Did you know that 65% of Americans who set clear financial targets do better than those who don’t? Over 12 years as a CFA®, I’ve seen how planning changes results.

“The investor’s chief problem—and even his worst enemy—is likely to be himself,” Warren Buffett once said. This shows why setting clear goals is key when starting out.

I worked with a young couple who wanted to “grow their money.” Without clear goals, every drop in the market made them panic. Setting a goal of $75,000 for a home down payment in seven years changed their approach. They went from feeling anxious to feeling confident.

Having clear investment goals is like having a financial GPS. It helps you make better choices instead of following market noise. This is especially important for beginners going through their first market cycle.

Your financial future is worth more than just hopes. A solid financial plan turns market movements into real progress. Starting with a clear goal makes your journey to investing success smoother and less stressful.

- Clear investment goals transform abstract market movements into meaningful progress markers

- Defined objectives reduce emotional decision-making during market volatility

- Setting specific targets creates accountability that improves both outcomes and peace of mind

Frequent progress monitoring boosts goal-achievement rates by roughly 40 %, underscoring the power of writing down targets and checking them regularly. Ref.: “Harkin, B., Webb, T. L., Chang, B. P. I., & Prestwich, A. (2016). Does Monitoring Goal Progress Promote Goal Attainment? Psychological Bulletin.” [!]

Connect Purpose to Investing Discipline

Successful investors and those who give up during market ups and downs differ by one thing: a clear purpose. I’ve seen this pattern in three Federal Reserve hiking cycles. Investors with clear goals stayed put, while those chasing returns sold at the worst times.

Investing for your goals gives you an emotional anchor in market storms. It’s not just advice; it’s practical psychology that safeguards your financial future.

Imagine two investors facing a 15% market drop. The one chasing benchmarks sees only loss. But the investor focused on a goal, like funding her daughter’s education in 2035, stays calm.

Purpose transforms investing from an abstract numbers game into a meaningful journey toward your most important life milestones.

I worked with a client who linked each investment to a goal. Her bond ladder wasn’t just earning 4.2%—it covered her retirement costs. Her ETFs weren’t just lagging the S&P—they were building a fund for her grandchildren’s education.

This approach changes how you look at investments. Instead of focusing on beating the market, you ask if it helps you reach your goals. This shift changes everything about your decisions.

Long-term goals need different investments. Your retirement fund might need growth assets for decades. But your home down payment fund needs stability and quick access.

| Investment Approach | Decision Driver | Emotional Response to Volatility | Long-Term Outcome |

|---|---|---|---|

| Benchmark-Chasing | Outperforming indexes | Panic, frequent portfolio changes | Performance gaps, higher taxes, missed compounding |

| Purpose-Driven | Progress toward specific goals | Contextual evaluation, steadier behavior | Goal achievement, lower taxes, compounding benefits |

| Trend-Following | Recent performance patterns | FOMO, chasing returns | Buy high, sell low cycle, underperformance |

| Goal-Based | Specific financial objectives | Confidence in strategy alignment | Appropriate risk exposure, better sleep at night |

The discipline from purpose-driven investing grows over time. When market news is bad, your purpose tells you to stay the course. When friends talk about crypto gains, your purpose reminds you to focus on your retirement.

This discipline is key when investing for retirement. The risk you take should match your retirement timeline and needs, not the latest financial trend.

Try this: Write down each investment and the goal it serves. If you can’t connect it to a purpose, question why you own it. This simple check often reveals investments that don’t align with your goals.

Your investment purpose evolves with your life. The discipline lies in keeping your investments aligned with your current goals, not sticking to old plans.

By linking every dollar to its purpose, you turn investing into a meaningful journey toward your goals.

Provide Measurable Milestones for Motivation

Setting specific, measurable investment goals helps keep you motivated. In my 12 years of guiding investors, I’ve seen how clear numbers keep people on track. Turning “I want to save for retirement” into “I need $1.2 million by age 65” makes your goal concrete.

Measurable milestones turn vague dreams into real targets. Instead of just wanting to buy a house, set a specific goal like saving $100,000 for a down payment in 10 years. This gives your plan direction and purpose.

Investors who track specific metrics do better than those with vague goals. Seeing your progress motivates you to keep going. When you’ve saved 40% of your target, you feel more determined to reach it.

Breaking big goals into smaller steps helps avoid procrastination. Instead of facing a huge challenge, you tackle smaller, achievable goals. Each goal reached is a reason to celebrate.

Track Savings Rate Against Target Timeline

A good investment plan has both goals and process metrics. Your goal might be saving $50,000 for your child’s education. But tracking your monthly investment of $250 shows you’re on the right path.

I suggest using a simple system to track your milestones. It should include:

- Monthly savings rate versus your target (Are you consistently investing the planned amount?)

- Portfolio growth against required returns (Is your money working hard enough?)

- Percentage completion toward each goal (How far have you come?)

- Time alignment (Are you ahead or behind schedule?)

This system turns financial goals into a rewarding journey. Seeing how today’s $500 contribution moves you closer to your goal makes investing rewarding.

Hitting milestones boosts your motivation, helping you stay on track even when the market is volatile. I’ve seen investors stay focused through tough times because they knew they were still on track.

Create a simple dashboard to track your progress. This visual reminder motivates you during tough times and celebrates your success. Regularly updating your tracking system strengthens your commitment to investing.

Make sure your milestones fit your life timeline. If you’re saving for a house in five years, your milestones will differ from someone saving for retirement in thirty years. The goal is to have milestones that are frequent enough to keep you motivated but significant enough to feel rewarding.

Reduce Emotional Reactions to Market Fluctuations

Successful investors and those who struggle often differ in how they handle emotions during market ups and downs. I’ve helped many clients through tough times like the 2008 crisis, the 2020 pandemic, and the 2022 inflation. Those with clear goals and risk plans kept their wealth, while emotional decisions led to losses.

Market swings can trigger strong feelings. Your brain sees a 20% drop as a threat, like danger. Without a goal-based plan, you might make decisions that harm your long-term finances.

Investment goals act as emotional brakes during storms. They remind you of your purpose and provide a rational view of market changes. Let’s look at ways to use your goals to stay calm.

“read also: How Market Changes Affect Investment Goals for Beginners“

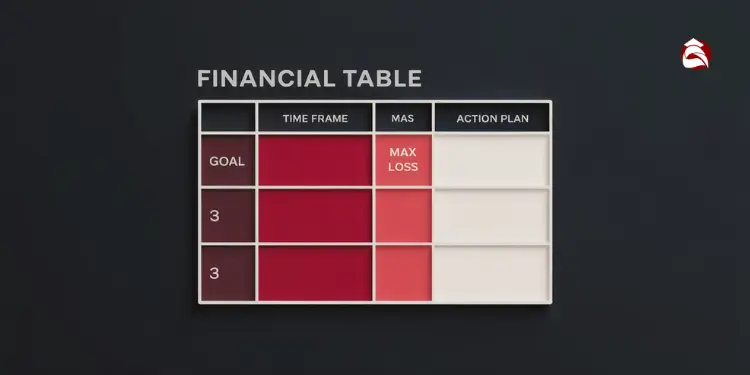

Set Risk Limits Before Buying Assets

Deciding on risk after markets drop is like planning your escape while your house burns. Set clear risk limits before buying assets as part of your goal-setting.

For each goal, decide on your maximum loss in percentage terms. For a home down payment in two years, you might accept a 5-10% loss. For retirement, you could handle a 25-30% drop, knowing markets usually recover.

Write down these risk limits and keep them with your goals. This helps you avoid making hasty decisions when markets fall. Your goals and risk tolerance work together as safeguards.

I suggest making a simple table for each financial goal:

| Investment Goal | Time Horizon | Maximum Acceptable Loss | Action If Exceeded | Reminder of Purpose |

|---|---|---|---|---|

| Emergency Fund | 0-1 years | 0-2% | Move to FDIC-insured accounts | Financial security during unexpected events |

| Home Down Payment | 2-5 years | 5-10% | Shift to 80% bonds/20% stocks | Stable housing for your family |

| College Fund | 5-15 years | 15-20% | Review allocation quarterly | Education without excessive debt |

| Retirement | 15+ years | 25-35% | Stay invested, consider adding during dips | Financial independence in later years |

IMPLEMENTATION CONSTRAINT:

Mortgage lenders and financial planners widely apply the 28/36 rule—housing costs ≤ 28 % of gross income and total debt ≤ 36 %—to preserve cash flow and curb over-leverage. Ref.: “Kagan, J. (2024). 28/36 Rule: What It Is, How to Use It, Example. Investopedia.” [!]

Plan Exit Strategies for Volatile Periods

Emotional decisions thrive in uncertainty. Without a plan, fear can lead to worst-case scenarios. Create simple exit strategies tied to your goals.

For each investment, set three thresholds: minor, serious, and major drops. Decide in advance what to do at each level. For long-term goals, rebalance if your allocation drifts by more than 5% or invest monthly, regardless of the market.

These plans remove the pressure of making decisions in the moment. They turn emotional triggers into mechanical actions guided by your goals. When the S&P 500 dropped 34% in March 2020, my clients followed their plans, not panicking.

Your exit strategy should also include who to consult before big portfolio changes. This could be a financial advisor, a knowledgeable friend, or even your future self through a 48-hour “cooling off” period.

Schedule Regular Reviews to Stay Rational

The most dangerous behavior is checking your portfolio too little or too much. Regular reviews help you stay focused on your goals, not just market news.

Set reviews based on your goals, not market movements. Quarterly reviews are common. Focus on goal progress, not short-term performance.

Create a structured review template. Start with your goals and time horizons before looking at numbers. This order helps you stay focused on long-term goals.

Ask goal-centered questions during reviews. “Am I still on track for retirement?” instead of “Why did my portfolio underperform last month?” This keeps you focused on your financial journey, not market noise.

Investors who review their goals regularly experience less anxiety during downturns. Their decisions become more consistent and less reactive. The review process reinforces rational thinking about your financial future.

Remember, your investment goals are your rational counter to market emotions. By setting risk limits, planning exits, and reviewing regularly, you keep your financial plan on track. These emotional guardrails prevent the common mistake of buying high and selling low, a pattern that destroys more wealth than any market correction.

Align Asset Allocation With End Goals

When you create your investment portfolio, matching your asset allocation with your goals is key. I’ve seen big differences in how well investors do when they tailor their portfolios to their goals. Your investment plan should match your life goals, not just a generic risk profile.

Every goal needs a different investment strategy. Saving for a house in 18 months is different from saving for retirement in 30 years. It’s not just small changes to a standard plan—it’s about making each goal its own special plan.

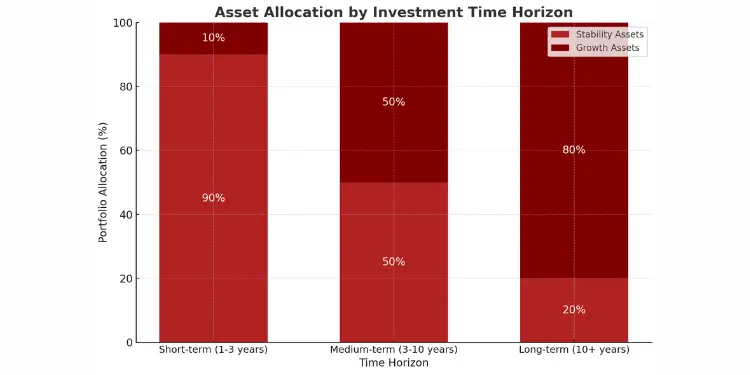

Time horizons play a big role in your investment choices:

| Time Horizon | Appropriate Allocation | Investment Options | Expected Rate of Return | Primary Consideration |

|---|---|---|---|---|

| Short-term (1-3 years) | 80-100% stability assets | High-yield savings, money market funds, short-term bonds | 1-3% | Capital preservation |

| Medium-term (3-10 years) | 40-60% growth assets | Balanced ETFs, bond funds, dividend stocks | 4-6% | Moderate growth with reduced volatility |

| Long-term (10+ years) | 70-90% growth assets | Stock ETFs, growth investments, real estate | 7-10% | Maximum growth potential |

Think of your portfolio as separate parts for different goals. This is called “destination mapping.” Each dollar should have a purpose in your financial future. This way, you get the right mix of investments for your needs, not just random numbers.

For example, saving for college in 12 years means you can take more risks than saving for taxes next year. The real value of an investment is how well it meets your financial needs, not just its numbers.

Your investment strategy should change as you get closer to your goals. A retirement fund might start with mostly stocks when you’re young, then switch to bonds as you get older. It’s about how much time you have left until you need the money, not just your age.

Start by listing your top three financial goals and when you need them. Then check if your investments match these goals. If not, it might be time to reallocate to better support your goals.

“read also: Why You Should Not Delay Your Investment Goals“

Optimize Tax Strategy Through Goal Timing

Your investment goals’ timelines offer natural tax optimization opportunities that many beginners overlook. Strategic tax planning can save 0.5-1.5% annually, which is a lot over time. This can add a lot to your wealth, more than trying to get high returns.

The timing of your goals is key for tax planning. A college fund in five years needs a different plan than retirement savings in thirty years. By understanding these differences, you can choose the best investment account for each goal.

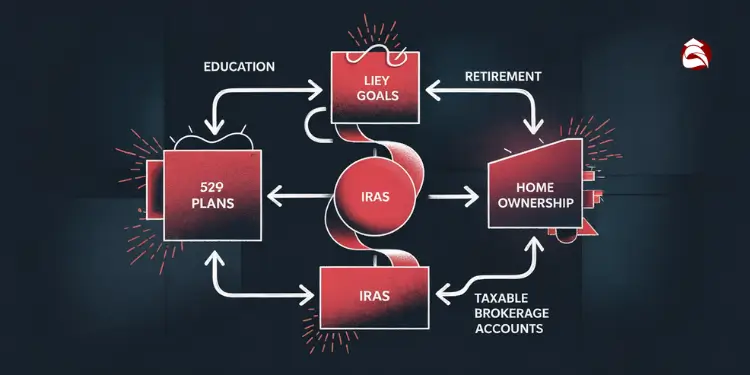

Matching goals with the right tax-advantaged accounts is powerful. Here are some examples:

- Education funding – 529 plans offer tax-free growth for qualified education expenses

- Early retirement – Roth IRA contributions can be withdrawn penalty-free before retirement age

- Home purchase – First-time homebuyers can withdraw up to $10,000 from IRAs without penalty

- Healthcare costs – HSAs provide triple tax advantages when used for medical expenses

- Legacy planning – Certain accounts receive stepped-up basis treatment at inheritance

529 plans allow tax-free growth and withdrawals for qualified education expenses—including up to $10,000 per year for K-12 tuition—making them a premier vehicle for college funding. Ref.: “Savingforcollege.com Editorial Team. (2025). 529 Qualified Expenses: What Can You Use 529 Money For? Savingforcollege.com.” [!]

The order in which you fund these accounts is crucial. I’ve seen two investors with the same goals have very different outcomes. One focused on tax-advantaged accounts first, while the other didn’t.

After 20 years, the tax-optimized investor had nearly 20% more wealth. This wasn’t from taking more risk or finding better investments. It was from strategic planning around variable income and choosing the right accounts.

When planning your investments, consider these tax factors for each goal:

- Your current and projected future tax brackets

- The specific timeline for when you’ll need the money

- Whether you’re investing a lump sum or making regular contributions

- State tax implications based on your residence

- Special tax provisions that align with your goals (education, first home, etc.)

Many financial advisors focus on investment selection but overlook tax planning. This can lead to costly changes later. By considering taxes early, you avoid these problems and keep more of your returns.

Setting tax-efficient investment boundaries is crucial, especially when goals change. Life doesn’t always go as planned. A tax-optimized strategy helps you adjust without big tax hits when priorities change.

Remember, tax rules change often, so regular reviews are key. Schedule annual tax planning sessions to keep your strategy up to date. This discipline can save a lot of wealth over time.

Celebrate Achievements to Reinforce Investing Habits

Recognizing your investment wins is powerful. It keeps you going, even when market knowledge doesn’t. Over the years, I’ve noticed a pattern. Those who celebrate their financial wins stay committed, even when things get tough.

Set personal celebration points to keep your motivation high. This helps you stay focused on your goals. It gives you the energy to keep moving forward.

Make a special “victory fund” for 3-5% of your goals. This positive feedback loop is what your brain needs. It keeps you going without losing sight of your goals.

When you reach your target, take a moment to celebrate. Acknowledge the discipline that got you there. Then, set new goals to keep pushing forward.

Read More:

Reinvest Windfalls Toward the Next Goalpost

Unexpected money is a great chance to boost your investments. Use bonuses, tax refunds, or gifts wisely. Follow the 70/30 rule: 70% goes to your goals, and 30% for fun or emergencies.

This way, you avoid treating surprise money as separate from your strategy. Linking it to your financial plan keeps you moving. It also gives you a psychological boost.

Have a clear plan for each windfall before it comes. This helps you avoid emotional decisions. By doing this, you make your investment journey more sustainable. You build discipline and rewards into your financial approach.

{kind=link}