Knowing the difference between saving and investing is key to a good financial plan. These two ways help you manage your money in different ways. But, many people mix them up.

Ever wonder why some people get rich while others don’t, even with the same income? It’s often because of how they use their money for saving and investing.

A 2023 Federal Reserve survey found that only 36% of Americans have enough cash for a $400 emergency. This shows why knowing the difference between saving and investing is very important. Warren Buffett said, “Someone’s sitting in the shade today because someone planted a tree long ago.”

I’ve helped many people through different market times. Success usually comes from knowing when to save and when to invest. It depends on your financial goals.

The time horizon for each financial goal is key in choosing the right strategy. A good financial plan uses both saving and investing wisely for different goals.

Quick hits:

- Saving prioritizes safety and accessibility

- Investing embraces risk for growth

- Goals dictate which approach works

- Most plans need both strategies

Defining Saving and Investing Core Differences

Saving and investing are two ways to handle your money. They help you grow your wealth but in different ways. Knowing when to save and when to invest is key to reaching your financial goals.

Choosing between saving and investing is more than just where you put your money. It’s about your mindset, how long you plan to keep your money, and how much risk you can take. Let’s look at these differences to help you find a balance that keeps your money safe and grows it too.

Saving Purpose and Typical Accounts

Saving is about keeping your money safe for later. It helps you build an emergency fund, reach short-term goals, and feel financially secure.

The main advantage of saving is that it’s safe. Your money is protected in a savings account. This safety comes with a trade-off: you might not earn as much as you could with investments.

Common places to save include:

- High-yield savings accounts: They offer better interest rates than regular savings accounts but are easy to access.

- Money market accounts: They mix features of checking and savings accounts with slightly higher interest rates.

- Certificates of deposit (CDs): They offer fixed interest rates for a set time, but you’ll face penalties if you withdraw your money early.

- Treasury bills: They are short-term government securities with little risk and tax benefits.

FDIC insurance protects up to $250,000 per depositor, per insured bank, for each ownership category—covering both principal and accrued interest in the event of bank failure.Ref.: “Federal Deposit Insurance Corporation. (2024). Deposit Insurance At A Glance. FDIC.” [!]

The good and bad of saving are clear. Saving keeps your money safe, accessible, and predictable. But, it might not grow as fast as inflation, which could make your money worth less over time.

Saving is best for short-term goals or emergencies. If you’re saving for a vacation soon or need money for unexpected bills, saving is usually the right choice.

Investing Purpose and Common Vehicles

Investing is different. It’s about growing your money over time. When you invest, you buy assets that could increase in value or earn income. The main goal is to build wealth through growth and income.

Investing needs a longer time frame, usually 5+ years, to handle market ups and downs and see good returns. Investing offers the chance for higher returns, income, and building wealth over time.

Common investment options include:

- Stocks: They are shares in companies that can grow in value and pay dividends.

- Bonds: They are debt securities that pay interest, including government, municipal, and corporate bonds.

- Mutual funds: They are professionally managed portfolios that pool money from many investors.

- Exchange-traded funds (ETFs): They are like mutual funds but traded like stocks all day.

- Real estate: It’s property investments that can earn rental income and grow in value over time.

The main trade-off with investing is taking on risk for the chance of higher rewards. Market ups and downs mean you could lose money short-term. But, history shows diversified investments grow over time. This makes investing better for long-term goals like retirement, college, or building wealth.

Investment accounts come in many forms, like taxable brokerage accounts, retirement accounts like 401(k)s and IRAs, and education-specific accounts like 529 plans. Each has different tax rules and withdrawal rules that can affect your returns.

| Feature | Saving | Investing |

|---|---|---|

| Primary Purpose | Capital preservation | Wealth growth |

| Typical Time Horizon | 0-3 years | 5+ years |

| Risk Level | Low (minimal chance of losing principal) | Moderate to high (possible loss) |

| Current Typical Returns (2023) | 3-5% (high-yield savings) | 7-10% (diversified portfolio, historical average) |

| Inflation Protection | Limited (may not keep pace) | Better chance to outpace inflation |

| Liquidity | High (easily accessible) | Varies (potentially lower) |

| Best For | Emergency funds, short-term goals | Retirement, education, wealth building |

Choosing between saving and investing isn’t a permanent decision. Most successful financial plans use both strategies. The right mix depends on your age, goals, and how much risk you can handle. Saving protects your money today, while investing builds your future wealth.

“Further Reading:

Risk Reward Tradeoffs Across Time Horizons

Your financial timeline changes how much you can risk and how much you can gain. When I talk to clients about saving or investing, I stress that time is key. It often decides the best strategy for you.

The risk and reward balance changes over time. It depends on when you need your money. Your ability to handle market ups and downs is less about feeling scared and more about when you need the cash.

Let’s look at how time affects your wealth-building:

- Short-term goals (0-2 years): For quick goals like an emergency fund or a vacation, saving is safer. It might not grow as much, but you can get your money when you need it.

- Mid-term goals (3-7 years): Saving for a home down payment can mix growth with stability. This balance works well for goals a few years away.

- Long-term goals (8+ years): For goals far off, like retirement, you can handle more risk. This means you might get more money in the long run.

The S&P 500 has delivered an average annual return of about 10 % since 1957—powerful historical support for using diversified equities to outpace inflation over multi-decade horizons.Ref.: “Maverick, J. B. (2025). S&P 500 Average Returns and Historical Performance. Investopedia.” [!]

For short-term goals, saving in a bank or money market account is best. The lower return might seem small, but you can get your money anytime. This is more important than a little extra growth.

Think about saving for a car in a year. A 7% return doesn’t help if the market drops 20% right before you need it. Having $10,000 when you need it is better than risking $8,000 to $11,000.

Mid-term goals offer more options. Saving for a home down payment in five years can use a mix:

- 50-60% in stable savings

- 30-40% in bond funds

- 10-20% in investments for growth

This mix aims for some growth while keeping your main goal safe. Before investing, think about how flexible your timeline is. Could you wait a year if the market drops?

For long-term goals, investing can lead to better results than saving. Over 10 years, stocks have usually done better than savings, even with big market swings.

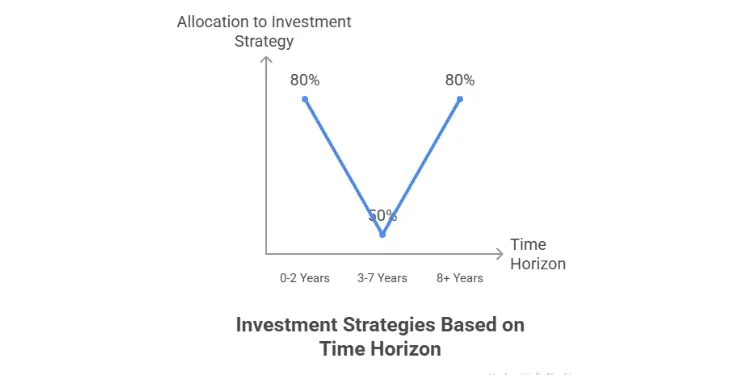

| Time Horizon | Recommended Strategy | Primary Benefit | Key Consideration |

|---|---|---|---|

| 0-2 Years | Savings (80-100%) | Capital preservation | Guaranteed access when needed |

| 3-7 Years | Blended (40-60% savings) | Moderate growth | Timeline flexibility |

| 8+ Years | Investing (70-90%) | Maximum growth | Ability to weather market cycles |

Volatility Impact on Goal Deadlines

Not all deadlines are the same. When deciding to save or invest, consider how strict your deadline is. Deadlines can be hard, soft, or floating.

- Hard deadlines: Fixed dates with serious consequences if missed (college tuition due dates, tax payments)

- Soft deadlines: Target dates with some flexibility (home purchase that could shift by 6-12 months)

- Floating deadlines: Goals with significant flexibility (retirement that could shift by 1-3 years)

For hard deadlines, saving is safer. If you need money fast, like for an emergency fund, you can’t afford to lose it to market swings.

Market ups and downs are a problem for short-term goals. When you invest, the order of returns matters a lot for goals with deadlines. A 20% drop followed by a 25% gain doesn’t get you back to even.

For goals with hard deadlines, I suggest a “glide path” strategy. As your deadline gets closer, move money from investments to savings. This helps secure your gains and reduce risk.

A practical timeline might look like this:

- 3+ years from goal: Maintain growth-oriented allocation

- 2 years from goal: Move 25-30% to more conservative options

- 1 year from goal: Shift 50-60% to savings vehicles

- 6 months from goal: Transfer 80-90% to guaranteed access accounts

This gradual move protects you from bad timing luck. Remember, money needed now behaves differently than money growing over time. The longer you can wait, the more you can risk for higher returns.

When setting goals, ask yourself: “What happens if this money isn’t available exactly when planned?” If the answer is bad, saving is safer. If you can wait, investing might help you reach your goals.

“Related Articles: Best Zero Budgeting Tools for Hassle-Free Planning“

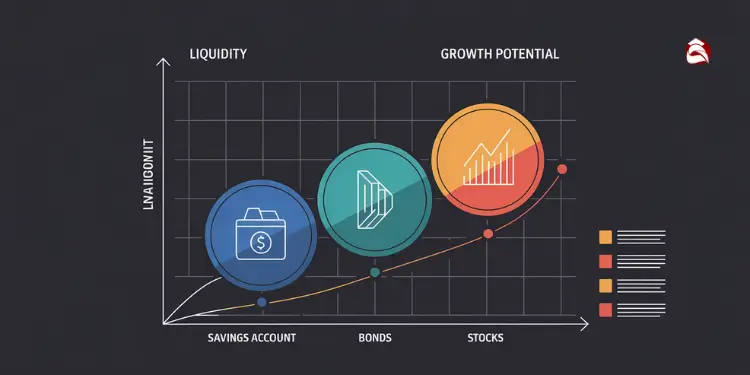

Liquidity Needs Versus Growth Potencial

It’s key to know that money can either be easy to get or grow a lot. This choice affects how you build wealth and stay safe financially.

Every dollar has to decide: stay easy to get or grow a lot. Money that’s easy to get doesn’t earn much. But, money that grows a lot is hard to get.

“The emergency fund isn’t just financial insurance—it’s psychological freedom that enables confident investing with your remaining assets.”

Starting a good financial plan means having an emergency fund. This fund should cover three to six months of living costs. It’s not just for car repairs or medical bills. It also lets you invest other money without worry.

Without an emergency fund, you might have to sell investments at bad times. This can lead to losing money. Many investors make this mistake by investing too much without enough cash.

Build an emergency fund covering 3–6 months of essential expenses in a liquid, FDIC-insured account before committing surplus cash to higher-risk investments.Ref.: “Felton, C. S. & Vanguard Research Team. (2023). In Case of Emergency, Break Glass: Managing Household Liquidity. Vanguard Research.” [!]

Your need for liquid money depends on your financial situation:

- Income stability (steady salary vs. variable income)

- Number of dependents relying on your finances

- Existing insurance coverage (health, disability, property)

- Debt obligations and monthly fixed expenses

- Career field and employment security

Money options range from easy to get to hard to get. Checking accounts are easy to access but don’t earn much. Retirement accounts are hard to get but offer tax benefits for long-term goals.

High-yield savings accounts are a middle choice. They’re safe and earn more than checking accounts. But, they don’t grow as much.

Looking at growth, small differences add up over time. For example, $10,000 growing at different rates shows big wealth differences:

| Investment Vehicle | Average Annual Return | Value After 10 Years | Value After 20 Years | Value After 30 Years |

|---|---|---|---|---|

| Bank Savings | 1% | $11,046 | $12,202 | $13,478 |

| Certificate of Deposit | 3% | $13,439 | $18,061 | $24,273 |

| Bond Portfolio | 5% | $16,289 | $26,533 | $43,219 |

| Investing in the Stock Market | 8% | $21,589 | $46,610 | $100,627 |

These numbers show why investing beats saving. The difference between a 1% savings account and an 8% stock market return is huge. It’s the difference between $13,478 and $100,627 after 30 years.

The national average savings yield is just 0.6 % APY, while top high-yield accounts exceed 4 %, illustrating the opportunity cost of leaving large balances in low-rate accounts.Ref.: “Bankrate Editors. (2025). Average Savings Account Interest Rate for June 2025. Bankrate.” [!]

But, these great returns need patience. Markets grow money over time, but there’s no promise of future success. Shorter time frames mean more risk.

The right approach isn’t just choosing between easy money and growth. It’s about creating a plan that matches your money to your goals:

- Immediate needs (0-3 months): High-liquidity checking/savings accounts

- Short-term safety (3-12 months): High-yield savings accounts or money market funds

- Medium-term goals (1-5 years): Certificates of deposit or short-term bond funds

- Long-term growth (5+ years): Diversified investment portfolios aligned with your risk tolerance

This plan keeps enough money for now while growing the rest for later. It uses the power of compounding.

What makes investors succeed isn’t always picking the right investments. It’s balancing money needs with growth chances through life’s ups and downs.

Tax Considerations Shaping Goal Outcomes

Every dollar you save or invest has a tax effect. This effect can help or hurt your financial goals. Knowing how taxes work with different accounts helps you keep more money.

The government gives tax breaks for certain money moves. These breaks can really help you grow your wealth. Let’s look at how to use these breaks based on your goals.

Sheltered Accounts for Long Term Goals

Accounts like 401(k)s and traditional IRAs are great for long-term goals. They offer tax breaks that can make your money grow faster.

With accounts like 401(k)s and traditional IRAs, you pay less in taxes now. For example, putting $6,000 in a traditional IRA could save you $1,320 if you’re in the 22% tax bracket. Your money grows without being taxed every year, which helps it grow more.

Think about this: $10,000 invested for 30 years at 7% grows to about $76,100 in a tax-deferred account. But it only grows to $57,400 in a taxable account (assuming a 22% tax rate). This tax break can make your investment 33% more effective.

With a traditional, non-Roth account, the money you contribute is deducted from your taxable income, meaning you pay less in taxes. Plus, the investments grow tax-deferred, so your money compounds without annual tax bills.

Roth accounts (IRAs and 401(k)s) work differently. You pay taxes on contributions now but get tax-free withdrawals later. This is good if you think you’ll be in a higher tax bracket later or want tax-free money in retirement.

Other tax shelters include:

- Health Savings Accounts (HSAs): Triple tax advantage with tax-deductible contributions, tax-free growth, and tax-free withdrawals for medical expenses

- 529 Plans: Tax-free growth and withdrawals for qualified education expenses

- ABLE Accounts: Tax-advantaged savings for disability-related expenses

Each account has its own rules for how much you can contribute and who can use it. For 2023, you can put up to $22,500 in a 401(k) ($30,000 if over 50), and up to $6,500 in an IRA ($7,500 if over 50).

Withdrawing money early from retirement accounts usually means a 10% penalty plus taxes. But there are exceptions for things like buying a first home, education, and certain hardships. This penalty makes these accounts for long-term use.

“Read More: Saving vs Investing for Financial Goals Explained“

Taxable Accounts for Short Term Safety

For goals within 5 years, taxable accounts are often better. They let you get your money without penalties, which is important for short-term needs.

Interest from savings accounts, CDs, and money market accounts is taxed as regular income. But, investments held over a year get lower tax rates. This difference can help you save or invest for 2-5 years.

Money market *mutual funds* are not federally insured and, unlike money-market deposit accounts, can lose value during severe market stress.Ref.: “FINRA. (2025). Start an Emergency Fund. Financial Industry Regulatory Authority.” [!]

This tax difference offers a strategic chance. If you need to save or invest for 2-5 years, consider these options:

| Account Type | Tax Treatment | Best For | Tax Minimization Strategy |

|---|---|---|---|

| High-yield savings | Interest taxed as ordinary income | Goals under 2 years | Consider municipal money markets if in high tax bracket |

| Taxable brokerage | Capital gains rates for investments held >1 year | Goals 2-5 years away | Tax-loss harvesting; hold positions over 1 year |

| I-Bonds | Federal tax-deferred; state tax-exempt | 1-5 year goals with inflation protection | Hold at least 5 years to avoid interest penalties |

When investing in taxable accounts, where you put your money matters. Put tax-efficient investments (like index ETFs) in taxable accounts. Put tax-inefficient investments (like REITs) in tax-advantaged accounts.

Tax-loss harvesting—selling investments at a loss to offset gains—can save you up to $3,000 in taxes each year. This is great during market downturns.

Your tax situation affects where you put your money. Those in higher tax brackets get more from tax-advantaged accounts. Those in lower brackets might prefer flexibility over tax savings.

The rule of thumb: match your account type to your goal timeline. Use tax-advantaged accounts for long-term goals like retirement. Use taxable accounts for short-term needs like emergencies or near-term purchases.

Remember, investment goals influence your portfolio at every level, including taxes. The best strategy balances tax savings with your need for quick access and the right risk level.

“Explore More: How to Avoid Overspending on House Purchase Budget“

Choosing Strategy for Each Goal Timeline

Deciding whether to save or invest depends on when you need the money. Saving is for now, while investing is for later. A good plan uses both, matching your goals.

Consumer prices rose an average 2.9 % per year from 1983 to 2013; savings earning below this rate suffer a loss of real purchasing power over time.Ref.: “Bureau of Labor Statistics. (2014). One Hundred Years of Price Change: The CPI and the American Inflation Experience. Monthly Labor Review.” [!]

Decision Framework Action Steps Guide

First, sort your goals by time. For needs in 0-3 years, like a house payment, save in safe places. These give 1-3% a year and keep your money safe.

For goals in 3-10 years, mix investments. This mix aims for 4-6% returns through balanced funds and dividend-paying investments.

“For More Information:

For goals over 10 years, like retirement, go for growth. These can give 7-10% returns and beat inflation over time.

Always have a 3-6 month emergency fund first. Then, grab any employer retirement matches, pay off high-interest debt, and fund your goals based on their timelines.

Make automatic transfers to your savings and investments. This makes your plan real. Check your progress every quarter and adjust as needed.

{kind=link}