Your financial journey needs to change as life does. Money is more than just numbers. It’s for your dreams, safety, and legacy.

Did you think about how your money plan fits with your life now?

A 2023 Fidelity survey found 72% of Americans don’t match their investment strategy to their time horizon. It’s like driving blind. Warren Buffett said, “Risk comes from not knowing what you’re doing.”

I’ve seen many clients turn financial uncertainty into confidence. They make their financial plan a living document. When my daughter was born, I changed my money plan too. This shows even experts need to follow their own advice.

Goals-based financial planning is about reaching specific goals, not just following the market. This way, you can live the life you want, not just track your money.

Quick hits:

- Match strategies to life stages

- Review plans after major events

- Personalize beyond market benchmarks

- Balance short and long-term needs

Identify Triggers For Goal Reassessment

In my 12 years helping investors, I’ve learned a key lesson. Knowing when to check your goals is important. It helps keep your money and life goals in line.

Don’t change your investment plan with every market move. But, big events need your attention right away. Investors who spot these signs keep their finances and goals in sync.

The secret to successful investment goals is knowing when to change. I’ve seen many clients stick to old goals because they missed the signs for change.

Life changes are a big reason to check your goals. Getting married or divorced can change your money plans. Having a child or losing a family member can also shift your goals.

Behavioral-finance studies show the brain favors **immediate rewards over long-term goals**, increasing the risk of impulsive money moves after a windfall. Building in a 30-day “cooling-off” period can help the rational, planning centers of the brain overrule short-term impulses. Ref.: “Bradt, S. (2004). Brain takes itself on over immediate vs. delayed gratification. Harvard Gazette.” [!]

Changes in your job are another reason to review your portfolio. Getting a big raise can speed up your plans to buy things. But, losing your job means you might need to adjust your money plans.

Getting a lot of money at once is a chance to check your goals. This could be from an inheritance, bonus, or selling a business. I tell clients to wait 30 days before making big money moves.

Health issues can also change your money plans. A serious illness might mean you need more money for medical bills. But, getting better health could mean you have more time to invest.

| Trigger Category | Specific Examples | Primary Impact | Recommended Response Time |

|---|---|---|---|

| Life Transitions | Marriage, divorce, birth, death | Goal priorities and time horizons | Within 60 days |

| Career Changes | New job, promotion, unemployment | Contribution capacity and timeline | Within 30 days |

| Financial Windfalls | Inheritance, bonus, business sale | Acceleration of goals | After 30-day cooling period |

| Market Conditions | 20%+ corrections, sustained inflation | Risk exposure and asset allocation | Within 14 days of confirmation |

| Regulatory Changes | Tax code revisions, new account types | Tax efficiency and vehicle selection | Before next tax year begins |

Moving to a new place can also change your money plans. Going to a more expensive area might mean you have to wait to buy things. But, downsizing could give you more money to save for retirement.

Big economic changes can also mean it’s time to check your money plans. A big drop in the market might be a good time to buy. High inflation can make your money worth less, so you might need to adjust your plans.

Changes in the law, like new tax rules, need your attention too. New rules can affect how well your money grows.

Don’t wait for your yearly check-up if you need to. Talk to your advisor or review your plans yourself if you manage your money. Your goals should match your current life, not what it was.

I suggest making a list of things that might make you need to check your goals. Look at it every few months. This helps you stay on track and make sure you’re always planning for the right things.

For assistance in determining your investment goals, How to Determine Your Investment Goals Properly

Review Life Events And Risk Tolerance

As your life changes, so should your investment plan. I’ve helped many clients update their strategies. Many don’t change their plans, even when their lives change a lot.

Big life events like getting married or having kids change your money needs. They also change how you feel about risk. For example, a new job might make you more willing to take risks. But having kids might make you want to play it safer.

Your comfort with risk changes as you do. After big life changes, it’s time to check your risk tolerance. Ask if your financial safety has changed. Do you have new dependents? Has your job changed?

The most successful investors I’ve worked with don’t just reassess their portfolios after market movements—they reassess after personal movements. Your life changes should trigger investment changes.

This check isn’t just for fun—it affects how you choose investments. If you’re less willing to take risks, you might choose safer bonds. If you’re more willing, you might try new, riskier investments.

A 2024 FINRA Foundation survey shows **80% of consumers grasp basic investment-risk concepts, yet only 55% can identify diversification as a risk-mitigation strategy**, underscoring the need to pair risk-tolerance reviews with targeted education. Ref.: “Fontes, A., Valdes, O., Mottola, G., & Ganem, R. (2024). How Consumers Think About Investment Risk. FINRA Investor Education Foundation.” [!]

Update Time Horizons After Milestones

Every big life event can change your financial goals. A big raise might speed up your plans to buy a home. Or, a career change might make you wait longer to retire. These changes need updates to your investment plan.

Changing your time horizon means adjusting your investments. For goals close to happening, like in three years, I suggest safer investments. This might mean moving to bonds or savings accounts.

You might have many goals with different timelines. Your portfolio is a mix of goals, not just one. A good investment goal has a target amount and a timeline.

Map each goal to its time frame and the right investments. This makes your money work better. Here’s a guide to match goals with investments:

| Time Horizon | Goal Examples | Ideal Asset Allocation | Investment Vehicles | Rebalancing Frequency |

|---|---|---|---|---|

| Short-term (0-3 years) | Emergency fund, Home down payment, Wedding | 80-100% Fixed Income, 0-20% Equities | High-yield savings, CDs, Short-term bonds, Money market funds | Quarterly |

| Medium-term (3-10 years) | College funding, Career sabbatical, Business startup | 40-60% Fixed Income, 40-60% Equities | Balanced funds, Intermediate bonds, Dividend stocks, Index ETFs | Semi-annually |

| Long-term (10+ years) | Retirement, Legacy planning, Generational wealth | 20-40% Fixed Income, 60-80% Equities | Growth stocks, Total market ETFs, Real estate, Long-term bonds | Annually |

| Transitional (Approaching goal) | Pre-retirement (5 years out), Education (2 years before need) | Gradually increasing fixed income percentage | Target-date funds, Bond ladders, Stable value funds | Quarterly |

When updating your goals, think about the whole journey. Some goals are flexible, while others have strict deadlines. Education funding is a must, but retirement can be more flexible.

Make a timeline of all your goals. This helps spot conflicts and find ways to stagger goals. This avoids selling investments at bad times.

Regularly updating your goals makes your investment plan dynamic. It keeps your portfolio in line with your changing life and goals. Your investment plan should reflect who you are now and who you’re becoming.

Adjust Allocation Contribution And Withdrawal Plans

Changing how you invest is key to success. I’ve helped many people adjust their strategies. Those who kept changing their plans did better than those who didn’t.

It’s better to plan ahead than to react. Set clear rules for when to change your investment plan. This helps you deal with life changes and market ups and downs. Knowing why goals matter helps make these changes count.

For guidance on setting realistic investment goals, How to Set Realistic Investment Goals Successfully

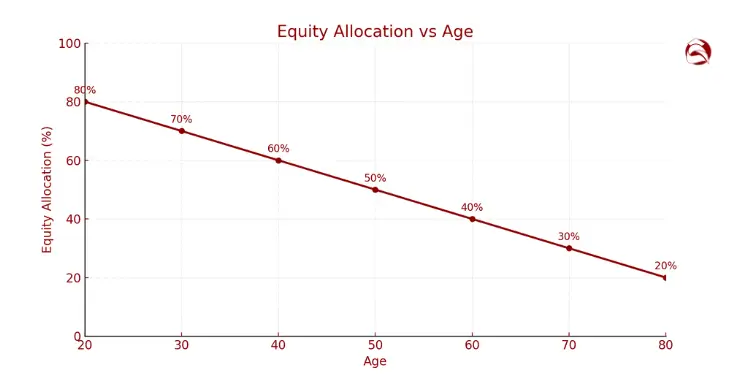

Shift Equity Weighting With Age

The usual rule for how much to invest in stocks is to subtract your age from 100. But, this rule needs to fit your life. For example, a 60-year-old might have 40% in stocks and 60% in bonds.

Think about these things when changing your stock investment:

- How long you might live based on your family and health

- Any steady income you have

- What you want your retirement to be like

- Any goals for your heirs or charity

The classic “100 minus age” stock allocation rule is **increasingly considered too conservative**; many planners now suggest 110–125 minus age to offset longevity and inflation risk—yet higher equity exposure can magnify short-term volatility. Calibrate the rule to personal life expectancy and income certainty. Ref.: “Gallo, N. (2025). Why Keeping Growth in Your Portfolio After 70 Is Crucial for Your Financial Health. Investopedia.” [!]

Some people in their 70s might keep 60% in stocks because they have a pension. Others in their 50s might choose to be more careful because of health issues. The goal is to match your investments with your own needs and goals.

“The investor’s chief problem—and even his worst enemy—is likely to be himself.”

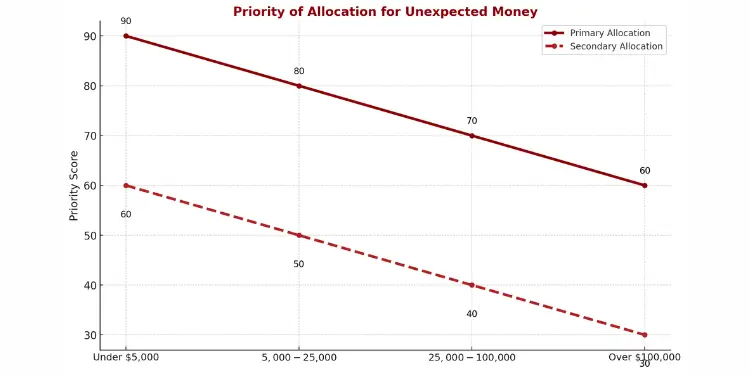

Redirect Windfalls Toward Priority Goals

When you get unexpected money, don’t spread it out evenly. This can weaken its impact on your main goals.

Instead, use this money for your most important goals. For example, if you’re saving for retirement but also for your kids’ education, put the bonus in retirement accounts.

Make a plan for how to use unexpected money. This plan should depend on how much money you get:

| Windfall Amount | Primary Allocation | Secondary Allocation | Timing |

|---|---|---|---|

| Under $5,000 | Emergency Fund | High-interest Debt | Immediate |

| $5,000-$25,000 | Retirement Catch-up | Medium-term Goals | Within 30 days |

| $25,000-$100,000 | Tax-advantaged Accounts | Real Estate/Business | Phased over 3-6 months |

| Over $100,000 | Diversified Portfolio | Legacy Planning | Dollar-cost average over 12-24 months |

Using unexpected money wisely can help you reach your goals faster. I’ve seen people achieve their goals years early by using this smart approach.

Reduce Exposure During Market Turbulence

Volatility can test even the most disciplined investors. Instead of making emotional decisions, have a plan ready. This plan will tell you what to do when the market gets tough.

Set rules for when to adjust your investments:

- 10% market decline: Review allocation but take no action

- 15% market decline: Rebalance to target allocation

- 20% market decline: Consider increasing equity exposure by 5%

- 30%+ market decline: Evaluate opportunities for tax-loss harvesting and Roth conversions

Write down these plans before the market gets rough. This way, you won’t make decisions based on emotions. Your plan should match your risk level and how long you have to invest.

In the 2020 market crash, those with plans did better. They adjusted their investments wisely, while others froze or panicked. Those who followed their plans recovered faster.

Reducing risk doesn’t mean selling everything. You might move to safer sectors, build up cash, or adjust how much you invest each month. This helps you average out the cost of investing during ups and downs.

Your investment plans should change as your life does. Check them every quarter to make sure they’re right for your goals and the market. Making small, steady changes will help you stay on track through life’s ups and downs.

Schedule Semiannual Portfolio Rebalancing Sessions

Twice a year, rebalancing your portfolio is key. It keeps your investments on track. After 12 years, I’ve seen it works best twice a year.

Vanguard simulations covering 1989-2021 found that **annual or semi-annual rebalancing captures 90% of the risk-control benefit** while avoiding the higher costs of more frequent trades—striking an optimal balance between drift control and transaction drag. Ref.: “Zhang, Y., Ahluwalia, H., et al. (2022). Rational rebalancing: An analytical approach to multi-asset portfolio rebalancing decisions and insights. Vanguard Research.” [!]

Mark May and November on your calendar. This avoids tax season and keeps a steady rhythm. It helps you regularly review and adjust your portfolio.

Here’s a five-step process for rebalancing:

- Document current allocation percentages across all accounts

- Compare against target allocations based on your current goals and risk tolerance

- Calculate specific dollar amounts needed to realign each asset class

- Execute trades in tax-advantaged accounts first when possible

- Update your investment policy statement with any adjustments to targets

Rebalancing stops your portfolio from drifting. It keeps your risk level where you want it. Without it, you might take on too much risk or miss out on growth.

In bull markets, your equity might grow too much. This can be risky when markets fall. After downturns, your conservative investments might be too much, limiting growth.

“The discipline to rebalance when it feels uncomfortable is often what separates successful long-term investors from the crowd.”

There are many rebalancing strategies. Each has its own benefits. Here’s a table comparing the best ones:

| Rebalancing Strategy | Frequency | Pros | Cons | Best For |

|---|---|---|---|---|

| Calendar-Based | Semi-annual or annual | Simple, disciplined, less emotional | May miss significant market moves | Busy professionals with limited time |

| Percentage Threshold (5%) | When allocations drift beyond set limits | Responds to market movements, potentially higher returns | Requires constant monitoring | Active investors who track markets regularly |

| Narrow Band (1-2%) | Frequent as needed | Tight risk control, minimal drift | Higher trading costs, tax implications | Conservative investors near retirement |

| Wide Band (8-10%) | Infrequent | Lower costs, potentially higher growth | Greater volatility, larger risk swings | Young investors with long time horizons |

| Hybrid (Calendar + Threshold) | Semi-annual plus trigger events | Balanced approach, responds to major shifts | More complex decision framework | Mid-career investors balancing growth and stability |

Rebalancing is more than just numbers. It’s a chance to check if your investments match your life and goals. It’s about making sure your investments are right for you now.

For example, if you’re close to paying off a house, you might add more stable investments. If your job or family situation changes, rebalancing is a good time to adjust your investments.

Keep a rebalancing worksheet. It tracks your decisions and reasons over time. It’s useful for managing your portfolio through different market cycles.

Your worksheet should include:

- Current allocation percentages across various asset classes

- Target allocation percentages

- Variance between current and target

- Actions taken to rebalance

- Brief notes on market conditions and personal circumstances

Some prefer rebalancing every quarter, others once a year. Semiannual is usually best. It balances returns and risk, but might not fit everyone’s comfort level.

Rebalancing needs vary by your financial goals. Retirement accounts might need semiannual checks. But accounts for shorter-term goals might need more frequent attention.

By rebalancing regularly, you manage market ups and downs. It keeps your investments aligned with your goals, no matter what.

Coordinate Changes With Advisors And Partners

Investment choices affect more than just your money. It’s key to work with advisors and partners for success. I’ve seen good investment plans fail because important people weren’t told or asked.

When your goals change or the market shifts, it’s vital to keep everyone on the same page. This avoids misunderstandings that can cost a lot.

Before making big changes to your investments, talk to three important groups. Each plays a big role in your financial life. Ignoring any one can mess up good plans.

Financial Professionals

Financial advisors and tax experts need to know about big changes early. Tell them at least two weeks before you plan to make changes. This lets them check for tax issues or other financial problems.

When things get complex, talking to your advisor is even more important. They might find ways to save on taxes or suggest better plans for you.

“The most successful investors I’ve worked with treat their financial team like co-pilots, not passengers. They share their destination early enough that course corrections can be made before takeoff.”

Trust companies and wealth management firms offer help with many financial areas. They’re great when you’re adjusting savings accounts or other low-risk investments. Their help can be very useful.

Investment Partners

Spouses, business partners, and others need to agree on investment changes. Make a simple summary of the changes, why you’re making them, and what you expect. This helps in talking about it.

Disagreements often come from different views on time or risk. When the market is shaky, having plans in place helps avoid emotional decisions.

Long-term goals need careful planning, while short-term needs might need more talks. Make clear rules for making decisions with partners. This helps when quick choices are needed.

Estate Planning Professionals

Estate planning lawyers should check big changes that might affect your legacy. A change in investments could affect your beneficiaries or trusts.

Change how you talk about your plans based on the size of the change. For small tweaks, a quick email might do. But for big changes, meet in person with everyone involved.

| Stakeholder Type | Advance Notice Needed | Communication Method | Key Discussion Points |

|---|---|---|---|

| Financial Advisor | 2 weeks | Detailed proposal | Tax implications, alignment with financial plan |

| Spouse/Partner | 1-2 weeks | One-page summary | Impact on shared goals, risk tolerance changes |

| Tax Professional | 3-4 weeks | Specific transaction details | Tax-loss harvesting, capital gains management |

| Estate Attorney | 1 month | Portfolio review meeting | Legacy impact, trust funding implications |

Coordination means making sure everyone knows about changes and their effects. You don’t always need to agree on every small change. But, it’s important to keep everyone informed.

Even if you manage your money yourself, coordination is key. Documenting your decisions and sharing them with family helps keep things clear and accountable.

The best investment changes are those where everyone understands the plan. They know why it’s important and what they need to do.

Track Performance Post Adjustment For Validation

Making changes to your investment strategy without tracking results is like sailing without checking your compass. I’ve found that setting clear investment goals initially is only half the equation—validating your adjustments completes the cycle. Studies show 65% of Americans who achieve financial success started with clear goals, but tracking progress is what keeps them on course.

For beginners learning investing fundamentals, create a simple system to measure whether your changes are working. Set calendar reminders to review your investment accounts quarterly—this regularity helps you stay connected to your financial goals without obsessing over daily market movements.

Read More:

Establish Metrics And Success Thresholds

Define what success looks like for each goal adjustment. For retirement accounts, track both dollar progress and percentage of target income replacement. Education funding requires monitoring account growth against projected future costs. Your mix of investments across various asset classes should align with both your timeline and risk tolerance.

I recommend creating a personal dashboard with three validation metrics for each goal:

1. Progress percentage toward target amount

2. Performance compared to appropriate benchmarks

3. Your comfort level with the new strategy

This third metric often gets overlooked, but it’s vital—the best financial security strategy is one you can maintain through market cycles. Remember that regularly reviewing and adjusting your approach based on these metrics will help you manage your portfolio effectively and stay on track to achieve your personal goals.

{kind=link}