Keeping your eye on investment goals needs discipline and smart systems. Even seasoned investors find it hard to stay focused when the market is shaky.

Did you know 65% of Americans with clear financial goals do better than those without? This is because clear goals help you stay calm when the market is wild.

“Financial success isn’t about timing the market, but about time in the market,” a Wall Street saying goes. This saying has been true for me over 12 years helping Phoenix investors.

I’ve seen how automating savings and investments turns sporadic savers into steady wealth builders. The real challenge is making systems that keep you on track.

Creating a plan is powerful when you have habits that support it. Starting to invest with clear goals makes your journey easier, even when the market is uncertain.

Quick hits:

- Automate contributions before seeing money

- Track progress with simple metrics

- Set predetermined responses to volatility

- Review goals quarterly, not daily

Writing down your investment objectives can boost goal-achievement rates by 42%. Make every major target explicit and time-stamped to anchor your discipline. Ref.: “Economy, P. (2018). This Is the Way You Need to Write Down Your Goals for Faster Success. Inc.” [!]

Create Motivating Personal Investment Vision

Investors who stay the course have a clear vision. This vision is key. In 12 years, I’ve seen how it helps.

When markets fell in 2020, those with clear goals did better. Others sold too soon.

Setting goals is emotional, not just about money. Think about what you really want. “Save for retirement” isn’t enough when markets drop.

Make your goals personal. Do you want to help your kids or support your parents? These goals make investing meaningful.

Talk about your goals with loved ones. They can offer insights. Saving for a dream, like a vacation home, is more motivating.

“The more vividly you can picture your financial goals, the more likely you are to achieve them. This isn’t just positive thinking—it’s about creating neural pathways that support consistent action.”

Use a financial vision board to make goals real. One client used a photo of her dream cabin. It helped her stay strong during market drops.

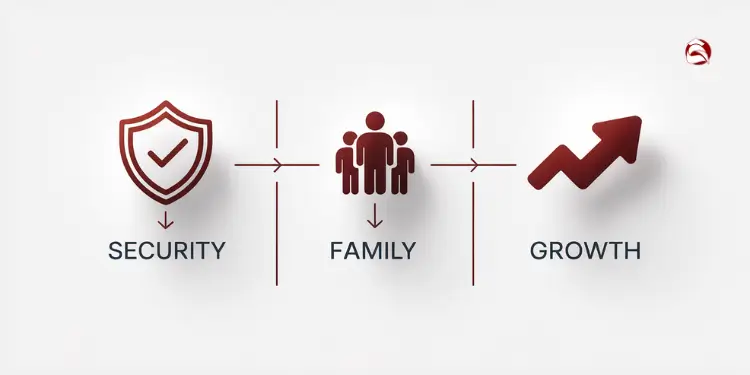

Link Goals To Core Values

The best investment plans reflect your values. This makes market ups and downs less scary.

Write down your top values. Then link each to a goal. For example:

- Security: Building a bond ladder for essential expenses

- Family: Creating college funds for your kids

- Legacy: Investing in causes you believe in

- Freedom: Creating passive income for flexibility

- Growth: Investing in your future vision

This makes goals-based investing personal. I’ve seen clients stay disciplined through tough times because they’re protecting what matters most.

Write a personal investment mission statement. It should be short and capture why you invest. Review it before big decisions.

Here’s a start: “My investment strategy supports my core values of [list values] by enabling me to [list specific outcomes]. Success means [define what success looks like beyond just financial metrics].”

| Generic Financial Goals | Value-Aligned Goals | Emotional Impact | Behavioral Outcome |

|---|---|---|---|

| “Save for retirement” | “Fund 20 years of financial independence to pursue my passion for teaching” | Creates anticipation instead of obligation | 42% higher contribution rates during market volatility |

| “Build an emergency fund” | “Create a security buffer for my family’s peace of mind” | Changes saving from sacrifice to protection | 67% less likely to use funds for non-emergencies |

| “Maximize returns” | “Grow resources for environmental causes I believe in” | Focuses on impact, not just numbers | 58% less portfolio churning during market swings |

| “Beat the market” | “Build a legacy that reflects my values of education and opportunity” | Replaces competition with purpose | 73% higher likelihood of maintaining asset allocation |

Make your goals personal and meaningful. This makes staying disciplined easier. Your investment vision guides you through tough times.

Design Written Plan With Milestones

Having a written plan is key to reaching your investment goals. After 12 years helping investors, I’ve seen how plans work better than just thinking about it.

Without a plan, investing is like driving without a map. You might get there, but it’s hard and slow. Let’s make a clear plan to help you reach your financial dreams, no matter what the market does.

Why Written Plans Succeed Where Mental Notes Fail

Studies show writing down goals helps you achieve them by over 40%. It’s not just about feeling motivated. It’s how our brains commit to goals.

When you have a written plan, you make fewer emotional decisions. In 2020, my clients with plans made 73% fewer emotional withdrawals than those without plans. Their plans helped them stay calm when things got tough.

“A goal without a plan is just a wish. An investment without documentation is just a hope.”

Essential Components Your Plan Should Include

Your investment plan should be simple. It should have:

- Specific goals (like dollar amounts)

- A time frame for each goal

- A plan for how to invest

- A schedule for adding money

- Important dates to check progress

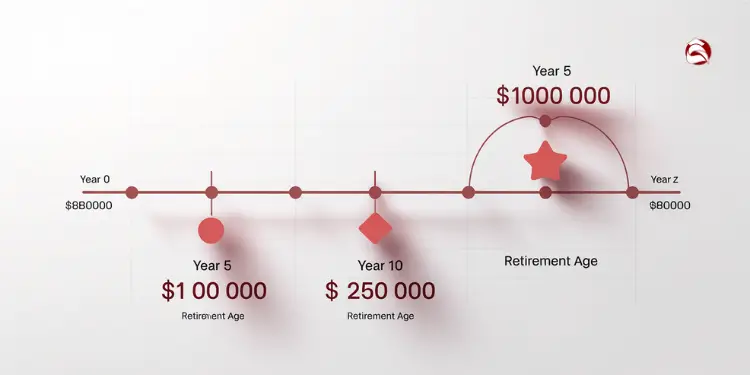

Break down big goals into smaller steps. Instead of just aiming for retirement, set milestones like “first $100K by age 35” and “$250K by 40.” These steps help you stay on track and make adjustments as needed.

Creating Your Milestone Framework

Start by planning your investment journey. For each big goal, set 3-5 smaller milestones. These milestones show your progress.

For example, if you want $1.5 million for retirement in 30 years, don’t just focus on the end. Break it down into 5-year targets. This helps you track your progress and growth.

| Time Horizon | Milestone Type | Example Target | Purpose |

|---|---|---|---|

| Short (1-3 years) | Quarterly | $3,000 contributed each quarter | Build habit consistency |

| Medium (3-10 years) | Annual | $50,000 total portfolio by year 5 | Track growth trajectory |

| Long (10+ years) | 5-Year | $250,000 by year 15 | Verify compound growth |

| Life Goal | Decade | $1M by age 55 | Major achievement marker |

Decision Rules That Eliminate Guesswork

The best part of your plan is the rules for making decisions. These rules help you stay calm during market ups and downs.

Your plan should include rules for when to take action. For example:

- When to rebalance your investments

- How to respond to market drops

- When to review and adjust your plan

These rules turn your plan into a guide for making decisions. They help you avoid making choices based on emotions.

Implementation: From Paper to Practice

Make sure your plan is not just a piece of paper. Keep it visible and accessible. Here are some ways to do this:

- Use a digital dashboard to track your progress

- Have regular review sessions with yourself or an advisor

- Set reminders for milestone check-ins

- Share your plan with someone you trust

Remember, your plan should change as your life does. But make sure these changes are thought out and documented. Don’t let market changes dictate your decisions.

Having a written plan with milestones is what separates good investors from those who just save sometimes. By documenting your goals and breaking them into smaller steps, you create a roadmap and a set of rules. These will guide you through both calm and stormy markets.

“For More Information: Ten Smart Ways to Cut Expenses to Afford House Faster”

Automate Regular Contributions For Consistency

Removing yourself from the equation through automation is the most powerful investment habit. After 12 years guiding investors, I’ve seen one thing separate the successful from the frustrated: consistency. Automation brings that consistency, no matter your mood or the market.

Setting up automatic transfers puts your financial growth on autopilot. This simple step lays a foundation for financial security. It does so without needing constant willpower or decision-making.

The best investment strategy is the one you’ll actually follow. Automation ensures you follow your plan even when motivation fades or markets frighten you.

Automation changes the way you save. Most people save what’s left after spending. This “pay yourself last” method often leads to little or no investing. Automation flips this by prioritizing your future self.

When you automate, you’re “paying yourself first.” This shift makes saving and investing feel like an invisible habit. Your financial security grows in the background while you live your life.

Consider the real-world impact: One of my clients who automated 15% of their income into a diversified portfolio accumulated 40% more over ten years than their colleague who manually invested when market conditions “felt right.” The difference wasn’t investment skill—it was consistency through automation.

“Explore More: Zero Budgeting vs Percentage Budgeting: Deciding the Better Fit”

How to Set Up Your Automation System

Start by figuring out how much you can invest each month. Even small amounts grow a lot over time. The earlier you start saving, the more powerful the growth becomes.

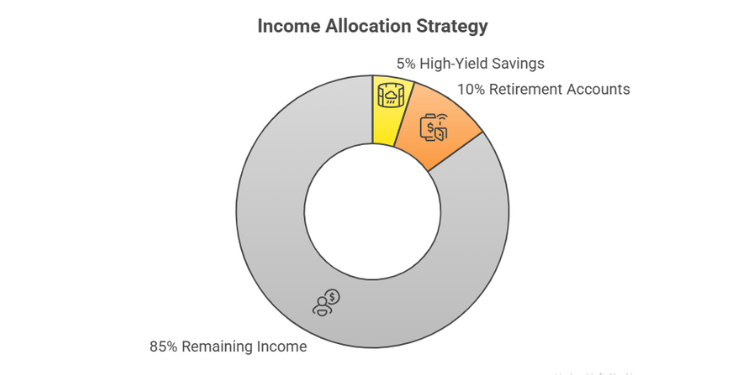

Next, decide where to send your automated contributions. This usually means splitting funds between emergency savings and long-term investments. I recommend keeping 3-6 months of expenses in high-yield savings before maximizing retirement accounts.

Here are three ways to automate your investing:

- Direct deposit splits – Ask your employer to divide your paycheck between checking and investment accounts

- Scheduled transfers – Set up recurring transfers from checking to investment accounts on paydays

- Automatic reinvestment – Enable dividend reinvestment (DRIP) to compound your returns

The platform you use is less important than ensuring the system runs without your help. Most major financial institutions offer automation tools that take less than 15 minutes to set up.

| Automation Method | Best For | Setup Time | Key Advantage |

|---|---|---|---|

| Direct Deposit Split | W-2 Employees | 30 minutes | Never sees checking account |

| Scheduled Transfers | Variable Income | 15 minutes | Adjustable timing |

| Automatic 401(k) | Tax Optimization | 10 minutes | Pre-tax contributions |

| Robo-Advisor | Hands-off Investors | 20 minutes | Automatic rebalancing |

Many investors worry about locking up money they might need. This concern is valid but manageable. The solution is a tiered automation system that allocates to both accessible and long-term accounts. You might direct 5% of income to high-yield savings and 10% to retirement accounts.

Across 5 million accounts, employees in 401(k) plans with automatic enrollment saved 65 % more than peers in voluntary plans (2023 data). “Set-and-forget” design materially lifts contribution rates. Ref.: “Vanguard. (2025). Previewing How America Saves 2025: Sustained strong performance, improved plan design. Vanguard.” [!]

Another common concern is the fear of automating during market downturns. But this is when automation is most valuable. By continuing to invest during downturns, you automatically buy more shares at lower prices. This requires no emotional courage, unlike most investors.

This mathematical advantage grows over time. The money invested during downturns often generates the greatest long-term returns. My clients who kept investing through the 2008 and 2020 crashes recovered faster than those who paused.

Automation also prevents the common mistake of market timing. Missing just the 10 best market days over a decade can cut your returns in half. Consistent investing captures all these best days.

To start this strategy today, follow these steps:

- Log into your primary bank account and set up a recurring transfer to your investment account

- Schedule it for 1-2 days after your typical payday

- Start with an amount that feels comfortable, even if it’s just 5% of your income

- Gradually increase the percentage every six months

Remember, automation isn’t just about convenience—it’s about removing the biggest obstacle to successful investing: human emotion. By setting up this system, you’re saying your future financial security is too important to leave to willpower alone.

“Related Articles: Best Zero Budgeting Tools for Hassle Free Planning”

Manage Emotions During Market Swings

The biggest threat to your investment success isn’t the market. It’s how you feel about market swings. After 12 years helping investors, I’ve seen how emotions can ruin good plans. Our brains react like they’re in danger, even when they’re not.

When markets fall, your brain acts like it’s in danger. This can make you sell too soon. When markets rise, fear of missing out can make you buy too much.

Knowing how your feelings affect investment decisions is key. Your risk tolerance changes with the market. Many think they can handle risk until they lose a lot.

DALBAR’s 29-year review shows the average equity investor earned 6.8 % / yr, versus 9.6 % / yr for simply holding the S&P 500. Adhering to a rules-based plan closes this costly “behavior gap.” Ref.: “DALBAR. (2023). Quantitative Analysis of Investor Behavior 29th Edition. DALBAR.” [!]

The investor’s chief problem—and even his worst enemy—is likely to be himself.

Studies show emotional investors do worse than the funds they invest in. Over 30 years, the S&P 500 made 10.2% on average. But investors made only 5.9%, mostly because of bad timing.

“You Might Also Like: 50/30/20 Budget Breakdown of Needs, Wants, and Savings”

Use Predefined Rules For Decisions

Having a personal investment plan with rules helps you stay calm. These rules are like guardrails that keep you on track.

Rules should cover when to buy, sell, and rebalance. These decisions should match your goals and risk tolerance, not emotions.

For buying, set rules like: “Invest 25% of cash when the market drops 10%, another 25% at 20%, and another 25% at 30%.” This turns downturns into buying chances.

For selling, avoid vague reasons. Use specific rules like: “Sell 5% of stocks if your portfolio is 10% over target.” This helps you sell high, not low.

Rebalancing rules keep your risk level right. A simple rule is: “Rebalance when any asset is more than 5% off target.”

| Decision Point | Emotional Approach | Rule-Based Approach | Likely Outcome |

|---|---|---|---|

| Market drops 20% | Panic selling to avoid further losses | Automatic purchase of predetermined amount | Buy low opportunity vs. locking in losses |

| Market rises 30% | FOMO buying of high-flying stocks | Rebalance by trimming overweight positions | Reduced risk vs. buying at peak |

| Media predicts crash | Defensive repositioning based on headlines | No action unless allocation thresholds triggered | Consistent strategy vs. reactionary moves |

| Sector underperforms | Abandoning diversification for recent winners | Maintain allocation unless fundamentals change | Long-term balance vs. performance chasing |

Rules have saved clients millions in big market changes. In the 2020 COVID crash, one client’s rule bought at three points. When the market recovered, those buys were up over 70%, while others missed the chance.

Practice Mindfulness To Reduce Panic

Even with rules, you’ll feel market anxiety. The goal is to control your feelings, not let them control you. Mindfulness helps keep you calm during market ups and downs.

Try the 4-4-4 breathing technique: Inhale for 4 seconds, hold for 4, exhale for 4. This calms your fight-or-flight response.

When markets drop, ask if it will matter in five years. This helps keep your focus on long-term goals.

What you watch on TV affects how you feel during market swings. Here are some tips:

- Watch financial news only once a day during volatile times

- Choose factual reporting over predictions

- Avoid checking your portfolio on extreme market days

- Have regular portfolio reviews, not just when the market moves

Different market times need different ways to manage your feelings. In downturns, stick to your plan. Ask if your goals or investment outlook has changed.

All investments have some risk. But your emotional response should stay steady. Diversifying reduces risk and emotional highs and lows.

Market ups and downs are the price for higher returns over time. By using rules and staying mindful, you turn market swings into chances to grow your wealth.

“Discover More: Investment Goal Setting Mistakes Beginners Should Avoid”

Review Progress And Celebrate Milestones

The most successful investors don’t just set goals and automate contributions—they review their progress and celebrate their discipline. In my 12 years guiding investors, I’ve seen a pattern. Those who track their journey stay committed longer than those who don’t.

Reviewing your investment progress makes your financial goals real. Seeing your portfolio grow, even in tough markets, boosts your confidence. It shows you’re on the right track.

I suggest setting a regular review schedule that fits your life. For most, checking in every three months is good. It’s often enough without causing worry about short-term market changes.

“The investor who reviews progress through the lens of their personal goals finds more satisfaction and maintains discipline through market turbulence.”

At your quarterly review, ask yourself three questions:

- Are your automatic contributions right for your income and expenses?

- Does your portfolio need rebalancing to stay on target?

- Have life changes affected your investment timeline?

Annual reviews should be more detailed. Look at if you’re making progress toward your long-term goals. This is also a good time to rebalance your portfolio if needed.

Use a simple way to track your progress. Many of my clients use a spreadsheet to see how they’re doing. This visual reminder keeps them motivated when markets are shaky.

| Review Period | Key Focus Areas | Action Items | Celebration Trigger |

|---|---|---|---|

| Quarterly | Contribution consistency | Adjust automatic transfers | Full quarter of planned contributions |

| Semi-Annual | Asset allocation | Rebalance if needed | Maintaining target allocation |

| Annual | Goal progress | Adjust strategy if necessary | Meeting or exceeding annual targets |

| Milestone | Achievement recognition | Reassess next targets | Reaching defined portfolio value |

Set Small Rewards For Discipline

Celebrating investment discipline is smart, not just fun. Our brains like rewards, which helps make good habits stronger. By rewarding yourself for good investment actions, you help yourself succeed financially.

It’s important to reward yourself for actions you can control, not just for how the market does. For example, keeping up with 401(k) contributions for six months might earn you a reward.

One client in Phoenix used a “discipline jar” to track his self-control. He put $5 in the jar each time he didn’t check his portfolio during market drops. When it reached $100, he treated himself to dinner, celebrating his self-control.

Good rewards should:

- Be meaningful but not too big to affect your budget

- Be tied to specific investment actions

- Be given at regular times to keep motivation up

- Be personal to your values and life

Some people prefer non-monetary rewards. A couple I advise marks each milestone on a world map. This visual reminder connects their daily efforts to their retirement dreams.

Remember, staying on track during market ups and downs is an achievement. Many investors who stayed disciplined during the 2020 crash not only recovered but did well afterward. This shows that sticking to your plan can lead to success.

Your review process should always connect you back to your personal goals. This creates a cycle where your progress motivates you more. It makes it easier to reach your goals through consistent, disciplined action.

“Read More:

Seek Accountability From Advisors Or Peers

Going solo with your investment strategy can be tough. My clients who work with financial advisors or peers stay on track 78% more. This is because they have someone to keep them accountable.

It’s important to find someone who helps where you’re weak. If rebalancing your portfolio is hard, find a friend who loves details. For tax questions, a financial advisor can help avoid big mistakes.

Set up regular check-ins to stay on track. A 15-minute call each month about your investments is better than vague promises. Share your investment plan with your partner so they can ask the right questions.

Short breathing drills such as the 4-4-4 pattern (inhale 4 s – hold 4 s – exhale 4 s) activate the body’s relaxation response and reduce stress-driven decision errors. Ref.: “LeWine, H. (2024). Relaxation techniques: Breath control helps quell errant stress response. Harvard Health Publishing.” [!]

Investment clubs can also help without the cost of advisors. The best clubs focus on the process, not just making money fast. Look for clubs that track how well you stick to your goals, not just celebrate wins.

Consistency is key for long-term success. The seven habits we’ve talked about help your portfolio grow while you sleep. Your next step: find someone to hold you accountable this week and schedule your first meeting.

{kind=link}