Starting with real financial goals means knowing what markets can do. I’ve seen many investors fail by aiming for too much. They don’t plan based on what markets have done before.

Some investors hit their goals, while others give up easily. Why is that?

65% of Americans with clear goals succeed, but only 17% without them do. Warren Buffett said, “Risk comes from not knowing what you’re doing.” After 12 years helping investors, I learned success is about setting reachable goals and staying with them.

Your goals should match what markets usually offer. Stocks give generally 7-10% returns, and bonds 3-5% over time. This way, you can handle market ups and downs without selling too soon.

Quick hits:

- Write down exact amounts and dates

- Sort goals by time: short, medium, long

- Choose a risk level that fits your time frame

- Set goals based on what markets have done before

- Check and change your goals every quarter

Analyze Historical Market Performance Ranges

Before you set your investment goals, look at past market trends. This can help you avoid being too pessimistic or too optimistic. Many investors make mistakes by focusing on recent trends instead of long-term patterns.

The S&P 500, a key stock index in the U.S., has seen about 10% average annual returns. But, this number hides big swings in returns over different times.

The market is the most efficient mechanism anywhere in the world for transferring wealth from impatient people to patient people.

Historical data shows big variations. For example, there were times when the S&P 500 lost money for five years. But, there were also times when it made over 20% in a year. Your goals and how long you plan to invest affect what numbers matter to you.

Since 1926, U.S. large-cap stocks (S&P 500) have delivered an average annualized total return of 9.81%, while long-term government bonds returned 5.42% and cash 3.66%—benchmarks that help set realistic return targets. Ref.: “Morningstar Research Team. (2025). What’s the Payoff? Historical Returns of the Asset Classes. Morningstar.” [!]

Bonds have given lower but steadier returns than stocks, usually between 3-5% a year. From 1980 to 2020, bonds averaged about 7.5%. But, recent years have seen lower returns as interest rates have dropped.

Volatility, or big swings in value, tends to lessen over longer periods. This is true for most investments. It’s a key part of good investment strategies.

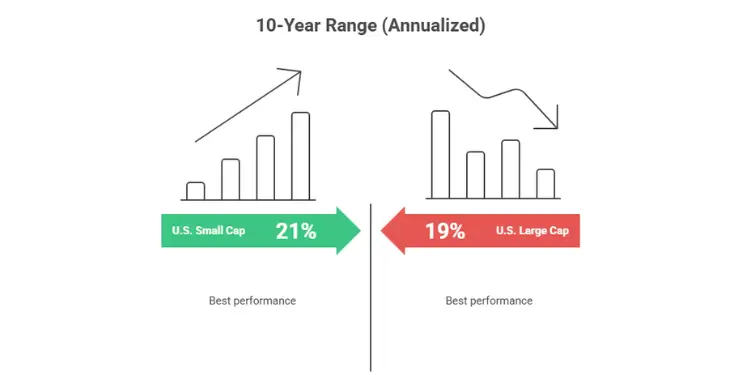

| Asset Class | 1-Year Range (Worst to Best) | 10-Year Range (Annualized) | 30-Year Range (Annualized) |

|---|---|---|---|

| U.S. Large Cap Stocks | -43% to +54% | -1% to +19% | 8% to 14% |

| U.S. Small Cap Stocks | -58% to +81% | -3% to +21% | 9% to 16% |

| U.S. Corporate Bonds | -8% to +43% | 1% to 14% | 5% to 11% |

| U.S. Treasury Bonds | -11% to +40% | 1% to 13% | 4% to 9% |

Financial markets often return to their average after big swings. This means chasing last year’s top investment can often lead to disappointment.

I suggest my clients look at historical returns for their investment goals. For a long-term goal like retirement, look at 30-year periods. For a short-term goal like a down payment, look at 5-year periods.

Focus on the worst periods, not just the averages. Your investment account should be ready for bad times, not just good ones. This helps match your investments with your risk tolerance.

My advice is to use long-term averages but be a bit more cautious. Don’t base your goals on recent trends or wishful thinking. The market gives what it gives, not what you want.

With these ranges in mind, you can see how much risk you can handle. This is key to your investment journey.

Estimate Personal Risk Capacity Honestly

Investing well isn’t just about knowing the market. It’s about knowing how much risk you can handle. After 12 years helping investors, I’ve seen a big mistake. It’s mixing up risk tolerance with risk capacity.

Risk tolerance is how much market ups and downs you can handle without freaking out. Risk capacity is how much financial risk you can handle based on your life. Knowing the difference is key to matching your goals and risk tolerance.

Your risk capacity depends on four things: how long you have to invest, how stable your income is, how much debt you have, and how safe your finances are. I suggest figuring out your “financial runway.” This is how many months you can live without a job.

For a real check, look at these three things:

- Debt-to-income ratio (monthly debt payments divided by monthly income)

- Emergency fund coverage (months of expenses saved)

- Income stability score (rate your job security from 1-10)

I’ve seen many investors think they can handle more risk than they can. One client thought he was safe with a stable job. But then he lost his job during a bad time. Without enough savings, he had to sell investments at a big loss.

Start with a real risk capacity check, not just guessing the market. This way, your long-term goals can stay on track, even with market ups and downs.

Consider Job Stability And Obligations

Your job affects how much risk you can take. People with steady jobs, like professors or government workers, can take more risk. But those with jobs that change a lot, like freelancers, can’t take as much.

I tell people to sort their job stability into three levels:

| Stability Level | Characteristics | Risk Capacity Impact | Recommended Emergency Fund |

|---|---|---|---|

| High | Tenured, government, essential services | Increases capacity | 3-6 months expenses |

| Medium | Corporate, established industry | Neutral impact | 6-9 months expenses |

| Low | Commission-based, freelance, new business | Decreases capacity | 9-12+ months expenses |

Having big financial responsibilities also limits your risk capacity. A high earner with lots of debt can’t take as much risk as someone with less debt. Saving for emergencies is even more important when you have big responsibilities.

Try this simple test: List all your financial responsibilities by when they need to be paid (1-3 years, 3-10 years, 10+ years). Then, figure out what percentage of your income goes to these responsibilities. If more than 50% goes to fixed costs, you can’t take as much risk.

Your debt-to-income ratio affects how you should split your investments. For example:

- Low obligations (under 30% of income): May support 70-80% growth assets

- Medium obligations (30-50% of income): Consider 50-70% growth assets

- High obligations (over 50% of income): Limit to 30-50% growth assets

Those with big responsibilities should save more before aiming for big growth. This way, you can keep up with your investment plan even when things get tough.

Check your job stability and responsibilities every year. Big changes, like a new mortgage or a child’s college fund, mean it’s time to rethink your investment plan. This keeps you focused on setting goals that really fit your financial situation.

Set Target Returns Matching Benchmarks

When you plan your investments, it’s smart to match your goals with benchmarks. This keeps you on the right path. Many people set goals that are too high, based on what they wish for, not what’s possible.

Start by knowing which benchmarks fit your situation. Your goals and time frame decide the right benchmark. For long-term goals like retirement, broad market indices are good. For short-term goals, like buying a house, more conservative benchmarks are better.

“The most dangerous words in investing are ‘this time it’s different,'” Warren Buffett said. Even though history won’t repeat exactly, it gives us a good idea of what to expect.

Your mix of investments affects what returns you can expect. Knowing your investment goals helps pick the right benchmark. Without this, you might take too much risk chasing high returns.

| Portfolio Allocation | Historical Annual Return | Risk Level | Appropriate For |

|---|---|---|---|

| 100% Bonds | 3-5% | Low | Short-term goals, conservative investors |

| 60% Stocks/40% Bonds | 7-8% | Moderate | Medium-term goals, balanced approach |

| 80% Stocks/20% Bonds | 8-10% | Moderately High | Long-term growth, higher risk tolerance |

| 100% Stocks | 9-11% | High | Long-term goals, high risk tolerance |

Current market conditions affect what returns you can expect. Investors often make mistakes by expecting too much during bull markets. High valuations or low interest rates usually mean lower returns later.

A financial advisor can help you avoid bad benchmarks. Using the wrong benchmarks can lead to frustration and poor decisions.

To set realistic goals, calculate your expected return based on your investments:

- List each asset class in your portfolio (stocks, bonds, etc.)

- Note the percentage allocation for each

- Assign a reasonable historical return to each based on benchmarks

- Multiply each allocation percentage by its expected return

- Add these figures to get your portfolio’s weighted expected return

Reference Historical Index Average Returns

Looking at historical returns helps set achievable goals. Different time periods show how market performance changes. This helps set clear goals for a specific time.

Morningstar’s rolling real-return analysis shows that a 100 % stock portfolio has avoided any cumulative loss over every 20-year window since 1926, underscoring how extended horizons dampen volatility. Ref.: “Rekenthaler, J. (2023). How Time Horizon Affects the Odds of Equity Investing. Morningstar.” [!]

Rolling returns give more insight than simple averages. They show the range of outcomes based on when you start and finish investing.

| Market Index | 10-Year Rolling Return Range | 20-Year Rolling Return Range | 30-Year Rolling Return Range |

|---|---|---|---|

| S&P 500 (Large US Stocks) | -3% to +19% | 4% to 18% | 8% to 14% |

| Russell 2000 (Small US Stocks) | -2% to +21% | 5% to 17% | 8% to 15% |

| MSCI EAFE (International Stocks) | -5% to +22% | 2% to 15% | 5% to 12% |

| Bloomberg Aggregate (US Bonds) | 2% to 13% | 3% to 10% | 4% to 9% |

Notice how the ranges get smaller with longer time horizons. This shows that longer time frames reduce the impact of market ups and downs. Your time horizon should match your return expectations.

Inflation-adjusted returns tell a fuller story than just nominal figures. A 7% return during 3% inflation means only 4% in real purchasing power. High-yield investments often barely keep up with inflation after taxes.

When using history to set targets, remember that higher returns mean higher risk. The best approach balances your return needs with your risk tolerance. As I tell my clients, “You can demand any return you want from your portfolio, but the market decides how much risk you’ll take to get it.”

Write down your return expectations for each goal. This makes you accountable and helps track progress. Investing may seem uncertain, but realistic expectations based on history guide your financial journey.

Plan Cushion For Market Volatility

Creating a financial buffer for market volatility is key. It’s a must for goal-based investing. After 12 years, I’ve seen markets rarely follow smooth paths. They zigzag, making it vital to plan for volatility.

There’s a big risk called “sequence of returns risk.” It means the order of your returns is very important. This is true when saving for big things like retirement or a new car. A big drop in the market early on can ruin your plans.

Sequence-of-returns studies show sustainable withdrawal rates varying from 1.6 % to 20.7 % for identical portfolios—purely due to the order of market returns—highlighting the need for buffers and glide-paths. Ref.: “Pfau, W. D. (2015). The Lifetime Sequence of Returns: A Retirement Planning Conundrum. Journal of Retirement.” [!]

Two investors with the same average returns over 20 years can have very different outcomes. This is because major losses early on can hurt your plans. So, it’s smart to save extra money as a cushion.

“For More Information: Investment Goal Planning Basics for Beginner Investors“

Practical Volatility Cushioning Strategies

From working with many clients, I’ve found four ways to protect against volatility:

- Set target dates earlier than actual need dates – Plan to reach your goal a few years early. This gives your money time to recover from market drops.

- Build in a 15-20% buffer amount – Add 15-20% to your goal amount. This helps absorb market ups and downs.

- Gradually reduce volatility – As your goal gets closer, move your money to safer investments. This helps lock in your gains.

- Create separate liquidity reserves – Keep some money set aside just for emergencies. This is your volatility buffer.

These strategies aren’t about trying to time the market. They’re about understanding market reality. The cushion you build should fit your personal timeline and risk level.

“The most successful investors I’ve worked with aren’t those who predicted market moves, but those who built in enough cushion to stay the course when markets inevitably surprised them.”

Recommended Volatility Cushions By Timeline

| Goal Timeline | Recommended Buffer | Volatility Reduction Strategy | Review Frequency |

|---|---|---|---|

| 1-2 years | 25-30% | Primarily cash and short-term bonds | Monthly |

| 3-5 years | 20-25% | Conservative allocation with limited equity | Quarterly |

| 6-10 years | 15-20% | Moderate allocation with increasing stability | Semi-annually |

| 10+ years | 10-15% | Growth focus with gradual de-risking | Annually |

These strategies have helped many clients. One client didn’t give up on buying a home during the 2020 crash. We had a 20% cushion and set his target date 18 months early.

When market volatility hits, you’ll need to adjust your plan. Having these buffers means you can make small changes. Your return expectations should always be realistic, not based on past averages.

Volatility can work for you too. The same strategies that protect you from downturns also help you make the most of market surges. This balanced approach makes volatility a manageable part of your investment journey.

Adjust Contributions When Circumstances Change

Being able to change your investment contributions when things change is key. I’ve seen many plans fail because they didn’t adapt to life’s ups and downs. Your financial path won’t always be straight. Incomes change, emergencies happen, and your goals can shift.

It’s smart to regularly check and adjust your investment plan. Look to change it when you get a new job, have a baby, get extra money, see market changes, or get closer to your goals.

Set up regular checks on your investment plan every three months. These should be about making smart, goal-based changes, not just reacting to market news. This way, you can keep moving forward, even when money surprises come up.

“The investor who knows when to adjust their sails often reaches their destination faster than the one who stubbornly maintains course through every storm.”

“Read More: Financial Goals vs Investment Goals Differences Explained“

Increase Savings After Salary Increases

One great way to change your finances is through “contribution laddering.” This means adding more to your investments when you get a raise. It helps you save more without spending more on everyday things.

When you get a raise or bonus, put at least half of it into your investments right away. This habit can grow your money faster than trying to get better returns.

Capturing your full 401(k) employer match provides an instant 50–100 % guaranteed return on the matched dollars—performance no conventional investment can replicate. Ref.: “The Vanguard Group. (2025). How Much Does an Employer Match Help? Vanguard.” [!]

Here’s a plan for how to use extra money:

- First, fill up employer-matched retirement accounts (get an extra 50-100% return)

- Then, build up your emergency fund for 3-6 months of living costs

- Next, pay off high-interest debt

- After that, put money into tax-advantaged accounts based on when you need it

- Lastly, use money for taxable investments for goals that are not too far away

I worked with someone who put 60% of each raise into investments. In 11 years, they reached financial freedom five years early. Starting early makes a big difference.

It’s easy to start: set up automatic increases, use payroll deductions, and schedule review times. Small, steady increases can lead to big results over time.

“Check This Out: Examples of Common Investment Goals for Beginners“

Pause Extras During Economic Downturns

When the economy is tough, you need to adjust your investment plan. I suggest a “contribution triage” method to cut back without hurting your long-term plan too much.

In 2008 and 2020, investors who paused some contributions but kept others recovered faster than those who stopped investing. It’s about making smart choices, not panicking.

Here’s how to cut back on contributions:

| Priority Level | Account Type | Action During Stress | Recovery Strategy |

|---|---|---|---|

| 1 – Highest | Employer-matched retirement | Maintain at least minimum match | First to restore to full funding |

| 2 | Emergency reserves | Temporarily redirect to build buffer | Resume investments once 3-month buffer exists |

| 3 | Tax-advantaged accounts | Reduce but don’t eliminate if possible | Gradually increase as stability returns |

| 4 | Non-essential goal funding | Pause completely if necessary | Last to restore after stability returns |

| 5 – Lowest | Speculative investments | Halt entirely | Resume only after all essentials funded |

When you pause contributions, set clear times to start again. This could be when you reach a certain savings goal, get back to your old income, or see the market stabilize.

In tough times, I often tell clients to use some investment money to build up their emergency fund. This gives peace of mind and prepares you to start investing fully again when things get better. Remember, pauses should be temporary, not permanent.

The best investors I’ve worked with kept their focus on long-term goals, not short-term ups and downs. Your investment path will face challenges, but with a solid plan, these won’t stop you for long.

“Related Topics: How to Adjust Investment Goals Over Time“

Review Goals Annually Against Performance

Checking your investments regularly is key to success. Set a reminder to look at your goals, money needs, time frame, and how much risk you can once a year. This helps a lot—65% of people with clear goals do better than those without.

Writing your goals down and sharing weekly progress boosts goal-achievement rates to 76%, versus just 43% for people who merely think about their goals. Ref.: “Matthews, G. (2007). The Impact of Commitment, Accountability, and Written Goals on Goal Achievement. Dominican University of California.” [!]

See if your investment mix has changed. It’s important because it can affect your returns a lot. If your mix is off by more than 5%, it’s time to fix it. Also, watch out for fees. A small difference can add up over time.

“Further Reading:

Revise Targets To Maintain Realism

Life changes, and so should your investment goals. For short-term needs like a house, consider high-yield savings or Treasury bills. They offer 4-5% returns now. For longer goals, keep the right mix of investments.

Good investors know the difference between short and long-term goals. This helps them make better choices when the market changes. Knowing your short-term needs are safe lets you see downturns as chances for growth. This mindset keeps you focused on your long-term goals, even when the market is shaky.

Keep a record of each review to see how you’re doing. This habit is good for both new and experienced investors. When your life changes, your goals should too. It shows you’re actively planning for your financial future.

{kind=link}