Deciding why get travel insurance is a big choice before booking flights. It offers more than just peace of mind. Without it, a medical evacuation from Europe could cost over $50,000.

A recent survey showed 38% of American travelers faced trip issues last year. Yet, only 21% had the right insurance. One client said, “The $200 policy saved me from a $7,000 hospital bill in Costa Rica.”

In my decade helping Idaho families plan trips, I’ve seen many happy travelers. They were glad they protected their investment. The 5-6% extra cost is worth it for the safety it offers.

Quick hits:

- Protects your hard-earned vacation investment

- Covers unexpected medical emergencies abroad

- Reimburses for cancellations and delays

- Assists with lost luggage situations

- Provides 24/7 emergency assistance services

Travel insurance scope and primary protections overview

Travel insurance offers protection for unexpected costs and emergencies. It’s not a one-size-fits-all product. A good policy fits your journey needs and covers three key areas: your trip, health, and belongings.

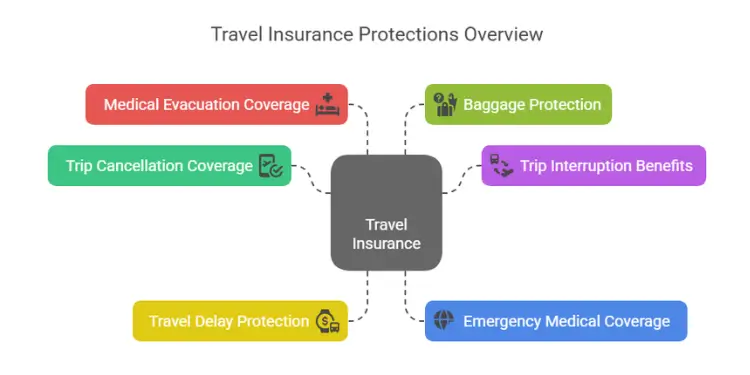

Most travel insurance plans have six main protections. These work together to protect you from financial loss. Knowing these protections helps you choose the right policy for your trip.

The Six Core Protections in Most Travel Insurance Policies

- Trip Cancellation Coverage: Helps if you must cancel your trip for reasons like illness or family emergencies. It covers up to 100% of your prepaid costs.

- Trip Interruption Benefits: Covers costs if you cut your trip short. It pays for the unused trip and gets you home early.

- Travel Delay Protection: Gives daily money for meals and hotels if flights are delayed. This helps avoid extra costs during waits.

- Emergency Medical Coverage: Pays for medical help if you get sick or hurt abroad. Most health plans don’t cover you outside the U.S.

- Medical Evacuation Coverage: Pays for moving you to better medical care or home. Costs can be over $100,000 in remote places.

- Baggage Protection: Reimburses for lost, stolen, or damaged items. It has limits per item and a total amount.

When looking at travel insurance companies, check how they offer these protections. Some offer all six in one package. Others let you pick what you need.

| Protection Type | What It Covers | Typical Coverage Limits | Key Considerations |

|---|---|---|---|

| Trip Cancellation | Prepaid, non-refundable expenses | 100% of trip cost | Verify covered reasons for cancellation |

| Medical Expenses | Emergency treatment abroad | $50,000-$500,000 | Check for pre-existing condition waivers |

| Evacuation | Emergency transport to hospitals or home | $250,000-$1,000,000 | Higher limits for remote destinations |

| Baggage | Lost, stolen, or damaged items | $500-$2,500 | Note per-item limits and exclusions |

| Travel Delay | Accommodations, meals during delays | $100-$200 per day | Check minimum delay requirement (hours) |

The value of your insurance depends on its limits and what it doesn’t cover. For example, $50,000 in medical coverage might be enough for a weekend in Canada. But it might not cover a month in Southeast Asia.

Insurance policies also differ in what they consider valid reasons for trip cancellation. Most cover illness and injury. But fewer include work-related cancellations or fear of traveling to places with safety concerns.

Travel insurance isn’t about covering everything that could possibly go wrong. It’s about providing financial protection against the most likely and most costly travel disruptions.

When looking at policies, focus on three key things:

- Coverage limits for each protection category

- Exclusions and restrictions that might void coverage

- Documentation requirements for filing claims

There are different types of travel insurance for different travelers. Business travelers might need coverage for electronics and frequent changes. Families need higher medical limits and coverage for all members. Adventure travelers should check if their activities are covered.

The best travel insurance isn’t always the most expensive. It’s the one that fits your travel needs and offers enough protection against financial risks.

Read More:

Trip cancellation interruption and medical benefits

Travel insurance has three main parts: trip cancellation, interruption, and medical benefits. These help protect you from unexpected costs. They make sure you don’t lose money if your trip is changed by illness, family issues, or natural disasters.

With trip cancellation insurance, you get back money for things you paid for but can’t use. If you have to stop your trip early, interruption insurance helps. Medical benefits are key when you’re far from home and need medical help.

Nonrefundable Expenses Reimbursement Scenarios Outlined

Life can surprise us, and trip cancellation and interruption insurance helps. They cover up to 100% of your trip costs if you have to cancel or stop early for certain reasons.

Here are some times when you might get your money back:

- Medical emergencies – You, your traveling companion, or a family member becomes seriously ill or injured before or during your trip

- Unexpected death – The passing of you, a traveling companion, or immediate family member

- Natural disasters – Your destination becomes uninhabitable due to severe weather, wildfire, or earthquake

- Job loss – Involuntary termination of employment after policy purchase

- Jury duty or legal proceedings – Court appearances you can’t reschedule

For example, if you paid $3,500 for flights, $2,000 for hotel, and $1,500 for activities, you could get this money back if you cancel for a covered reason. Without insurance, you might only get some of your money back or lose it all.

Trip interruption insurance works the same way but if you’ve already started your trip. If you have to go home early, it covers the costs of your trip and getting home.

Emergency Medical Evacuation Cost Coverage Details

Medical emergencies abroad can be very expensive without the right insurance. Travel medical insurance covers doctor visits, hospital stays, and more if you get sick or hurt while traveling.

Emergency medical evacuation is a big part of this. It pays for getting you to a hospital if you’re seriously sick or hurt. This might mean an air ambulance in remote areas.

| Evacuation Scenario | Estimated Cost Without Insurance | Typical Coverage Limit | Additional Benefits |

|---|---|---|---|

| Ground ambulance (local) | $500-$1,000 | 100% of cost | No out-of-pocket expense |

| Air ambulance (regional) | $20,000-$50,000 | $250,000-$500,000 | Medical escort included |

| Medical jet (international) | $50,000-$200,000+ | $500,000-$1,000,000 | Medical team & equipment |

| Repatriation of remains | $10,000-$25,000 | $25,000-$50,000 | Transportation arrangements |

Allianz says medical evacuation can cost from $20,000 to over $200,000. Most health insurance doesn’t cover you abroad. So, travel medical insurance is key for trips outside the U.S.

Comprehensive travel medical coverage also includes:

- Emergency medical and dental treatment

- Hospital room and board

- Prescription medications

- Follow-up care coordination

- 24/7 assistance services with medical professionals

When picking a policy, look at the limits for medical and evacuation. For far-off places or adventure trips, choose at least $100,000 for medical and $500,000 for evacuation.

Claim filing process and documentation requirements

Learning how to file a travel insurance claim is key. You need to know what your insurance wants and when. I’ve helped many people in Idaho Falls with this. Being organized and acting fast can really help.

First, call your insurance if travel problems happen. Most have 24/7 help lines for travelers. Save this number in your phone before you go.

Step-by-Step Claim Filing Process

Filing a claim is pretty straightforward:

- Notify your insurer right away – Most policies want you to tell them within 24-48 hours. Waiting too long can hurt your claim.

- Ask for a claim form – Your provider will send you the right form for your situation.

- Get your documents ready – Collect all important papers and receipts while things are fresh in your mind.

- Send in your claim – Follow the exact steps they tell you for submitting your claim.

- Keep track of your claim – Remember your claim number for all future talks with your agent.

Travelers who follow these steps well get their claims processed faster. Keeping in touch with your insurance can make things smoother.

Essential Documentation Checklist

Each type of claim needs different papers. Here’s what you might need for common ones:

| Claim Type | Required Documentation | Submission Timeline | Common Pitfalls |

|---|---|---|---|

| Trip Cancellation | Booking confirmations, cancellation notices, receipts for non-refundable expenses | Within 30 days of cancellation | Missing original booking documentation |

| Medical Expenses | Medical reports, hospital bills, doctor’s statement of necessity | Within 90 days of treatment | Incomplete diagnosis documentation |

| Baggage Loss | Police report, airline PIR form, itemized list with values | Within 24 hours of discovery | No proof of ownership for valuable items |

| Travel Delay | Airline verification of delay, receipts for additional expenses | Within 30 days of delay | Missing official delay confirmation |

Insurance often wants the real deal, so scan your documents first. This way, you have a copy if something gets lost.

Documentation Best Practices

After looking at many claims, I found some tips to help you get approved:

- Take photos of everything – Capture damage, accident scenes, and property damage.

- Keep a travel journal – Write down dates, times, and names of officials for all incidents.

- Request written statements – Ask for written accounts from hotel managers, tour guides, or doctors when needed.

- Save all receipts – Even small purchases during a delay or disruption might be covered.

- Obtain police reports – For theft or crime claims, you need official reports.

“The difference between a denied claim and full reimbursement often comes down to documentation quality and submission timing.”

Before you go, ask for a claim packet preview. Many don’t know what’s covered until it’s too late. Your travel agent or insurance provider can help.

If your claim is denied, don’t give up. About 35% of denied claims are approved on appeal with more info. Insurance agents must tell you why it was denied, helping you appeal.

Travel insurance is great for most trips. Knowing how to use it makes it even better. It’s not just about having coverage, but knowing how to get it when you need it.

Related Posts:

Situations warranting coverage before booking confirmation

Planning trips to tough places or for fun activities means you need travel insurance early. I’ve seen many travelers buy insurance too late. They find out their risks aren’t covered.

Buying travel insurance on time is key. Many policies offer the best benefits when bought within 14-21 days of your deposit. This early purchase lets you get benefits like pre-existing condition waivers and “cancel for any reason” options.

Travel insurance is a must in certain situations. If your trip has big upfront costs, you’re going to far-off places, or you’ll be doing risky activities, get insurance early. Without it, you could face big financial losses.

High Risk Destinations and Adventure Activities

Some places and activities need special insurance because they’re very risky. Even if you’re healthy, traveling to areas with poor medical care is risky. You need to choose policies made for these high-risk situations.

Adventure travel often needs special insurance. Here are some high-risk situations that need insurance before booking:

- Remote or politically unstable destinations where emergency evacuation might be necessary

- Adventure activities like mountaineering, scuba diving, or helicopter skiing that standard policies exclude

- Hurricane-prone regions during storm season when weather disruptions are likely

- Countries with inadequate medical infrastructure where getting sick or injured could require expensive evacuation

- Multi-destination itineraries with complex connections increasing delay/cancellation risks

For adventure seekers, regular insurance often isn’t enough. If you plan to get sick or hurt while rock climbing in Thailand or skiing off-piste in Japan, regular insurance may not cover your medical expenses. Specialized adventure travel policies offer the specific protections you need for high-adrenaline activities.

| Risk Category | Example Scenarios | Special Coverage Needed | Typical Cost Impact |

|---|---|---|---|

| Remote Destinations | Himalayan trekking, Amazon expeditions | Enhanced evacuation coverage | 25-40% premium increase |

| Extreme Sports | Heli-skiing, technical climbing | Adventure sports rider | 15-30% premium increase |

| Political Instability | Regions with travel advisories | Security evacuation benefits | 20-35% premium increase |

| Medical Deserts | Rural developing countries | Higher medical/evacuation limits | 15-25% premium increase |

Traveling to countries where your health insurance doesn’t cover you is another big reason to buy insurance early. Many insurance providers need local partners to pay for medical care abroad. Without the right coverage, you might have to pay a lot of money upfront.

“The time to discover your insurance doesn’t cover bungee jumping isn’t while you’re standing on the platform ready to jump.”

When traveling to places prone to natural disasters, buying insurance early is even more important. Once a disaster is named or forecasted, you can’t get insurance for it. Getting coverage early means you won’t worry about money if you get sick or hurt.

Many travel insurance policies have exclusions for certain countries and activities. Always read the fine print to know you’re covered. Knowing you’re protected before booking gives you peace of mind.

Selecting plan tiers fit travel itinerary

Choosing the right travel insurance is key. It should match your travel plans. This way, you won’t pay too much or not enough.

Many people make mistakes. They buy too much or too little insurance. It’s important to find the right balance.

First, check what insurance you already have. Some credit cards offer travel insurance. But, it’s not as good as travel insurance plans.

For example, American Express cards only cover round-trip flights. If you’re taking a one-way flight, you need more insurance. Also, only the Chase Sapphire Reserve® covers emergency medical and dental.

| Plan Tier | Best For | Key Benefits | Typical Cost |

|---|---|---|---|

| Basic | Domestic trips, minimal prepaid expenses | Trip cancellation, minimal medical | 4-6% of trip cost |

| Mid-level | International travel, moderate activities | Higher medical limits, evacuation coverage | 6-8% of trip cost |

| Premium | Remote destinations, adventure activities | Comprehensive medical, cancel for any reason | 10-12% of trip cost |

Big names like Allianz Global Assistance and Travel Guard have different plans. Look at these important things:

- Trip duration and destination (domestic vs. international)

- Total prepaid, non-refundable expenses

- Planned activities (like adventure sports)

- Health insurance gaps

- Age and health

If your trip is canceled, insurance can help with costs. But, how much it covers depends on the plan. Basic plans might only cover up to $10,000, while premium plans can cover $100,000 or more.

Medical coverage is very important. Your health insurance might not cover you abroad. For trips overseas, look for plans with at least $50,000 for medical emergencies and $100,000 for evacuations.

If you love adventure, make sure your plan covers it. Many basic plans don’t cover activities like skiing or diving. You might need a special rider or a premium plan.

I learned this lesson the hard way in Costa Rica when a basic policy wouldn’t cover a zip-lining accident. The $200 I “saved” on insurance resulted in a $3,500 out-of-pocket medical bill.

Travel insurance is a good investment if it matches your trip. Don’t just pick the cheapest plan. Think about your risks and choose the right coverage. The right plan gives you peace of mind without wasting money.

Check out the below:

Premium pricing variables and policy savings tactics

Travel insurance costs are usually 4% to 10% of your trip’s cost. For a $3,000 vacation, you might pay $185 for coverage. A $5,000 trip could cost $264 for protection. Recent data shows the average cost is about 6.87% of your trip’s total cost.

Impact of Trip Length on Premiums

Long trips mean more risks. A two-week trip to Southeast Asia costs more to insure than a short weekend trip. Each extra day adds more risk for baggage issues, flight delays, or medical needs.

Some insurers give discounts for trips over 30 days. If you’re planning a long trip, ask about these discounts.

Bundling Multi-Trip Annual Coverage Advantages

If you travel three or more times a year, annual policies save money. Instead of buying separate coverage for each trip, one policy covers all your travels for 12 months. These plans cover trip interruption, travel medical, and pre-existing medical conditions if you buy them early.

The best time to buy travel insurance is 14-21 days after your first trip deposit. This lets you get pre-existing condition waivers and optional benefits like cancellation insurance. Buying early also gets you better rates and more protection. For families, look for plans where kids under 17 are free when traveling with adults. This is a great way to save money without losing protection.

{kind=link}