Recent data indicates that 57% of Americans are living paycheck to paycheck in 2025. It’s not about willpower. It’s about finding the right money management system for you.

I tried three different budget systems in six months. None seemed to work. That’s because no single method fits everyone.

“The best financial plan is the one you’ll actually follow,” says Dave Ramsey. This is true when comparing budgeting strategies.

Today, we compare two big players in personal finance. The envelope method, also known as “cash stuffing,” involves allocating physical cash into labeled envelopes designated for specific spending categories. It helps you see your spending limits. The other method assigns every dollar a job on paper or digitally. It makes sure you account for all your money.

Both methods help you manage your monthly income. But they work in different ways. By choosing the right system for you, you’ll save time and start making progress with your money.

Assess Your Monthly Expenses Before Selecting a Budgeting Method

Before picking a budgeting style, it’s key to know where your money goes. Knowing this helps your budget work, no matter the style. Without this knowledge, even the best budget can fail when life gets real.

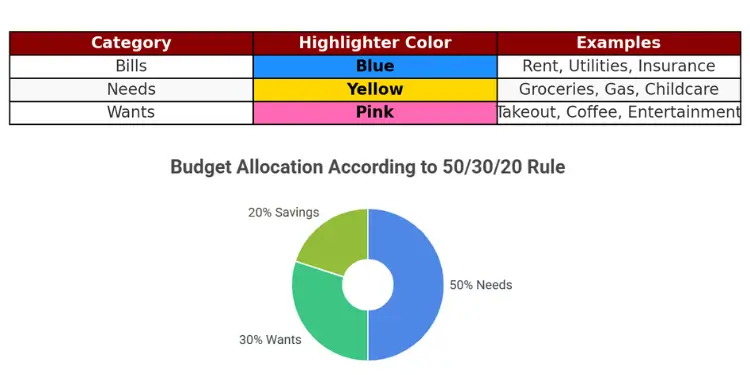

Start by looking at your last three months of bank statements. Use three highlighters: blue for bills, yellow for needs, and pink for wants. This simple step can show you where your money really goes.

Many people find they spend a lot more on takeout than they thought. One person was shocked to spend $430 on coffee in one month. Being honest about your spending is key to a realistic budget.

Categorize Your Expenses: Fixed, Variable, and Occasional

To make a budget that works, know your three main expense types. Each needs a different approach in your budget:

Fixed expenses stay the same every month. These are your rent, car payment, and insurance. List these first because they’re set in stone.

Variable necessities change but are always needed. This includes your food and utility bills. These need some wiggle room in your budget.

Don’t forget occasional expenses that can mess up your budget. I once forgot my $2,200 property tax and had to scramble. Car registrations and holiday gifts also need a spot in your budget.

Using budgeting apps can help track these expenses. Many apps let you save small amounts monthly for big, infrequent costs.

The 50/30/20 rule is a good starting point. It suggests 50% for needs, 30% for wants, and 20% for savings. Use this as a base before making your budget more detailed.

| Expense Type | Examples | Budgeting Approach | Tracking Method |

|---|---|---|---|

| Fixed Bills | Rent, insurance, subscriptions | Set exact amounts | Monthly calendar alerts |

| Variable Necessities | Groceries, utilities, gas | Flexible category limits | Weekly check-ins |

| Occasional Expenses | Car registration, gifts, taxes | Monthly savings toward total | Dedicated sinking funds |

| Discretionary Spending | Dining out, entertainment, shopping | Strict category caps | Daily or real-time tracking |

This exercise isn’t about being perfect but about being aware. It gives you the data to make cash stuffing or zero budgeting work. Knowing your spending habits helps you set realistic cash limits.

After mapping your finances, you’ll see where you need to tighten up. You’ll know which budgeting method fits your spending best. This ensures your chosen system matches your real spending habits, not just an ideal.

Implementing Cash Stuffing to Establish Clear Spending Limits

Handling cash and putting it in envelopes makes spending limits clear. This method, called cash stuffing, stops you from making quick buys. I tried it and my spending changed a lot in just a few days.

Our brains handle cash differently than digital money. Studies suggest that using cash can lead to spending 12-18% less compared to digital payments. This helps us spend less without trying too hard.

Utilizing cash for transactions can enhance spending awareness. The Consumer Financial Protection Bureau notes that handling physical money can make consumers more mindful of their spending habits compared to using digital payments. Ref.: “Investopedia. (2025). How Gen Z’s ‘Cash Stuffing’ Trend Trades Digital Convenience for Physical Control. Investopedia.” [!]

“read also: How zero sinking fund works for future emergency peace“

Physical Cash in Envelopes Reinforces Intentional Choices Daily

The envelope system makes budgeting real and touchable. You pay bills online and then take out cash. You put it in envelopes for different things like food and fun.

For example, you might have $400 for food, $200 for eating out, and $150 for fun. When you want to buy takeout, you look at your “Eating Out” envelope. This makes choosing more thoughtful.

Daniel Chong, a financial planner, notes that handling physical cash makes spending limits more tangible, enhancing budgeting discipline. This makes spending limits clear and not just numbers.

The cash envelope system is simple. When an envelope is empty, you can’t spend in that category. It’s easy to stick to your limits because you can see them.

Color-Coded Binders Simplify Category Recognition at a Glance

Many people use color-coded binders to organize their envelopes. This is popular on TikTok, where the trend is growing.

They use green for food, blue for personal care, purple for fun, and red for savings. This makes it easy to know where to spend your money.

I used to buy coffee without thinking. Now, seeing my “Coffee & Treats” envelope get smaller makes me think twice. I wonder if I should save that $5 latte for the weekend.

Some people add tracking sheets to their envelopes. This helps them see spending patterns and adjust their cash as needed.

Cash stuffing is great for people who learn by seeing. It helps you make smart choices about spending. When you see your “Restaurant” envelope empty, it tells you something.

This method makes spending choices easier and less stressful. You make smart choices every day, not just at the end of the month.

Enhancing Spending Awareness with Zero-Based Budgeting

Zero-based budgeting (ZBB) requires assigning every dollar a specific purpose, enhancing awareness of spending habits. It’s about giving every dollar a job before you spend it. I learned this after wondering where my money went each month.

This method is different from traditional budgeting. You don’t just set aside money for things. You make sure every dollar is used for something specific.

It makes your financial situation clear right away. When I first tried it, I was amazed at how easy it was to make a budget. It works for anyone, no matter how much money they make.

Every Dollar Assignment Exposes Lifestyle Trade-Offs Instantly

Zero-based budgeting is powerful because you assign roles to your money. For example, if you make $4,000 a month, you might spend $1,200 on housing. Then, $500 on groceries, and so on.

This method makes you see trade-offs right away. Want to save more for vacation? You have to spend less somewhere else. It’s all about balancing the numbers.

I’ve found it stops overspending better than anything else. When my car broke down, I knew exactly where to cut back. Every dollar had a job.

| Zero Budget Feature | Benefit | Real-Life Application | Impact on Habits |

|---|---|---|---|

| Every dollar assigned | Complete financial visibility | No mystery spending | Reduces impulse purchases |

| Forced trade-offs | Conscious spending decisions | Choosing between wants | Aligns spending with values |

| Monthly reset | Regular financial check-ins | Adjusting to life changes | Builds financial awareness |

| Digital tracking | Real-time budget status | Checking before purchases | Creates spending pause button |

Monthly Reset Encourages Reflection On Evolving Priorities

Zero-based budgeting has a monthly reset. This means you start fresh every month. It’s a chance to look at your spending and see if it matches your priorities.

Maybe you spend too much on dining out. Or maybe you want to pay off debt faster. Your budget can change to reflect these new goals.

This reset helped me see patterns I never noticed. I realized I spent too little on groceries in winter and too much on entertainment. Adjusting my budget helped reduce stress.

Tools like YNAB (You Need A Budget) and EveryDollar facilitate zero-based budgeting by helping users allocate funds to specific categories. They track your spending and show what’s left in each category. But a simple spreadsheet works too.

The secret to success is the mindset. When you give every dollar a job, you take control of your money. You spend on purpose, not by accident. This reduces stress and makes you more aware of your spending.

Managing Irregular Income: Cash Envelopes vs. Digital Budgeting Tools

Managing money when your income changes a lot needs special tools. These tools help keep your finances stable. I learned this while freelancing for three years.

Traditional budgets don’t work well with changing paychecks. Cash stuffing and zero budgeting are two ways to handle this. They work in different ways.

Cash stuffing stops you from spending too much when you earn more. Zero budgeting lets you track every dollar, even when money is tight. It’s all about dealing with income ups and downs.

Build starter emergency cushion to level income dips

First, make a one-month emergency fund. This fund helps keep your budget stable. For cash stuffers, create an “Income Smoothing” envelope.

Fill this envelope first when you earn more. Then, use it to cover basic needs when money is tight.

For example, landscapers save extra cash in summer for winter. This is great for those with seasonal jobs.

If you like digital tools, open a savings account for income smoothing. Online banks often have no fees for extra accounts. This way, your money earns interest and is safe.

- Your money earns interest while waiting to be used

- Funds are protected from theft or loss

- You avoid the temptation of seeing a large stack of cash

- Automatic transfers can help maintain discipline

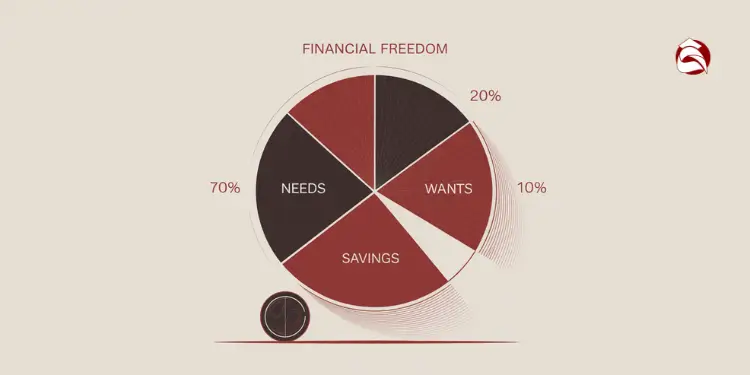

Allocate percentage of windfalls into top priority envelopes

Using percentages for spending works well with changing income. Divide your money into percentages for each category. This way, you always spend the right amount.

Start with:

- 70% to essential envelopes (housing, food, utilities)

- 20% to savings account or debt reduction

- 10% to wants and discretionary spending

For cash stuffers, divide each paycheck into these percentages. This way, you don’t spend too much when you get extra money.

Zero budgeting uses digital buffers for income changes. Apps like YNAB help manage money month to month. This way, you only budget what you have, not what you might get.

This method makes your money last longer. When you get more money, use it for future months. This keeps your spending stable.

Commission-based workers like this method because it helps plan for the future. It’s also good for quarterly taxes, which can be hard to manage.

Stay away from credit cards when money is tight. They can lead to debt. Your emergency fund should protect you, not credit cards.

Both methods need more effort when income changes. Check your finances weekly, not just monthly. This helps catch problems early.

Practical comparison table revealing time effort and mindset needs

I’ve helped hundreds find their budgeting match. This table shows what each method needs from you. The right method isn’t just what experts like. It’s what fits your life and habits.

Both cash stuffing and zero-based budgeting can transform personal finance management by promoting intentional spending. But they ask for different things from you. Let’s look at these differences so you can choose wisely.

| Factor | Cash Stuffing | Zero Budgeting | Which Might Be Better For You |

|---|---|---|---|

| Time Investment | Weekly bank trips to withdraw cash; 30-45 minutes to sort into envelopes | Daily or every-few-days digital tracking; 15-20 minutes per session | Cash stuffing if you prefer batch processing; Zero budgeting if you like quick daily check-ins |

| Learning Curve | Simple concept, minimal tech skills needed | Moderate learning curve with apps or spreadsheets | Cash stuffing for tech-hesitant people; Zero budgeting for the digitally comfortable |

| Spending Awareness | Immediate physical feedback when an envelope is empty | Digital alerts and category tracking throughout the month | Cash stuffing for tactile learners; Zero budgeting for data-driven people |

| Flexibility | Limited – requires physically moving cash between envelopes | High – digital reallocation takes seconds | Cash stuffing for strict boundaries; Zero budgeting for life’s unpredictability |

| Security Concerns | Risk of theft or loss with physical cash | Digital security depends on password strength and app security | Zero budgeting if theft concerns you; Cash stuffing if you distrust digital tracking |

Cash stuffing suits some lifestyles better than others. If you’re always on the move, carrying cash might be hard. But, it helps those who learn by seeing money go.

Adopting a hybrid budgeting approach, such as ‘cash stuffing lite,’ allows individuals to manage discretionary spending with cash while handling fixed expenses digitally, combining the benefits of both methods for improved financial control. Ref.: “SavingAdvice.com. (2025). Cash Stuffing: Why This Old-School Method Is Trending Again in 2025. SavingAdvice.com.” [!]

Zero budgeting is great for digital tracking. Budget apps make it easy, but you need to be tech-savvy and check your spending often.

Quick Scoring System Helps Decide Fastest Fit

Find your best match quickly with these five yes or no questions:

- Do you feel more in control when you can physically touch your money? (Yes = Cash Stuffing)

- Do you prefer using cards or digital payments for most purchases? (Yes = Zero Budgeting)

- Do you struggle with impulse spending when using cards? (Yes = Cash Stuffing)

- Do you want detailed spending analytics and patterns? (Yes = Zero Budgeting)

- Is your income irregular or unpredictable? (Yes = Zero Budgeting)

Count your answers. If most point to one method, start there. You can mix methods too.

For example, use cash for spending you can’t control but keep cards for bills. This mix is great.

“I tried strict zero budgeting for years but kept overspending on groceries. Switching just that category to cash stuffing cut my food bill by 22% in the first month. Sometimes the best system is a blend of methods.”

Handling cash can feel overwhelming. If you don’t want to carry a lot, try “cash stuffing lite.” Keep most money in your account but use envelopes for problem areas.

Consistency is key, not perfection. Cash stuffing fails if you use cards when an envelope is empty. Zero budgeting fails if you don’t check your spending before buying.

“read more: How zero budget toolkit works for handy finance toolkit“

Pilot either method in thirty days with simple checkpoints

Consider piloting a budgeting system for 30 days to assess its compatibility with your financial habits. Pick the one that feels right for you. You can try cash stuffing or zero-based budgeting.

See if it fits your life during the month-long trial.

Weekly Reflections Track Stress and Satisfaction Levels

Check in with your budget every week for 10 minutes. Ask if you felt stressed about spending. Also, how easy was it to follow your plan?

Rate your feelings on a scale of 1-5. These notes help you see if your budget works with you or against you.

For cash stuffing, count what’s left in each envelope weekly. Zero budget users should compare actual spending to planned amounts in each category. This simple tracking reveals patterns in your spending style.

Read More:

Adjust Categories After First Full Cycle for Smoother Ride

After 30 days, review your budget categories. Did you spend too much in some areas and have extra in others? This is normal! Your first budget is just a starting point.

Zero-based budgeting, while promoting detailed financial planning, can be resource-intensive and may lead to short-term planning biases if not managed carefully. It’s essential to balance thoroughness with practicality to maintain long-term financial health. Ref.: “Investopedia. (2025). Zero-Based Budgeting: Benefits and Drawbacks. Investopedia.” [!]

If cash stuffing was too hard with too many envelopes, merge similar categories. Zero budgeters might need to add extra money for things like groceries. The perfect budget evolves with your life – adjust and try again.

Remember, the best budget isn’t perfect. It’s about feeling in control of your money without being unhappy.

{kind=link}