Personal liability protection often falls short when major accidents happen. Umbrella insurance gives you that extra layer of coverage. It goes beyond your standard home or auto policies.

Have you thought about what happens if someone gets hurt badly on your property? Their medical bills might be more than your homeowner’s coverage can handle.

The truth is scary—the average liability lawsuit in America is over $1.5 million. Yet, most standard policies only cover up to $300,000. As financial advisor Warren Buffett says, “It takes 20 years to build a reputation and five minutes to ruin it.”

In my decade helping Idaho families, I’ve seen how one accident can threaten everything. One client was saved from financial disaster when a child got hurt on their property. Their extra protection covered the $750,000 settlement that would have ruined their retirement savings.

Personal umbrella coverage isn’t just for the wealthy. It’s for anyone who wants to protect their assets or future earnings.

Quick hits:

- Covers legal fees beyond primary policies

- Protects current and future assets

- Typically costs less than $400 annually

- Extends protection across multiple properties

- Safeguards against today’s higher settlements

Umbrella Insurance Meaning and Core Purpose

Umbrella insurance is an extra layer of protection. It kicks in when your standard policies are used up. It’s like a safety net for unexpected big expenses.

It’s not just for one thing. It protects your whole financial life. It’s a boost to your insurance when you really need it.

Extends Liability Beyond Primary Policies

When a claim is too big for your main insurance, umbrella steps in. For example, if your auto insurance has $300,000 and you owe $700,000, your umbrella pays the extra $400,000.

This extra layer works with your current policies. It kicks in automatically when you hit your limit. You don’t have to deal with extra claims or complicated steps.

Umbrella insurance also covers more than just more money. It includes things your main insurance might not. This can be libel claims, false arrest, or liability on rental properties.

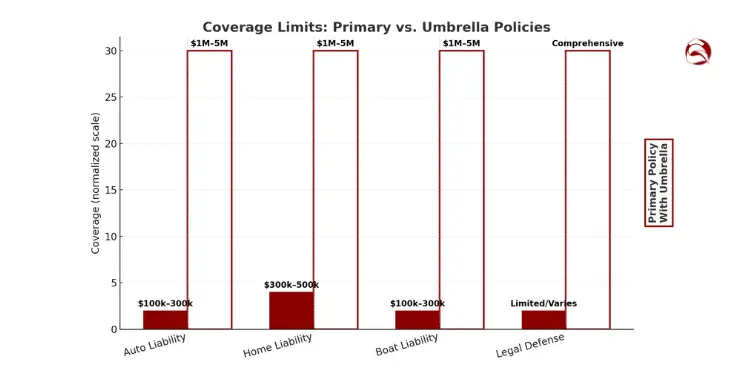

| Coverage Type | Primary Policy Typical Limits | With Umbrella Addition | Protection Increase |

|---|---|---|---|

| Auto Liability | $100,000-$300,000 | $1,000,000-$5,000,000 | 3-50× more coverage |

| Home Liability | $300,000-$500,000 | $1,000,000-$5,000,000 | 2-16× more coverage |

| Boat Liability | $100,000-$300,000 | $1,000,000-$5,000,000 | 3-50× more coverage |

| Legal Defense | Limited/Varies | Comprehensive | Significant enhancement |

Protects Savings from Large Lawsuits

Umbrella insurance is great for protecting your money from big lawsuits. Without it, your savings, investments, and home could be at risk.

Big lawsuits can cost a lot. A serious car accident can lead to damages over $500,000. Medical bills alone can go over your insurance limits, leaving you with a big bill.

Your umbrella policy is like a shield for your money. For a small price, you get protection against huge financial losses. This can save your retirement or stop you from having to sell important things.

This protection is for your whole family. It covers everyone living with you, including kids and college students. This gives you peace of mind when risks are higher.

Key Protections Personal Umbrella Policies Provide

Understanding what a personal umbrella policy offers is key. It’s a layer of protection many homeowners don’t know they need until it’s too late. As an insurance expert, I’ve seen how these policies help fill gaps in coverage.

A personal umbrella policy is like a safety net. It kicks in when your regular insurance runs out. You can get coverage from $1 million to $5 million or more, depending on your needs.

Core Liability Protections

Umbrella liability insurance covers many important areas. These include:

- Bodily injury to others – Covers medical bills, lost wages, and pain and suffering when someone is injured on your property or due to your actions

- Property damage to others – Pays for repairs or replacement when you damage someone else’s belongings

- Legal defense costs – Covers attorney fees, court costs, and other legal expenses even if a lawsuit is groundless

I helped a client whose teenage driver caused a multi-car accident. The family’s auto policy covered $300,000 in damages, but the total claims exceeded $800,000. Their umbrella policy covered the remaining $500,000, protecting their home and retirement savings from being seized.

Extended Protection Beyond Standard Coverage

Umbrella insurance is valuable because it covers things standard policies often don’t. Your umbrella policy typically covers:

- Defamation claims – Including libel (written) and slander (spoken)

- False arrest or imprisonment – Legal costs if you’re accused of wrongfully detaining someone

- Malicious prosecution – Protection if you’re sued for wrongfully initiating legal proceedings

- Invasion of privacy – Coverage for claims related to violating someone’s right to privacy

- Wrongful eviction or entry – Protection for landlords facing related claims

These protections are more important than ever in our digital age. A careless comment on social media could lead to a defamation lawsuit. Or, a neighborhood dispute might turn into claims of harassment or privacy invasion.

Global Coverage Benefits

Unlike many standard insurance policies, umbrella policies cover incidents worldwide. This is great for families who:

- Travel internationally for vacation

- Own property in other countries

- Send students abroad for education

- Work temporarily in international locations

This global protection ensures you’re not exposed to financial risk when away from home. For example, if you accidentally damage a priceless artifact while touring a museum in Europe, your umbrella policy would likely cover the damages that your homeowners policy might exclude.

What Umbrella Insurance Doesn’t Cover

While umbrella insurance is very helpful, it does have some limits. Knowing these gaps helps you plan your insurance strategy better:

- Your own injuries or property damage

- Damage caused by business or professional activities

- Intentional or criminal acts

- Liability assumed under contract

- Damage to your own property

For business-related liability, you’ll need separate professional liability or commercial umbrella coverage. Personal umbrella policies focus on personal risks.

| Coverage Type | Standard Insurance | Umbrella Policy Addition | Real-World Protection Example |

|---|---|---|---|

| Bodily Injury | Typically $100K-$300K limit | Extends to $1M-$5M+ | Guest falls down your stairs, suffers permanent disability requiring long-term care |

| Property Damage | Often capped at $100K | Covers excess up to policy limit | Your teenager crashes into a luxury vehicle causing $250K in damages |

| Legal Defense | Limited to policy amount | Additional defense costs covered | Complex liability lawsuit with $175K in legal fees beyond standard coverage |

| Defamation/Privacy | Often excluded | Typically included | Social media post leads to $400K defamation claim against your family member |

| International Incidents | Usually excluded | Worldwide coverage | Accidentally injuring someone while on vacation in Italy |

When thinking about getting a personal umbrella policy, consider your current assets and future earnings. Many people only think about protecting what they own today. But a big liability judgment could also affect your wages for years.

The cost of umbrella liability insurance is low, usually $150-$300 a year for $1 million in coverage. For most families, the peace of mind it offers is worth the small price.

Who Needs Umbrella Coverage and Why

Not everyone needs umbrella insurance. But, if you have a lot of assets or take on risks, you might need it. Unlike car or home insurance, there’s no law that says you must have umbrella coverage. It depends on how much you have and your lifestyle.

Many families find out too late that their insurance isn’t enough. Personal umbrella coverage helps by adding extra protection. It’s more important as you get wealthier or take on more risks.

Here are signs you might need umbrella insurance:

- You’ve saved a lot of money or have investments

- You own more than one home

- You have teenage or new drivers in your family

- You often have parties at your house

- You help out on nonprofit boards or volunteer

- You write reviews online about products or businesses

Umbrella insurance isn’t just for the rich. Anyone with something to lose or who takes on risks can benefit. Even small savings need protection from big lawsuits.

Common High Liability Risk Scenarios

Some things in your life can make you more likely to face big lawsuits. Knowing these risks helps you decide if you need umbrella insurance. Let’s look at some common scenarios.

Things like pools, trampolines, and playgrounds can attract visitors. This increases the chance of injuries on your property. Umbrella insurance helps when your home insurance isn’t enough.

Having pets, like some dog breeds, can also be risky. Even friendly dogs might bite under stress. This can lead to big medical bills and lawsuits that your insurance might not cover.

The average dog bite claim in the United States now exceeds $50,000. Some cases can result in judgments over $100,000 when there’s scarring or disability.

In 2024, insurers paid $1.57 billion on 22,658 dog-related injury claims, with the average payout hitting $69,272—costs that can quickly pierce standard homeowner limits.Ref.: “Insurance Information Institute. (2025). Spotlight on: Dog Bite Liability. III.” [!]

Teenage drivers in your home increase your risk. While your car insurance covers some, umbrella insurance helps with more serious accidents. Young drivers are inexperienced and more likely to be in accidents.

Having rental properties also raises your liability risk. Claims from tenants, property damage, or even lawsuits for discrimination can go beyond your landlord policy. Umbrella insurance is key for property managers.

Online activities can also lead to liability risks. Posting negative reviews, making comments on social media, or blogging can lead to defamation claims. Umbrella insurance often covers these risks that many overlook.

| Risk Factor | Potential Liability | Standard Policy Limitations | How Umbrella Insurance Helps |

|---|---|---|---|

| Swimming Pool | $300,000-$1,000,000+ | Homeowners typically caps at $300,000 | Provides additional $1-5 million coverage |

| Teenage Drivers | $250,000-$2,000,000+ | Car insurance policies often limit to $250,000 per person | Covers excess damages beyond auto policy limits |

| Dog Ownership | $50,000-$500,000+ | Some breeds excluded from homeowners coverage | Offers broader protection for pet-related incidents |

| Rental Properties | $100,000-$1,500,000+ | Landlord policies have strict coverage caps | Extends liability protection for tenant claims |

| Online Activities | $50,000-$1,000,000+ | Often excluded from standard policies | Covers defamation and privacy violation claims |

Traveling abroad also increases your liability risk. Many insurance policies don’t cover you outside the U.S. Umbrella insurance can protect you when you’re abroad.

Whether or not to get umbrella coverage depends on your risk tolerance and finances. For most people, the cost (usually $150-$300 a year for $1 million coverage) is worth the peace of mind.

Before getting a quote, check your current policies for gaps. This helps make sure your umbrella policy fits with your other insurance. It gives you full protection against unexpected risks.

Umbrella Policy Pricing Factors and Savings

Umbrella policy pricing is based on several factors. This high-limit coverage is actually quite affordable. For most families, it’s a great value in the insurance world.

An ACE Private Risk Services report shows umbrella insurance costs about $383 a year for $1 million coverage. That’s just over $1 a day. It can save you from big financial losses.

Umbrella policies are affordable because they cover a lot. They offer extra protection beyond your standard policies. They also cover areas your primary insurance might not.

Factors That Determine Your Premium

Insurance companies look at several things to set your umbrella policy premium:

- Location – Where you live affects rates based on local claim statistics and legal environments

- Credit history – Many insurers use credit-based insurance scores to help determine pricing

- Driving record – Traffic violations and accidents can significantly impact your rates

- Assets requiring protection – More properties, vehicles, or watercraft typically mean higher premiums

- Number of household members – More drivers or dependents may increase your risk profile

Your risk of filing a claim affects your premium. If you have teenage drivers, host parties, own a pool, or have other high-risk factors, expect higher premiums.

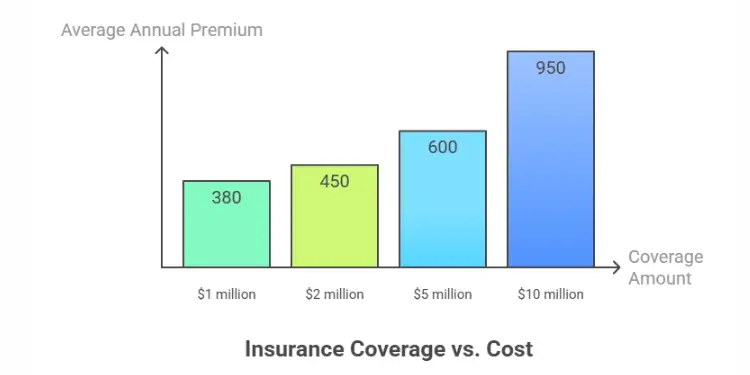

Cost Comparison by Coverage Amount

| Coverage Amount | Average Annual Premium | Monthly Cost | Daily Cost | Value Ratio* |

|---|---|---|---|---|

| $1 million | $380 | $31.67 | $1.04 | Excellent |

| $2 million | $450 | $37.50 | $1.23 | Excellent |

| $5 million | $600 | $50.00 | $1.64 | Excellent |

| $10 million | $950 | $79.17 | $2.60 | Very Good |

*Value ratio compares protection amount to premium cost

Trusted Choice says umbrella policies start at $200 a year. For $1 million coverage, the average is about $380. This makes umbrella insurance a great deal for the protection it offers.

Why Umbrella Insurance Offers Superior Value

Umbrella policies are a smart choice. They offer a lot of protection for a good price. For example, adding $200,000 to your auto liability might cost as much as a $1 million umbrella policy for all your assets.

Insurance companies can offer umbrella policies at good rates because:

- They require you to have a lot of underlying coverage first

- Catastrophic claims are rare

- They exclude high-risk activities

- They spread the risk among many policyholders

Saving on Umbrella Insurance

I’ve helped many clients save on umbrella insurance. Here are some tips:

- Bundle policies – Most insurers give discounts for umbrella coverage with home and auto policies

- Maintain good credit – Better credit scores can lower your insurance rates

- Drive safely – Clean driving records mean lower premiums

- Increase deductibles – Higher deductibles on other policies can help offset umbrella costs

- Review coverage annually – Update your insurance as your life changes

Umbrella insurance offers protection your standard policies might not. It’s a small price to pay for the extra security it gives. It’s very valuable for families with growing assets or more liability risks.

“Umbrella insurance is a great value. For a small premium, you get a lot of extra liability protection. It can protect your financial future.”

When looking at umbrella policy costs, think about the protection it offers. The peace of mind it gives is worth the investment many times over.

Buying Umbrella Insurance Step by Step

When you want more liability protection, buying umbrella insurance the right way is key. I’ve helped many families get the right coverage without spending too much. Let’s go through the steps to get an umbrella policy that protects your assets well.

First, talk to your current insurance company. They might give you a discount for adding an umbrella policy. But don’t stop there. Get quotes from at least two other companies to compare prices and what they offer. An independent agent can help you compare different companies.

Requirements for Underlying Policy Limits

To buy umbrella insurance, you need to meet certain requirements for your current policies. Insurance companies need these minimums because an umbrella policy only kicks in after your main coverage is used up.

Most insurers want you to have:

- Homeowners insurance with $300,000 in personal liability coverage

- Auto insurance with $250,000 bodily injury per person and $500,000 per accident

- Property damage liability of $100,000 per accident

- Similar liability minimums for watercraft or recreational vehicle policies if you own them

Most insurers require at least $250 k auto liability and $300 k homeowners liability before issuing even a $1 million umbrella—plan to raise those base limits first.Ref.: “Insurance Information Institute. (2025). Should I Purchase an Umbrella Liability Policy? III.” [!]

If your current policies don’t meet these limits, you’ll need to increase them. This will change your premium costs. But, the total cost is usually less than facing a lawsuit without enough protection.

When looking at quotes, notice how different companies set their requirements. Some might need higher limits, while others offer more flexibility. The goal is to find a balance between good protection and affordable prices.

Choosing Adequate Coverage Limit Amount

Finding the right umbrella coverage amount depends on your financial situation and risks. While $1 million policies are common, they might not be enough for everyone.

To figure out your coverage needs, use this formula:

- Add up the value of your assets (home, investments, savings, etc.)

- Calculate your future income (annual income × number of working years left)

- Think about any extra risks (teenage drivers, swimming pool, rental properties, etc.)

- The total is how much you could lose in a lawsuit

Most advisors suggest starting with at least $1 million in coverage. But if your net worth is higher or you have big risks, consider $2-5 million policies. Remember, umbrella policies are pretty affordable—usually $150-300 a year for each million in coverage.

When choosing a policy, ask about their claims process and legal defense coverage. The best policies pay judgments and cover legal fees without using up your policy limit. This can save you thousands if you’re sued.

Also, check your coverage needs every year. As your assets grow or your life changes, you might need to update your umbrella policy. Insurance should grow with you, protecting your future earnings and assets.

“The most common mistake I see is people underestimating their liability exposure. It’s not just about what you own today—it’s about protecting your future earnings and assets as well.”

After picking an insurer and coverage amount, applying is easy. Most companies just need some basic info about your policies, property, vehicles, and family. Once approved, your umbrella policy starts right away, giving you that extra protection for your financial future.

Read More:

Next Actions Securing Personal Umbrella Protection

Ready to move forward? Start by checking your current policy limits. Umbrella insurance acts as an extra safety when your standard coverage isn’t enough. It usually costs about $380 a year for $1 million in protection.

Next, make a list of your assets. This includes your home, savings, investments, and future income. Remember, while 401(k)s are usually safe, IRAs might not be. Knowing what you have helps figure out how much extra coverage you need.

Then, talk to your current insurer to see if they offer umbrella policies. Many give discounts if you add this to your existing coverage. Ask how it helps protect you from things like dog bites or slip-and-fall accidents.

If you rent, don’t think you’re off the hook. Almost 60% of renters don’t have the right insurance. Standard renters policies (usually $100,000) might not cover you enough.

Lastly, get quotes from at least three different providers. Look at the price, policy limits, and what’s not covered. The small cost of umbrella insurance could save you millions if you face a big liability claim. It keeps your home, savings, and future safe.

{kind=link}