The 50/30/20 budget rule helps freelancers manage their money better. It’s flexible for those with changing income. Traditional budgets don’t work well when money comes in differently every month.

Ever wondered how to plan your finances when you can’t predict next month’s earnings? You’re not alone. A surprising 83% of Americans with fluctuating incomes report struggling with conventional budget approaches, according to recent financial surveys.

“Financial stability isn’t about having consistent income—it’s about creating consistent systems,” notes financial advisor Janet Rivera, who specializes in freelance economics.

I’ve worked with hundreds of independent contractors who transformed their money management by adapting percentage-based budgeting to their unique cash flow. The key lies not in rigid dollar amounts but in proportional thinking that scales with your earnings.

When monthly income varies, your budget needs built-in flexibility while maintaining core financial goals. This guide will show you exactly how to modify this popular approach for unpredictable earnings.

Quick hits:

- Adapt percentages to income fluctuations

- Create essential buffer fund first

- Automate savings during abundant months

- Establish your true baseline needs

- Prioritize financial stability over spending

Estimating Baseline Income from Variable Sources

Turning unpredictable freelance money into a steady budget is key. You can’t just use one number in the 50/30/20 rule. You need a way to figure out what “income” means for you.

As a freelancer, I found out that without a steady income, budgeting is hard. But, there are ways to make your money stable, even if it changes a lot. Let’s look at how to build a strong financial base when regular budgeting doesn’t work.

Average Last Twelve Months Revenue

Start by looking at your income from the past year. Check your bank statements, payment records, and taxes. This will show you patterns you might not see.

Make a spreadsheet with columns for each month’s income, taxes, and what you take home. Seeing these patterns can help you plan better.

The Federal Reserve reports that 28 % of adults experience month-to-month income swings and 10 % struggle to pay bills because of this variability. Basing budgets on a rolling 12-month net-income average smooths these swings and aligns spending with long-term earning capacity. Ref.: “Board of Governors of the Federal Reserve System (2024). Economic Well-Being of U.S. Households in 2023. Federal Reserve.” [!]

The most dangerous financial mistake for freelancers is treating exceptional months as the new normal. Your twelve-month average keeps you honest about what you actually earn.

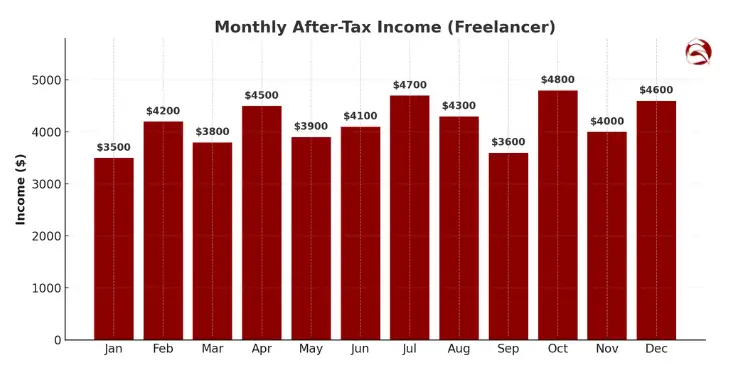

For example, wedding photographers might make a lot more in summer. Knowing this helps you plan for slow times. After recording all twelve months, find your average monthly income after taxes.

This average helps you start with the 50/30/20 rule. But, it’s risky with income that’s not steady. So, we need something extra.

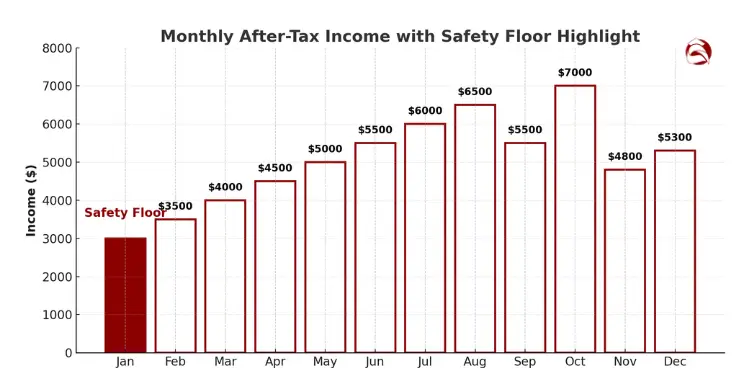

Use Lowest Month as Safety Floor

While your 12-month average is helpful, using only this can cause money problems in slow months. I learned this the hard way in my first year of freelancing.

Find your lowest-earning month and use that as your “safety floor” for basic needs. This safe approach helps you cover basics even when money is tight.

- Record your lowest monthly income after taxes from the past year

- Calculate 50% of this amount for your maximum “needs” budget

- Use this figure as your baseline for rent, utilities, groceries, and other essentials

- Any income above this floor becomes available for wants and savings

For example, if your income ranged from $3,000 to $7,000 last year, budget around $3,000. This means your needs category (50%) would be capped at $1,500, no matter how much you earn in better months.

This way, you have a buffer in good months. If you earn $7,000 in a month, you’ll only spend $1,500 on needs. This leaves a lot for wants, savings, and paying off debt.

| Income Level | Needs (50%) | Wants (30%) | Savings (20%) |

|---|---|---|---|

| Lowest Month ($3,000) | $1,500 | $900 | $600 |

| Average Month ($5,000) | $1,500 (fixed) | $1,500 | $2,000 |

| Best Month ($7,000) | $1,500 (fixed) | $2,100 | $3,400 |

Notice how the “needs” category stays the same, no matter your income. This helps you spend wisely and saves more in good months.

JPMorgan Chase Institute analysis shows 55 % of U.S. workers see income change by more than 30 % from one month to the next—evidence that even a “low-month safety floor” can be breached without disciplined expense caps. Ref.: “Farrell, D. & Greig, F. (2016). Paychecks, Paydays, and the Online Platform Economy. JPMorgan Chase Institute.” [!]

If your income changes a lot, try zero-based budgeting with the 50/30/20 rule. This mix gives you more flexibility when money is unpredictable.

Your first task: Make a 12-month income tracking spreadsheet today. Include columns for income, taxes, and net income. Then, find your lowest earning month and use 50% of that for your “needs” budget.

Knowing your income patterns helps make the 50/30/20 rule work, even when your money changes. This system reduces financial stress and boosts your financial planning confidence.

Creating Buffer Funds Before Percentage Allocation

بEmergency Runway Versus Tax Reserve

Your emergency fund and tax reserve are for different things. They must be kept separate.

Your tax reserve is a must. Freelancers should save 25-30% of their income for taxes. This money is for the government, not yours.

Open a special savings account for taxes. Move money to it right away when you get paid. This avoids the shock of owing a lot in taxes.

Your emergency fund is for different reasons. Freelancers need a bigger safety net because of income changes. It helps during slow times or gaps in work.

Experts say save 3-6 months of expenses. But freelancers might need 6-12 months. This gives more financial security.

Start small if you can. Even $500 can help with small surprises. Add more when you can to reach your goal.

“The self-employed person should have 12 months of living expenses because their income can be so volatile. You might have a great month and then nothing for two months.”

Remember, your tax money is not for emergencies. Using it for other things can lead to trouble.

pay-as-you-go. Ref.: “Internal Revenue Service (2025). Publication 505: Tax Withholding and Estimated Tax. IRS.” [!]

To do this right:

- Open separate accounts for taxes and emergencies

- Move 25-30% of each payment to your tax account automatically

- Save for emergencies first, then spend on things you want

- Use the 50/30/20 rule only after saving for these needs

This way, freelancers can handle income changes and work on long-term goals. Once you have these funds, you can use the 50/30/20 rule for the rest of your money.

Setting Flexible Needs and Wants Caps

When your income changes every month, setting spending limits is key. The 50/30/20 budget breakdown is great for steady paychecks. But freelancers need a flexible way to split their income.

Let’s rethink what “needs” mean for you. Unlike people with steady jobs, your “needs” need extra care. This is because your income and some costs change with your work.

Identifying Your True Fixed Necessities

First, sort your expenses into two groups: fixed and variable necessities. Fixed necessities stay the same no matter your income or work.

Start by making a list of monthly costs that don’t change. This includes rent, minimum debt payments, insurance, and subscriptions. These are your financial basics.

Add up these costs and compare them to your lowest income from the past year. This shows if you can afford them when money is tight.

Managing Variable Necessities

Variable necessities change each month but are essential. These are things like groceries, transportation, utilities, and business costs that vary with your work.

For these, find a three-month average to set a baseline. When you’re busy, your business costs might go up. But so should your income. The goal is to keep things balanced.

Your fixed and variable necessities should not take up more than 50% of your lowest income. If they do, you need to cut back on some expenses.

| Expense Category | Examples | Budgeting Approach | Income Percentage | Adjustment Strategy |

|---|---|---|---|---|

| Fixed Necessities | Rent, insurance, minimum debt payments | Fixed monthly amount | 30-35% of lowest monthly income | Renegotiate or downsize if exceeding target |

| Variable Necessities | Groceries, utilities, business expenses | 3-month rolling average | 15-20% of lowest monthly income | Scale with workload, find efficiencies |

| Flexible Wants | Entertainment, dining out, non-essential shopping | Percentage of current month’s income | 10-30% based on current income | Scale up/down based on monthly revenue |

| Savings & Debt | Emergency fund, investments, extra debt payments | Percentage of current month’s income | 20% minimum, more in high-income months | Increase percentage during abundant periods |

Creating a Flexible Wants System

The 50/30/20 rule is good for steady income. But with irregular income, you need a flexible wants system. Instead of a fixed amount, use a percentage that changes with your income.

In good months, you can spend up to 30% on wants. In tough months, cut it to 10-15% to stay financially stable. This stops you from spending too much when you can afford it.

Using a separate account or credit card for wants helps keep spending in check. When the money’s gone, it’s gone. This way, your spending adjusts with your income.

“Financial freedom isn’t about having unlimited resources – it’s about having complete control over the resources you have.”

Practical Implementation Steps

To make this flexible system work:

- List all your fixed necessities and calculate their total

- Track variable necessities for three months and determine their average

- Add these two figures and calculate what percentage they represent of your lowest monthly income

- If the total exceeds 50%, identify expenses to reduce

- Open a separate account for wants and transfer a percentage of each payment based on that month’s income level

This method helps you manage spending and savings without being too strict. It divides your income into three parts, knowing the amounts will change.

Remember, unexpected costs will happen. Saving for emergencies is key, aiming for 3-6 months of expenses in your savings. This safety net helps when your income is unpredictable.

By setting clear limits between needs and wants, but being flexible, you’ll learn to manage money well even with changing income. The best money plan isn’t about limiting yourself. It’s about finding a way to work with your income that makes sense for you.

Handling Windfalls and Seasonal Dry Spells

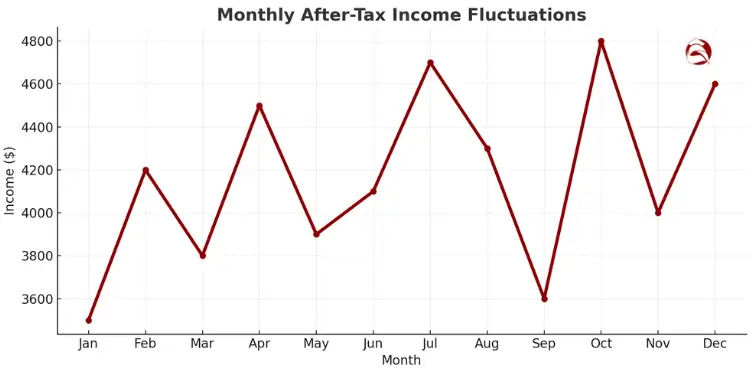

Freelance work can be like a rollercoaster with ups and downs. Your income might jump high one month and then drop. This makes it hard to follow the 50/30/20 rule, but it’s not impossible.

When you get a big payment, you might want to celebrate. Maybe you’ll go shopping or buy something you’ve wanted. But it’s better to plan wisely with your money.

Good freelancers have a plan for both good and bad times. They make sure to save during the good months and be ready for the bad ones. Their budget is flexible but keeps their financial goals in mind.

“Related Articles: 50/30/20 budget example for a typical monthly income“

Percentage Split for One-Time Bonuses

For big payments, a special version of the 50/30/20 rule works well. It’s called the “windfall split.” It helps you use unexpected money wisely.

Here’s how to budget your money when you get a surprise windfall:

- Tax reserve first (25-30%) – Always save for taxes first. Freelancers don’t have taxes taken out automatically.

- Emergency fund boost (50% of remaining) – Put half of what’s left into your emergency fund. This helps you reach your goal of 3-6 months of expenses.

- Debt repayment or retirement (30% of remaining) – Use this part to pay off debt or save for retirement. Learn more about these goals.

- Discretionary spending (20% of remaining) – Treat yourself or invest in your business with this small part.

To avoid IRS penalties, freelancers must either pay 90 % of the current-year tax or 100 % of the prior-year tax (110 % for high-income filers) through withholding and estimated payments—known as the safe-harbor

rule. Ref.: “Internal Revenue Service (2025). Topic No. 306, Penalty for Underpayment of Estimated Tax. IRS.” [!]

This way of budgeting focuses on long-term stability. It uses 80% of windfall money for savings and debt. This helps you get financially secure while enjoying some benefits now.

Decide how much money you need to consider a windfall. For most freelancers, it’s any payment that’s 1.5 times their average monthly income.

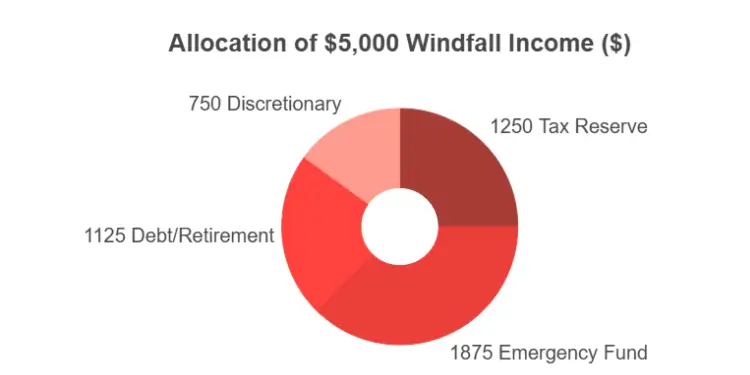

| Income Level | Tax Reserve | Emergency Fund | Debt/Retirement | Discretionary |

|---|---|---|---|---|

| $5,000 Windfall | $1,250 (25%) | $1,875 (50% of $3,750) | $1,125 (30% of $3,750) | $750 (20% of $3,750) |

| $10,000 Windfall | $2,500 (25%) | $3,750 (50% of $7,500) | $2,250 (30% of $7,500) | $1,500 (20% of $7,500) |

| $20,000 Windfall | $5,000 (25%) | $7,500 (50% of $15,000) | $4,500 (30% of $15,000) | $3,000 (20% of $15,000) |

For slow periods, being prepared is key. Many freelancers face times when work is less. This can be after taxes, in summer, or in January.

If you know when you’ll have less work, set up a special fund. Call it your “income smoothing fund.” It should have 3-4 months of basic expenses. It’s different from your emergency fund.

- Emergency Fund – For true emergencies only (like medical issues or equipment failure)

- Income Smoothing Fund – For planned slow periods in your work cycle

Having two funds helps you manage income changes better. Your budget plan becomes more stable. You’re ready for emergencies and slow periods.

Look at your income over the last two years to find patterns. Most freelancers find their income follows seasonal trends. Knowing your slow seasons helps you prepare.

Your job is to set a windfall threshold and plan how to use it. Then, figure out how much you need for your income smoothing fund. This will keep you financially stable all year.

“You Might Also Like: 50/30/20 budget calculator for quick planning and spending balance“

Automating Transfers with Irregular Pay Dates

When your money comes in at random times, using automation is key. It helps you stay on top of your finances. Unlike regular paychecks, freelancers and gig workers need a system that fits their income schedule.

Start by picking a “primary receiving account.” This is where all your money first goes. It’s like a central hub before money moves to other places. From there, set up automatic transfers based on how much money you have, not when.

CFP-quoted guidance in Investopedia advises workers with volatile earnings to target an emergency fund of 12–18 months of living expenses—double the traditional 3–6-month rule—to buffer dry spells and project delays. Ref.: “Paljug, K. (2025). Is Your Emergency Fund Enough? Calculate the Ideal Amount Based on Income or Expenses. Investopedia.” [!]

For example, when your account hits $1,000, the system can move 25% to taxes, 10% to savings, and 5% to retirement. This way works better than setting transfers for specific dates.

Many online banks let you do this through their apps. If yours doesn’t, look into third-party tools that can connect to your accounts. These tools watch your money and move it when you set rules.

Multiple Small Transfers Reduce Temptation

Breaking transfers into smaller amounts helps in more ways than one. Seeing a big sum of money can make you want to spend it. But, moving money in small bits makes saving easier.

This method keeps you from spending what you should save. It helps you stay on budget even when income is unpredictable.

Being consistent is more important than being perfect with money. Even small, regular savings add up over time. Saving 3% for retirement when you can is better than nothing.

The table below shows different ways to manage money for freelancers and gig workers:

| Automation Approach | Best For | Advantages | Limitations | Setup Difficulty |

|---|---|---|---|---|

| Date-Based Transfers | Freelancers with somewhat predictable monthly totals | Simple to set up, works with most banks | Can overdraft when income is delayed | Easy |

| Threshold-Based Transfers | Highly variable income patterns | Adapts to actual cash flow, prevents overdrafts | Requires specialized apps or banks | Moderate |

| Percentage-Based Sweeps | Project-based workers with large payments | Automatically scales with income size | May require manual adjustments for expenses | Moderate |

| Manual with Reminders | Beginners or those with very unpredictable income | Complete control, no unexpected transfers | Requires discipline, easy to forget | Easy |

Try setting up an automatic transfer to a savings or tax account this week. Start small if you need to. Even saving a little for taxes can reduce stress. Watch your spending for a month to see how it changes your habits.

“Read More:

Spreadsheet Template Tailored for Freelancers

A custom tracking system is key for freelancers to budget well. I’ve made a special spreadsheet template. It helps you budget with irregular income and follows the 50/30/20 rule.

This template has a 12-month income tracker. It shows your average earnings. There’s also a tax estimation worksheet and a way to split your after-tax income into needs, wants, and savings.

The wants category should be about 30% of your budget. This is for things that make life better but aren’t needed, like dining out or daily coffee. Every budget needs room for fun, but how much depends on your money situation.

To start, download the template below and fill in your income from the last three months. This tool will help you see where your money goes each month. It gives you financial clarity that fits your life as a freelancer. Your budget should cover basics and let you enjoy spending too.

{kind=link}