3% increase yearly. This way, you’re prepared and won’t be surprised by costs.

Open a “home maintenance” savings account. Set up automatic monthly transfers for 1/12th of your yearly maintenance budget. This keeps emergencies from affecting your main emergency fund.

Good maintenance makes your home a forever home. By planning for these costs, you make your housing expenses stable and manageable.

Calculate total cost of ownership timeline

The last step to avoid overspending is to make a total cost of ownership timeline. Don’t just look at today’s price. Plan for all costs over time. Most first-time buyers own their homes for about 7 years before selling.

Make a spreadsheet for each year. Track mortgage payments, property taxes, homeowners insurance, and maintenance. If you put down less than 20%, add private mortgage insurance costs. Also, remember to save $200-$400 monthly for HOA fees if you have them.

I’ve seen many clients surprised by hidden costs of homeownership they didn’t think about. You’ll also have moving costs of $800-$2,500 and immediate repair costs of $1,000-$5,000.

Bankrate’s 2025 study finds hidden ownership costs now average $21,400 per year—covering maintenance, taxes, insurance, utilities, and connectivity—reinforcing the need for a comprehensive total-cost-of-ownership budget. Ref.: “Bankrate Staff. (2025). Hidden Homeownership Costs Hit $21,000 A Year in 2025. Bankrate.” [!]

Compare your expected costs with your income growth. Will you be able to afford your dream home if your family grows or your career changes? This detailed look helps you avoid mistakes and spend less over time. Remember, successful homeownership is not just getting the keys. It’s keeping them without financial stress.

{kind=link}