Vision insurance is primarily intended to help make eye care affordable. It uses regular payments instead of health insurance and covers eye exams, glasses, and some eye surgeries.

Many people in the U.S. have trouble with eye costs, even with health insurance. Did you know 79% of U.S. adults need vision correction? Yet, they often pay for it themselves.

Dr. Martinez says, “Eye care is not just for seeing well. It’s also about your health.”

In my 10 years helping Idaho families, I’ve seen how good eye care plans help. They save money, mainly when glasses or contacts change. Plans cost $5-35 a month and can save hundreds a year.

Eye care plans work by getting lower prices from doctors. This makes visits and glasses cheaper than buying them at full price.

Quick hits:

- Detects health issues beyond eye problems

- Saves money on prescription eyewear

- Offers discounts on LASIK procedures

- Costs less than weekly coffee

- Complements your existing health insurance

Vision Insurance Basics and Core Purpose

Vision insurance is a special safety net for eye care costs. It helps keep your eyes healthy. Many people think their health insurance covers eye care, but it often doesn’t.

These plans cost $10-30 a month. They are cheaper than health insurance. You pay a little each month to cover eye care costs.

Vision insurance helps with costs that most people will face. Here are some common needs:

- Annual or bi-annual eye exams

- Prescription glasses and frames

- Contact lenses and fitting services

- Vision correction procedures (partial coverage in some plans)

- Discounts on non-covered services

These plans focus on prevention and maintenance. They are not for unexpected medical issues. This is why vision care is a separate insurance type.

“Explore More: What is the purpose of an insurance policy explained and why coverage matters“

Separate from General Health Coverage

Health insurance covers unexpected medical needs. It includes serious eye problems like glaucoma or cataracts. But, it usually doesn’t cover routine eye care.

This separation makes sense. Health insurance is for big, unexpected costs. Vision care is for regular, needed services.

Today, there are two main vision coverage types:

| Coverage Type | How It Works | Best For | Typical Cost |

|---|---|---|---|

| Vision Insurance Plans | Fixed benefits for specific services with copays | Regular glasses/contacts users | $150-250 annually |

| Vision Discount Plans | Reduced rates at participating providers | Occasional vision services | $75-100 annually |

| Vision Benefits in Health Plans | Limited coverage within health insurance | Basic preventive care only | Included in health premium |

Many people don’t know Medicare doesn’t cover eye exams, glasses, or contacts. Vision insurance fills this gap for seniors.

Vision benefits are different from medical coverage. Vision plans offer scheduled benefits for routine services. They are more predictable but limited.

Knowing the difference helps you understand why you might need both. Health insurance covers eye diseases and injuries. Vision insurance covers routine eye care.

“For More Information: What is the purpose of gap insurance explained for drivers with loan balances“

Key Coverages: Glasses, Exams and Lenses

Vision insurance plans cover eye exams, glasses, and contact lenses. Knowing these basics helps you choose the right plan. This way, you won’t pay too much for things you don’t need.

Eye exams are key to good vision care. They check your eyes every year or two. These exams look for diseases like glaucoma and cataracts early on.

Most vision plans pay for these exams. Without insurance, you might spend $150-$200. Even basic plans cover one exam a year, which is a big plus.

The national average out-of-pocket cost for a routine eye exam is about $200, meaning a single visit can exceed a full year of basic-tier vision-plan premiums.Ref.: “NVISION Centers. (2024). Getting an Eye Exam Without Insurance: What to Expect. NVISION.” [!]

For glasses, plans offer money for frames and basic lenses. You might get $100-$200 for frames. But, designer frames cost more. Plans cover single-vision lenses but charge extra for progressive or bifocal ones.

Contact lens plans work differently. They give money for your yearly contacts. This money usually covers the cost of contacts and the fitting fee, which can be $50-$100 without insurance.

Some plans also offer discounts on lens enhancements. These can include:

- Anti-glare coatings (normally $50-$100)

- Scratch-resistant treatments (normally $15-$30)

- Photochromic lenses that darken in sunlight (normally $100-$150)

- High-index lenses for stronger prescriptions (normally $60-$120)

How much you save depends on your vision needs. If you wear glasses with many enhancements or need many contacts, you’ll save a lot. But, if you don’t need much correction, your savings will be less.

| Vision Service | Typical Retail Cost | With Basic Plan | With Premium Plan |

|---|---|---|---|

| Comprehensive Eye Exam | $150-$200 | $10-$25 copay | $0-$10 copay |

| Standard Frames | $150-$250 | $100-$130 allowance | $150-$200 allowance |

| Basic Single-Vision Lenses | $80-$120 | $25 copay | $10 copay or $0 |

| Annual Contact Supply | $200-$300 | $120 allowance | $150-$200 allowance |

| Lens Enhancements | $50-$200+ | 20-30% discount | 40-60% discount |

Don’t forget about how often you can get these services. Most plans cover one exam a year. But, you might only get new frames every 24 months. Lenses and contacts can be replaced every 12 months, when your prescription changes.

When looking at vision insurance, think about your specific needs. If you wear contacts, find plans with good contact allowances. Don’t worry about frame coverage if you don’t use it.

For families, vision insurance can save a lot of money. A family of four could save $1,000 or more a year. This is true, even more so if kids need new glasses often as their vision changes.

Remember, vision insurance is for routine care, not medical eye treatment. If you get an eye infection or injury, your regular health insurance will cover it. Vision insurance is for keeping your eyes healthy through exams and glasses.

Current market offerings show individual premiums starting near $5–$8 per month and rising to roughly $30–$45 for family or premium tiers, based on EyeMed and VSP plan comparisons.Ref.: “NVISION Centers. (2025). EyeMed vs. VSP: Compare Vision Insurance Plans & Benefits. NVISION.” [!]

“You Might Also Like: Should I use 50/30/20 budget versus other personal budgeting styles“

When Vision Plans Deliver Real Value

Many Americans with regular vision needs find vision plans helpful. They can save a lot on eye care. Over a decade, I’ve seen how they help some people a lot.

Vision insurance is best for those needing yearly eye exams and new glasses or contacts. These costs add up fast. A single eye exam can cost $150-$300 without insurance. Glasses and lenses can cost over $300.

The savings are big in certain situations:

Family Coverage Advantages

Families with many members needing vision correction save a lot. When three or four family members need exams and glasses or contacts, the savings grow.

Many parents were unsure about vision care insurance at first. But they saved over $600 a year for their whole family.

Specialty Vision Needs

Those needing special lenses or frequent prescription changes save a lot. Vision plans often cover a big part of these costs. This includes things like progressive lenses and anti-glare coatings.

People with strong prescriptions or special needs find insurance helps a lot. It makes thin lenses and special treatments more affordable.

“The average American family spends $1,056 annually on routine vision care when paying out-of-pocket, but only $358 when utilizing comprehensive vision benefits.”

Hereditary Conditions Requiring Monitoring

Family history of eye diseases means regular checks are key. Vision insurance makes these exams cheaper. It helps catch serious problems early.

Preventive care is cheap compared to treating advanced eye problems later.

Calculating Your Savings

To see if vision insurance is worth it, compare your costs to the premiums. Here’s a simple table:

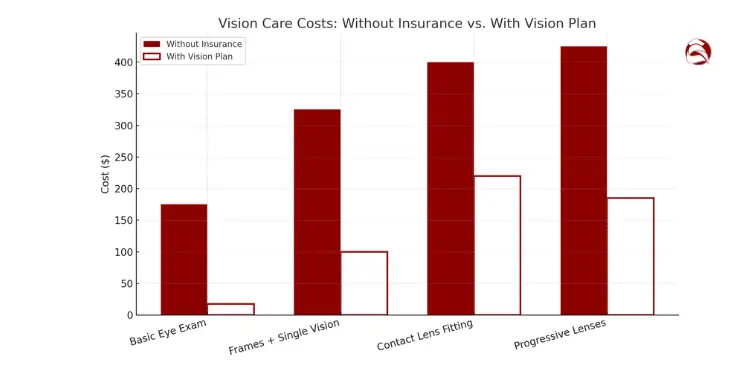

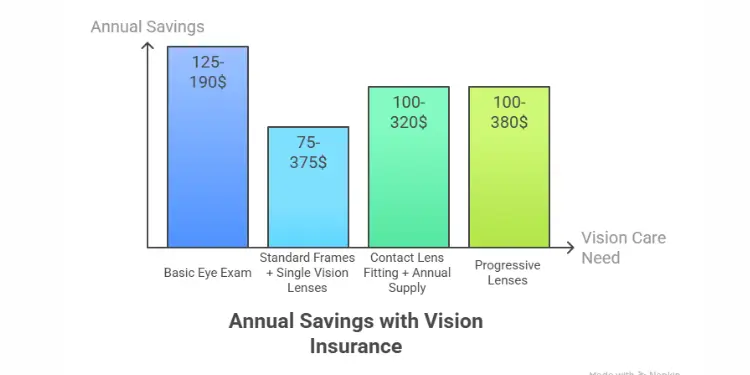

| Vision Care Need | Typical Cost Without Insurance | Cost With Vision Plan | Annual Savings |

|---|---|---|---|

| Basic Eye Exam | $150-$200 | $10-$25 copay | $125-$190 |

| Standard Frames + Single Vision Lenses | $250-$400 | $25 copay + $0-$150 | $75-$375 |

| Contact Lens Fitting + Annual Supply | $300-$500 | $60 copay + $120-$200 | $100-$320 |

| Progressive Lenses | $350-$500 additional | $120-$250 additional | $100-$380 |

When Vision Plans May Not Be Worth It

Vision insurance isn’t for everyone. If you rarely need new glasses or contacts, it might not be worth it. The premiums could be more than you save.

I’ve told clients with stable vision to save money for glasses instead of getting insurance. If you only need reading glasses, you won’t save much.

Decision Framework

Ask yourself these questions to decide if vision insurance is right for you:

- Do you or family members need yearly eye exams?

- Do you replace glasses or contacts at least once every two years?

- Do you require specialty lenses or treatments?

- Does your family have a history of eye conditions requiring monitoring?

- Would you be more likely to get recommended eye care if costs were reduced?

If you answered yes to two or more questions, a vision plan could save you money.

Remember, vision plans often have limits. They usually cover one exam and either glasses OR contacts per year. If you need both, consider this when deciding.

Vision insurance works best when you use all the benefits. Many people miss out on savings by not using their full frame allowance or skipping annual exams.

Premium Factors: Copays and Allowance Caps

Vision coverage’s value comes from premiums, copays, and allowances. I’ve helped families with insurance for over a decade. Knowing these parts helps decide if vision insurance is right for you.

Vision insurance plans cost $5-$35 a month. The price changes based on coverage levels. Your premium keeps your policy active, but it’s just the start of your vision care costs.

Copays are fixed amounts you pay for services. Most plans charge $10-$25 for eye exams and $25-$40 for frames or lenses. These fees make your costs easier to handle.

Allowances are often misunderstood. Your insurance lowers the cost of frames, lenses, or contacts up to a certain dollar limit. For example, a $150 frame allowance means you pay nothing for frames up to that price. For more expensive frames, you pay the difference.

| Cost Component | Typical Range | What It Covers | Your Responsibility |

|---|---|---|---|

| Monthly Premium | $5-$35 | Basic plan access | Full premium amount |

| Exam Copay | $10-$25 | Comprehensive eye exam | Copay amount only |

| Materials Copay | $25-$40 | Basic frames/lenses | Copay plus costs above allowance |

| Frame Allowance | $100-$200 | Frame selection | Costs exceeding allowance |

Frequency Limits for Exam Benefits

Vision insurance covers services on a schedule, not on-demand. Most plans limit how often you can use benefits. This affects the value of your coverage.

Standard vision plans cover one eye exam every 12 months. This matches eye health advice for most adults. Frame coverage usually refreshes every 24 months, and lens replacements are available every 12-24 months.

These limits are important. They decide when your insurance covers new eyewear. If you change glasses every year but your plan only covers frames every two years, you’ll pay full price in the off years.

Contact lens benefits usually replace every 12 months. Most plans offer contacts or glasses within a benefit period—not both. Vision insurance provides predictable coverage on this schedule, not for emergencies or as-needed care.

“Related Articles: What is zero paycheck budget and why irregular earners need it“

Frame and Lens Upgrade Costs

Basic vision coverage includes standard lenses and frames up to your allowance. But, many people need or want upgrades that cost extra.

While insurance lowers the cost of basic options, premium features cost more. Common upgrades include:

- Progressive lenses: $50-$175 additional

- Anti-glare coatings: $40-$90 additional

- Photochromic lenses: $70-$150 additional

- High-index (thinner) lenses: $60-$120 additional

Let’s say you have a plan with a $150 frame allowance and a $25 materials copay. A pair of basic glasses with frames priced at $200 would cost you $75 out-of-pocket. Add progressive lenses ($120) and anti-glare coating ($60), and your total is $255.

This example shows why knowing what your vision coverage includes is key. Vision insurance doesn’t eliminate all costs. It makes them more predictable and generally lower than retail prices.

When looking at plans, focus on how they handle lens upgrades. Some premium plans offer higher allowances or discounts on enhancements. This can save a lot if you need specialized lenses.

Selecting the Right Vision Provider Network

When looking at vision insurance, the provider network is key. It can save you a lot of money. Vision insurance is different from health insurance. It affects where you can go for eye care.

Vision plans work with specific eye doctors and stores. This helps keep your costs down. Staying in-network means your plan works best. Going out-of-network can make your costs much higher.

For example, an eye exam might cost $10 with an in-network doctor. But it could be $150 or more without network discounts. Some plans help a bit with out-of-network costs, but it’s not as good.

“Discover More: What is zero-based budgeting and why beginners gain control fast“

Checking Participating Optometrists and Retailers

Before picking a vision plan, do these things:

- Make a list of your favorite eye doctors and stores

- Check the insurance company’s website for providers

- Call your doctors to see if they accept your plan

- See if big stores like LensCrafters or Walmart Vision Center are in the network

- Find out when the network list was last updated

Staying in-network matters—going out-of-network typically triggers higher out-of-pocket costs and requires manual claim submission, reducing overall savings.Ref.: “Vision Service Plan. (2021). Your Vision Coverage Works Overtime In-Network. VSP.” [!]

Not all vision services are covered the same way. I helped a client find out her plan covered frames at Walmart but better lenses at a local optometrist. Using both wisely saved her money.

If you need special eye care, check if specialists are in the network. Some plans don’t cover ophthalmologists or specialists for conditions like glaucoma or macular degeneration.

| Provider Type | Typical In-Network Benefit | Typical Out-of-Network Benefit | Potential Cost Difference |

|---|---|---|---|

| Chain Retailers | Full coverage after copay | Partial reimbursement | $50-150 more out-of-pocket |

| Independent Optometrists | Full coverage after copay | Partial reimbursement | $75-200 more out-of-pocket |

| Specialty Eye Care | Discounted services | Little to no coverage | $100-300+ more out-of-pocket |

Provider networks can change. A doctor might not be in-network anymore. Always check before making appointments.

Going out-of-network can make eye care very expensive. A $20 exam might cost $150 without discounts. Frames and lenses can cost $300-500 without network savings.

Some plans have online tools to show savings at different providers. These tools help you see which plan is best for you.

“The most common complaint I hear from vision plan members isn’t about coverage limits—it’s about discovering too late that their favorite eye doctor doesn’t participate in their network.”

Think about convenience too. A plan with less benefits but more providers near you might be better. It’s about what works best for you.

“Read More:

- Why is health insurance important for everyone?“

- What is the purpose of Medicare supplement insurance?“

- Zero budgeting vs envelope budgeting: which method wins“

Next Steps for Obtaining Vision Coverage

Most people get vision insurance from their jobs. These plans are cheaper than buying your own. They help you save money on eye care and plan your vision health.

If you can’t get it through work, you have two choices:

1. Individual vision plans: Buy from companies like VSP, EyeMed, or Davis Vision. Some offer discounts if you add dental too. Vision insurance is all about eye care.

2. Vision discount programs: These aren’t insurance but give you lower prices at certain places. They cost less but don’t cover as much as insurance.

When looking at plans, check these things:

• How many providers are in the network

• How much you can spend on frames and contacts each year

• What you pay for exams and materials

• How often you can get services

• Prices for extra lens features like anti-glare

Choosing the right plan saves you money. If you wear glasses or contacts, a good plan can pay off. But if you just need check-ups, a basic plan or discount might be enough.

Think about how much you spend on eye care now. Then, see if a plan can save you money. The right plan keeps your eye care costs steady and your health on track.

{kind=link}