Professional liability insurance helps protect experts when things go wrong. Doctors, lawyers, and consultants face risks not covered by regular insurance. Have you ever thought about what happens if a mistake leads to a huge lawsuit?

Over 43% of U.S. service providers will face a claim in their career. These disputes can cost $54,000 in defense, even if there was no mistake.

“In today’s litigious world, experts need protection,” says the American Bar Association.

I’ve seen how special insurance helped a local accounting firm. A small tax error turned into a big problem. But their insurance covered legal costs and damages, saving them from financial disaster.

Professional liability insurance (PLI) is a claims-made liability product that indemnifies service providers against third-party financial losses arising from alleged negligence, errors, omissions, or breach of professional duty. Policies typically provide per-occurrence and aggregate limits (e.g., $1M/$3M), include defense cost provisions (inside or outside the limit), and exclude intentional acts, bodily injury, or regulatory fines. Coverage is triggered only when the claim is first made and reported during the policy period and relates to services rendered after the retroactive date.

Industries such as healthcare, legal, financial advisory, engineering, and technology mandate or contractually require PLI due to high-exposure service risks. Premiums are actuarially priced on class of business, revenue, jurisdiction, claims history, and limits selected, with typical annual costs ranging from $400–$2,500 for freelancers and $5,000–$50,000+ for medical specialties. Risk-transfer effectiveness depends on maintaining continuous coverage, appropriate tail endorsements, and alignment of retroactive dates to avoid coverage gaps when switching carriers or retiring.

Quick hits:

- Covers negligence claims and service errors.

- Pays legal defense regardless of fault.

- Protects business reputation during disputes.

- Tailors coverage to specific professions.

- Responds when general policies won’t help.

The average liability lawsuit costs $54,000, underscoring the importance of securing defense-cost coverageRef.: “Derigiotis, D. (2025). Professional Liability Insurance vs General Liability Insurance: A Broker’s Guide to Client Conversations. Flow Specialty.” [!]

Errors and omissions coverage essentials

Errors and omissions insurance protects professionals from big financial losses. It helps when mistakes happen in work. Many professionals feel safer with this insurance.

This insurance covers mistakes made during work. It’s different from general liability, which deals with physical harm. It focuses on financial losses from mistakes in service.

If a client says you made a mistake, your insurance helps. It covers legal costs and possible settlements. This helps small businesses and freelancers a lot.

“Read More: Purpose of Renters Insurance Safeguarding Your Belongings“

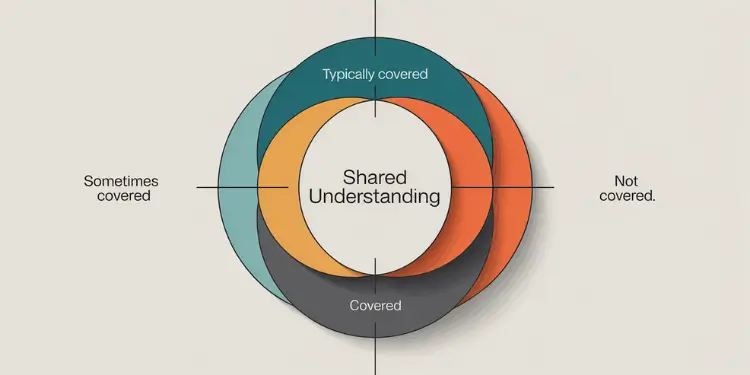

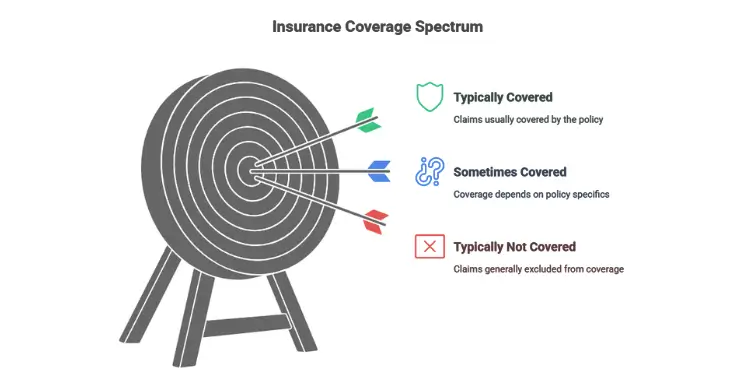

What Your Policy Typically Covers

Your policy protects against claims of negligence. This means if your work didn’t meet standards, you’re covered. It includes mistakes in judgment and wrong advice.

It also covers missed deadlines that cause client losses. For example, if an accountant is late with tax returns, you’re covered.

It protects against claims of misrepresentation too. This means if you promised something you couldn’t do, you’re covered. This is very important when things don’t go as planned.

Important Coverage Limitations

It’s important to know what your insurance doesn’t cover. It doesn’t cover criminal acts or intentional harm. Mistakes are okay, but not on purpose.

Most policies only cover claims made during the policy period. This is different from other insurance types.

Read your policy carefully. Knowing what’s covered helps avoid surprises when you need it most.

| Typically Covered | Sometimes Covered (Check Policy) | Typically Not Covered |

|---|---|---|

| Professional errors and mistakes | Copyright infringement | Criminal prosecution |

| Negligence claims | Temporary staff errors | Intentional wrongdoing |

| Missed deadlines | Subcontractor mistakes | Bodily injury/property damage |

| Defense costs | Work completed before policy start | Employee disputes |

| Breach of contract | Cyber liability | Business overhead expenses |

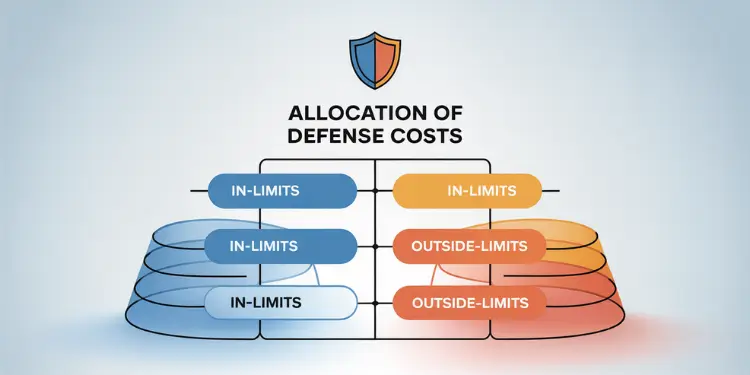

Defense Costs Consideration

One big plus of professional liability insurance is defense cost coverage. Even if you’re not found guilty, legal costs can be very high. Your policy covers lawyer fees and other legal expenses.

Some policies cover defense costs within your limits. Others add them to your limits. This makes a big difference in how much protection you have.

Always check how defense costs are covered in your policy. This detail can greatly affect your protection.

Industry-Specific Considerations

Professional liability insurance covers different risks in different fields. Medical malpractice insurance is different from IT consultant policies. Each field has its own risks.

For consultants, coverage for wrong advice is key. Financial advisors need protection for bad investment advice. Designers need coverage for mistakes in plans.

Knowing these differences helps get the right insurance for your field. Generic insurance is not enough for specialized fields.

In the next section, we’ll see how some industries need this insurance by law. This shows how serious the risks are in these fields.

Read More:

Industries requiring professional liability policies

Some industries face more risks and need special insurance. This insurance protects businesses from big financial losses. It covers mistakes, oversights, or negligence in service delivery.

Every service-based business can benefit from this insurance. But some fields are at higher risk because of their work.

I’ve worked with many clients across different sectors. I found that tailored insurance is best for each industry’s risks. Let’s look at which professionals need this insurance most and why.

| Industry | Common Liability Risks | Coverage Considerations | Typical Annual Premium Range |

|---|---|---|---|

| Medical Professionals | Misdiagnosis, treatment errors, patient injury | High coverage limits, defense costs included | $5,000-$50,000+ |

| Financial Advisors | Investment losses, improper advice, fiduciary breaches | Regulatory defense coverage, prior acts coverage | $1,500-$7,000 |

| Technology Consultants | Project failures, data breaches, missed deadlines | Intellectual property protection, cyber liability | $1,000-$5,000 |

| Real Estate Professionals | Disclosure errors, misrepresentation, fair housing violations | Transaction coverage, defense against licensing complaints | $600-$1,200 |

| Architects/Engineers | Design flaws, structural failures, code violations | Project-specific coverage, extended reporting periods | $2,000-$15,000 |

Many other fields also need this insurance. These include accountants, advertising agencies, consultants, graphic designers, interior designers, and market research firms. They all provide specialized services where mistakes can cause big financial losses to clients.

For small businesses, this insurance is very important. They often can’t afford the costs of a big claim. The average cost is between $600 and $1,200 a year for many professions. This insurance helps protect against legal costs that could close a business.

“Related Topics: Purpose of Homeowners Insurance Covering Property“

Negligence, Misrepresentation, and Breach of Duties

Professional liability policies cover three main types of claims. Knowing these helps you see if your policy is right for you.

Negligence is when a professional doesn’t do what a reasonable one would. For example, an accountant’s big mistake on a tax return can cause penalties for the client.

Misrepresentation is giving wrong or incomplete information to a client. This can be unintentional or on purpose. Most policies cover unintentional misrepresentation, like a real estate agent’s mistake about a property’s size.

Breach of duty is when you don’t meet your profession’s standards or your contract with the client. For instance, an attorney missing a deadline has broken their duty to the client.

When looking at policies, pay attention to how these terms are defined. Insurance companies use different words that can change what’s covered. Some policies use broad terms like “wrongful acts,” while others list specific scenarios.

“The difference between a $500 policy and a $5,000 policy often isn’t just the premium—it’s the definition of covered professional services and how broadly the insurer interprets negligence and breach of duty claims.”

Professional liability insurance protects even when you’ve done nothing wrong. About 40% of claims against professionals are found to be without merit. But defending against these claims can cost a lot, and your policy will cover it.

Gallagher Healthcare data shows nearly 70% of closed medical liability claims are dropped before trialRef.: “Gallagher Healthcare. (2017). How Much Does Medical Malpractice Insurance Cost? Gallagher Healthcare.” [!]

“Further Reading: Why Is Car Insurance Important for Protecting You“

Regulatory Fines Versus Civil Damages

It’s important to know what your policy covers. This can prevent surprises when facing a claim or regulatory action.

Civil damages come from lawsuits by clients or third parties. Professional liability insurance covers these damages. This includes direct financial losses, indirect losses, legal defense costs, and settlement expenses.

But regulatory fines are different. These are penalties from government agencies or licensing boards for breaking laws or standards. Most policies don’t cover these fines, but they might cover legal defense costs.

For example, a $50,000 fine from the SEC for a financial advisor might not be covered by their insurance. But the insurance will help with legal defense costs. This is important when choosing your coverage.

Some industries are watched closely by regulators. Healthcare, finance, and real estate are examples. In these fields, you might need special insurance that covers regulatory defense better.

When comparing policies, look for “regulatory defense coverage” or “licensing board defense coverage.” The best policies cover civil liability and also defend against regulatory actions, even if they don’t pay fines.

Professional liability insurance protects your expertise and business. It covers legal costs to defend your reputation and practice. While no policy covers everything, knowing the differences helps you choose the right one for your needs.

“You Might Also Like: Do I Need Life Insurance Today“

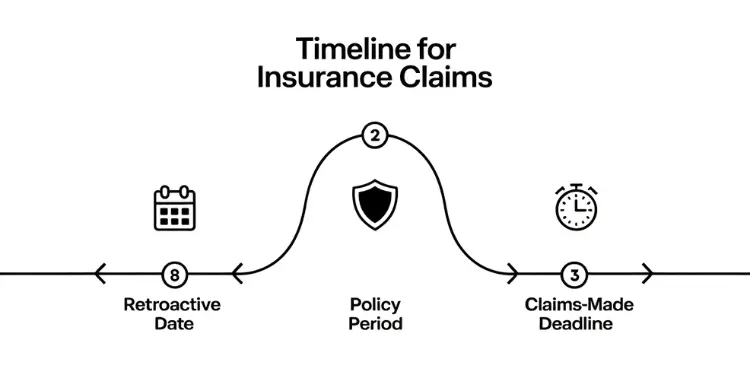

Claims made basis and retroactive dates

Professional liability insurance works on a claims-made basis. This means you need to file claims while your policy is active. The incident must have happened after your retroactive date but before your policy ends.

Many professionals are surprised when they find their old work isn’t covered. This is because of the retroactive date. It shows how far back your coverage goes.

Claims-Made vs. Occurrence Policies

There are two main types of coverage: claims-made and occurrence. Claims-made policies are more common for professionals. Occurrence policies are less common but offer different protection.

Claims-made policies cover incidents and claims during your policy period. If you cancel and a claim is filed later, you’re not covered. Even if the incident happened while you were insured.

Occurrence policies cover incidents during your policy period, no matter when the claim is filed. This means you’re protected for work done while the policy was active, even if you’ve canceled it.

| Feature | Claims-Made Policy | Occurrence Policy | Impact on Protection |

|---|---|---|---|

| When claim must be filed | While policy is active | Anytime (even years later) | Claims-made requires continuous coverage |

| Coverage for past work | Only after retroactive date | Only during policy period | Retroactive date determines historical coverage |

| Premium costs | Initially lower, increases over time | Higher but consistent | Budget planning differs between types |

| Availability | Common for professional liability | Rare for professional liability | Limited options for occurrence coverage |

| Coverage after cancellation | None without tail coverage | Continues for incidents during policy period | Occurrence provides better long-term protection |

Understanding Retroactive Dates

The retroactive date on your policy marks the start of your coverage. Work done before this date isn’t covered, even if a claim is filed later.

When you first get a policy, your retroactive date is the same as your policy start date. But when you renew or switch insurers, you can keep your original retroactive date. This keeps your past work covered.

Let’s say you started your consulting business in January 2020 and got your first policy then. Your retroactive date is January 2020. If a client files a claim in 2023 for work you did in 2021, you’re covered.

Coverage Gaps and How to Avoid Them

The biggest risk with claims-made policies is coverage gaps. These can happen when you switch insurers or let policies lapse. If you switch without keeping your retroactive date, you could lose protection for all your past work.

To keep coverage when switching insurers, make sure your new policy includes prior acts coverage. This goes back to your original retroactive date. It might cost a bit more, but it’s worth it for the protection against legal liability for damages from past work.

If you’re retiring or changing careers, don’t just cancel your policy. Consider getting “tail coverage.” This lets you report claims after your policy ends for incidents that happened while you were insured.

Setting the Right Retroactive Date

When setting your retroactive date, think about how long your work might be subject to malpractice claims. Some professions have longer statutes of limitations than others.

Your retroactive date should go back to when you first started giving professional advice or services. If you’re changing careers or starting a new business, your retroactive date will likely start with your new policy.

The further back your retroactive date goes, the more coverage you get. But your premium might also go up. This is because the insurer is taking on more risk by covering your past work.

I always tell professionals to keep their coverage going without gaps. Even a day without coverage can leave a permanent gap that no future policy can fix. The cost of defending against malpractice claims is much higher than the savings from temporary lapses.

“Related Articles: Compelling reasons why get travel insurance for every upcoming trip“

Policy limits selection and tail coverage

Professional liability insurance protects you financially. It depends on the policy limits you choose and if you get tail coverage. Knowing these helps you stay safe without spending too much.

In my ten years helping professionals, I’ve seen many cases. They were left without enough protection and lost a lot of money. The right limits are like a safety net against claims of negligence.

Understanding Policy Limits Structure

Liability policies have two limits: per-occurrence and aggregate. The per-occurrence limit is for one claim. The aggregate limit is for all claims in your policy period.

Most policies start with $1 million for each. But, you can choose from $250,000 to $2 million or more. Your needs depend on your job, clients, and risk.

When choosing policy limits for malpractice insurance, think about these:

- The typical claim size in your industry

- Your client profile and project values

- Contractual requirements from clients or partners

- Your personal assets requiring protection

- Regulatory requirements in your field

Defense costs are key. Some policies include defense costs in your limits. Others offer defense outside your limits. This can make a big difference.

| Profession | Typical Per-Claim Limit | Typical Aggregate Limit | Common Deductible Range |

|---|---|---|---|

| Physicians (non-surgical) | $1M – $3M | $3M – $5M | $5,000 – $25,000 |

| Architects/Engineers | $1M – $2M | $2M – $4M | $2,500 – $15,000 |

| Attorneys | $500K – $2M | $1M – $4M | $1,000 – $10,000 |

| IT Consultants | $500K – $1M | $1M – $2M | $1,000 – $5,000 |

| Accountants | $500K – $1M | $1M – $2M | $1,000 – $5,000 |

For high-risk jobs or big client contracts, you might need more limits. Excess liability policies can offer extra protection at a good price.

Your deductible choice affects your costs and what you pay out of pocket. Higher deductibles mean lower premiums but more costs when claims happen. Pick a deductible you can afford.

Extended Reporting Endorsement Considerations

Liability policies cover claims made during the policy period. But, there’s a gap when you change carriers or retire. Tail coverage is key.

Tail coverage, or Extended Reporting Period (ERP), keeps you covered after your policy ends. Without it, you could face uncovered claims years later.

Get tail coverage in these situations:

- When retiring from practice

- When changing careers or professional focus

- When selling your practice or business

- When changing insurance carriers

- When your insurer cancels or non-renews your policy

The right tail coverage length depends on your state’s statute of limitations. Most professionals need coverage for 2-7 years.

Tail coverage costs vary. They can be 100% to 300% of your annual premium. Some policies offer automatic tail coverage in certain situations. Others require a separate endorsement.

“The most common mistake I see professionals make is failing to secure adequate tail coverage when transitioning practices or retiring. This oversight can leave decades of good work unprotected against future claims.”

When looking at tail coverage, consider these:

- Coverage duration (limited vs. unlimited reporting periods)

- Covered services and exclusions

- Whether the tail covers all prior acts or only those after a specific retroactive date

- Premium costs and payment options

- Availability of installment payments for the tail premium

Some insurers offer “prior acts” coverage when switching carriers. This might mean you don’t need tail coverage from your old insurer. But, it needs careful planning to avoid gaps.

Understanding policy fundamentals is key for long-term protection. By choosing the right limits and tail coverage, you protect your practice and legacy.

“Dive Deeper: why get umbrella insurance for expanded personal liability“

Cost factors for freelance professionals

Knowing what affects the cost of professional liability insurance is key. It helps freelancers choose the right coverage without spending too much. Your premium is based on your unique risk, not a one-size-fits-all rate.

The type of business you have affects your insurance cost. Graphic designers usually pay less than financial advisors. This is because design errors are less likely to cause big damages than financial mistakes.

Your location also plays a big role in your premium. Freelancers in states with more lawsuits, like California or New York, pay more. I’ve seen the same business pay 30% more just because of where it’s located.

Experience and Claims History Impact

Your experience affects how insurers see your risk. New freelancers pay more than those with years of experience. Insurers like businesses with a proven track record.

Previous claims can raise your rates a lot. A policy protects against future claims, but past incidents are seen as a sign of future risk. Even one claim can increase your premium by 10-50%.

“The best insurance policy is the one you never need to use. Each year without claims builds credibility with insurers and often translates to premium discounts.”

Insureon says the median cost for their clients is $61 monthly ($735 annually). Most freelancers pay between $600 and $1,200 a year. But costs vary a lot based on individual situations.

| Profession | Average Annual Premium | Risk Level | Typical Coverage Limit |

|---|---|---|---|

| Web Developer | $500-$1,000 | Moderate | $1M per occurrence |

| Accountant | $800-$1,500 | High | $1M-$2M per occurrence |

| Graphic Designer | $400-$800 | Low | $500K-$1M per occurrence |

| Management Consultant | $1,000-$2,500 | Very High | $2M+ per occurrence |

Business Structure and Coverage Options

Your business structure affects your liability and insurance costs. Sole proprietors face unlimited personal liability, making full coverage essential. But it might cost more. Forming an LLC offers some protection but doesn’t eliminate the need for liability insurance.

Coverage limits and deductibles impact your costs. A $1 million policy with a $1,000 deductible might seem good. But adjusting these can make coverage more affordable. Liability insurance protects your business assets, but finding the right balance between coverage and cost is key.

The more employees or subcontractors you have, the higher your premium. Each person adds to your liability exposure. Insurance covers mistakes made by anyone working for you.

“For More Information: defining the purpose of dental insurance“

Strategic Ways to Manage Premium Costs

There are practical steps to lower your insurance costs without losing necessary protection:

- Bundle policies – Combining professional liability with general liability or business owner’s policies often results in multi-policy discounts

- Pay annually – Many insurers offer discounts of 5-10% for paying your premium in full instead of monthly

- Implement risk management practices – Documented quality control procedures and client communication protocols can qualify you for lower rates

- Adjust coverage limits strategically – Match your coverage to your actual risk exposure instead of choosing the highest limits

- Consider project-specific policies – For occasional high-risk projects, a short-term policy may be more cost-effective than year-round high-limit coverage

Project-specific policies are great for freelancers with variable workloads. They offer protection for a single project or client engagement, not continuous coverage. They’re useful for freelancers with occasional high-risk projects.

When comparing quotes, don’t just look at the price. The cheapest policy might not offer all the protections you need. The best value is finding the right coverage at a fair price, not just the cheapest option.

“Check Out: explaining the purpose of vision insurance“

Risk management practices reducing claim frequency

Getting professional liability insurance is just the start. Strong risk management can really cut down on claims. These practices work with your insurance to protect you well.

Insurance can cover claims up to a certain amount. But, stopping claims before they happen saves you money and keeps your reputation safe.

Engagement Letters Clarifying Service Scope

Clear documents are your first line of defense. They prevent misunderstandings that can lead to claims. Engagement letters clearly state what services you’ll do, when, and what results clients can expect.

These letters help avoid disputes about what was promised versus what was delivered.

Your engagement letter should include:

- Specific deliverables with measurable outcomes

- Project timeline with key milestones

- Fee structure and payment terms

- Process for handling scope changes

“Learn More About: clear purpose of mortgage life insurance for outstanding home“

Continuing Education to Maintain Competence

Keeping up with your field is key. It’s not just smart business—it’s a must for risk management. Professional liability insurance guards against negligence claims. But, old practices raise your risk.

Learning new things through workshops and courses is worth the $600-$1,200 a year for errors and omissions insurance. Your knowledge stops claims before they start.

{kind=link}