The 50/30/20 budget for beginners is easy to follow. It helps you manage your money without stress. It splits your income into three parts: needs, fun, and savings.

Do you know why many people struggle with money? The Federal Reserve says almost 40% of adults can’t handle a $400 emergency without debt. The budget rule by U.S. Senator Elizabeth Warren helps.

“Financial freedom isn’t about being rich, but about having options,” Warren says in “All Your Worth.” This method isn’t about cutting back. It’s about finding a balance that works.

Many people have changed how they see money with this method. It’s flexible. You can change the numbers to fit your life, but keep the main idea of spending wisely.

When looking at ways to manage your money, this method is simple and works well.

Quick hits:

- Calculate your after-tax monthly income

- Identify needs versus wants clearly

- Start small with savings goals

- Adjust percentages to fit your reality

- Track progress without obsessing daily

The Federal Reserve’s latest Survey of Household Economics shows that just 63 % of U.S. adults could pay a $400 emergency expense with cash—leaving 37 % who would need debt or be unable to cover it. A robust savings bucket in your 50/30/20 plan directly addresses this gap. Ref.: “Board of Governors of the Federal Reserve System. (2024). Economic Well-Being of U.S. Households in 2023. Federal Reserve.” [!]

Why beginners love the percentage approach

Percentage-based budgeting is popular with newbies because it’s simple. It doesn’t feel as complex as old methods. At my budgeting workshops, people get lost in spreadsheets with many categories.

The 50/30/20 budgeting method is easy. It doesn’t make you track every dollar. You just make sure your spending fits into three main areas.

Setting automatic transfers on payday mirrors Vanguard data: plans that use auto-enrolment see employees save roughly 65 % more over time than voluntary-enrolment plans, thanks to inertia working in your favor. Ref.: “Clark, J. (2025). A Sneak Peek at ‘How America Saves 2025’. Vanguard.” [!]

Old budgeting ways often confuse beginners. Here’s why:

- Too many categories to track (sometimes 15+ different spending areas)

- Rigid allocations that don’t adapt to real life

- Time-consuming maintenance requiring constant updates

- Guilt-inducing when small deviations occur

Percentage-based budgeting is great because it scales. It works for anyone, no matter how much they make. Let’s see how it works:

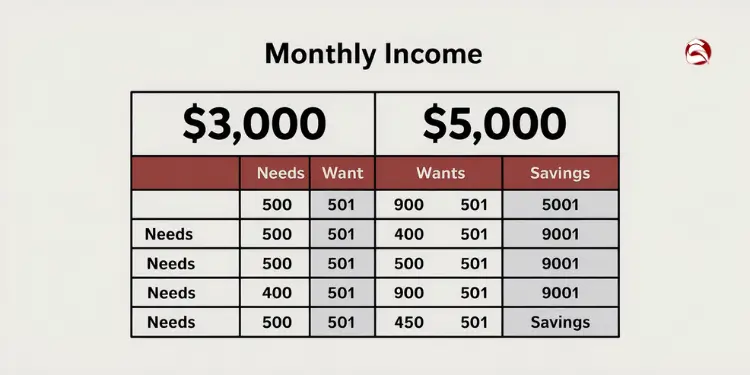

| Category | Percentage | $3,000 Monthly Income | $5,000 Monthly Income |

|---|---|---|---|

| Needs | 50% | $1,500 | $2,500 |

| Wants | 30% | $900 | $1,500 |

| Savings | 20% | $600 | $1,000 |

Dividing your income into three categories helps. It makes budgeting easier without controlling every purchase. You won’t stress over small things like buying coffee.

The 50/30/20 rule is smart. It lets you enjoy life while saving. This stops the cycle of strict budgeting followed by big splurges.

The percentage approach works because it balances structure with flexibility. It gives you rules without feeling trapped. This is perfect for beginners.

To figure out your percentages, first find your monthly income after taxes. You can:

- Check recent pay stubs for net (take-home) pay

- Multiply weekly pay by 4.33 to get a monthly figure

- Add any consistent side income or benefits

Once you know your monthly income, use a budget calculator. Or just your phone’s calculator. Multiply your income by 0.5, 0.3, and 0.2 for needs, wants, and savings.

Before moving on, calculate these numbers for yourself. Having these numbers will help you decide if the 50/30/20 budget is right for you.

Gathering income and expense numbers quickly

Getting your financial numbers doesn’t have to be hard. You can understand your money flow in under 15 minutes. It’s not about perfect accounting, but a quick look at where your money goes each month.

Many people don’t budget because tracking expenses seems too hard. I’ve been there too! But, you don’t need to keep track for months to start. Just enough to make a 50/30/20 plan.

First, find out your monthly after-tax income. This is what you get in your checking account each month. If your income is not regular, use your average from the last three months.

Then, get your basic expense info. It’s simple:

- Look at last month’s bank and credit card statements

- Make a list of your regular monthly payments (like rent, utilities, and subscriptions)

- Guess how much you spend on things like groceries and fun

- Remember any automatic payments you might forget

Sort these expenses into three groups: needs, wants, and savings. Needs are things you must pay for, like housing and food. Wants are things that make life better but aren’t essential. Savings is for extra debt payments and saving money.

If you’re not sure which budgeting method to use, try the 50/30/20 method. It’s good for beginners because it’s flexible but structured.

Using Bank App Export Features

Tracking expenses is easier now thanks to technology. Most banks let you export your transaction history to spreadsheets or budgeting tools. This saves time and gives you accurate data.

Here’s how to use these features in common banks:

- Log into your bank’s website or app

- Go to your account transaction history

- Find “Download,” “Export,” or “Statement” options

- Pick your preferred format (like CSV for spreadsheets)

- Choose a date range (30-60 days is good for starting)

After downloading your transactions, you can quickly sort them in any spreadsheet. Use filters to group similar expenses or sort by amount to see your biggest spending areas.

Many banking apps automatically sort transactions for you. This helps you understand your spending patterns. Check these categories to make sure they fit your 50/30/20 plan. What your bank calls “shopping” might include both needs and wants.

After looking at your spending, set up automatic transfers to your savings account. This “set it and forget it” way helps you save before you can spend it.

Estimating Cash Purchases Accurately

Cash spending can be hard to track because it’s not recorded. Small purchases like coffee or snacks add up but often aren’t included in our budgets.

Instead of trying to track every cash purchase, try these easy methods:

- The envelope method: Take out a set amount of cash each week for spending. When it’s gone, you can’t spend more.

- The notes app method: Keep a running total of cash spent in your phone’s notes app, rounded to the nearest dollar.

- The ATM tracking shortcut: Just record your ATM withdrawals as “spent” in the category you usually use cash for.

For most people, cash purchases are wants. But if you use cash for needs like transportation or groceries, include that in your budget.

A simple weekly cash log can give you insights without being a chore. Just write down rough amounts in broad categories:

- Food and drinks: $___

- Transportation: $___

- Entertainment: $___

- Other: $___

Don’t worry about tracking every penny. Set aside a small “untracked cash” buffer in your budget, like 3-5% of your monthly expenses. This helps you feel less stressed about small unrecorded expenses while keeping an eye on your budget.

The goal of tracking your income and expenses isn’t to have a perfect system. It’s to understand your money habits well enough to make smart decisions based on the 50/30/20 rule.

Plugging figures into the starter worksheet

Now you have your income and expenses ready. It’s time to put them into a starter worksheet. This will make your 50/30/20 budget real.

Let’s look at Bo’s story. Bo had $3,500 a month after taxes and used the 50/30/20 budget. They found their needs cost $1,750, which is 50% of their income.

Bo then put $1,050 (30%) into wants like eating out and fun stuff. The last $700 (20%) went to savings and investments. Bo saved this money automatically every payday.

The 50/30/20 budget is flexible. If your spending doesn’t match these numbers, it’s okay. The worksheet helps you see where you are and where you want to go.

Saving 20% is key for both now and later. First, build an emergency fund. Then, save for big goals likea down paymentor retirement.

Free Google Sheet Explained Stepwise

A digital spreadsheet makes budgeting easy. It does the math for you. Here’s how to use a Google Sheet:

1. Make a new Google Sheet or use a 50/30/20 template.

2. Set up three sections: “Needs (50%),” “Wants (30%),” and “Savings (20%).”

3. Put your monthly income at the top. The sheet will show how much you should spend in each area.

4. List your expenses in each section. For needs, include rent, utilities, and insurance. For wants, list fun stuff. For savings, include retirement and other goals.

5. Use formulas to sum each section and see how much you spend in each area.

Spreadsheets give you a clear view of your spending. Use colors to show when you spend too much in a category.

Make a pie chart to see how your spending looks. This makes it easy to see where you can cut back.

Check your spreadsheet weekly at first. This helps you stay on track and catch small spending mistakes early.

Printable PDF For Offline Tracking

Some people like writing down their spending. A printable PDF worksheet lets you do this while staying organized.

A good budget PDF has:

1. A monthly calendar for tracking expenses

2. Pages for calculating your 50/30/20 percentages

3. Space for noting financial goals and progress

4. A section for identifying spending patterns

To use a printed budget worksheet:

First, print a new one each month. Keep it somewhere you can see it, like on your fridge.

Second, have a way to collect receipts. This could be an envelope or a box. Write down your expenses in your worksheet every day or a few times a week.

Third, have a weekly budget check-in. Spend 15 minutes on Sunday evening reviewing your spending. This helps you make better choices during the week.

Writing down your spending makes you think more about it. It helps you know what you really need versus what you just want.

Choose digital or paper, but be consistent. Your budget worksheet helps you spend wisely and plan for the future.

Adjusting spending categories without budget stress

The 50/30/20 budget is flexible. You can change these numbers to fit your financial goals. Think of them as starting points, not strict rules.

When I first taught this budget to my workshop in Henderson, many were worried. They thought their situation didn’t fit the percentages. But remember, your budget should help you, not the other way around.

“The 50/30/20 rule isn’t meant to be followed to the letter. It’s a framework that helps you understand where your money is going and gives you permission to adjust based on your unique situation and priorities.”

Let’s talk about when and how to change these percentages. This way, you can reach your financial goals without feeling stressed.

When Standard Percentages Need Adjustment

Some life situations might need you to change the percentages. For example, if you live in a very expensive area, housing might take more than 50% of your income. Or, if you’re paying off debt fast, you might need to save more.

Other times you might need to adjust include:

- Preparing for a job loss or career change

- Working faster to save for retirement

- Living on income that changes a lot

- Managing student loans and other financial goals

- Trying to save for both short- and long-term goals

Your financial situation changes as your life does. The percentages that work for you today might need to change later.

Common Percentage Modifications That Work

While 50/30/20 is a good start, you might need to make changes. Here are some common ones:

| Budget Variation | Needs | Wants | Savings/Debt | Best For |

|---|---|---|---|---|

| Standard | 50% | 30% | 20% | Balanced financial situation |

| High-Cost Living | 60% | 20% | 20% | Expensive housing markets |

| Debt Crusher | 50% | 20% | 30% | Accelerated debt payoff |

| Retirement Booster | 45% | 25% | 30% | Late-start retirement and savings |

| Financial Independence | 40% | 20% | 40% | Early retirement aspirations |

Find a balance that works for you. For example, if you’re paying off debt fast, you might save more. This way, you can make progress without feeling too tight.

In 2023, 49.7 % of U.S. renter households spent more than 30 % of their income on housing, a level HUD defines as “cost-burdened.” If fixed costs already exceed the 50 % needs cap, shift percentages or raise income before cutting essentials. Ref.: “U.S. Census Bureau. (2024). Nearly Half of Renter Households Are Cost-Burdened. Census.gov.” [!]

Making Smart Adjustments Without Feeling Deprived

When you change your budget, do it in a way that feels good. Here are some tips:

- Make gradual changes: Change percentages by 5% at a time

- Set clear timelines: Decide if the change is temporary or permanent

- Identify low-impact cuts: Cut things you don’t miss much first

- Increase income when possible: Sometimes, earning more is better than spending less

- Reassess regularly: Check your budget every three months to see if it’s working

The best budget changes match your values and goals. If 50/30/20 doesn’t fit you, make changes that do.

Decision Framework: Adjust Categories or Cut Expenses?

When your budget feels tight, you have two choices. You can adjust the percentages or cut expenses. Here’s how to decide:

Adjust percentages when:

- Your needs and wants always go over budget

- You have big long-term financial goals

- Your income has changed a lot

Cut expenses when:

- You spend too much in areas that don’t matter to you

- You haven’t checked your subscriptions in a while

- You spend more than usual on things like food or entertainment

Often, the best plan is to adjust percentages and cut expenses. This way, you can save money and enjoy your life.

Finding Your Personal Balance

The goal is to find a budget that works for you. It’s not about following a set percentage. Your ideal income to savings ratio might be different from others.

Think about if 50/30/20 fits you. If not, find one change that helps your financial goals. Remember, you can always save more by spending less on wants.

By making smart changes, you can create a budget that feels like a roadmap to financial success. It’s not about restrictions, but about reaching your goals.

“Explore This: How to make 50/30/20 budget with clear practical step by step“

Tracking your progress in first three months

Your first three months with the 50/30/20 budget are key. They help you build good money habits and find out what challenges you face. It’s when you see how you really spend money and learn to change.

Staying consistent is very important during this time. Bo, one of my students, found that tracking money regularly helped them stay on track. “I got used to it fast,” they said.

Don’t worry too much about being perfect in these months. You’ll find forgotten subscriptions and unexpected costs. These are chances to learn and get better at managing your money.

If you spend more than planned, don’t give up. Use these times to learn and adjust. Maybe you need to spend a bit more on needs or change what you consider wants.

Holidays, birthdays, and seasonal costs can disrupt your budget. Plan for these by adding small buffers or adjusting your percentages. Remember, you’ll go back to the 50/30/20 rule later.

Financial planners interviewed by TIME recommend a flexible 60/30/10 split for savers in high-cost cities, adjusting needs upward and savings downward temporarily until income grows—reinforcing that 50/30/20 is a guideline, not a mandate. Ref.: “White, M. C. (2024). Why a 60/30/10 Budget Could Be the New 50/30/20. TIME.” [!]

Make a checklist for the end of three months. Check how well you’re doing, if you’re comfortable with the budget, and what you can improve. By then, managing your money should feel natural.

Weekly Check-In Five Minute Routine

Do a quick weekly check to avoid big budget problems. This simple routine keeps you aware of your finances without feeling overwhelmed.

Here’s a quick weekly routine:

- Review recent transactions (1 minute): Quickly scan your accounts for any unexpected charges or forgotten purchases.

- Update category totals (2 minutes): Add new expenses to your needs, wants, and savings categories.

- Identify possible issues (1 minute): Look for categories getting close to their limits.

- Make notes for next week (1 minute): Write down any changes needed.

Field experiments synthesized by the CFPB show that households using weekly micro-check-ins paired with automatic savings boosts increased emergency-fund balances by up to 20 % within six months—evidence that small, regular reviews compound results. Ref.: “Consumer Financial Protection Bureau. (2020). Evidence-Based Strategies to Build Emergency Savings. CFPB.” [!]

These weekly checks aren’t about being perfect. They’re about staying aware and making adjustments. Many people find it helpful to link their check-in to something they already do. Try checking your finances every Sunday or Monday.

Banking app alerts can help you track money between formal checks. Set alerts for big purchases or when accounts get low. This helps you stay on top of your finances without needing to check every week.

When unexpected expenses come up, quickly sort them during your weekly check. This stops “mystery spending” that can mess up your budget. Remember, just five minutes a week can save you hours of stress later.

“The weekly check-in was my game-changer. Before that, I’d go months without looking at my accounts, then feel overwhelmed by the mess I’d created. Now I never feel out of control with my money.”

Monthly Summary Charts Visualize Savings

Seeing your budget progress in charts can motivate you more than just numbers. It shows your savings grow and spending patterns change, giving you a boost.

Three key charts can change how you see your budget:

- Category Percentage Chart: Shows how well you stick to the 50/30/20 rule

- Savings Growth Chart: Shows how your emergency fund is growing

- Spending Trends Chart: Helps you spot spending patterns

You don’t need to be tech-savvy to make these charts. Use Google Sheets or draw them by hand. What matters most is that you keep doing it.

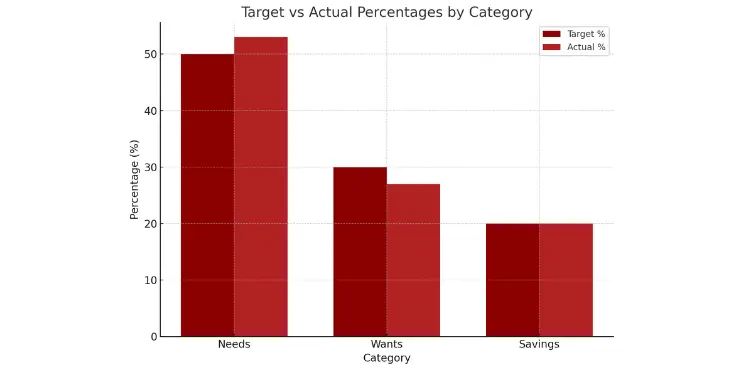

For digital tracking, make a simple table that updates your percentages automatically:

| Category | Target % | Actual % | Amount Spent | Difference |

|---|---|---|---|---|

| Needs | 50% | 53% | $1,325 | +3% |

| Wants | 30% | 27% | $675 | -3% |

| Savings | 20% | 20% | $500 | 0% |

Pay special attention to your savings in your charts. Seeing your progress toward big goals can really motivate you.

Charts can show things that numbers alone can’t. For example, a line graph might show your “wants” spending goes up mid-month. This could mean you need to plan better then.

Use these charts to review your budget each month. Spend 30 minutes at the end of the month to make your charts, celebrate your progress, and plan for the next month. This helps you stay focused on your long-term goals and see your progress.

When you look at your charts, think about how you can save more. Even a small increase in savings can add up over time. These charts help you find ways to save without giving up too much.

By the end of three months, these charts will show you how far you’ve come. Whether you’re saving for retirement, building an emergency fund, or working toward other big goals, seeing your progress can be very motivating.

Read also:

Celebrating milestones and staying motivated

Reaching financial goals is more than just numbers. It’s about celebrating your successes. When you save your first dollar or pay off a debt, celebrate. 40% of Americans can’t handle a $400 emergency, so saving is a big win.

Set clear goals for your money. These could be:

• Saving $1,000 for emergencies

• Saving three months of living costs

• Paying off a debt

• Reaching 20% of your retirement goal

Treat yourself with small, cheap things when you reach these goals. Enjoy a homemade meal, watch a movie, or go on a cheap outing. These rewards help you feel good about managing your money.

When you feel unmotivated, think about why you’re saving. Are you saving for a house? For your family’s safety? For freedom to change jobs? Linking your daily savings to these reasons helps keep you motivated.

The 50/30/20 rule is easy and works because it balances saving with fun. Saving 20% of your income could mean over $1 million in 25 years. And you can enjoy your life today.

Financial goals are about freedom, not limits. Every small step counts in your financial journey. Keep track of your progress, celebrate your wins, and keep moving.

{kind=link}