Buying a home on a tight budget is possible without a lot of money. I’ve helped many first-time buyers find homes. They learned to use what they have wisely.

Did you know 80% of first-time buyers don’t make more money before buying? They just use what they have better. Studies show people who plan well can buy homes they thought were too expensive.

“The difference between wishful thinking and homeownership is often just a well-executed plan,” my mentor said. I’ve seen many people go from worried renters to confident buyers. They learned to invest in homebuyer education that pays off big time.

When you want to buy a home, you need to know all about your finances. Many first-timers only think about down payments. But there are hidden costs of buying a house that can mess up your plans.

Quick hits:

- Start with pre-approval, not house hunting

- Calculate total monthly costs, not just mortgage

- Consider location flexibility for better value

- Negotiate seller concessions when possible

- Explore first-time buyer assistance programs

Arrive at every showing with a fresh mortgage pre-approval. Freddie Mac notes that documented borrowing power “helps you stand out from other homebuyers,” speeds negotiations, and prevents wasted time on homes outside your price range. Ref.: “Freddie Mac. (2025). How Do I Get Pre-Approved for a Mortgage? My Home by Freddie Mac.” [!]

Prioritize must have features first

Buying a home on a budget means knowing what you really need. I’ve helped over 200 first-time buyers in Greenville. This simple rule can save you thousands.

Every dollar counts when you’re short on funds. Knowing what’s important is the first step.

Most buyers start with a long wish list. They want the best location, a modern kitchen, and more. But this can lead to trouble or spending too much.

Before looking at homes, make two lists. Do this with everyone who will buy the home.

Separate Needs Versus Wants Honestly

It’s key to know what you need versus what you want. Finding a home that fits your life is important.

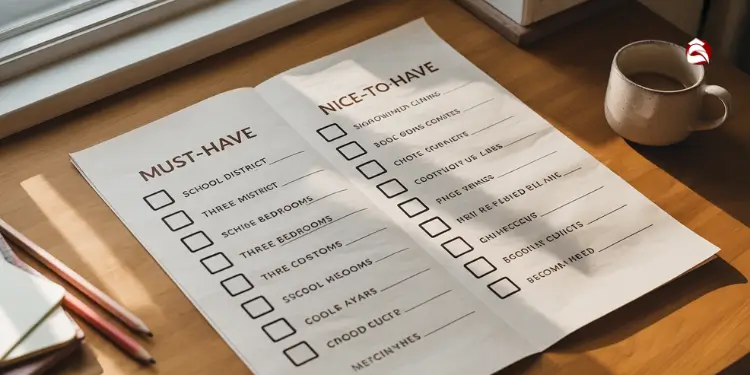

Your “Must-Have” list should have only the most important things. These are things you can’t change or would cost too much to fix later.

These include:

- Location and school district

- Minimum square footage for comfortable living

- Number of bedrooms required for your family

- Basic structural soundness

- Maximum commute distance

Your “Nice-to-Have” list has things you’d like but aren’t essential:

- Updated kitchens or bathrooms

- Specific flooring types

- Backyard size or features

- Garage capacity

- Aesthetic preferences like paint colors or fixtures

For example, Melissa and Jason had a $275,000 budget. They started with 14 must-haves that were too expensive. After talking about needs and wants, they narrowed it down to 5 essential features.

They found a home in their school district for $268,000. It needed some updates, but they could do those later without high payments. They saved $42,000 by choosing a home with older but working bathrooms.

Over three years, they updated the bathrooms for less than $15,000. They built equity instead of stretching their budget from the start.

| Feature | Need or Want? | Cost Impact | Modification Difficulty |

|---|---|---|---|

| School District | Need | High | Impossible (without moving) |

| Three Bedrooms | Need | Medium | Very Difficult |

| Updated Kitchen | Want | $15,000-$30,000 | Moderate |

| Hardwood Floors | Want | $5,000-$12,000 | Easy |

| Finished Basement | Want | $10,000-$25,000 | Moderate |

Remember, each must-have you add means fewer homes to choose from. It also raises your price. Most first-time buyers I work with start with 12-15 must-haves and end up with 4-5.

PERFORMANCE TRADE-OFF:

Zillow-backed research shows most upscale kitchen and bath remodels recoup less than 70 percent of their cost at resale—meaning early upgrades can strain budgets without delivering full value. Prioritize structural soundness now and tackle cosmetic projects later. Ref.: “Bird, B. (2025). This One Small Home Renovation Could Add More to Your Home’s Value than Any Other. Investopedia.” [!]

Being clear about what you need helps you use your budget wisely. Your lender will thank you. You’ll avoid being house-poor, where you have no money left for improvements.

Be honest with yourself. Honesty is your best friend when buying a home on a tight budget.

Expand search to emerging neighborhoods

Looking at new areas can help you buy more in today’s market. When people say they can’t afford homes, I suggest looking beyond their usual spots. Often, you can find homes 15-25% cheaper in areas that are getting better.

Money Management International says to spend at least a year looking at places. This lets you see how prices change in different areas. You’ll learn what’s a good deal in your market.

I’ve helped many first-time buyers find homes in areas that are just starting to get better. These places have the same good things as popular areas but cost less. The trick is finding places where prices haven’t caught up yet.

Begin by looking at neighborhoods next to popular ones. These “next-wave” areas have good things but cost less. One client bought a home for $275,000 in a new area. Three years later, similar homes were selling for $345,000 after new shops and parks were added.

Evaluate Safety, Commute, and Amenities Balance

When looking at new areas, do your homework instead of just guessing. Check crime stats on police websites. Many areas are safer than people think.

Try driving to work during rush hour to see how long it takes. Apps might show the best route, but real traffic is different. This helps you figure out how much you can afford in different places.

Go to areas you’re thinking about at different times and on weekends. This shows you things like noise and community life. It helps you decide if a place is right for you.

Look at what’s being built in your city’s plans. New stores and restaurants can make an area more valuable. This research helps you find places where your home might be worth more soon.

| Neighborhood Type | Average Price Difference | Safety Considerations | Commute Impact | Future Growth Indicators |

|---|---|---|---|---|

| Established Popular | Baseline (highest prices) | Well-documented safety profile | Often centrally located | Limited appreciation |

| Adjacent Emerging | 15-25% below established areas | Improving safety metrics | 5-10 minute increase | New retail and amenities planned |

| Early Revitalization | 25-40% below established areas | Requires thorough research | 10-20 minute increase | Infrastructure improvements funded |

| Future Development | 40%+ below established areas | Variable by specific location | 20+ minute increase | Master plans approved but not started |

What’s best for you depends on what you want. Some like a short commute, others more space. Your agent can find places that fit your needs and budget.

Keep track of your search with a simple spreadsheet. Compare prices, safety, commute, and amenities. This helps you find the best place for now and the future, keeping your credit score strong.

Look for tax credits for buying in areas that are getting better. Ask your lender about special programs for first-time buyers. These can make buying in new areas even more affordable.

“For More Information: Affordable first home ideas for budget buyers“

Leverage first time buyer assistance programs

Exploring first-time buyer assistance programs can save you thousands. In nine years, I’ve seen these programs turn dreams into reality. They can be the difference between renting and owning your home.

Many states, counties, and cities have programs for first-time buyers. These programs define a first-time buyer as someone who hasn’t owned a home in three years. Even if you’ve owned a home before, you might qualify if you’ve been renting for a while.

These programs can make a big difference. Last month, I helped a couple save $15,000 upfront and lower their monthly mortgage payment by $167. This helped them buy the home they really needed.

Down payment assistance was the game-changer for us. We were looking at another two years of saving, but these programs helped us buy now while interest rates were favorable. The homebuyer education course was actually incredibly helpful too.

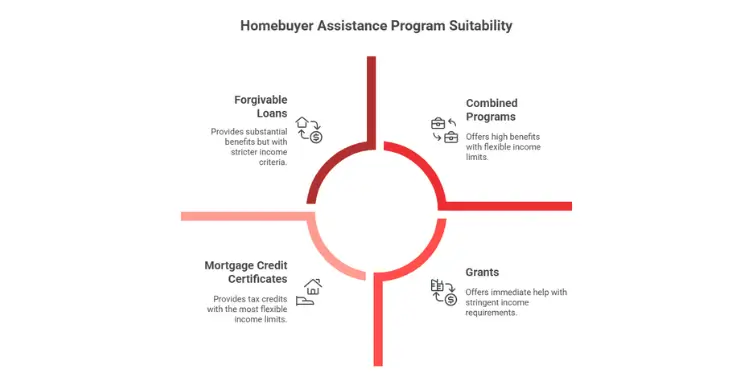

Compare Grants, Forgivable Loans, Tax Credits

Understanding the three main types of assistance can help you maximize your benefits. Each serves a different purpose and comes with unique advantages depending on your situation.

A Mortgage Credit Certificate (MCC) converts up to 30 % of annual mortgage interest—capped at $2,000 per year—into a dollar-for-dollar federal tax credit for the life of the original loan, directly lowering after-tax housing costs. Ref.: “Internal Revenue Service. (2024). About Form 8396, Mortgage Interest Credit. U.S. Department of the Treasury.” [!]

Grants provide the most straightforward benefit – they’re free money that never needs repayment. These funds typically range from $3,000 to $10,000 and can be applied toward your down payment or closing costs. The catch? They often have the strictest income limits and may require you to choose from approved lenders.

Forgivable loans offer a middle-ground approach. You’ll receive funds at closing, but the loan is gradually forgiven (typically 20% each year) if you remain in the home for a specified period, usually five years. If you sell or refinance before the forgiveness period ends, you’ll repay the remaining balance.

Tax credits, like the Mortgage Credit Certificate (MCC), work differently by reducing your tax liability. An MCC allows you to claim a tax credit for a portion of the mortgage interest you pay each year – typically 20-30% of interest payments, up to $2,000 annually. This credit continues for the life of your original mortgage, potentially saving tens of thousands over time.

| Assistance Type | Average Benefit | Repayment Required | Income Limits | Best For |

|---|---|---|---|---|

| Grants | $3,000-$10,000 | Never | Strictest (80-100% AMI) | Buyers needing immediate down payment help |

| Forgivable Loans | $5,000-$15,000 | Only if moving before 3-5 years | Moderate (100-120% AMI) | Buyers planning to stay 5+ years |

| Mortgage Credit Certificates | $1,000-$2,000 annually | N/A (tax credit) | Most flexible (up to 140% AMI) | Buyers focused on long-term affordability |

| Combined Programs | $10,000-$25,000+ | Varies by program | Depends on programs used | Strategic buyers working with knowledgeable agents |

The WSJ / Realtor.com Emerging Housing Markets Index finds that low-priced metros such as Toledo, OH list homes at up to 57.3 % below the national median—validating the 15-25 % savings target when buyers look just beyond “hot” districts. Ref.: “Hale, D. & Jones, H. (2024). Winter 2024 Wall Street Journal/Realtor.com Emerging Housing Markets Index. Realtor.com Research.” [!]

“Learn More About: How to reduce debt before buying house effectively“

Confirm Eligibility, Income and Occupancy Rules

Before getting your hopes up about specific programs, understand the qualification requirements. Most assistance programs evaluate three primary factors: your income level, your homebuyer status, and your intended occupancy.

Income limits typically range from 80% to 120% of Area Median Income (AMI), which varies by location. For example, in many mid-sized cities, a family earning $75,000 annually would qualify for multiple programs. These limits are often more generous than people expect – don’t assume you earn too much without checking.

Your homebuyer status matters significantly. While programs target first-time buyers, remember the three-year rule: if you haven’t owned a home in the past three years, you typically qualify as a “first-time” buyer regardless of previous ownership.

Occupancy requirements are straightforward but strict. You must intend to live in the property as your primary residence – these programs don’t support investment properties. Most require you to move in within 60 days of closing and maintain residency for at least one year.

Documentation requirements typically include:

- Income verification (tax returns, W-2s, pay stubs)

- Completion of a homebuyer education course (usually 4-8 hours)

- Signed affidavits confirming first-time buyer status

- Pre-approval from an approved lender (for many programs)

- Property inspection reports (some programs have property standards)

The homebuyer education requirement deserves special mention. While it might seem like a bureaucratic hurdle, these courses provide valuable information about the home buying process, maintaining your property, and avoiding foreclosure. Many of my clients report that these courses helped them feel more confident about their purchase decision.

When evaluating type of mortgage options, remember that some assistance programs work well with government-backed loans. FHA loans pair excellently with down payment assistance due to their low 3.5% down payment requirement. VA loans for eligible veterans can be combined with certain assistance programs, creating an even more powerful financial package.

Start your search at your state’s housing finance agency website, which typically maintains a database of available programs. Local housing authorities and nonprofit organizations like NeighborWorks America also offer resources. Don’t overlook employer-based programs – some large employers provide homebuyer assistance as an employee benefit.

The application process requires organization but isn’t overly complex. Begin gathering your documentation early, as some programs have limited funding and operate on a first-come, first-served basis. The extra effort pays off – these programs can dramatically reduce both your upfront costs and ongoing property taxes and insurance expenses.

“Related Articles: Ten smart ways to cut expenses to afford house faster“

Negotiate effectively with motivated sellers

Learning to negotiate with sellers can save you a lot of money. Many first-time buyers miss out on these savings. They are not listed online but can greatly reduce your monthly payment.

I’ve helped many buyers find these savings. It’s all about knowing where to look.

Finding sellers who are eager to sell is like finding hidden discounts. There are four main signs that a seller might be willing to negotiate:

- Extended market time – Properties that have been on the market for a long time often have sellers who are more open to negotiations.

- Multiple price reductions – When a seller lowers the price more than once, it shows they are willing to adjust to the market.

- Vacant properties – Homes that are empty cost the owner money every month. This can make them more willing to sell.

- Telling listing language – Certain phrases in the listing, like “motivated seller,” can hint at a seller who is open to negotiations.

Once you find a motivated seller, make an offer that works for both of you. This way, everyone gets what they want.

The best negotiations aren’t about winning or losing—they’re about finding creative solutions where both parties walk away satisfied with the outcome.

When you’re on a tight budget, here are some negotiation tips that can help:

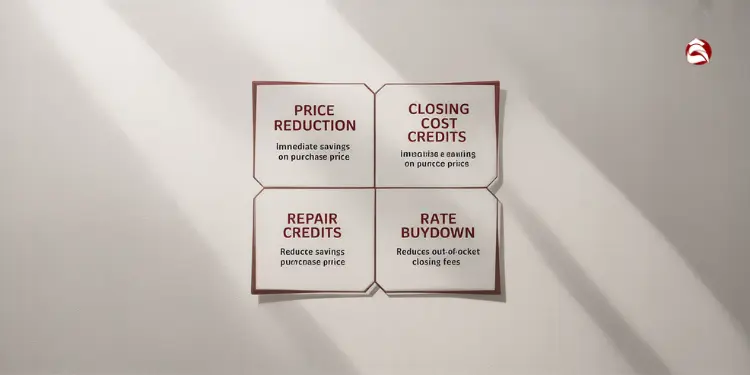

Ask the seller to help with closing costs instead of just lowering the price. This can save you money at closing. It’s good for buyers who are worried about balancing debt versus down payment.

Instead of asking for repairs to be done, ask for a credit for repairs. This way, you can choose who does the work and save money. You might find someone who can do the repairs for less.

Offer to close the deal at a different time if it helps the seller. This can make your offer more appealing without costing you more.

One of my clients saved $12,000 on a $230,000 home. They offered the full price but asked for help with closing costs and a credit for a new HVAC system. The seller agreed because they got the price they wanted, and my client saved money.

Knowing how different negotiation strategies affect your money is key to buying a home. The table below shows how different strategies can change your costs:

| Negotiation Strategy | Impact on Purchase Price | Impact on Cash Needed | Impact on Monthly Payment | Best For |

|---|---|---|---|---|

| Price Reduction | Lower | Moderate Decrease | Slightly Lower | Buyers concerned with PMI thresholds |

| Closing Cost Credits | Unchanged | Significant Decrease | Unchanged | Cash-strapped buyers |

| Repair Credits | Unchanged | Moderate Decrease | Unchanged | Homes needing immediate work |

| Rate Buydown | Unchanged | Slight Increase | Lower | Long-term owners seeking lower interest |

| Home Warranty Inclusion | Unchanged | Slight Decrease | Unchanged | First-timers worried about home maintenance |

Market conditions can affect how much you can negotiate. In a seller’s market, you might have less room to negotiate. But in a buyer’s market, you have more power.

Lender rules cap total seller concessions—often between 3 % and 6 % of the purchase price—and anything above that can jeopardize loan approval. Verify limits early to avoid renegotiating at underwriting. Ref.: “National Association of REALTORS®. (2024). Consumer Guide: Seller Concessions. National Association of REALTORS®.” [!]

It’s important to know what concessions are most important to you. If you want to buy a bigger home, focus on lowering your monthly costs. If you’re on a tight budget, try to reduce upfront costs even if it means a slightly higher monthly payment.

By finding motivated sellers and negotiating smartly, you can buy a home that might seem out of reach.

“Explore More: How to make home buying budget step by step“

Optimize mortgage terms to lower payment

Finding an affordable home is just the start. You can also lower your monthly costs by optimizing your mortgage terms. I’ve seen clients save $200-300 monthly on the same purchase price by choosing the right mortgage. This can save thousands over the life of your loan, adding to your savings account.

The mortgage you choose affects your monthly payment and how quickly you build equity. Even small changes in interest rates or loan structure can make a big difference. This is true, even if you plan to stay in the home for a long time.

“You Might Also Like: How to avoid overspending on house purchase budget“

Choose Loan Products with Minimal Downpayment

For budget-conscious buyers, there are loan programs with low down payments. Each has its own benefits, depending on your situation:

- FHA Loans: Need only 3.5% down and have flexible credit requirements (minimum 580 score). These loans are good if you have little savings or past credit issues. But, you’ll pay mortgage insurance forever, which raises your monthly costs.

- Conventional 97 Loans: Require only 3% down and let you remove PMI when you reach 20% equity. This option is best if you think your income will grow or home prices will rise in your area.

- USDA Rural Development Loans: Offer 100% financing (zero down payment) for properties in eligible areas. Many suburban areas qualify. Income limits apply, but they’re often higher than expected.

- VA Loans: Provide 100% financing for veterans and active-duty service members with no mortgage insurance. If you’ve served, this program usually offers the best deal.

Choosing the right loan is just the start. Here are more ways to lower your payments:

| Strategy | How It Works | Best For | Potential Savings |

|---|---|---|---|

| Rate Buydowns | Pay points upfront to lower your interest rate forever | Buyers planning to stay in the home 5+ years | $50-100 monthly per point paid |

| Temporary Buydowns | Lower rate for first 1-3 years (like 2-1 buydowns) | Buyers expecting income growth | $150-250 monthly in early years |

| Lender-Paid MI | Slightly higher rate but no separate PMI payment | Buyers with limited monthly cash flow | $30-80 monthly in net savings |

| Adjustable-Rate Mortgages | Lower interest rate for initial period (3-10 years) | Buyers planning to move within 5-7 years | $100-200 monthly during fixed period |

Most first-time buyers choose a 30-year fixed-rate mortgage. This spreads payments over three decades with a consistent rate. But, a 15-year loan has a lower interest rate and builds equity faster, though monthly payments are higher.

“I helped a young couple use a 2-1 buydown that reduced their effective rate by 2% the first year and 1% the second year. This saved them $175 monthly during their transition from renting to owning—exactly when they needed breathing room in their budget.”

Some states offer mortgage credit certificates (MCCs). This is a one-time tax credit program. It converts part of your mortgage interest into a direct tax credit. This can save you up to $2,000 annually on your taxes, making your monthly housing costs more affordable.

When comparing loan options, look beyond the monthly payment and closing costs. Calculate the total expense over your expected ownership period. I’ve had clients choose a slightly higher monthly payment to save thousands in fees or future interest costs. This was a smart choice for their situation.

“Read More:

Strengthen credit profile before application

When you’re on a tight budget, your credit score is key. A good score can save you a lot of money on your mortgage. For example, a score of 740+ can cut your monthly payments by $100-150 on a $250,000 loan. That’s over $36,000 saved over 30 years.

Get your free credit reports from annualcreditreport.com at least 4 months before you start looking for a house. I’ve seen scores go up by 40+ points by fixing wrong late payments or collection accounts. Keeping your credit card balances low, below 30% of the limit, can also boost your score by 20-30 points in 60 days.

Don’t apply for new credit cards or auto loans while you’re house hunting. Each application can lower your score by 5-10 points. Also, don’t close old accounts. The length of your credit history counts for 15% of your score.

If you need to cover closing costs without spending too much, a better credit score can help. One client went from 664 to 703 in just two months. This score change let them get conventional financing instead of FHA, saving $180 a month.

Looking at manufactured homes or new neighborhoods might help stretch your budget. But, improving your credit score offers the best long-term savings. Work with a licensed real estate agent who knows about credit and lenders for the best advice.

{kind=link}