Setting goals for investing is key to financial success. I’ve helped investors for 12 years. I’ve seen how big the gap can be between what they want and what happens.

Did you know 93.5% of people stop trying to reach their money goals within six months? Most quit by February. Warren Buffett said, “The stock market is a way to move money from impatient people to patient ones.”

I worked with someone who wanted 30% returns every year. They thought about crypto millionaires. But I showed them that even pros only get 7-10% on average. By setting smart goals, they built a lot of wealth.

How we set our goals can make a big difference. Research shows that 65% of Americans with clear goals do better than those without.

Since 1957 the S&P 500 has delivered an average annual return of 10.33 %, providing a realistic long-run benchmark for growth-oriented portfolios.Ref.: “Maverick, J. B. (2025). S&P 500 Average Returns and Historical Performance. Investopedia.” [!]

Quick hits:

- Match timeframes to appropriate return expectations

- Break big objectives into smaller milestones

- Consider your personal risk tolerance

- Track specific metrics, not vague hopes

- Adjust strategies as market conditions change

Defining Realistic and Unrealistic Goal Traits

Knowing the difference between realistic and unrealistic goals is key. It’s about understanding what makes a goal doable versus a dream. Over the years, I’ve seen that good goals lead to success, not just luck.

Good goals are clear and match your financial situation. They’re not just about wanting something. It’s about making a plan you can follow.

Bad goals lead to disappointment and give up on plans. Learning to spot the difference saves time, money, and stress. It’s the first step in your investment journey.

Quantifiable Time Bound Target Requirements

Good investment goals have a few key traits. They must have specific numbers and a deadline. For example, “I want to save $50,000 for an emergency” is clear, not “I want to save more money.”

Goals also need a time frame. Realistic goals have a deadline that’s not too tight. “I want to save $12,000 for a down payment in 24 months” is specific.

Goals must also fit your current financial situation. They should consider your income, assets, and the market. This makes your goals realistic, not limiting your dreams.

Lastly, good goals are measurable. You should be able to track your progress regularly. This helps you make changes when needed.

Speculative Undefined Wish List Indicators

Unrealistic goals often have warning signs. Vague language is a big red flag. Goals like “getting rich through investing” are too vague.

Goals with unrealistic timelines are another problem. The stock market usually returns about 10% a year before inflation. Goals like “double my money in six months” ignore this.

Unrealistic goals often rely on exceptions, not averages. While some investors get amazing returns, expecting this is not realistic.

Goals that rely on things you can’t control are also unrealistic. “I’ll retire when Tesla stock hits $5,000” is too dependent on one company.

| Characteristic | Realistic Goals | Unrealistic Goals |

|---|---|---|

| Specificity | Precise numbers and targets | Vague aspirations without metrics |

| Timeframe | Reasonable deadlines based on market norms | Aggressive timelines disconnected from reality |

| Foundation | Based on historical averages and personal capacity | Based on exceptional cases or market anomalies |

| Control | Primarily dependent on your actions | Heavily reliant on external factors |

| Flexibility | Includes room for adjustment and learning | Rigid expectations with no contingency plans |

Setting smaller goals that lead to bigger ones is often better. It builds momentum and keeps you motivated. The best investors break big goals into smaller steps.

Field research found that writing goals, outlining action steps, and sending weekly updates to an accountability partner boosted achievement rates to 76 %, versus 43 % for unwritten goals.Ref.: “Michigan State University Extension. (2014). Achieving Your Goals: An Evidence-Based Approach.” [!]

Remember, realistic doesn’t mean easy. Challenging goals can help you grow, but they must be possible. The best goals are those that challenge you but stay within reach.

“Related Articles: How to Adjust Investment Goals Over Time”

Matching Resources to Desired Goal Scope

Investors should match their goals with what they can afford. Many beginners set goals that are too high. Your current money situation sets limits on what you can achieve.

Investing is like building a house. You can’t build a big house on a small budget. Your goals must fit your money, time, and how well you can handle market ups and downs.

Before you start investing, know what you have. Look at your income, savings, debts, and expenses. These help decide how much you can invest without hurting your finances.

Capital Constraints and Risk Capacity

Capital limits help you know what’s possible. I help new investors count how much they can invest. This includes money for emergencies and other important needs.

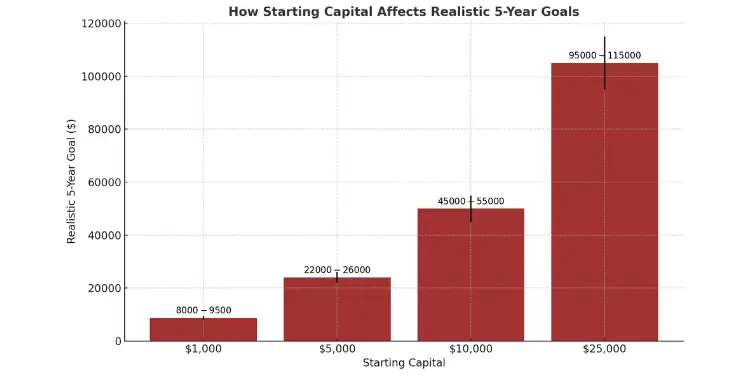

Where you start affects what you can do. A 25-year-old with $1,000 can’t do the same as someone at 45 with $50,000. Here’s how different starts affect 5-year goals:

| Starting Capital | Monthly Contribution | Time Horizon | Risk Capacity | Realistic 5-Year Goal |

|---|---|---|---|---|

| $1,000 | $100 | 5 years | Low | $8,000-$9,500 |

| $5,000 | $250 | 5 years | Medium | $22,000-$26,000 |

| $10,000 | $500 | 5 years | Medium | $45,000-$55,000 |

| $25,000 | $1,000 | 5 years | High | $95,000-$115,000 |

Risk capacity is about how much you can lose. It’s not just about how you feel about risks. Someone with a lot of savings can take more risks than someone with little money.

To figure out what you might earn, use this formula:

Future Value = Starting Capital + (Monthly Contributions × Months) + Investment Returns

The returns depend on how risky your investments are. Safe choices might earn 3-5% a year. Riskier ones might earn 7-10%, but they can also lose a lot.

Always put money into tax-advantaged accounts first. This helps your money grow more. Many beginners miss this and lose a lot of money.

As you make more money, you can set bigger goals. Start small and build up. Success early on helps you aim higher later.

Remember, limits help you focus on what’s possible. Working within these limits helps you make steady progress, not get stuck chasing dreams that are too big.

Typical Beginner Goals Stretching Reality

New investors often set goals that are too high for the market. After 12 years of helping investors, I’ve seen many unrealistic goals. These goals can lead to disappointment.

Many dream of making money fast, but this is often unrealistic. I’ve seen many new clients with big dreams. Their goals seem too good to be true.

The High Return/Low Risk Paradox

Many think they can get high returns without risk. A client wanted 15% return without risk. This shows a big misunderstanding of risk and reward.

The S&P 500 has averaged 10% return before inflation over time. Wanting more without risk is not smart. Investments promising high returns without risk often hide risks.

The Market Timing Fantasy

Some dream of timing the market perfectly. A client wanted to wait for the next crash to invest. This sounds smart but is hard to do.

Even pros rarely time the market right. Missing just 10 best days in 20 years can halve your returns. Being in the market is more important than timing.

The “Best Investment” Hunt

Many think they can pick the next big winner. This ignores how hard it is to beat the market. Markets are efficient, making it tough to outperform.

- Expecting to find “the next Amazon” regularly

- Planning to outperform market averages every year

- Believing you can consistently pick winning sectors

- Assuming you’ll avoid all market downturns

Even pros struggle to beat the market. A better plan is to build a diversified portfolio that matches your goals.

The Quick Income Replacement Dream

Many want to make money fast to replace their salary. One client wanted $5,000 monthly from $50,000. This is a 120% return.

This goal is unrealistic. It needs either high risk or a lot of time. A better plan is to start small and grow your investments slowly.

“You Might Also Like: Best Investment Goal Tracking Apps for Beginners”

The “Buy a Car” Timeline Mismatch

Short-term goals like buying a car soon are often unrealistic. High-risk investments can ruin your plans if they don’t work out.

I tell clients to match their investments to their goals. Short-term money should be in safe, liquid options. Long-term goals can handle more risk for growth.

Unrealistic goals come from optimism, not ignorance. The goal is to set realistic goals that match the market. By understanding these pitfalls, beginners can aim high without risking too much.

Blueprint for Crafting Realistic Objectives

Setting investment goals needs a clear plan. Many investors aim too high without a solid plan. The right method makes a big difference.

Good goals are both challenging and possible. You need a plan and a check against past results. This makes a roadmap for your financial future.

SMART Method Aligns Investment Milestones

The SMART method makes vague wishes clear. It’s great for financial goals because it’s precise.

Let’s see how each part helps your investment journey:

- Specific: Say “I want to grow my money” becomes “I aim to build a $50,000 emergency fund.”

- Measurable: Use clear numbers like “10% portfolio growth” instead of “significant returns.”

- Achievable: Set goals that challenge you but are not too hard.

- Relevant: Make sure each goal aligns with your values and your financial plan.

- Time-bound: Set deadlines that create urgency but are realistic.

For example, “I want to retire comfortably” turns into “I will save $1.2 million by age 65 with $1,500 monthly and 7% return.” This is a clear plan, not just a wish.

“The gap between dreams and achievement is action with structure. SMART goals aren’t just about setting targets—they’re about creating the pathway to reach them.”

To start, make a template for each goal:

| SMART Element | Your Goal Details | Questions to Answer |

|---|---|---|

| Specific | [Your exact target] | What precisely do you want to accomplish? |

| Measurable | [Your metrics] | How will you track progress? |

| Achievable | [Reality check] | Is this doable given your resources? |

| Relevant | [Purpose alignment] | Why does this matter to your overall plan? |

| Time-bound | [Deadline] | When will you reach this milestone? |

Break big goals into smaller steps. This boosts motivation with small wins. Celebrate each $100,000 milestone in your portfolio. These small victories make the journey more fun.

“Discover More: Realistic vs Unrealistic Investment Goals for Beginners”

Backtesting Returns Against Market History

Even the best plans need a reality check. Backtesting compares your goals to past market results. It shows if your goals are ambitious but realistic.

You don’t need fancy software for basic backtesting. Just follow these steps:

- Set your target annual return (e.g., 8%).

- Look up historical returns for your investment mix.

- Compare your goal to past results.

- Adjust your goals if they’re too high.

For example, aiming for 12% returns with a conservative portfolio is too high. But expecting 4% from a risky stock portfolio might be too low.

Remember to consider important factors when backtesting:

- Inflation’s effect on real returns.

- Investment fees and taxes that lower your returns.

- Different market times (bull vs. bear).

- The time period you’re looking at.

Use online tools from trusted financial sites as a benchmark for past performance. These tools show how different investments have done over time. They help set realistic goals.

“The best use of history is not to be bound by it, but to be informed by it. Past performance won’t predict your future exactly, but it sets reasonable boundaries for what’s possible.”

The best thing about backtesting is the range of possibilities it gives you. This range helps set goals that are exciting but also possible.

Get expert advice when looking at past data, if you’re new to investing. Financial advisors can help understand which past periods are most relevant to today and your situation.

The best way to set realistic investment goals is to mix SMART goals with backtesting. This method creates goals that are inspiring and reachable. It lets you enjoy the journey while making progress toward your financial dreams.

“Further Reading: How to Set Realistic Investment Goals Successfully”

Tracking Progress and Resetting Expectations

Setting goals is just the start. Keeping track and managing expectations are key to success. Many investors start strong but give up when the market changes.

Markets and personal lives change. Your first plans might not always work. Beginners should track their progress closely to avoid mistakes.

Tracking helps you stay focused on your goals. It’s easier to make smart changes when you see your progress clearly.

“Related Topics: Free Investment Goal Setting Worksheet for Beginners”

Quarterly Reviews and Threshold Triggers

Beginners should review their investments every quarter. This keeps you on track without getting too stressed. It’s a good balance of watching and waiting.

FINRA urges investors to perform at least an annual portfolio review to catch allocation drift and rebalance; neglecting this step can quietly derail progress toward stated goals.Ref.: “Financial Industry Regulatory Authority (FINRA). (2024). Evaluating Performance.” [!]

Start with simple questions in your reviews. This helps you build a good habit. As you get more experience, you can ask more detailed questions.

| Review Element | Key Questions | Action Threshold | Adjustment Strategy |

|---|---|---|---|

| Performance Tracking | Is my portfolio return within 5% of my target? | ±10% deviation from expected return | Rebalance or reassess asset allocation |

| Goal Alignment | Have my financial priorities changed? | Major life events (marriage, children, job change) | Revise timeline or return expectations |

| Risk Assessment | Am I comfortable with recent volatility? | Losing sleep or checking accounts daily | Adjust risk profile or investment mix |

| Contribution Rate | Can I increase my investment amounts? | Income increase of 5% or more | Boost regular contributions by 1-2% |

Also, set “threshold triggers” for big changes. These are like early warnings for your strategy. For example, check your goals if your performance drops by 20% or if you have big life changes.

Changing your goals is normal. It’s part of learning and growing. Warren Buffett said, “The most important quality for an investor is temperament, not intellect.”

When checking your goals, know the difference between normal changes and big problems. A 5% market drop is normal, but steady losses mean you need to rethink your strategy.

When you need to adjust your investment goals, don’t do it in isolation. Share your thinking with a trusted advisor or knowledgeable friend who can provide perspective on whether your changes are reactive or strategic.

Talk about changing your goals with important people. This keeps you accountable and flexible. For example: “Based on the last two quarters’ performance, I’m extending our timeline by one year to reduce pressure on our risk profile.”

Keep a record of your reviews. This helps you see patterns in your investing. Many beginners learn to avoid overreacting or being too optimistic.

By tracking and adjusting your goals, you make investing a steady journey. The basics are: set realistic goals, track regularly, and adjust wisely.

“For More Information:

Getting Feedback from Financial Mentors

Even the best plans need someone else’s view. Studies show 65% of people who share their goals with advisors do better than those who don’t.

Choosing the right person for advice is key. A good adviser knows your comfort with risk. They make sure your goals match your money situation. They ask about your emergency fund and retirement plans, not just to sell you something.

Potential feedback sources include:

• Professional financial planners (fee-only advisors have fewer conflicts)

• Investment club members

• Financially savvy family members

• Online communities focused on specific investment strategies

The best mentor cheers for your small wins and keeps you on track for the long haul. They help you know what’s possible and what’s just a dream, like short-term investment goals that need careful planning.

When you ask for advice, have specific questions ready. Be careful of anyone promising too much or ignoring your worries. The best mentors guide you but let you make your own choices.

Remember, feedback is to help, not to tell you what to do. By mixing your own research with advice from others, you’ll set goals that are both big and doable.

{kind=link}