The 50/30/20 budget is like trying to balance on a busy pier. Families try to find the perfect balance but face big challenges like rent hikes and medical bills.

In this guide, we explore how families can overcome these obstacles. They often face unexpected expenses, like a $400 surprise from the Federal Reserve. Ben Franklin once said, “Small leaks sink big ships.”

I’ve helped Maine parents who use credit when money is tight. They’re not alone in their struggles.

Wonder who’s left treading water? I once carried $80k debt until I found a solution.

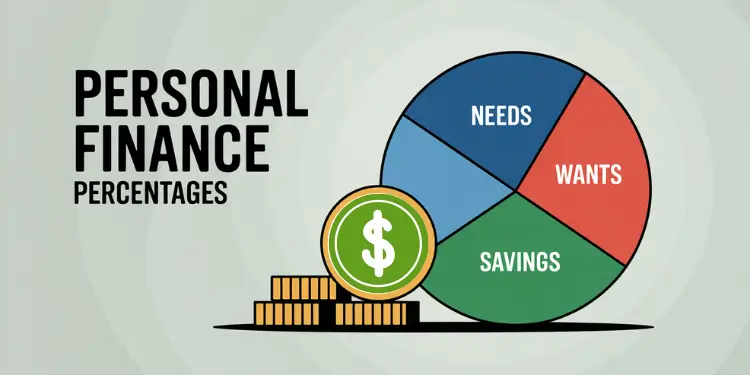

The 50/30/20 budget allocates 50 percent of net income to essential needs, 30 percent to discretionary spending and 20 percent to savings or debt repayment. In practice, variable income streams, escalating housing costs and unplanned expenses frequently disrupt these targets. Establishing a reliable baseline—by averaging earnings over several months—and maintaining a buffer fund covering one to three months of expenses can mitigate income volatility and unexpected outlays.

To preserve the intended allocation, households can negotiate recurring costs, employ sinking funds for predictable events and apply the debt-snowball method to reduce high-interest balances. Automating savings contributions and setting incremental micro-goals reinforces discipline and maintains adherence to the 50/30/20 structure over time.

Key Takeaways

- Balance needs, wishes, and data weekly.

- Plug leaks before they sink progress.

- Track real costs for calm savings.

- Variable income requires baseline earnings calculation.

- Build three-month buffer for lean months.

- Negotiate recurring costs to reduce expenses.

- Use debt-snowball method for faster repayment.

- Automate savings transfers to enforce discipline.

Variable income skews percentage targets

Income that changes like Maine’s tides can make budgeting hard. Big tips in Bar Harbor or seasonal work in Portland can make your money go up and down. We’ll make a plan to keep your money steady, no matter what.

Average earnings to set baseline percentage

Start by finding your usual take-home pay over three to six months. This helps make the 50/30/20 rule clearer. Add any side-gig or tip money to this average. It’s like using a steady lighthouse to guide you, even when waves are high.

According to this resource, 83% of people with changing pay struggle without a baseline.

Build buffer fund for lean months

Having a savings cushion helps when money is tight. It keeps your basic needs covered, so you can cut back on wants. Our advice is to save at least one month’s expenses, then aim for three.

Start by saving 5% of each paycheck for your buffer. Set aside 10 minutes tonight to automate this, making sure you’re ready for tough times.

High housing costs squeeze needs allowance

Rent is like a jammed lobster trap line, taking too much of our paycheck. We struggle to save money. In coastal areas, wages don’t keep up with rising rent, making it hard to meet our needs.

Trying to save 50% of our income is tough when bills add up. Rent, utilities, food, and car insurance make it hard. A study in Maine showed that 35% of income on rent is too much (the budget comparison).

Read More:

Negotiate rent or find roommates

Talking to a landlord about rent can help. Or, sharing a place with someone can cut costs. This way, we can save for loans and food. Try to find roommates quickly by setting a timer for ten minutes.

Offset cost via remote work savings

Working from home saves money on gas and parking. It also reduces stress. This extra money can go into savings or paying off debt.

| Monthly Model | Needs | Wants | Savings |

|---|---|---|---|

| 50/30/20 | 50% | 30% | 20% |

| 60/20/20 | 60% | 20% | 20% |

Around one-third of average household budgets go toward rent or mortgage payments Ref.: “Personal Finance Statistics in 2025” (2024). Millennial Money. [!]

Large debt payments crowd out wants

Debt can feel like barnacles slowing your boat. Big car loans or credit card balances often shrink the “fun” budget we crave. Wishes slip away when interest demands more than we planned.

We’ll map cash currents together by blending discipline with a proven strategy. Data from local state surveys shows that nagging monthly debt often eats into about 30% of take-home pay. The impact drains our motivation and cuts into family outings or a well-deserved treat.

Allocating over 11% of disposable income to debt payments can significantly cut funds for wants and savings Ref.: “Household Debt Service Ratios” (2025). Federal Reserve Board. [!]

Snowball debt to free wants share

Try focusing on one balance at a time. Pay extra toward the smallest debt first while sending minimum payments to the rest. Then move on to the next in line. Each cleared balance frees money for a restored “wants” share. For more on comparing methods, visit this budgeting overview.

- List all debts from smallest to largest.

- Throw extra funds at the top debt until cleared.

- Roll that payment into the next balance.

Time needed: 15 minutes to set up a payment schedule and reclaim more room for the joys you deserve.

Research shows the debt-snowball method boosts repayment success by leveraging psychological momentum Ref.: “Debt snowball method” (2025). Wikipedia. [!]

Family obligations demand budget flexibility

In Maine, a cousin’s wedding or a surprise reunion can feel like a rogue wave knocking us off course. We need a flexible plan that cushions these sudden turns.

Our wants fund may be 30% of after-tax income, as seen in a 50‑30‑20 budget example. That share often includes family trips or birthday gifts. A Bureau of Labor Statistics report finds many households spend over $1,600 yearly on extended-family events. Without planning, a new arrival or a milestone party can upset our financial balance.

Many households spend over $1,600 annually on extended-family events, straining discretionary budgets Ref.: “New Survey Shows Consumers, No Matter Their Income or Assets, Need Support with Spending Household” (2019). CFP.net. [!]

Use sinking funds for family events

Sinking funds help by saving ahead for reunions, graduations, or last-minute travel. We set aside small, regular amounts marked for big gatherings. This method shields our core budget from major hits.

- Open a separate “Family Event” account

- Transfer a set sum each payday, even $20 adds up

- Revisit the fund before that next big get-together

Let’s aim for ten minutes today to schedule an automatic transfer into this special account. We’ll ride those family waves with calmer waters under our hull.

Lifestyle inflation threatens savings discipline

Imagine cruising Maine’s steady coast, then overspending when the wind picks up. Fresh income often tempts us to upgrade gadgets or dine out more. This habit inflates our monthly bills and shrinks our savings. We need a plan before new cash washes over our financial boundaries.

Automate raises directly into savings

One strategy is automatic direct deposit. Each time pay increases, put a part into savings. This stops fresh dollars from going to impulse buys. Tracking each category with budget software helps too. We see where spending flows and cut extras if they harm our savings.

- Set a targeted automation goal, like 50% of every raise for growth.

- Check statements monthly to prevent lifestyle creep.

New income may tempt bigger indulgences, but we can enjoy small rewards. This balance keeps discipline strong. For a clearer path, explore this budgeting approach that breaks unhealthy spending cycles. Let’s anchor our future by steering new funds into healthy harbors.

Automating savings via direct deposit may require employer setup and can take several days to activate, delaying your plan Ref.: “Direct Deposit: What It Is, How It Works, Benefits & Risks” (2024). Investopedia. [!]

Motivation fades after initial enthusiasm

Our excitement often wanes once the first few paychecks pass. Unexpected bills then creep in. I’ve seen many people in Maine slide back into old patterns after a promising budget sprint.

We can avoid that slump by breaking down goals into smaller markers. Fueling our own momentum is key.

Set micro goals and celebrate progress

Think of a sailing trip that marks each harbor on the chart. Each pit stop represents a modest savings milestone. You might start by nudging your emergency fund from $500 to $1,000.

Then treat yourself to a short Maine day trip or a coffee on the waterfront. Those little rewards keep wishes alive and push you forward. This is important when Census Maine data shows the average personal savings rate hovering below comfortable levels.

Track every deposit with a simple scoreboard. Watching your progress rise in real time motivates you to stay the course. Glance at this resource on 50/30/20 vs pay yourself first to see how consistent contributions build a stable cushion.

Each step cements healthier money habits and helps you weather life’s storms with greater peace. Remember, we’re on this journey together, charting a path toward steady gains designed for real life in the United States. Just keep marking each small triumph, and the long haul feels easier to manage.

{kind=link}