Your investment goals need regular checkups to stay healthy. As December approaches, this timing offers a perfect opportunity to assess how well your financial strategy aligns with your life objectives. Year-end reviews aren’t just calendar rituals—they’re navigation tools that keep your money working effectively for you.

Did you know that investors who conduct structured annual reviews typically see 12-18% better long-term results? I’ve witnessed this firsthand guiding clients through market cycles. As Warren Buffett wisely noted, “Risk comes from not knowing what you’re doing,” and annual reviews directly address this knowledge gap.

Over my 12 years in Phoenix, I’ve noticed how life changes can subtly shift your financial needs without triggering immediate attention. Your investment goals influence your entire portfolio structure, making regular recalibration essential—not optional.

I recently helped a client discover $27,000 in unnecessary fees through their annual review—money that’s now working toward their retirement instead of padding someone else’s pocket.

Quick hits:

- Identify performance gaps against benchmarks

- Reassess risk tolerance after life changes

- Capture tax opportunities before year-end

- Realign allocations with current priorities

Implementing a disciplined, annual review process can add up to 3 percentage points in net yearly returns—compounding to roughly 15-20 % more wealth over five years—by integrating rebalancing, tax management, and behavioral coaching.Ref.: “Kinniry, F. M., Jaconetti, C. M., DiJoseph, M. A., & Walker, D. J. (2022). Putting a Value on Your Value: Quantifying Vanguard Advisor’s Alpha. Vanguard Research.” [!]

Adopt Annual Goal Review Discipline

Successful investing is not just about picking the right assets. It’s also about regular reviews. Without them, even the best portfolios can stray from your goals. Just like you wouldn’t skip doctor visits, your money needs regular check-ups too.

Set a time each year for your investment review. It could be January for a new start or October for year-end planning. What’s important is being consistent, not the exact time.

Many investors only review their portfolios when the market is shaky. This can lead to emotional decisions. By setting a fixed date, you review your investments in calm and stormy times alike.

Keep all your investment documents in one place. This could be a folder or a digital file. It makes reviewing your investments easier and less scary.

Before you start reviewing your investment goals, check your current financial situation. Life changes like new jobs or family members can change your goals. What was right last year might not be today.

Prepare Checklists For Efficient Review

A checklist helps you not miss important parts of your review. Without it, you might only look at how your investments are doing. You might forget to check if they match your risk level and if you’re paying too much in fees.

Start getting ready for your review two weeks early. This gives you time to gather all your documents and think about any life changes. Rushing through can lead to shallow analysis.

Mark any big life changes that have happened. These could be:

- Career changes or income changes

- Family additions or losses

- Getting an inheritance or other big money

- Health changes that affect your plans

- Changes in retirement plans or goals

Make a simple chart to track your goals. It will show if you’re on track or not. For each goal, write down the target amount, how much you have now, and how close you are to reaching it.

Give yourself a block of time without interruptions for this review. I recommend at least two hours. This time can reveal insights that improve your future investments.

Sort your goals into short-term (less than 3 years), mid-term (3-10 years), and long-term (more than 10 years). Each type needs a different approach to risk and how you spread your investments. This helps make sure your strategy fits your goals.

| Review Category | Documents Needed | Key Questions | Action Items |

|---|---|---|---|

| Goal Assessment | Previous investment policy statement, financial plan | Have my goals changed? Am I on track? | Update goal timeline and target amounts |

| Performance Review | Account statements, benchmark data | How did my investments perform vs. benchmarks? | Identify underperforming assets for possible changes |

| Risk Evaluation | Risk tolerance questionnaire, portfolio allocation | Does my current risk match my comfort level? | Adjust asset allocation if risk tolerance has changed |

| Cost Analysis | Fee disclosures, expense ratios | Am I paying more than necessary? | Find lower-cost options for similar investments |

| Life Changes | Personal records, tax returns | What major life events affect my strategy? | Adjust my investment approach based on new circumstances |

Over time, your annual reviews become more valuable. They help you see patterns in your investment choices and results. Each year’s review is a reference point for better decision-making.

Remember, reviews are key for tracking performance and staying aligned with your life. Regular reviews can make you a successful investor, not just someone who misses their financial goals.

Collect Portfolio Performance And Benchmark Data

To check how well your investments are doing, you need to collect all the data. This step is key to making smart choices about your money. Without the right data, you’re making choices without knowing the facts.

Start by getting statements from all your investment accounts for the last year. Look at more than just the start and end balances. See how each part of your portfolio did and how they all work together. This helps you know what’s helping and what’s not.

Knowing why investment goals are important becomes clear when you collect this data. Your numbers only make sense when compared to your own goals, not just any standard.

Calculate Time Weighted Returns Accurately

When you check your investments, how you calculate matters a lot. Time-weighted returns give a clear picture by ignoring cash flow changes.

Many investors get their results wrong by not accounting for cash flow. For example, adding money during a dip can make your returns seem lower. Taking money out during a peak can make your returns seem higher than they are.

Most brokerages now offer time-weighted returns. If yours doesn’t, you can calculate them by breaking your period into parts between each cash flow. Then, find the return for each part and compound them together.

The GIPS standards require time-weighted returns for most portfolios because they remove the distortion of external cash flows, providing a fair basis for manager comparison.Ref.: “CFA Institute. (2025). Overview of the Global Investment Performance Standards for Firms. CFA Institute.” [!]

Always compare your results to the right benchmarks. Using the S&P 500 for your whole portfolio is not always right. Match each part of your portfolio with its own index:

- Large-cap U.S. stocks: S&P 500

- Small-cap U.S. stocks: Russell 2000

- International developed markets: MSCI EAFE

- Core bonds: Bloomberg U.S. Aggregate Bond Index

- Real estate: FTSE NAREIT All REITs

For bonds, look at yield and total return separately. Yield shows income, while total return includes price changes. In rising rate times, bonds might show negative total returns but keep giving income.

Compare Costs Against Industry Averages

Investment costs cut into your returns over time. Even small fee differences add up over years. Paying 1% instead of 0.5% means losing tens of thousands of dollars over time.

Find your portfolio’s “true cost” by adding all expenses. This includes fund fees, trading costs, advisory fees, and account charges. Don’t forget tax drag, the loss in returns due to taxes on income and gains.

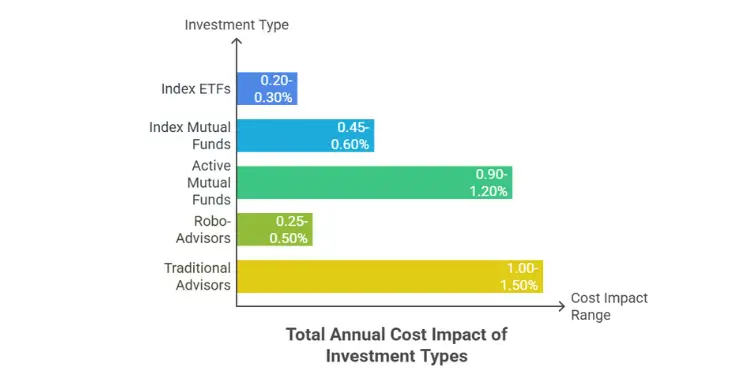

Expense ratios have dropped a lot in recent years. Passive funds now charge 0.03%-0.25%, while active funds average 0.60%-0.90%. If you’re paying more, look for cheaper options that might give similar results.

The table below shows current average investment costs to help you compare:

| Investment Type | Average Expense Ratio | Trading Costs | Tax Efficiency | Total Annual Cost Impact |

|---|---|---|---|---|

| Index ETFs | 0.18% | $0-$5 per trade | High | 0.20%-0.30% |

| Index Mutual Funds | 0.40% | $0-$20 per trade | Medium | 0.45%-0.60% |

| Active Mutual Funds | 0.76% | $0-$20 per trade | Low | 0.90%-1.20% |

| Robo-Advisors | 0.25% | Included | Medium-High | 0.25%-0.50% |

| Traditional Advisors | 0.25%-0.50% | Varies | Varies | 1.00%-1.50% |

Keep your findings in a way that lets you compare year to year. This shows patterns that aren’t clear in one year. When looking at mutual funds or ETFs, compare them to others in their group, not to different types.

Also, separate the results from the market and from the manager. This helps you avoid switching funds too soon. You want to know when a manager is really not doing well, not just when the market is down.

To learn about prioritizing multiple investment goals, visit How to Prioritize Multiple Investment Goals as a Beginner.

Assess Goal Progress And Risk Alignment

Your investment journey needs regular checks. This ensures your portfolio matches your financial goals and risk comfort. Over the years, I’ve seen that checking goals needs numbers and honest thoughts. This mix shows if you’re on the right path or need to change.

First, figure out the return you need for each goal. For example, if you want $500,000 in 15 years and have $200,000 now, what return do you need? Compare your goal return with what you’re getting. If there’s a difference, like needing 7% but getting 5%, you have choices.

Your risk tolerance changes with life. Big life events, income changes, or retirement plans can affect how much risk you can handle. I suggest doing a risk tolerance quiz every year. Think deeply about how market changes make you feel.

The most dangerous risk is the one you’re taking without realizing it. Annual alignment between your stated risk tolerance and actual portfolio construction eliminates this blind spot.

Look at your portfolio’s risk levels (standard deviation, beta, duration) and compare them to what you’re comfortable with. Many find their investments are riskier or safer than they thought. This can happen as markets change what they hold.

Check each goal’s investment time horizon and adjust your investments. Goals near 3-5 years should focus on keeping your money safe, no matter your risk level. Your ability to handle market ups and downs drops as you get closer to needing the money.

| Assessment Area | Key Questions | Action If Off-Track | Frequency |

|---|---|---|---|

| Performance Gap | Is your actual return meeting required return? | Increase contributions or adjust timeline | Annually |

| Risk Alignment | Does portfolio volatility match your comfort level? | Rebalance to target allocation | Annually |

| Time Horizon Shifts | Have goal deadlines changed? | Adjust asset allocation accordingl | Annually |

| Risk Capacity | Has your financial cushion changed? | Modify emergency reserves | Annually |

Keep track of your risk capacity (emergency funds, income, insurance) and willingness to take risk (comfort with market swings). These can move in opposite ways as your wealth grows. It’s common for investors to want less risk as they get closer to their goals.

If you find you’re not on track to meet your investment goals, don’t worry. Small, steady changes can make a big difference. The financial markets reward those who stay true to their goals and risk tolerance. Regular checks are key to long-term success.

Plan Rebalancing And Contribution Adjustments

When some assets do better than others, your portfolio’s mix changes. This lets you sell high and buy low. It’s like a chance to fix your portfolio’s balance.

Every investor’s portfolio changes over time. What was once a 60/40 mix might now be 70/30. This happens when the stock market does well.

Setting clear rules for when to rebalance is key. Most pros use a ±5% rule for big asset classes. For example, if you want 40% in stocks, rebalance when it’s 45% or 35%.

INDUSTRY BEST PRACTICE:

Vanguard’s 2022 multi-asset study shows annual rebalancing outperforms quarterly and monthly schedules by 6–28 bps a year across most equity-bond mixes, while reducing transaction costs.Ref.: “Zhang, Y., Ahluwalia, H., & colleagues. (2022). Rational Rebalancing: An Analytical Approach to Multi-Asset Portfolio Rebalancing. Vanguard Research.” [!]

Look at your portfolio to see what made it perform well. Also, see how much it has changed. This helps you check if your investment goal time horizon is right.

“Rebalancing is one of the few free lunches in investing. It enforces a ‘buy low, sell high’ discipline without requiring market timing or forecasting skills.”

Frequent rebalancing can trigger unnecessary capital-gains taxes; RBC analysis shows that annual rebalancing with a 5 % tolerance band maximizes risk-adjusted returns while limiting taxable events.Ref.: “Hubbs, B. (2019). Strike a Balance: The Importance of Portfolio Rebalancing. RBC Portfolio Advisory Group.” [!]

Investors who rebalance based on rules do better than those who guess. Emotional rebalancing can lead to bad timing and missed chances.

Think about taxes before you rebalance. Selling some assets might cost more in taxes than it’s worth. For taxable accounts, try these tax-smart rebalancing tips:

- Put new money into underweighted areas

- Rebalance in tax-advantaged accounts first (401(k)s, IRAs)

- Use tax losses to offset gains

- Use income (dividends, interest) to build up underweighted areas

Review your contributions every year. If you’re not using tax-advantaged accounts fully, see how more contributions can help. Even a 1% increase can make a big difference over time.

Check your cash reserves too. Too much cash earning little interest might be better in your portfolio. But not enough cash can force you to sell when the market is down. Aim for a balance that’s both safe and efficient.

Write down your rebalancing rules to keep emotions out. I suggest making a simple table with:

| Asset Class | Target Allocation | Acceptable Range | Current Allocation | Action Required |

|---|---|---|---|---|

| Domestic Equities | 40% | 35-45% | 47% | Reduce by 7% |

| International Equities | 20% | 15-25% | 18% | No action |

| Fixed Income | 35% | 30-40% | 30% | Increase by 5% |

| Cash/Alternatives | 5% | 3-7% | 5% | No action |

Rebalancing rules can vary by goal. Retirement portfolios often need regular rebalancing to keep risk in check. But college funds might need to reduce risk as the college date gets closer.

For tax efficiency, think about where to put different investments. Tax-inefficient ones like high-yield bonds or REITs go in tax-advantaged accounts. Tax-efficient ones like index funds are better in taxable accounts.

By rebalancing and adjusting contributions, you stay disciplined. This helps you make the most of your investments. It keeps your portfolio balanced with domestic and international markets, matching your long-term plan.

To delve into the basics of investment goal planning, check out Investment Goal Planning Basics for Beginner Investors.

Record Decisions In Investment Policy Statement

After your annual review, update your investment plan in your Investment Policy Statement. This document is key to guiding your portfolio. It helps you make smart choices, even when markets are tough.

Your IPS turns your investment goals into clear rules. It helps you stay focused, even when markets change. After your review, write down any new goals or changes in your risk level.

Be detailed when you update your IPS. Talk about how much you want to invest, when you might take money out, and how you’ll handle taxes. This way, all parts of your investment plan work together well.

“An investment policy statement is to your portfolio what a constitution is to a government—it establishes the fundamental principles and structures that guide all decisions, even when times are tough or uncertain.”

Update Target Allocations And Benchmarks

When you update your IPS, focus on your asset class targets. You might say “U.S. Large Cap: 25% target, 20-30% acceptable range.” This helps you stay on track with your investments.

Choose benchmarks for each asset class and your whole portfolio. This helps you see if your investments are doing well. It stops you from making quick changes that might not be needed.

| Asset Class | Target Allocation | Acceptable Range | Benchmark | Review Trigger |

|---|---|---|---|---|

| U.S. Large Cap | 25% | 20-30% | S&P 500 | ±7% from target |

| U.S. Small Cap | 15% | 10-20% | Russell 2000 | ±5% from target |

| International Developed | 20% | 15-25% | MSCI EAFE | ±5% from target |

| Fixed Income | 35% | 30-40% | Bloomberg Agg | ±7% from target |

| Cash | 5% | 2-10% | T-Bill 90-day | Below 2% |

Write down any special investment moves with clear reasons to stop them. This keeps your portfolio focused. For example, if you’re holding more cash than usual, say when you’ll start investing again.

Update your rules for picking investments. This might include things like how much a fund costs or the experience of its managers. These rules help you make choices that fit your goals.

If you work with a registered investment adviser or financial advisor, review your IPS with them. This makes sure you’re both on the same page. Advisors say this helps keep things clear and fair.

Keep your updated IPS with your other important financial papers. Share it with family or your financial team. This is very helpful during big life changes or market ups and downs.

For a comprehensive guide:

- How to Review Your Investment Goals Annually.

- How to Adjust Investment Goals Over Time.

- How to Set Realistic Investment Goals Successfully.

Set Reminders For Next Annual Review

Don’t forget to follow up on your investment review. Mark a date on your calendar for your next check-up. It should be at least once a year.

Choose a time each year that works for you. Maybe after taxes or on your birthday. This way, you can see how your money is doing.

Also, have quick checks every few months. Spend 15-30 minutes reviewing your progress. Studies say these short meetings are just. They catch issues early but don’t feel rushed.

Life changes mean you need to check your investments more often. Things like a new job, getting money, or getting married. Also, big changes in the market (±20%) need a closer look.

Keep an eye on a few important numbers each month. This simple system helps you stay in touch with your investments. It’s not about daily changes but keeping an eye on the big picture.

If you have a financial advisor, meet with them halfway through the year. This helps make sure you’re on track with your plans. It’s a smart way to manage your money, with help when you need it.

{kind=link}