Tracking home buying expenses from the start can save you a lot of money and stress. Buying a home has many costs, not just the down payment and monthly payments. Have you thought about how fast small fees add up while searching for a property?

Bankrate’s Home Affordability Report shows 78 percent of people struggle with affordability. Also, 40 percent of homeowners wish they had known about hidden costs like maintenance.

“Tracking expenses can make a big difference in the homebuying process,” I tell my clients in Greenville. After helping first-time buyers for nine years, I’ve seen how tracking expenses helps avoid surprises.

Creating a detailed budget for buying a house is key. Costs like inspection fees ($300-500) and title insurance (0.5% of your loan) need attention. Even professional movers can cost $883-$2,569, a cost many forget.

The national average home-inspection cost is $343, with most buyers paying between $296 and $424—figures that should be earmarked early in your budget.Ref.: “Hoffman, R. (2025). How Much Does a Home Inspection Cost? Angi.” [!]

Quick hits:

- Down payments range 3.5-20% of price

- Closing costs typically reach 2-5%

- Housing should stay under 28% income

- Save 1-2% annually for repairs

- Budget planners prevent financial surprises

Choose centralized expense tracking platform

A unified expense tracking platform is key for your home purchase journey. I’ve helped over 200 first-time buyers. They see how easy it is to lose track of expenses without tracking.

There are three good ways to track your homebuying budget. First, apps like Mint or YNAB have home purchase categories. They update your spending in real time.

Second, cloud-based spreadsheets are flexible. Google Sheets or Excel Online let you track expenses in different tabs. I have a free template that helps you stay on budget. Many clients like spreadsheets because they can be tailored.

Third, banking apps with tagging features are simple. They let you mark home purchase-related transactions. This keeps everything in one place.

“The average homebuyer underestimates their total expenses by $3,500 when using fragmented tracking systems instead of a centralized platform.”

Choose a platform that’s easy to use. You should record expenses right away. Your system should show your budget, generate reports, and let you upload receipts.

Knowing how much you can spend on a home is important. Your system should show your down payment, closing costs, reserves, and moving expenses. These can add up to a lot.

Try out your platform with small expenses before big payments. This makes sure you’re comfortable with it. It should work on both phones and computers.

Take 30 minutes to set up your system. Make categories for each stage of buying a home. This saves time and avoids surprises.

Categorize costs by buying stage

Breaking down your homebuying costs by stage makes it easier. It turns a complex journey into simple steps. First-time buyers often worry about unexpected costs.

By organizing your expenses, you can avoid surprises. This helps you stay in control of your finances.

Creating a system to track your expenses is key. It helps you prepare for costs before they happen. This way, you won’t have to rush to cover expenses.

“The most successful homebuyers I’ve worked with treat their purchase like a project with distinct phases. They know exactly which expenses fall into each phase and prepare according to. This organization alone can save thousands in rushed decisions and emergency loans.”

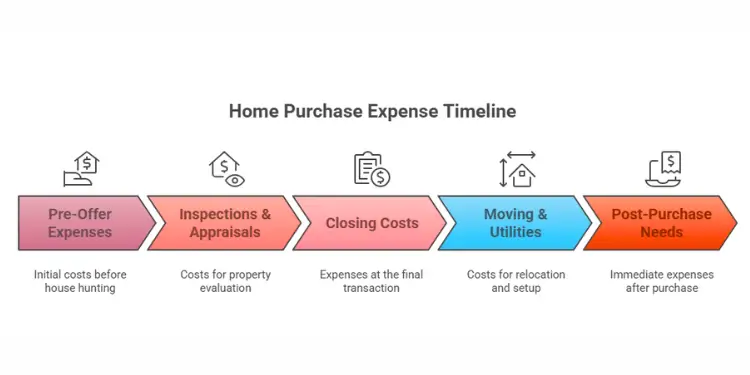

I suggest dividing your homebuying journey into five stages. Each stage has its own costs and timing. Learn more about costs when buying a house.

Pre-Offer and Early Process Expenses

Before you make an offer, several costs need their own category. These include pre-approval fees, credit report costs, and earnest money deposits.

Your earnest money is not an expense. It goes toward your down payment. But, you need it ready when making an offer. Keep it separate from your down payment.

Group Inspections, Appraisals, and Legal Fees

After your offer is accepted, you’ll face many professional fees. Home inspections cost $300-500. Specialized inspections add $100-300 each.

Appraisal fees are $300-450. Your lender needs this to check the property’s value. Legal fees vary but can be $500-1,500.

These costs come quickly, usually 7-14 days after your offer. Grouping them helps you prepare funds in advance.

“Learn More About: Frugal home buying tips for budget conscious buyers“

Closing Costs and Final Documentation

Closing costs are a big expense, 2-5% of your loan amount. They include application fees, origination fees, title insurance, and recording fees.

Many first-time buyers forget to budget for closing costs. Tracking them separately ensures you have enough money at closing.

Split Moving and Utility Activation Expenditures

Expenses don’t stop after you own the home. Moving costs need their own category. Professional movers charge $883-$2,569.

If you’re moving yourself, budget for truck rental and packing supplies. Utility activation fees and deposits should also be tracked here.

These costs hit your budget around the same time as closing costs. Separating them helps manage your finances better.

Post-Purchase Necessities

After buying, you’ll have immediate expenses. These include repairs, furniture, security systems, and lawn care equipment.

Some purchases can wait, but others need immediate attention. A separate category helps prioritize your spending.

| Expense Stage | Typical Timing | Cost Range | Payment Method | Budget Priority |

|---|---|---|---|---|

| Pre-Offer Expenses | Before house hunting | $50-125 + earnest money | Credit card or check | Essential |

| Inspections & Appraisals | 7-14 days after offer | $600-1,250 | Credit card or check | Non-negotiable |

| Closing Costs | At closing | 2-5% of loan amount | Wire transfer or cashier’s check | Essential |

| Moving & Utilities | Week of closing | $1,000-3,200 | Credit card, check, or cash | Essential but flexible |

| Post-Purchase Needs | First month of ownership | $500-5,000+ | Credit card or financing | Partially deferrable |

This method does more than track expenses. It helps you plan for upcoming costs. Knowing what expenses are coming helps you make better financial decisions.

I’ve seen this method save buyers from last-minute financial scrambles. It helps you avoid costly financing solutions by planning ahead.

“Check This Out: 50/30/20 budget breakdown of needs, wants, and savings“

Scan receipts immediately for digital records

When buying a home, it’s key to digitize receipts right away. This stops you from missing important costs and keeps a good financial record. Home buying paperwork can get very confusing. You’ll have lots of papers like inspection reports and receipts for unexpected expenses.

Many first-time buyers lose important documents. But, if you scan everything right away, you won’t lose anything. This also helps you keep track of your budget and taxes.

The best buyers follow a simple system to manage their costs:

- Use a dedicated scanning app on your phone. Apps like Adobe Scan make documents clear and easy to search.

- Give each file a clear name. Use a format like “2024-06-15_HomeInspection_425”. This makes finding costs easy.

- Save scans in cloud storage. This way, you can get to your records from any device. It’s great for talking about costs with others.

- Write down important details. Note who you paid, what service you got, and the property address. This helps when comparing costs of different homes.

This digital system helps you spot mistakes in your expenses. One client found a $750 mistake in title services thanks to her digital records. Without it, she would have lost that money.

It also helps with taxes. The IRS lets you deduct some homebuying costs. You need proof for things like mortgage interest and property taxes.

For those buying investment properties, keeping records is even more important. It helps with taxes when you sell. Having everything digitized from the start makes tax time easier.

It only takes a few seconds to scan each receipt. But, it saves a lot of trouble later. It helps you avoid surprises in your budget.

Remember, 40% of homeowners regret not planning for maintenance costs. Your digital system helps you track these costs early. This way, you can plan better for the future.

“The difference between financially confident homeowners and stressed ones often comes down to documentation habits established in the first week of the purchase process.”

Scanning receipts right away is more than just organizing. It’s like having a financial dashboard. It shows you the exact costs of owning a home. This helps you decide what expenses are worth it and what you can save on.

Make scanning receipts a part of your daily routine when buying a home. It may take a few seconds, but it saves a lot of trouble later. It helps you avoid missing out on important costs or tax deductions.

Set alerts for budget overruns quickly

Automated alerts for budget thresholds are a big help when buying a home. I’ve helped first-time buyers for nine years. Even small overruns can cause big financial stress.

Setting up alerts early can make a big difference. It helps you avoid last-minute scrambles. This is key to a smooth homebuying journey.

Budget overruns can happen to anyone. The trick is to catch them early. This way, you can avoid big problems that affect your home buying budget.

Start by setting alerts for each expense category. Use 80% of your budget as the main alert. For big costs like closing or down payments, add alerts at 70% and 90%.

Your income and cash flow need protection too. When unexpected costs come up, these alerts help you adjust. They also let you talk to your lender before things get worse.

Create SMS email notice thresholds

Make sure your tracking system sends alerts your way. Most apps offer SMS or email alerts. If not, tools like IFTTT can help.

Use three alert levels:

- Approaching Budget (80%) – Early warning to monitor spending

- Budget Reached (100%) – Time to evaluate priorities or adjust other categories

- Budget Exceeded (Any amount over) – Immediate action required

Alerts should come early enough for you to act. For example, an alert about inspection costs during the contract phase can help you negotiate. This is impossible if you find out later.

One client saved thousands by getting a better mortgage rate. They received an alert about closing costs and acted fast.

Zillow’s 2024 Consumer Housing Trends Report found 42 % of buyers said their closing costs exceeded expectations—reinforcing the need for a separate, closely monitored closing-cost category.Ref.: “Zillow Research. (2024). Consumer Housing Trends Report 2024 – Buyers. Zillow.” [!]

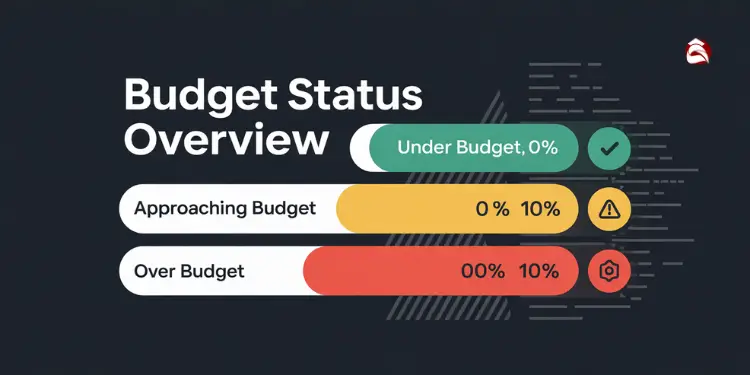

Weekly reports show your budget status. Green means you’re under budget, yellow means you’re getting close, and red means you’ve gone over. This helps you know where to focus.

These alerts are like guardrails for your homebuying journey. They turn home prices and budgets into clear, actionable steps. This protects your path to owning a home.

Remember, smart financial management is key to owning a home. By using these alert systems, you’re not just tracking expenses. You’re protecting your financial future and making closing day smoother.

Read More:

Generate weekly reports for stakeholder review

Weekly expense reports make buying a home clear. They keep everyone on the same page. This stops big money mistakes in your housing budget.

Lenders need to see your money plans. Show them what you’ve paid and what’s coming. This stops surprises that could delay your loan.

Co-buyers should know how much each is contributing. This is key for keeping costs in check. Housing costs should not be more than 28% of your.

Your agent needs to know about closing costs. This helps them get you a good deal. It might even save you money on interest.

Make your report simple. List what you’ve spent, what’s coming, and any changes. Use the right ways to share this info with everyone.

Do these reports every Sunday. It keeps everyone in sync. And makes sure everyone knows the financial plan for the week.

{kind=link}