Buying a home on one income is possible with the right plan. Many families live on just one income. This shows it can work.

“The difference between wishful thinking and homeownership is having a realistic plan tailored to your individual situation,” I tell my clients regularly. During my nine years as a REALTOR®, I’ve guided dozens of solo buyers through purchasing property on one income successfully.

It’s important to know all the costs of buying a house. Many first-timers forget about the hidden costs beyond the down payment. These costs can stop even the most determined buyer.

What makes some succeed while others struggle? It’s all about preparation. My clients who buy on one salary usually spend 3-4 months getting ready before making offers.

Quick Hits:

- Calculate your true purchase ceiling

- Build emergency reserves before shopping

- Explore specialized assistance programs

- Consider alternative property types

- Maintain employment stability throughout process

Calculating realistic price range alone

Buying a home alone starts with knowing your price range. It’s key when you have only one income. You must know what you can afford well.

Many first-time buyers start with the highest pre-approval amount. But, your pre-approval amount is not your target price. I’ve helped many single-income clients understand this.

First, figure out your monthly budget for a home. Home costs include more than just mortgage payments. You also need to think about property taxes, insurance, maintenance, and utilities.

It’s wise to keep your housing costs under 30% of your monthly income. This leaves room in your budget. It helps you avoid being “house poor,” where you spend too much on a home.

Large-scale lender studies show approval odds rise sharply when the front-end (housing) ratio stays below 28 %—and below 31 % for FHA loans—keeping borrowers safely out of “house-poor” territory.Ref.: “Kenton, W. (2021). Front End Ratio: What It Is and How to Calculate It. Investopedia.” [!]

Income Multipliers Lenders Typically Accept

Lenders use special formulas to see how much you can borrow. They look at your debt-to-income ratio (DTI). This compares your monthly debts to your income.

Lenders usually say your DTI can’t be over 43%. But, for better chances and rates, aim for 36-38%. This is my advice.

FHA underwriting flags applications when the mortgage payment exceeds 31 % of gross income or total monthly debts top 43 %; ratios above these marks demand documented compensating factors and can slow—or sink—approval.Ref.: “U.S. Department of Housing and Urban Development. (2011). HUD 4155.1 Chapter 4, Section F: Borrower Qualifying Ratios. HUD.” [!]

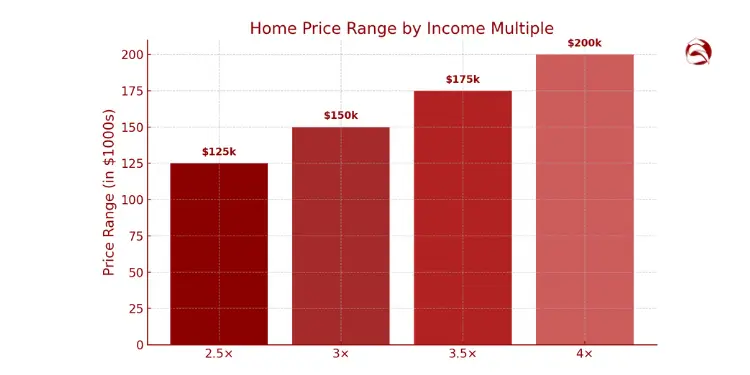

Financial advisors suggest using a specific factor to find a price range. The house price to income ratio helps figure out what you can afford.

For single-income buyers, use a more careful multiplier. You have only one income, so you need a safety net.

| Income Multiplier | Risk Level | $50,000 Income | $75,000 Income | $100,000 Income |

|---|---|---|---|---|

| 2.5x | Very Conservative | $125,000 | $187,500 | $250,000 |

| 3x | Conservative | $150,000 | $225,000 | $300,000 |

| 3.5x | Moderate | $175,000 | $262,500 | $350,000 |

| 4x | Aggressive | $200,000 | $300,000 | $400,000 |

| 4.5x+ | Very Aggressive | $225,000+ | $337,500+ | $450,000+ |

Loan types vary in how much of your income they allow for housing. Conventional loans say your housing costs should be under 28% of your income. FHA loans are a bit more flexible at 31%.

Staying 5% below these limits can help you get better deals from lenders. This can lead to lower interest rates and better loan terms.

For example, with an annual income of $60,000 (or $5,000 monthly), a safe choice is a home worth $180,000-$210,000. This keeps your housing costs in line with your income and accounts for other costs.

Remember, the median household income is for two incomes. As a single-income buyer, you have less income. So, you need to be careful with your purchase.

By knowing these income multipliers and sticking to your budget, you ensure financial security. Don’t stretch to the maximum lenders will approve.

Boosting down payment through savings

Building a down payment fund with one income is tough. You need to save and find ways to get more money. This first step is key to buying a home and keeping your finances strong.

Many of my clients have found ways to save more, even with a small income. They’ve learned to overcome the down payment challenge.

“Read More: Essential single income home buying budget strategies“

Automating Savings Toward Deposit Goal

Successful single-income buyers don’t rely on willpower. They ask their employer to send 10-15% of their paycheck to a savings account. This way, saving becomes automatic.

Today, you can earn 3.5-4.5% interest on your savings. This is much better than regular savings. Saving for 1-2 years can make a big difference.

Automating a fixed slice of each paycheck into a high-yield savings account earning about 4.40 % APY can trim months off a 24-month down-payment schedule without increasing risk.Ref.: “McRae Ngo, S. (2025). High-yield savings rates today: June 2, 2025 | Highest APY remains 4.40% as the Fed prepares its next move. Bankrate.” [!]

Set a goal and break it down into smaller steps. For example, to buy a $200,000 home, you need $7,000 down and $5,000 for closing costs. This makes saving easier.

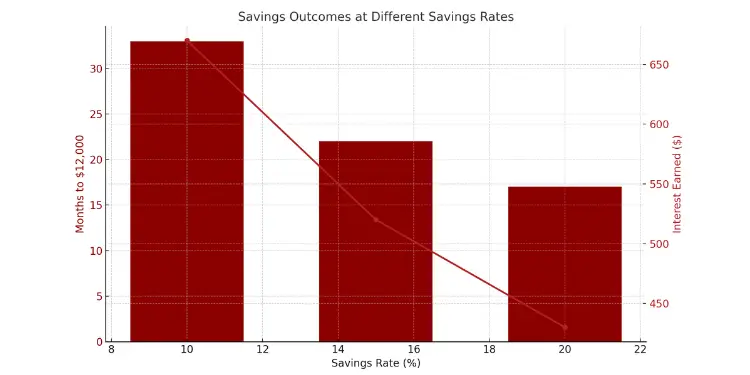

Here’s how saving works for someone making $55,000 a year:

| Monthly Income | Savings Rate | Monthly Contribution | Months to $12,000 | Interest Earned |

|---|---|---|---|---|

| $3,400 | 10% | $340 | 33 | $670 |

| $3,400 | 15% | $510 | 22 | $520 |

| $3,400 | 20% | $680 | 17 | $430 |

Use an app or spreadsheet to track your savings. Seeing your progress helps keep you motivated. Clients who track their savings reach their goals 40% faster.

Remember, the size of your down payment affects your mortgage. The choice between a big or small down impacts your monthly payments, interest rate, and future home value.

“Related Articles: How to avoid overspending on house purchase budget“

Side Hustle Options for Capital

Side hustles can help you save faster. The key is to use this extra money only for your down payment.

One client, Melissa, made extra money by teaching online cooking classes. This added $400 to her savings each month. It cut her savings time by nearly eight months.

The best side hustles for single-income buyers are flexible, cheap to start, and have clear earnings. Think about what you’re good at:

- Sharing economy participation – Weekend driving, food delivery, or home rentals offer immediate income with flexible hours

- Digital freelancing – Writing, design, programming, or virtual assistance can generate $25-75 hourly with minimal equipment

- Skill monetization – Teaching, tutoring, or consulting in your professional field typically commands premium rates

- Hobby conversion – Selling crafts, photography, or other hobbies can be a steady source of income

Open a separate savings account for your side hustle money. This keeps it separate from your regular money. It helps you stay focused on your goal.

Family gifts can also help with your down payment. If you get money from relatives, make sure they give you a “gift letter.” This letter says you don’t have to pay them back. Lenders need this to know the money isn’t a loan.

Think about taxes when you save from side hustles. You’ll have to pay taxes on this income. Set aside 25-30% of your earnings for taxes. This way, you won’t be surprised when you file your taxes.

By saving automatically and using side hustles, you can save faster. My clients who do this reach their down payment goals 30-50% faster than those who just save.

“Explore More: How to reduce debt before buying house effectively“

Leveraging assistance programs for solos

As a single income homebuyer, you get special help to buy a home. I’ve helped many first-time buyers in Greenville. Solo buyers often get help that dual-income families can’t.

Buying on one income has its perks. You might qualify for financial help that others don’t. Most programs help those earning 80-120% of the area median income.

I’ve helped many single home buyers. Teachers, nurses, and retail workers thought buying a home was far away. But with the right help, they moved their plans up by 2-3 years.

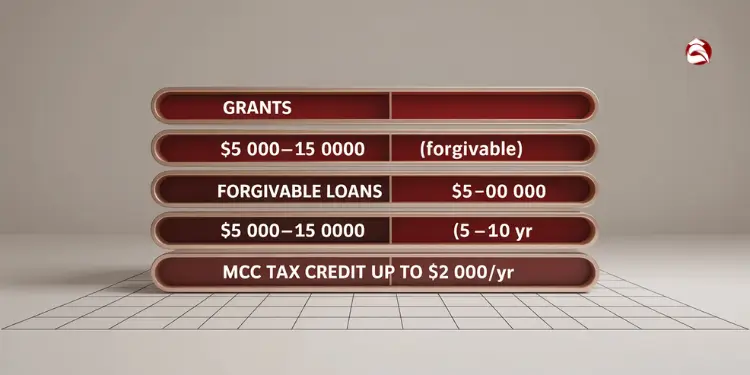

Grants and Forgivable Loan Examples

Start with your state’s Housing Finance Agency. They have programs for moderate-income buyers. Single income households get special benefits.

These programs offer down payment help, from $5,000 to $15,000. Many are forgivable loans. This means you get free money if you stay in the home for 5-10 years.

State housing agencies regularly deploy five-figure assistance; North Carolina’s 1st Home Advantage program, for instance, offers up to $15,000 in down-payment aid that is fully forgiven after 15 years of owner occupancy.Ref.: “North Carolina Housing Finance Agency. (2025). NC 1st Home Advantage Down Payment. NCHFA.” [!]

I never thought I could afford a home as a single mom until my realtor connected me with our state’s Housing Finance Agency. Their forgivable loan covered my entire down payment, and my mortgage payment is now $230 less than my old rent.

Single moms and solo buyers get extra help through the Family Self-Sufficiency Program. It uses escrow accounts that grow with your income. This helps you financially while you build equity.

National programs like Fannie Mae’s HomeReady and Freddie Mac’s Home Possible are great for single income buyers. They need only 3% down and offer lower mortgage insurance costs. This saves you hundreds each month.

The HomeReady® mortgage permits as little as 3 % down and accepts gifts, grants, or sweat-equity contributions—dramatically lowering cash barriers for single-income purchasers.Ref.: “Fannie Mae. (2025). HomeReady Low Down Payment Mortgage. Fannie Mae.” [!]

Don’t forget about local programs. City and county programs often offer the best deals. I’ve seen grants of $10,000+ for buyers in revitalization areas. These programs have higher income limits than you might think.

One of my clients used a state program and a county grant to cover their down payment and closing costs. They only had to pay for the home inspection.

| Program Type | Typical Benefit | Income Limit | Repayment Terms | Best For |

|---|---|---|---|---|

| State HFA Loans | $5,000-$15,000 | 80-120% AMI | Forgiven after 5-10 years | First-time buyers with steady income |

| HomeReady/Home Possible | 3% down payment | 80% AMI | Standard mortgage | Buyers with limited savings |

| City/County Grants | $7,500-$20,000 | 100-140% AMI | No repayment | Buyers in targeted neighborhoods |

| Family Home Guarantee | 2% down payment | Varies by location | Standard mortgage | Single parents with dependents |

The application process takes 30-45 days. Start two months before you start looking for houses. You’ll need to finish a HUD-approved homebuyer education course (4-8 hours online).

These programs help communities grow. They make neighborhoods stable by helping residents own homes.

You’ll need to provide a lot of documents. This includes proof of income, tax returns, bank statements, and letters about your job or credit.

Keep all your documents in one place. Set reminders for when things are due. Missing deadlines can cost you.

Think about how much you can spend on housing. These programs can help you spend a bit more.

The Family Home Guarantee program helps single parents. It lets them buy a home with a single income and little down payment. This can save you over $100 a month.

Apply early in the year for these programs. They often run out of money by mid-year.

“For More Information: Cost breakdown buying house for first time buyers“

Minimizing debt to strengthen profile

For single income buyers, cutting down debt can really help your mortgage application. Lenders look closely at your debt-to-income ratio when you’re alone. I’ve helped many first-time buyers see how paying off debt can make a big difference.

Your debt-to-income ratio is very important when you’re applying alone. Lenders like to see it under 43%. But for single earners, aiming for 36% or less is even better. Remember, lenders use minimum payments on your credit report, not what you actually pay.

I suggest a 90-day debt reduction plan before getting pre-approved. This gives you time to see improvements in your credit score and debt ratios. Start by listing all your debts, their interest rates, and minimum payments.

First, work on revolving debts like credit cards. Paying down credit card balances can raise your score by 20-40 points in 60 days. This can help you get better interest rates, saving you thousands over time.

Here are some ways to tackle multiple debts:

- Avalanche Method – Pay off debts with the highest interest first

- Snowball Method – Start with the smallest balances for quick wins

- Balance Transfers – Move high-interest debts to a 0% card (but don’t make new purchases)

- Debt Consolidation Loan – Replace many payments with one lower-interest payment

Don’t close paid-off credit accounts. This can lower your credit score. Instead, keep them open but not active.

For student loans, look into income-driven plans to lower your payments. Auto loans also affect your debt ratio. Consider paying off or reducing these before looking for a house. When deciding whether to pay down debt or save for a down payment, focus on high-interest debt first, then save.

After paying down a lot of debt, ask your lender for a rapid rescore. This costs $25-75 but can update your credit in 2-3 days. Even a small improvement in your credit score can save you thousands in interest.

For single income earners, every bit of debt reduction helps. A client of mine paid down $4,000 in credit card debt. This improved her DTI by 3% and increased her buying power by nearly $25,000. This smart approach to debt before applying can open up more housing options for you.

Selecting mortgage products with flexibility

For solo homebuyers, picking the right mortgage is key. It turns a dream into reality. With only one income, the mortgage choice is more important.

Let’s look at options that offer both stability and flexibility for you.

Comparing Fixed Versus Adjustable Rates

Fixed-rate mortgages have steady payments. This is great for budgeting on one income. Your payments won’t change, giving you peace of mind.

But, don’t ignore adjustable-rate mortgages (ARMs). They start with lower rates, saving you money early on.

I’ve seen many single-income clients benefit from 7/1 or 10/1 ARMs when they had clear plans to either move or refinance within that fixed timeframe. The savings during those initial years allowed them to build emergency funds faster.

Here are some mortgage options for single-income buyers:

- FHA loans: Down payments as low as 3.5% with credit scores starting at 580

- Conventional 97: Only 3% down required with credit scores above 620

- 7/1 or 10/1 ARMs: Lower initial rates with 7-10 years of payment stability

- USDA Rural Development: 100% financing for homes in eligible areas (including many suburbs)

- VA loans: Zero-down options for qualifying veterans and service members

“Learn More About: How to budget for closing costs in advance“

Evaluating Lenders for Manual Underwriting

If you’re self-employed or have non-traditional income, look for lenders that do manual underwriting. They look at your whole situation, not just numbers.

Credit unions are good at this, thanks to their focus on members. They consider things like rent payments and utility bills.

When talking to lenders, ask about their manual underwriting. Ask for examples of how they’ve helped others like you. The best lender will talk about your specific situation.

| Lender Type | Manual Underwriting Availability | Benefits for Single Income Buyers | Typical Requirements |

|---|---|---|---|

| Credit Unions | High | Relationship-based lending, flexible criteria | Membership, consistent banking history |

| Community Banks | Moderate to High | Local market knowledge, personalized service | Local residence, complete documentation |

| FHA-Approved Lenders | Moderate | Government-backed flexibility | Alternative credit references, higher down payment |

| Major Banks | Low | Competitive rates when qualified | Strong credit profile, substantial documentation |

Considering Shorter Terms for Savings

While 30-year mortgages are common, think about 20-year or 15-year terms. These save you money and build equity faster. You might save 0.5% to 1% in interest.

For example, a $200,000 loan at 6% interest costs about $1,199 a month for 30 years. A 15-year term costs $1,687 a month but saves over $100,000 in interest.

If the higher payment is hard, try a compromise. Get a 30-year loan but pay like it’s a 15-year one when you can. This gives you flexibility and helps pay down the loan faster.

When comparing loans, look at the “Comparisons” section on page 3 of your Loan Estimate. It shows your total cost over five years and how much you’ll pay toward the principal. This is key for single-income buyers.

“Related Topics:

Planning emergency buffers post purchase

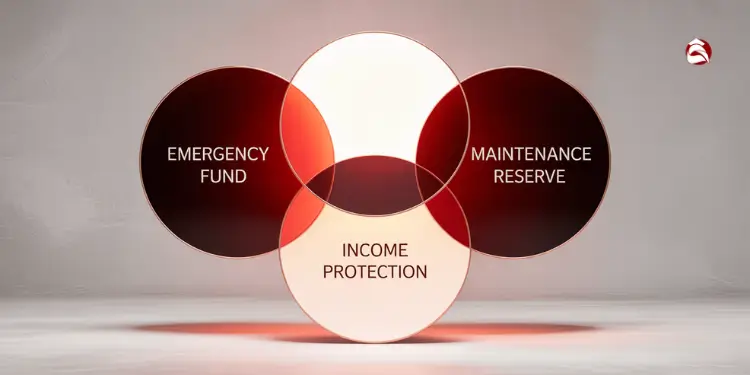

As a single income homeowner, your financial safety net is key. Unlike those with two incomes, your home payment security depends on one income. This means you need to plan carefully after buying your home.

I suggest making a three-part emergency plan. First, save 3-6 months of house costs in a high-yield savings account. Second, set aside 1% of your home’s price for repairs, adding 0.5% each year. Lastly, look into unemployment mortgage insurance for 6-12 months of payments after losing your job.

Make automatic transfers to fill up these funds after you use them. For new homeowners, this helps avoid the stress of sudden repairs on a tight budget. Also, think about getting a home equity line of credit for extra money when you need it.

Check your disability insurance too. Most employer plans only cover 60% of your income. For upkeep, plan for replacing home systems based on your inspector’s report. This way, you won’t be caught off guard by expected costs.

Also, remember that property taxes might go up after you buy your home. So, plan for possible increases in your escrow payment after the first year. Doing a budget check every six months keeps single homeowners ahead of financial surprises and lets them enjoy their home confidently.

{kind=link}