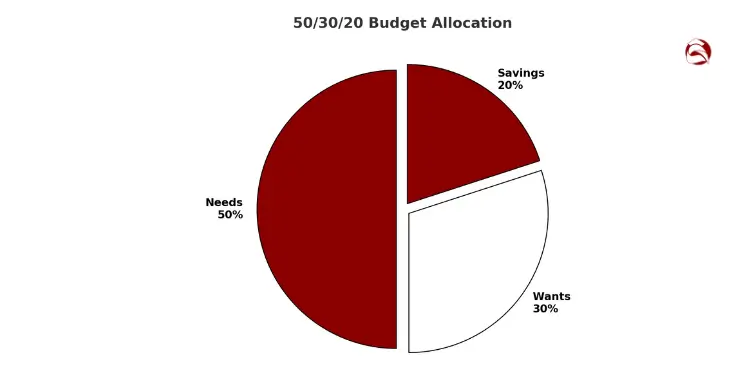

The 50/30/20 budget is easy to follow and helps families stay financially stable. It splits your after-tax money into three parts: needs (50%), wants (30%), and savings (20%). Many families struggle, even with good incomes. Almost 4 in 10 Americans would have to borrow for a $400 surprise expense, the Federal Reserve found.

“Financial peace isn’t about fancy investment strategies—it’s about having a system that works for your family’s real life,” notes many financial advisors. I’ve seen many parents feel more confident about money by using this method. It helps them deal with childcare and unexpected school costs.

This method is flexible. You can change the percentages to fit your family’s needs. It keeps the main idea of intentional spending on needs, wants, and. With credit card delinquency rates high, having a clear plan is key.

Quick hits:

- Simplifies complex household money management

- Creates breathing room for family priorities

- Works without tracking dozens of categories

- Adapts to changing family circumstances

- Builds financial confidence through clarity

Pinpoint household needs before dividing income

Knowing what your family really needs is key to managing money well. Before you can split your income into three parts, you must know where your money goes. This is even more important for families with kids.

Start by tracking your spending for two weeks. You don’t need anything fancy. Just write down every purchase in your phone or a notebook. For families, this helps see spending patterns that might be hidden with kids around.

It’s also important to set financial goals. Do you want to buy a house, save for college, or pay off debt? Having goals helps you stick to your budget and gives meaning to your savings.

List Upcoming Expenses For Accurate Picture

First, write down all your monthly bills. This includes your mortgage, utilities, groceries, and more. Don’t forget small charges like streaming services.

Next, look at your last three months of bank statements. Highlight child expenses in one color and necessities in another. This makes it clear where your money goes.

Many families find they spend more than they thought. One parent realized they spent $200 a month on quick foods. This money could be better spent in their 50/30/20 budget example.

Identify Irregular Costs Like Annual Premiums

Don’t forget to plan for expenses that don’t come every month. These can mess up your budget if you’re not ready.

Make a list of these costs, like:

- Annual insurance premiums

- Quarterly tax payments

- School fees and supplies

- Seasonal clothes

- Holiday and birthday gifts

One family spent $2,400 a year on birthday gifts. That’s $200 a month if budgeted right! Knowing these costs helps you avoid surprises.

Take an hour this weekend to get your financial papers ready. This work might seem hard, but it helps you make a budget that really works for your family.

The 50/30/20 budget works best when it’s based on your real spending. Only after you know your spending can you split your income into three parts that really fit your family’s needs.

Allocate 50 percent to core living costs

Learning to manage your family’s money starts with knowing what you spend on needs. This is the first step in the 50/30/20 rule. It’s about knowing what you really need versus what you want.

Needs include things like a home, food, and healthcare. These are the basics for your family’s life. They also include things like car payments and school costs.

Many families find they spend more than 50% on these things. This is common, but it’s not a problem. It’s just a starting point, and it can be changed.

It’s important to know the difference between needs and wants. Ask yourself if you really need something. If not, it’s a want, not a need. Making a budget helps you see this clearly.

Negotiate Utilities and Insurance for Savings

One way to save money is to talk to service providers. They might lower your rates if you ask. This is easy and can save a lot.

Call your internet, cable, and insurance companies. Ask for discounts or promotions. If you’ve seen better deals, tell them.

Last month, a family in Henderson saved $840 by making a few calls. Their insurance went down by $32 a month. Their internet and phone plans also got cheaper.

For insurance, think about bundling policies. You can also increase deductibles if you have enough savings. These changes can save money without losing protection.

Compare Grocery Tactics Meal Planning Bulk Shopping

Groceries are a flexible part of your budget. With smart planning, you can save money on food. This way, you can give your kids healthy meals.

Try a two-week meal plan that uses common ingredients. This cuts down on food waste by about 30%. It also helps you use up ingredients before they go bad.

Here are some tips for saving on groceries:

- Plan meals around sales and seasonal produce

- Buy staples and non-perishables in bulk

- Use a grocery app to compare prices

- Make double batches and freeze half

- Get kids involved in cooking to avoid eating out

Structured weekly meal planning reduces duplicate purchases, curbs impulsive buys, and measurably cuts household food waste—translating directly into lower grocery bills. Ref.: “Lynch, K. (2018). Meal Planning Can Improve Health and Reduce Food Waste. Michigan State University Extension.” [!]

One family I helped saved 20% on groceries. They went from spending $1,200 to $950 a month. They used the saved money for emergencies while eating well.

Reducing expenses isn’t about being cheap. It’s about being smart and avoiding waste. By focusing on what you really need, you can save for the future.

This weekend, take a closer look at your monthly bills. Call service providers to see if they can offer better rates. Also, plan meals that use ingredients wisely. These small steps can make a big difference in your budget.

Dedicate 30 percent to flexible lifestyle choices

Your family’s quality of life improves when you spend 30% of your income on wants. This money is for joy, memories, and showing your family’s values. It’s not just for spending.

Wants are flexible. You can change how much you spend on them. It’s better to make choices than let money slip away.

So, what are “wants”? They include:

- Family vacations and travel

- Restaurant meals and coffee shops

- Entertainment subscriptions and activities

- Children’s extracurricular programs

- Holiday and birthday gifts

- Non-essential clothing and electronics

The 30% rule is a starting point. Some families might need to adjust this percentage based on their needs. This is true for those with high housing costs or childcare expenses.

Set Entertainment Caps Without Harming Fun

Entertainment can be a big expense. Many families spend a lot on things they don’t really enjoy. This can make money disappear without bringing much joy.

Setting limits doesn’t mean no fun. It means more fun. Try a “Fun Fund” jar where everyone suggests free or cheap activities. Then, pick one on weekends.

One family saved $200 monthly by doing this:

“We canceled three streaming services and started our Fun Fund jar. Our kids love drawing activities now. Last weekend, we had a backyard camping night that everyone loved. We’re spending less but enjoying more quality time together.”

For entertainment subscriptions, check if they’re worth it each month. Cut what doesn’t make your family happy.

Balance Dining Out With Family Cooking Nights

Dining out can take up too much of your budget. The average family spends 5-10% of their income on restaurants. This money could be saved.

Instead of cutting out restaurants, try a “2-2-3” system. Eat out two times a month, have two home cooking nights, and prep three meals. This saves money and teaches kids to cook.

Teaching kids to cook is valuable. They learn about nutrition and enjoy trying new foods.

One parent shared this:

“Our Thursday cooking nights are something we all look forward to. My 8-year-old daughter makes the shopping list for her ‘restaurant night’ and feels proud serving her special pasta dish. We’re saving at least $150 monthly while creating better memories than we ever did at actual restaurants.”

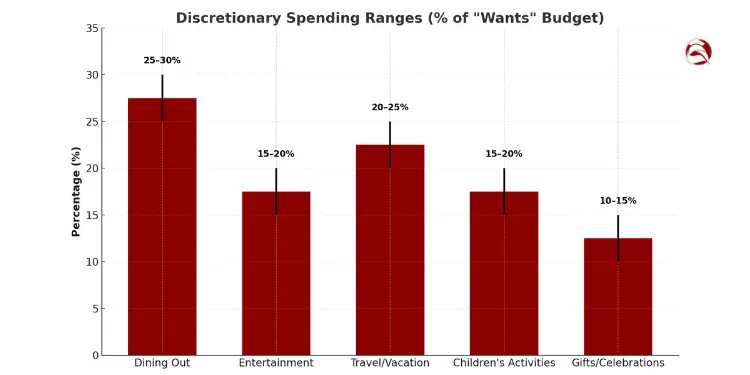

Discretionary spending shows your family’s values. There’s no one right way to spend 30% of your income. Just be intentional.

| Discretionary Category | Typical % of “Wants” Budget | Benefits | Smart Savings Strategy |

|---|---|---|---|

| Dining Out | 25-30% | Convenience, social connection, special occasions | Use restaurant loyalty programs, limit to 1-2 times monthly |

| Entertainment | 15-20% | Relaxation, family bonding, cultural experiences | Rotate streaming services, use library resources, find free events |

| Travel/Vacation | 20-25% | Memory creation, education, stress reduction | Travel off-season, use credit card points, plan “staycations” |

| Children’s Activities | 15-20% | Skill development, socialization, confidence building | Choose one primary activity per child, seek scholarships |

| Gifts/Celebrations | 10-15% | Relationship nurturing, tradition building | Set per-person gift limits, emphasize experiences over objects |

This week, look at one “want” area where you spend too much. Could you spend less on something that brings more joy? Small changes can make a big difference in your finances and happiness.

Route 20 percent toward savings and debt

Starting your journey to financial freedom is easy. Just save 20% of your income for savings and debt. It might seem hard now, but it’s a smart move for your family’s future.

The average American saves only 4.4% of their income. But you can do better. Plan wisely to save more.

The U.S. personal saving rate averaged just 4 – 5 % of disposable income in early 2025—well below the 20 % ‘savings & debt’ target in the 50/30/20 framework. Ref.: “U.S. Bureau of Economic Analysis. (2025). Personal Saving Rate. BEA.” [!]

Setting aside 20% is tough because it means saying no to today’s wants. But it’s worth it. It helps you stay safe when things go wrong and grows your wealth.

Use the 50/30/20 budget to find a balance. It helps you save for tomorrow while enjoying today.

Automate Transfers into Emergency Cushion

First, focus on building an emergency fund. Start with $1,000 and aim for 3-6 months of expenses. This fund protects you from sudden costs.

Automate your savings. Set up transfers to a savings account right after you get paid. Even $25 a week adds up. Choose a savings account that’s easy to reach but not too easy.

Automatic savings features mirror workplace success: 61 % of Vanguard-tracked plans now use auto-enrollment, and a record 45 % of participants increased their deferral rates in 2024—proof that automation steadily boosts savings momentum. Ref.: “Samuels, R. (2025). Vanguard Sees All-Time High Deferral Rates, Plan Design Improvements in 2024. PLANSPONSOR.” [!]

“The habit of saving is itself an education; it fosters every virtue, teaches self-denial, cultivates the sense of order, trains to forethought, and so broadens the mind.”

Automating your savings makes it easier. Your emergency fund grows without you thinking about it every month.

“Learn More About: 50/30/20 needs vs wants categories for confident everyday spending“

Snowball Credit Cards Then Tackle Loans

For those with debt, try the snowball method. It helps you pay off debts one by one. Here’s how:

- Make minimum payments on all debts to keep your credit good

- Put extra money toward your highest-interest debt first (usually credit cards)

- After clearing high-interest debts, focus on student loans and other debts

- Watch your progress to stay motivated

One family paid off $14,800 in credit card debt in 18 months. Seeing debts disappear kept them going.

Every extra dollar you pay on debt helps. It cuts interest and shortens your debt time.

| Debt Type | Typical Interest Rate | Repayment Priority | Strategy |

|---|---|---|---|

| Credit Cards | 15-24% | Highest | Pay beyond minimums aggressively |

| Personal Loans | 6-36% | High | Target after high-interest cards |

| Student Loans | 4-7% | Medium | Consider income-based options |

| Mortgage | 3-6% | Low | Pay scheduled amounts while focusing on higher-interest debt |

Some prefer the pay yourself first method. It puts savings and debt repayment first, before other spending.

If you have student loans, look into income-driven plans. They might lower your monthly payments. This could help you pay off other debts faster or build your emergency fund quicker.

Getting to financial security is a journey. Some months you might save more, others less. What’s key is to keep going and get back on track when needed.

Today, start by setting up automatic transfers to your emergency fund. This small step puts you ahead of most families and begins building your financial security.

“Explore More: 50/30/20 vs zero based budgeting complete comparison guide“

Adjust percentages for childcare and education

The 50/30/20 budget is a good start, but families with kids need to change it. Childcare costs can be as high as a mortgage. The 50/30/20 rule is flexible, not strict.

In 45 states and D.C., the annual price of center-based care for two children now exceeds average yearly mortgage payments, pushing many families well past the 50 % ‘needs’ guideline. Ref.: “Child Care Aware of America. (2025). Child Care in America: 2024 Price & Supply. CCAoA.” [!]

Many families adjust to 60/25/15 or 65/20/15 during busy childcare years. This keeps their finances on track. Your family’s needs are unique, so your budget should be too.

Account for Extracurricular Fees and Supplies

Kids’ activities add to your expenses. Dance, sports, and music lessons cost a lot. Create a special fund for these costs.

Set a budget for activities every quarter. This helps you choose wisely without overspending. Some families use a rating system to decide.

- Does the activity align with the child’s genuine interests?

- Will participation build meaningful skills or relationships?

- Is the cost proportionate to the benefit received?

- Can we afford this without sacrificing our core financial goals?

School supplies are another challenge. Save money each month for these costs. This keeps your budget stable during back-to-school time.

Adjust Savings Rate During Parental Leave

Life changes like parental leave or job changes affect your budget. Your income might go down while expenses go up.

Don’t worry if you can’t save as much during these times. View it as a temporary change. Compare different budget models to find the best one for you.

Have three budgets for different times:

- Standard operations: Your usual 50/30/20 or adjusted family percentages

- Reduced income periods: A modified plan for parental leave or similar transitions

- Catch-up phases: An accelerated savings plan for when income returns to normal

This way, you won’t give up on budgeting. Financial health is about your family’s values, not just numbers.

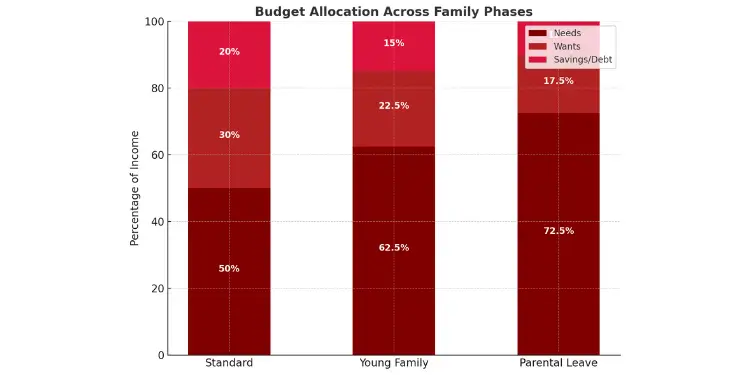

| Budget Category | Standard 50/30/20 | Young Family Adjustment | During Parental Leave | Key Considerations |

|---|---|---|---|---|

| Needs | 50% | 60-65% | 70-75% | Childcare, healthcare, and education push this category higher |

| Wants | 30% | 20-25% | 15-20% | Temporarily reduce discretionary spending during intensive child-raising years |

| Savings/Debt | 20% | 10-15% | 5-10% | Lower temporarily with planned catch-up periods later |

| Timeline | Ongoing | Until school age | 3-12 months | Set clear timeframes for each budget phase |

The numbers above show how to adjust your budget for different life stages. Your changes should match your income, local costs, and priorities.

Check if your budget reflects your family’s needs this month. Small changes now can avoid financial stress later. They help keep your finances strong while supporting your kids.

Track progress weekly and refine categories

Make your 50/30/20 budget a habit by checking in often. Spend just 10 minutes each week to see how you’ve split your money. This helps spot small problems before they get big.

Hold monthly budget huddles with kids

Family money works best when everyone knows the plan. Have monthly meetings to teach kids about family money. One family lets teens see some budget parts, like why they carpool.

Talking about money teaches kids about saving for the future. Even little kids can learn about saving.

“Read More:

Use free apps to monitor categories

Technology makes sticking to the 50/30/20 rule easy. Free budget apps sort your spending into needs, wants, and savings. Look for apps with clear spending reports.

Good tools send alerts when you’re close to spending limits. They also help you reach long-term goals. Many apps remind you to pay bills and make payments automatically.

This budget idea, from Elizabeth Warren, is simple and works for many families in the U.S. Adjust it when your situation changes. Budgeting gets better with time.

{kind=link}