Managing money with a small income needs smart planning and useful tools. The percentage-based way to handle money makes it easier. It turns money worries into simple steps. Have you ever wondered how some families live on tight budgets?

Recent data shows nearly 40% of Americans can’t handle an unexpected $400 expense. This shows why budgeting strategies are more important than ever. Elizabeth Warren said in her book “All Your Worth,” “Getting your money in balance doesn’t have to be complicated.”

I’ve seen many families take back control by dividing their income into three parts: essentials, personal choices, and future security. This method isn’t about cutting back—it’s about feeling in control.

When money is scarce, this percentage-based budgeting can be tweaked to fit your needs. Its beauty is in being simple—no need for fancy apps or complex spreadsheets.

Quick hits:

- Works with any income level

- Adapts to changing financial situations

- Creates clear spending boundaries

- Builds savings even when tight

- Reduces financial anxiety effectively

Calculate bare minimum living expense list

To make the 50/30/20 budget work for low-income households, you first need to calculate your bare minimum living costs. This honest assessment becomes even more critical when every dollar matters. The goal is to fit your true needs within that 50% slice of your after-tax income, though this might take time to achieve if you’re starting with limited resources.

Begin by gathering your bank statements, bills, and receipts from the past three months. This gives you a clear picture of where your money actually goes, not where you think it goes. Many people are surprised to discover their true spending patterns when they see the numbers in black and white.

If you’re wondering whether the 50/30/20 approach is right for your situation, exploring the benefits of this budget can help you decide. The key advantage for low-income households is its flexibility while maintaining financial discipline.

Federal Reserve data show that 37 percent of U.S. adults could not pay an unexpected $400 bill with cash or its equivalent—evidence of how financially fragile many households remain and why nailing down true baseline costs is the first priority.Ref.: “Board of Governors of the Federal Reserve System. (2025). Report on the Economic Well-Being of U.S. Households in 2024. Federal Reserve.” [!]

“Explore Further: 50/30/20 budget for low income households that stretches every dollar“

List Fixed Costs: Rent, Utilities, Transport

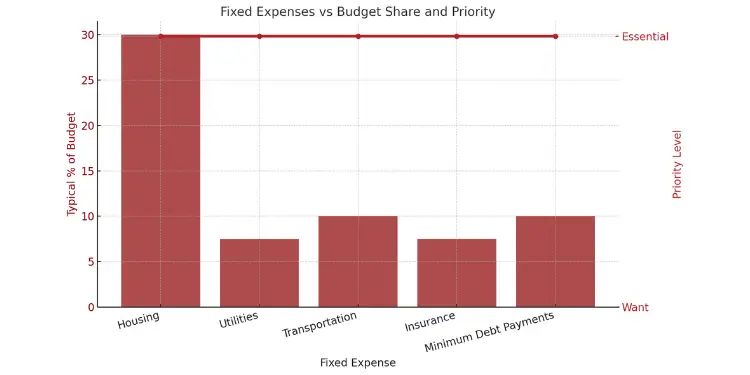

Fixed costs are expenses that remain relatively constant each month. These form the backbone of your necessity category and typically consume the largest portion of your monthly after-tax income. Start by listing these non-negotiable expenses:

- Housing payments (rent or mortgage)

- Utilities (electricity, water, gas, basic internet)

- Transportation (car payment, insurance, fuel, or public transit passes)

- Insurance premiums (health, renters/homeowners)

- Minimum debt payments (credit cards, loans, student debt)

Create a simple tracking system with three columns: expense name, due date, and amount. This becomes your financial foundation. For many low-income households, these fixed costs might already approach or exceed 50% of take-home pay. Don’t get discouraged—we’ll address adjustments in the next section.

Be ruthlessly honest about what constitutes a true need versus a comfortable want. For example, basic phone service is a necessity, but the latest smartphone plan with unlimited everything might fall into the wants category.

More than 50 percent of U.S. renters now pay over 30 percent of income for housing and utilities—often leaving little room to hit the 50 percent “needs” target without downsizing or sharing costs.Ref.: “Joint Center for Housing Studies. (2024). America’s Rental Housing 2024. Harvard University.” [!]

| Fixed Expense | Typical % of Budget | Priority Level | Potential Savings Strategy |

|---|---|---|---|

| Housing | 25-35% | Essential | Consider roommates, smaller unit, or relocation |

| Utilities | 5-10% | Essential | Energy-saving habits, assistance programs |

| Transportation | 5-15% | Essential | Public transit, carpooling, fuel efficiency |

| Insurance | 5-10% | Essential | Bundle policies, increase deductibles |

| Minimum Debt Payments | 5-15% | Essential | Debt consolidation, hardship programs |

Tag Variable Expenses That Can Be Trimmed

Beyond your fixed costs, you’ll have variable necessities that fluctuate month to month. These expenses—like groceries, household supplies, and medication—are essential but offer room for strategic trimming. Track these variable costs for at least two weeks to establish baseline spending patterns.

Groceries often present the biggest opportunity for adjustment in low-income budgets. While food is obviously essential, how and where you purchase it matters significantly. Look for patterns in your spending: Are convenience foods inflating your grocery bill? Could meal planning reduce waste? Are you shopping at higher-priced stores when more affordable options exist?

The USDA reports that 13.5 percent of U.S. households experienced food insecurity in 2023—so grocery reductions must protect nutritional adequacy rather than just slash calories.Ref.: “Rabbitt, M. P., Hales, L. J., & Reed-Jones, M. (2024). Food Security and Nutrition Assistance. USDA Economic Research Service.” [!]

I recommend using a simple tagging system for each expense:

- E – Essential as-is: Cannot be reduced without hardship

- T – Trimmable: Necessary but can be reduced

- C – Could eliminate: If absolutely necessary in a financial emergency

This tagging approach helps prioritize where to make cuts when your necessities exceed 50% of income. For example, basic internet might be coded “T”—necessary for job searching and bill paying, but perhaps you could downgrade to a lower speed tier.

Remember that trimming doesn’t mean eliminating—it means finding the minimum acceptable level for each necessity. The goal is to gradually work toward fitting true needs within that 50% target, even if it takes several months to achieve.

Create a separate list of your variable expenses with their current amounts and possible reduced targets. This becomes your roadmap for gradually bringing your budget into balance without sacrificing quality of life.

“The art of budgeting isn’t about restriction—it’s about redirection. Every dollar you save on necessities becomes a dollar you can put toward your future security.”

By carefully analyzing both fixed and variable expenses, you create a clear picture of your financial baseline. This honest assessment is the foundation for making the 50/30/20 budget work effectively, even with limited income. The next step will be prioritizing which bills to pay first within that 50% necessity slice.

“Discover More: How to stick to 50/30/20 budget without constant willpower battles“

Prioritize urgent bills within 50 percent slice

The 50% slice for needs in your budget is very useful. It helps you focus on urgent bills and get better rates. When you spend more than half of your income on needs, it’s hard. But, knowing which bills are most important helps a lot.

Many families have found a way to manage their money better. They know which bills to pay first and which can wait. This way, they avoid big problems and keep their money safe for the future.

First, sort your bills by how urgent they are:

- Housing payments (to prevent eviction notices)

- Utilities with disconnection warnings

- Court-ordered payments (child support, legal obligations)

- Essential medications and healthcare

- Minimum debt payments to avoid credit damage

- Transportation costs needed for work

Make a calendar to show which bills to pay first when money is tight. This helps you make smart choices instead of just paying whatever comes first.

Negotiate Payment Plans to Avoid Penalties

Talking to creditors early can save you from big fines and keep your credit score good. The worst thing is to stay silent. Most companies have special plans for hard times if you ask before it’s too late.

When you call, say: “I want to pay my bill but I’m short on money. What can you do to help?” Write down who you talked to, what they said, and any numbers they gave you.

For different bills, you need different plans:

- Utilities: Ask for budget billing to smooth out seasonal changes

- Medical bills: Get itemized statements and ask about help programs

- Student loan: Look into income-driven plans that adjust payments based on income

- Credit cards: Ask for hardship programs that lower rates or payments

Many people don’t know that zero-based budgeting can help when talking to creditors. It shows you have a solid plan for your money.

The goal is not to skip payments. It’s to make payments you can handle. A good deal helps you keep important services and protects your credit score. This is key for future money chances.

Bundle Insurance or Phone for Lower Rate

By bundling and optimizing services, you can cut down on fixed costs. This helps you get closer to the 50% goal for needs. I saved over $200 a month with these strategies when I was really struggling.

Insurance offers big savings chances. Call your providers to ask about discounts for multiple policies. Don’t stop at one call; get quotes from at least three places, saying you’re comparing.

For phone and internet, check if you’re paying for too much:

- Check how much data you use versus your plan

- Look into family plans to save on each person’s cost

- Consider prepaid options for cheaper rates than contracts

- See if you qualify for the Affordable Connectivity Program ($30 monthly discount)

- Check the Lifeline program for cheaper phone service

When talking to service providers, mention other offers and ask: “What can you do to keep me?” The retention team often has special deals that regular customer service can’t offer.

For subscriptions, choose annual payments to save money. Small savings add up and make your budget easier to manage. This frees up money for savings or debt repayment.

Keep track of your current rates and aim to call one provider each week. Every dollar saved on fixed costs helps you stay stable financially.

“Read More: 50/30/20 budget for beginners simple steps toward money confidence today“

Channel 30 percent toward realistic daily comforts

When money is tight, the 30% of the 50/30/20 budget for wants is key. It’s for things that make life better but aren’t needed to survive. This includes things like dining out or buying fun clothes.

For those with less money, using 30% for wants might seem hard. You might start with 5-10% and that’s okay. The goal is to enjoy life a little, even if it’s small.

Understanding what “wants” means is important. It’s not about fancy trips or expensive clothes. It’s about small joys like a better coffee or a family movie night.

The 50/30/20 budget is flexible. You can compare it to other budgets to find what works best for you. This way, you can enjoy life a bit while staying on track.

Budget Fun Money Without Derailing Needs

Setting clear limits for fun money is key. Using the envelope system helps. This way, you know when to stop spending on wants.

This method keeps your spending in check. It helps you avoid overspending on things you don’t need. A budget calculator can help figure out how much to spend on wants.

Find ways to have fun without spending a lot. Parks, libraries, and nature are great options. They offer fun at little to no cost.

Identify your top three small pleasures and budget for them. This could be a monthly movie night or a weekly coffee. It helps you enjoy life without overspending.

This isn’t about cutting out fun. It’s about being smart with your spending. By planning, you can enjoy life and save for the future, even when money is tight.

Safeguard 20 percent for goals and emergencies

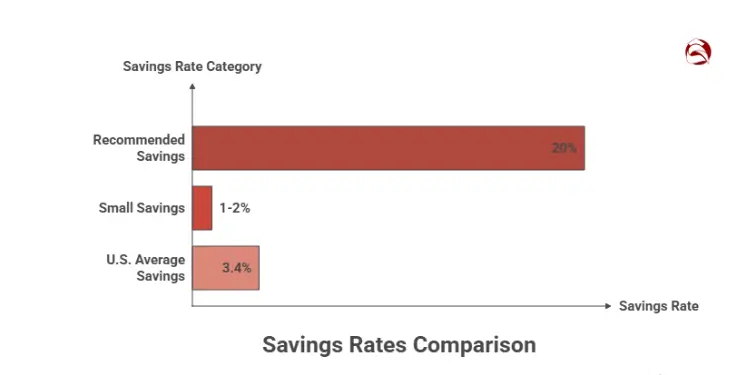

Setting aside 20% of your income for savings and emergencies might seem hard. But, even small amounts can help a lot. Families with low incomes have built emergency funds by saving a little each time.

Start small, like saving 1-2% of what you earn after taxes. Saving just $5 a week adds up to over $250 a year. This helps you feel more secure.

In June 2024, the U.S. saved only 3.4% on average. This shows many people struggle to save. But, saving is key for your financial health.

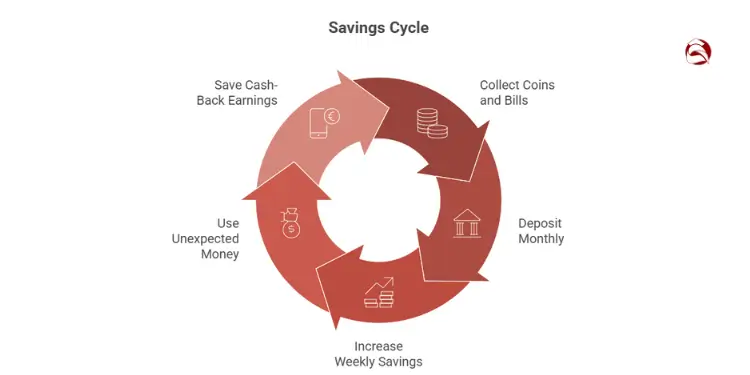

Start Micro-Savings Using Roundup Transfers

Roundup tools make saving easy when it feels hard. Apps like Acorns round up your purchases to save more. This way, you save without feeling it.

These small savings add up over time. For example, saving $0.75 from a $3.25 coffee purchase helps a lot. You won’t miss these small amounts.

Roundup transfers are easy to ignore, which helps you save more. You can even double or triple your savings as you get more comfortable.

Users of round-up apps such as Acorns and Chime typically accumulate $240–$300 in automatic micro-savings every year—money that would otherwise slip through daily spending.Ref.: “MoneyWise Staff. (2023). Round-Up Savings Apps: Are They the Best Way to Save? MoneyWise.” [!]

I couldn’t imagine saving anything on my income until I tried roundups. After six months, I had nearly $300 saved without feeling any different about my spending.

Here are more ways to save on a tight budget:

- Save all coins and $1 bills in a jar, depositing monthly

- Save $1 the first week, $2 the second, and so on

- Use unexpected money like tax refunds for savings

- Save all earnings from cash-back apps in your emergency fund

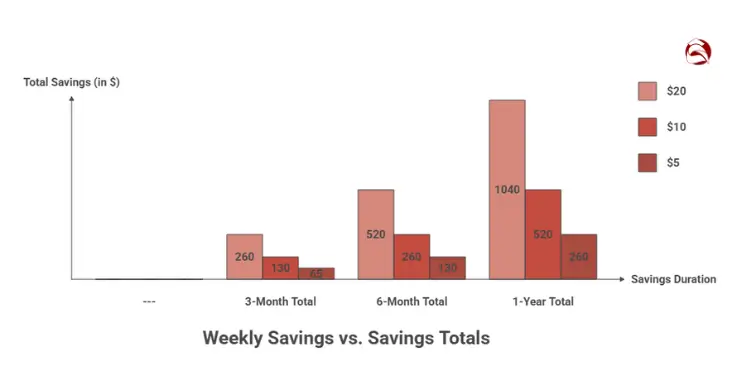

Build Rainy-Day Fund Even Five Dollars Weekly

Building an emergency fund on a tight budget is a mindset change. Even a little savings can help a lot. I’ve seen $200 emergency funds prevent big problems by fixing small issues early.

Start with a goal of saving $500-1,000 before saving for other things. This small fund can stop many financial problems. Then, you can save more as you can.

For those with unpredictable income, save first. Set aside a small amount from each paycheck. This way, saving is consistent, not based on leftover money.

| Weekly Savings | 3-Month Total | 6-Month Total | 1-Year Total |

|---|---|---|---|

| $5 | $65 | $130 | $260 |

| $10 | $130 | $260 | $520 |

| $20 | $260 | $520 | $1,040 |

Having a small savings buffer is very helpful. Many low-income families feel less stressed with just $300-500 saved. This gives them room to breathe and prevents small problems from getting worse.

Open a special savings account for emergencies. Choose one that doesn’t charge fees. This makes it easier to save without distractions.

Remember, saving a little each week adds up. $5 a week for a year is $260. This can cover many emergencies. As your savings grow, you’ll feel more confident to save for the future.

Start by saving $5 from each paycheck. This small step is the first step to financial security, even when money is tight.

Stretch income with community and government resources

Managing money well means using community and government help. These resources can ease your budget stress. They can add $200-400 a month without needing more money.

These programs help you be smart with money. They let you save for emergencies or pay off debt. Let’s see how to use them well.

Apply for Utility Grants and Food Assistance

Utility bills can take up a lot of your money. But, there are ways to lower these costs.

Many utility companies offer discounts based on income. Call them to see if you qualify. The federal Low Income Home Energy Assistance Program (LIHEAP) also helps with heating and cooling costs.

For food, the Supplemental Nutrition Assistance Program (SNAP) can help. A family of four might qualify if they make less than $3,000 a month. Many states now have online applications.

Local food pantries also help. They offer food like grocery stores. You don’t need to show your income to get help. This can save you money for other needs or financial goals.

The federal LIHEAP program can cover winter heating or summer cooling bills for households earning up to 150 % of the Federal Poverty Guidelines (or 60 % of State Median Income), and applications are accepted through local agencies each fiscal year.Ref.: “Administration for Children & Families. (2024). LIHEAP Primer FY 2024. U.S. Department of Health & Human Services.” [!]

“Using assistance programs when needed isn’t a failure—it’s a strategic decision that creates space in your budget to build stability while working toward long-term financial goals.”

Community Action Agencies help in every county. They offer support and help you find programs you qualify for. Their staff can help with applications and paperwork.

Do something this week. Look for a program in your area and apply. Even a small cut in expenses can help your budget.

Use Free Budgeting Tools from Nonprofits

Managing debt or saving on a tight budget is easier with the right tools. Free budgeting resources offer help without extra costs.

Nonprofit credit counseling agencies like the National Foundation for Credit Counseling (NFCC) offer free help. They have certified counselors for one-on-one sessions. You get special budgeting tools too.

Local groups also offer free budgeting workshops. Check your library, college, or church for these. Many have childcare, so you can attend.

For online tools, try these:

- The Consumer Financial Protection Bureau has free budget worksheets for variable incomes

- Capital One’s Money & Life Program offers free budgeting tools for everyone

- Many credit unions have free financial tools online, even for basic accounts

Nonprofit resources focus on teaching, not selling products. They help you learn to manage your money better.

These tools are great for adjusting the 50/30/20 budget example for lower incomes. They help track debt and set savings goals, even with little spending room.

For those with credit card debt, nonprofit counseling can help. They offer plans to lower interest rates and make payments easier.

Try one free budgeting tool before your next payday. The right tool can change how you manage your money, even on a tight budget.

Review budget monthly to capture income shifts

Living on a tight income means your money situation changes often. Set a regular “budget date” to keep your 50/30/20 budget on track. Pick the same day every month and mark it on your calendar.

During your monthly review, ask yourself: Did I earn what I expected? Which spending areas went over budget? What changes do I need to make for next month? This 30-minute check-in prevents small problems from becoming budget disasters.

“For More Information:

Track Cash Flow with Envelope Wallet App

Digital envelope systems make tracking your 50/30/20 budget easier. Apps like Goodbudget, YNAB, or EveryDollar create virtual envelopes that adjust as your income changes. These tools work well because they focus on the money you actually have, not what you expect to get.

Cash spending often becomes a budget leak for many people. Take a photo of receipts or log cash purchases right away in your app. During higher-income months, try increasing your savings percentage toward a specific savings goal. When money gets tighter, your necessities might temporarily need 70% instead of 50%.

The power of percentage-based budgeting comes from its flexibility. Your budget calculator might show different numbers each month, but the basic budget design method stays the same. The goal isn’t perfect math—it’s building awareness of where every dollar goes so you can stretch limited income further.

{kind=link}