Wedding insurance helps protect a big investment in life. When couples plan their big day, they often forget about unexpected problems. What if your venue closes or bad weather forces a delay?

The average American wedding costs $28,000. But, only about 30% of couples get insurance to protect against disasters. One of my clients said, “The policy cost us less than our cake, but saved our entire celebration.”

I’ve helped many Idaho couples with their insurance choices. Wedding coverage is like a safety net. It protects against damage, no-show vendors, and sickness without costing too much.

Most couples think it’s worth it. It costs only 1-2% of your total budget. This gives you peace of mind during a stressful time.

Quick hits:

- Covers both ceremony and reception events

- Protects deposits from vendor bankruptcies

- Reimburses for weather-forced postponements

- Typically costs $200-$600 total

- Many venues now require liability coverage

What wedding insurance covers and why

Wedding insurance can save your big day from disaster. I’ve seen it help many couples in Idaho Falls. It covers things like venue fires and vendor bankruptcies.

It’s like a safety net for your wedding. Most couples spend $20,000 to $40,000 on their big day. But many forget to protect that investment.

The average couple spends over $30,000 on their wedding, making it one of the largest uninsured investments many people will ever make.

When people ask if wedding insurance is worth it, I say yes. It gives you peace of mind. Your venue might need some coverage, but you want more.

There are two main types of policies: liability and cancellation. You can get them together or separately. It depends on what you need.

Liability insurance helps with damage and injuries. For example, if someone gets hurt or breaks something, it helps pay for it. Policies start at $125 and offer $1-2 million in coverage.

More venues now ask for liability insurance. Last month, I helped a couple get the $1.5 million policy their venue needed. It protects both you and the venue.

Cancellation insurance helps if you have to cancel or postpone your wedding. It covers non-refundable payments. Policies cost between $75 and $160, based on your budget.

It covers things like bad weather, illness, and venue damage. It also covers vendor issues, but with some limits.

Last year, a couple’s outdoor wedding was saved by a cancellation policy. A storm was coming, but they rented a tent. It shows how insurance can help in unexpected situations.

Special event insurance is another term you might see. It’s like wedding insurance but for other big events too. Wedding policies often include extra protections for your dress, rings, and gifts.

| Policy Type | What It Covers | Typical Cost | When To Purchase | Coverage Limits |

|---|---|---|---|---|

| Liability Insurance | Property damage, bodily injury, alcohol-related incidents | $125-$275 | 1-3 months before wedding | $1-2 million |

| Cancellation Insurance | Non-refundable deposits, rescheduling costs, weather issues | $75-$350 | When making first deposits | Up to total wedding cost |

| Combined Coverage | Both liability and cancellation protections | $175-$550 | When booking venue | Customizable |

| Jewelry Rider | Engagement/wedding rings, ceremonial jewelry | $50-$125 additional | After purchasing rings | $2,000-$10,000 |

When you buy wedding insurance, timing is key. Get cancellation coverage early and liability insurance closer to your wedding. Most insurers give a 15% discount for both types together.

Always read what your policy covers before buying. Some policies don’t cover things like change of heart or pre-existing conditions. Knowing what’s not covered helps you choose the right policy.

Your insurance needs depend on your venue, budget, and how much risk you’re willing to take. A small wedding is different from a big one at a historic mansion.

Wedding insurance is a small price to pay for peace of mind. The right policy keeps your special day safe from surprises.

Event liability protection for venue damages

Event liability coverage is key when you’re planning your big day. It helps protect against damage to the venue. I’ve helped many couples in Idaho Falls find the right insurance. This coverage can save you thousands of dollars.

Many policies offer coverage from $500,000 to $5 million. The exact amount depends on your venue’s needs.

Venue damage can happen more often than you think. I’ve seen dancers damage marble floors and decorations mark historic walls. One couple had to pay $3,200 to fix a damaged wood paneling. Their insurance covered it, so they could enjoy their honeymoon without worry.

Event insurance helps with these damages. It covers repair costs that would come out of your pocket. Many venues now ask for proof of insurance before booking.

Guest Injury Medical Payment Provisions

Wedding liability insurance also covers guest injuries. It pays for minor injuries, up to $1,000 to $5,000 per person. This is true even if it’s not your fault.

Medical payment coverage is quick to act. It doesn’t need proof of fault. I remember a client whose guest fell at the reception. The $2,300 emergency bill was covered right away, avoiding awkward payment talks.

Common injuries include falls on the dance floor and allergic reactions. Your policy’s medical payment provision helps without hurting your budget.

Alcohol Service and Host Liquor Liability

Alcohol at your wedding adds big risks. Host liquor liability coverage protects you if a drunk guest causes damage or injuries. It’s part of many wedding insurance policies.

Alcohol-related incidents can cost a lot. Venues with open bars often need $1 million to $2 million in coverage. If you provide your own alcohol, you might need even more.

Standard homeowner’s policies don’t cover event alcohol. One couple I worked with faced a lawsuit over a drunk guest’s accident. Their insurance helped with legal costs and settlements, protecting their finances.

Choosing the right liability limits is important. Look at your venue’s needs, guest count, and event risks. Historic venues and outdoor events might need higher limits. Always check your venue contract for insurance requirements before buying your policy.

Cancellation coverage for unforeseen circumstances

Things don’t always go as planned, making cancellation coverage key. In my decade helping Idaho couples, I’ve seen how it saves money when the unexpected happens.

Wedding cancellation insurance helps pay back non-refundable costs if you have to cancel. It covers venue deposits, catering, and more. This way, you don’t lose thousands of dollars.

When disaster strikes, this coverage can help pay for a new wedding. It covers many reasons you might need to change your plans.

Weather Events and Natural Disasters

Extreme weather can force you to cancel your wedding. Last year, a Coeur d’Alene couple got $12,000 back after a wildfire. Their insurance paid for new venue costs.

Cancellation insurance covers:

- Hurricanes and tropical storms

- Blizzards and ice storms

- Flooding and water damage

- Wildfires and evacuations

- Earthquakes and structural damage

But you must buy it 14-15 days before the weather event. This way, you’re covered before a hurricane hits.

“Check This Out: Early lease termination clause helps exit without penalty”

Illness, Injury, and Military Deployment

Illness or military duty can also cancel your wedding. A Boise couple got their money back when the bride’s father had a heart attack. They postponed for three months.

Insurance helps when serious health issues or military duty affect your wedding:

- Serious illness requiring hospitalization

- Accidents and injuries

- Military deployment or reassignment

- Death in the immediate family

After my fiancé received unexpected military orders, our wedding insurance saved us from losing over $15,000 in deposits. We rescheduled six months later without any financial stress.

Venue and Vendor Issues

Venue closures and vendor problems are big issues. Cancellation coverage is key here. It helps cover costs of finding new vendors.

I helped a Twin Falls couple after their venue closed due to a fire. Their insurance paid for new venue costs.

| Cancellation Scenario | Typically Covered | Usually Excluded | Coverage Timing |

|---|---|---|---|

| Severe Weather | Hurricanes, blizzards, flooding | Light rain, normal seasonal conditions | Policy must be purchased 14+ days before event |

| Health Issues | Unexpected illness/injury requiring hospitalization | Pre-existing conditions, minor illness | Coverage effective immediately after purchase |

| Venue Problems | Bankruptcy, damage, closure | Venue aesthetic changes, management disputes | Coverage effective immediately after purchase |

| Vendor Failure | Bankruptcy, no-shows | Dissatisfaction with services provided | Coverage effective immediately after purchase |

Important Exclusions to Understand

While cancellation coverage is great, it’s not all-inclusive. Most policies don’t cover:

- Change of heart or cold feet

- Pre-existing medical conditions

- Known circumstances when you purchase the policy

- Normal seasonal weather (light rain or snow)

- Financial issues or budget changes

Standard event policies do not reimburse costs when a wedding is cancelled voluntarily (a “change of heart”). Couples must absorb all non-refundable expenses in such cases. Ref.: “National Association of Insurance Commissioners (2009). Event Insurance. NAIC.” [!]

Always read the exclusions carefully. Highlight them in your policy. Talk to your agent about any concerns before buying.

“Explore More: Why is health insurance important for everyone?”

Determining Your Coverage Limits

To figure out how much coverage you need, make a list of all non-refundable costs. Add these up to find your total risk:

- Venue deposits and final payments

- Catering and bar service commitments

- Photography and videography contracts

- Entertainment and music deposits

- Floral arrangements and decorations

- Attire alterations and deposits

- Transportation reservations

This total is the minimum coverage you should aim for. Most couples in Idaho need $15,000-$30,000.

Additional Benefits Worth Considering

Many policies offer extras beyond basic coverage. These extras can make your coverage even better:

- Rescheduling cost coverage for new invitations and announcements

- Photography/videography reshoot expenses

- Professional counseling if you experience emotional distress

- Travel arrangement change fees

- Honeymoon coverage if cancellation affects travel plans

When comparing policies, look for these extras. They can make a big difference in your coverage.

Timing Your Purchase Wisely

Buy cancellation coverage as soon as you start making deposits. This gives you the most protection. Most couples buy it 9-12 months before their wedding.

Buying early is key for weather-related coverage. Most insurers need you to buy 15 days before a weather event to cover it.

Wedding cancellation insurance costs $150-$550. It’s a small part of your wedding budget but offers big peace of mind.

“Related Articles: Why is car insurance important to have?”

Safeguarding attire rings and decor expenses

Protecting your wedding dress, rings, and decorations is key. These are big investments that need to be safe from start to finish. I’ve helped many couples in Idaho Falls with their insurance claims, giving them peace of mind.

Wedding attire coverage keeps your dress, tuxedo, and accessories safe. It starts when you buy them and goes until your wedding day. Policies usually offer $1,500 to $10,000 in coverage. Deductibles are low, making it easy to file a claim if needed.

Wedding ring insurance covers bands but not engagement rings. It’s important to know this when planning your insurance. A client once told me:

“I thought my engagement ring was covered by our wedding insurance. But it needed its own coverage through our homeowners policy, which could have saved us thousands.”

Wedding-insurance policies typically exclude engagement rings; they must be insured separately (e.g., a jewelry rider or standalone policy) to avoid coverage gaps. Ref.: “Fusaro, K. (2014). 1 Easy Way to Prevent 99 Percent of Winter Wedding Disasters. Glamour.” [!]

Ring coverage is for loss, damage, or theft from policy start to reception end. I’ve helped couples who found damage to their bands just before the ceremony. They were glad to have insurance.

Decor expenses also get protection. Your flowers, table settings, and more are usually covered against damage or loss. But, coverage limits vary. Most insurers have per-item caps and don’t cover very expensive items without extra riders.

| Item Category | Typical Coverage Range | Common Deductible | Coverage Period |

|---|---|---|---|

| Wedding Dress | $1,500-$10,000 | $25-$50 | Purchase to ceremony end |

| Wedding Bands | $1,000-$5,000 | $50-$100 | Policy purchase to reception end |

| Decorations | $1,000-$7,500 | $50-$100 | 48 hours before to event end |

Good documentation is key for successful claims. Here’s how to protect your investment:

- Keep all receipts for attire, rings, and décor in both digital and physical formats

- Take clear photographs of all items, showing unique features or craftsmanship

- Create a detailed inventory with descriptions and values of each covered item

- Store documentation in multiple locations, including with your insurance policy

When choosing coverage, calculate the full replacement value of your items. Don’t use what you paid. Add 15-20% for price increases or rush fees.

Timing is important with this coverage. Attire coverage starts at purchase, while décor starts 48 hours before your event. Knowing these times ensures you’re protected when it counts. I’ve seen couples assume coverage started earlier, only to find a gap when problems happened.

“You Might Also Like: Clear purpose of condo insurance for every condominium unit owner”

Vendor failure reimbursement and rescheduling help

A wedding insurance policy helps protect against common wedding day problems. In my decade helping Idaho couples, I’ve seen vendor issues cause nearly 40% of all claims. It’s clear why wedding insurance is important when your photographer doesn’t show up or your venue closes.

Vendor failure coverage helps when businesses don’t deliver services you’ve paid for. This is more common than you think. Photographer and videographer issues are a big part of claims, followed by venue closures and DJ no-shows.

If your photographer doesn’t show up, insurance can help. It will reimburse your lost deposit and cover the cost of a new photographer. This can save you thousands of dollars during a stressful time.

“Discover More: Essential purpose of flood insurance for protecting vulnerable property”

Deposits Lost to Bankruptcy Coverage Details

When vendors go bankrupt or close before your wedding, your deposits are often lost. But with the right insurance, you can get them back. Wedding insurance covers deposits up to policy limits if businesses close.

To file a claim for lost deposits, you need:

- A signed contract with the vendor

- Proof of payment (receipts or bank statements)

- Documentation of the vendor’s bankruptcy or closure

- Evidence that you tried to get your deposit back

While no couple wants to think about vendor failures, it’s wise to take precautions. Check online reviews, verify licenses, and ask for references before signing. But even good vendors can face financial troubles. That’s why wedding cancellation insurance is key.

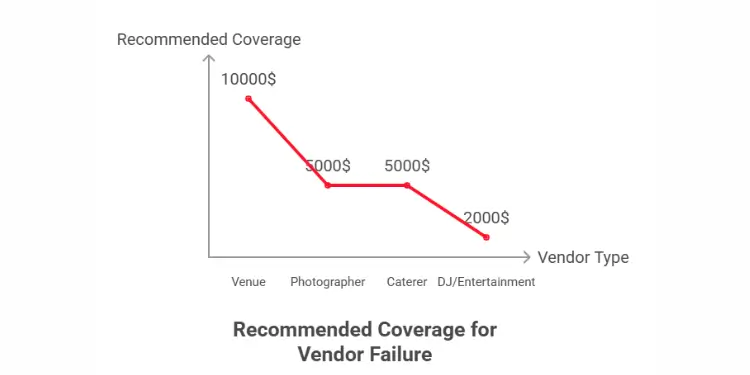

Coverage for vendor failure usually ranges from $1,000 to $10,000 per vendor. Make sure your policy limits match your biggest deposits, like venues and photographers.

| Vendor Type | Average Deposit | Claim Frequency | Recommended Coverage |

|---|---|---|---|

| Venue | $3,000-$10,000 | High | $10,000 |

| Photographer | $1,000-$3,000 | Very High | $5,000 |

| Caterer | $1,000-$5,000 | Medium | $5,000 |

| DJ/Entertainment | $500-$2,000 | Medium | $2,000 |

Wedding insurance also helps with rescheduling if you need to postpone. It covers costs for:

- Reprinting and resending invitations

- Notifying guests of changes

- Securing new vendors (often at higher rates)

- Rescheduling fees for other vendors

For beginners, knowing wedding insurance covers cancellation and vendor failure is reassuring. The small premium cost can save thousands of dollars in deposits and payments.

Remember, timing is key. Buy your policy early for the best protection. Most policies cover deposits made after the policy starts, so get insurance before big payments.

“Read More:

Wedding insurance premium costs and savings

Wedding insurance costs change a lot based on what you need. Basic plans start at $100. But, full coverage that includes both liability and cancellation can cost up to $1,000. Most couples in Idaho pay $200-$500 for a wedding with 100-150 guests.

Four main things affect how much you pay:

1. Guest count – More guests mean higher risk

2. Coverage limits – More protection costs more

3. Wedding location – Destination weddings cost more to insure

4. Special activities – Things like alcohol or fireworks raise rates

Couples can save money without losing protection. Getting both liability and cancellation coverage can save 15%. Changing your deductible can also lower costs while keeping your wedding safe.

The best time to buy wedding insurance is when you start making deposits. This is up to 24 months before your wedding. It makes sure your policy covers the whole planning time. This is important because vendors can go bankrupt or venues can change hands.

Wedding insurance protects your big day from unexpected problems. For couples spending $15,000+ on their wedding, a $300 insurance policy is worth it. It gives peace of mind for a small part of your budget.

{kind=link}