Motorcycle insurance is more than just a legal must. It acts as a financial shield, guarding riders from huge costs after crashes. Did you know riders without insurance face over $31,000 in expenses after an injury crash?

I’ve helped many Idaho riders as an insurance advisor. I’ve seen how good coverage saves them from financial ruin. My mentor always said, “Insurance is not a cost. It’s a smart investment in your future.”

Riding without insurance is risky. It’s not just your bike you’re risking. Medical bills, lawsuits, and damage costs can lead to huge debts.

I recall a case where a $25 monthly premium saved a client from a $175,000 lawsuit. That’s the true worth of good insurance.

Quick hits:

- Shields against catastrophic liability claims

- Covers medical expenses after accidents

- Protects your bike from theft

- Fulfills state legal requirements easily

- Provides peace of mind riding

Motorcycle insurance essentials and coverage scope

Knowing about motorcycle insurance is key for riders. It gives them safety and peace of mind. Motorcycle insurance is like car insurance but has special protections for bikes.

Most policies have basic parts. Bodily injury and property damage liability are must-haves in many places. They help pay for damage or injuries you cause.

There are also extra coverages. Collision and theft coverage protect your bike. Uninsured/underinsured motorist coverage helps if someone hits you without enough insurance.

What coverages you need depends on your bike and riding habits. If your bike is pricey, you might want more coverage. Riders with custom parts need special equipment coverage.

Differences from Standard Auto Insurance Policies

Motorcycle and auto insurance are similar but different. Motorcyclists face unique risks. This affects how insurance is priced and structured.

One big difference is guest passenger liability. It covers injuries to people riding with you. Auto policies don’t need this because passenger injuries are usually covered elsewhere.

Seasonal coverage is another difference. Some insurers offer lower rates when you store your bike. This is because many riders don’t ride all year, like in cold places.

Insurance companies look at different things for motorcycles. Engine size, bike style, and riding experience matter. These don’t affect auto insurance the same way.

| Coverage Feature | Motorcycle Insurance | Auto Insurance | Key Difference |

|---|---|---|---|

| Passenger Protection | Guest passenger liability | Standard passenger coverage | Motorcycle requires specific passenger coverage |

| Seasonal Options | Lay-up periods available | Year-round coverage assumed | Motorcycles often stored seasonally |

| Equipment Coverage | Specialized for accessories/gear | Limited aftermarket coverage | Motorcycles often have significant customization |

| Risk Assessment | Based on bike type, engine size | Based on vehicle safety ratings | Different risk factors considered |

| Medical Coverage | Higher limits often recommended | Standard medical payment options | Greater injury risk for motorcyclists |

When looking for motorcycle insurance, knowing the differences is key. Many riders think their needs are the same as car owners. But this can leave them without the right protection.

I always tell new riders to talk to a motorcycle insurance expert. These agents can explain things clearly. They help find the right coverage for your bike, riding, and safety needs.

Read More:

Bodily injury and property liability limits

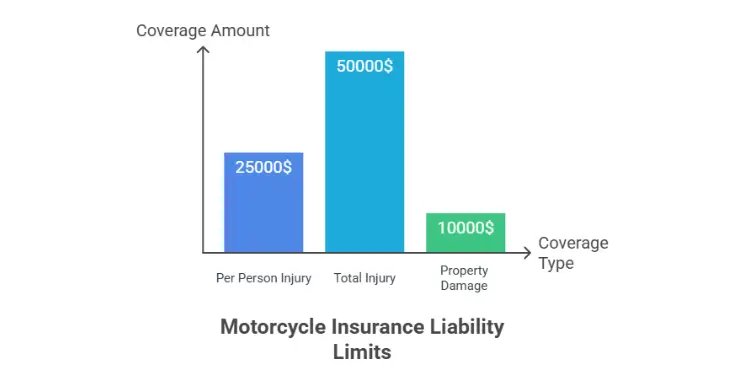

Every motorcycle insurance policy has a key part called liability coverage. It has limits for injuries and damage to property. When you look at your policy, you’ll see these limits with slashes, like $25,000/$50,000/$10,000.

The first number, $25,000, is the max your insurance pays for each person hurt in an accident you cause. The second number, $50,000, is the total for all injuries in one accident. The third number, $10,000, is for damage to property, like cars or buildings.

I’ve seen how fast these limits can go up. A rider hit a car and the other driver had $32,000 in medical bills. The car repairs cost $14,000. With only $25,000/$50,000/$10,000 coverage, the rider had to pay $11,000 from his savings.

State Minimum Requirements and Penalties

Every state has its own minimum for motorcycle insurance. These are the least you can legally carry. Riding without it can lead to big problems.

Getting caught without insurance means fines from $100 to over $1,000. Your license and registration might get suspended. You might have to do community service or have your motorcycle taken away.

Riding without insurance means you could be sued for all damages and injuries you cause. The NAIC says the average claim for injuries in motorcycle accidents is over $15,000. That’s a lot to pay yourself.

| State | Bodily Injury (per person/per accident) | Property Damage | First Offense Penalty |

|---|---|---|---|

| California | $15,000/$30,000 | $5,000 | $100-$200 fine + fees |

| Florida | Not required for motorcycles* | $10,000 (PD only) | License/registration suspension |

| New York | $25,000/$50,000 | $10,000 | Up to $1,500 fine + license revocation |

| Texas | $30,000/$60,000 | $25,000 | $175-$350 fine + fees |

| Michigan | $50,000/$100,000 | $10,000 | $200-$500 fine + possible jail time |

*Florida requires $10,000 in Personal Injury Protection (PIP) for cars but has different requirements for motorcycles.

Higher Limits for Asset Protection

State minimums haven’t changed much in years. Medical costs and car prices have gone up a lot. This makes minimum coverage not enough.

Your liability coverage protects not just others but also your money. If damages are more than your policy, you could lose your savings, home, and future earnings. Most experts say you should have at least $100,000/$300,000/$50,000 coverage.

Here’s an example: A rider caused an accident with two cars. The damages were $75,000 in medical bills and $30,000 in car repairs. With only $25,000/$50,000/$10,000 coverage, he had to pay $45,000 himself. If he had $100,000/$300,000/$50,000 coverage, his insurance would have covered it all.

Going from minimum to recommended coverage usually costs only $100-$200 a year. This is a small price for the extra protection it gives.

Remember, liability insurance covers damages you cause to others, not your own injuries or bike. We’ll talk about coverages for you in the next parts. For now, think of your liability limits as your first defense against financial trouble after an accident.

Comprehensive coverage against theft and vandalism

When your motorcycle gets stolen, damaged by weather, or vandalized, coverage is key. It’s not like liability insurance, which protects others. Instead, it keeps your motorcycle safe, even when it’s parked.

Many riders find out the hard way that basic insurance doesn’t cover everything. But, with the right policy, you can get help for theft, vandalism, and more.

So, what does this coverage do? It usually pays for:

- Theft of your motorcycle

- Vandalism and malicious damage

- Fire damage

- Storm and weather damage (hail, flooding, wind)

- Falling objects (tree branches, debris)

- Animal collisions

Last summer, a Harley in Idaho Falls got hit by hail. The damage cost $2,300 to fix, but the rider only had to pay $500.

Deductibles are important. They’re the amount you pay first before insurance kicks in. A higher deductible means lower premiums but more cost if you need to claim.

| Deductible Amount | Premium Impact | Financial Risk |

|---|---|---|

| $250 | Higher premiums | Lower out-of-pocket cost |

| $500 | Moderate premiums | Moderate out-of-pocket cost |

| $1,000+ | Lower premiums | Higher out-of-pocket cost |

Some think homeowners insurance covers motorcycles in the garage. But, this is usually not true. Most policies don’t cover vehicles that need to be registered.

If your bike is stolen, your insurance pays its actual cash value. This value decreases over time, which can be a big loss for older bikes. Some policies offer agreed value, where you and the insurer agree on the bike’s value.

Is this coverage right for you? Think about this:

If your motorcycle’s value is less than 10 times your annual premium, you might not need it.

For example, if your bike is worth $3,000 and coverage costs $350 a year, you might not need it. But, for most riders, it’s a good idea to keep it.

Keep coverage even when your bike is not in use. Theft and damage can happen anytime, and winter storage has its own risks.

Remember, this coverage works with collision coverage, not instead of it. It covers non-collision incidents, while collision covers accidents with other vehicles or objects.

Related Posts:

Medical payments and personal injury protection

After a motorcycle accident, knowing about medical payments and personal injury protection is key. These options help you when you get hurt. They are not the same as liability coverage, which protects others.

Medical payments coverage, or Med Pay, is like health insurance for motorcycle accidents. It pays for your medical costs, no matter who was at fault. This means you get help with bills if you hit something or someone hits you.

Med Pay is easy to understand and helps right away. It covers things like:

- Emergency room visits

- Hospital stays

- Doctor appointments

- X-rays and diagnostic tests

- Surgical procedures

- Ambulance fees

Personal Injury Protection (PIP) offers more than Med Pay. It’s not in every state, but it’s great for extra costs. It can help with things like lost wages and childcare costs.

PIP covers more than just medical bills. It also helps with other costs you might not think about when looking for motorcycle insurance medical coverage.

PIP covers things like:

- Lost wages if you can’t work

- Childcare expenses during recovery

- Funeral expenses in worst-case scenarios

- Essential services you can’t perform while injured

Med Pay and PIP are optional, but they’re very important. They offer extra protection that you might not get from other insurance.

Some riders wonder why they need these coverages if they have health insurance. The reason is simple: health insurance might not cover everything. Med Pay and PIP can fill in the gaps, often with no deductible and quick payment.

| Coverage Type | What It Covers | Availability | Cost Factors | Typical Limits |

|---|---|---|---|---|

| Medical Payments | Medical expenses only | Optional in most states | Riding history, coverage limit | $1,000 to $25,000 |

| Personal Injury Protection | Medical expenses plus lost wages, childcare, funeral costs | Required in some no-fault states, optional or unavailable in others | State requirements, coverage limit, riding history | $2,500 to $50,000 |

| Health Insurance | Medical expenses (subject to policy terms) | Separate from motorcycle insurance | Plan type, deductible, network | Varies by plan |

When choosing medical coverage, think about these things:

- Your health insurance deductible and out-of-pocket maximum

- Whether your health insurance has motorcycle exclusions (some do)

- Your financial ability to cover immediate medical costs before health insurance reimbursement

- Your income and how a period of disability would affect your finances

- Whether you have dependents who rely on your income

These coverages are not very expensive. Med Pay of $5,000 to $10,000 adds $50-100 a year to your premium. PIP costs vary by state and coverage level but usually range from $100-300 a year.

Motorcycle injuries are common. Riders are 28 times more likely to die in a crash than car drivers. Having the right medical coverage is about protecting your finances, not just being scared.

Before choosing Med Pay or PIP, check your health insurance. Look for exclusions, ambulance coverage limits, and how quickly benefits are paid. This will help you see where motorcycle-specific coverage can help.

After my minor crash last year, Med Pay covered my $3,500 ER bill immediately while my health insurance was processing the claim. That immediate coverage meant I could focus on healing without worrying about medical bills.

Understanding these options helps you protect yourself when riding. It’s about keeping your body and wallet safe.

State specific motorcycle insurance regulations

It’s key to know your state’s motorcycle insurance rules. This keeps you legal and safe. You must understand what coverage your state needs before you ride.

Most states require two main types of insurance. Bodily injury liability covers medical costs for others if you’re in an accident. Property damage liability pays for damage to other vehicles or property. These coverages protect others, not you or your bike.

Some states have strict rules, while others are more lenient. For example, Florida lets some riders skip insurance if they show they can pay for accidents. New York, on the other hand, requires more coverage.

Many new riders think their car insurance covers their motorcycle. But, this is not true. Your motorcycle needs its own policy that fits your state’s rules.

| State Example | Minimum Liability Requirements | Helmet Law | Special Considerations |

|---|---|---|---|

| California | 15/30/5 ($15,000 bodily injury per person, $30,000 per accident, $5,000 property damage) | Universal (all riders) | Lane splitting legally permitted |

| Florida | 10/20/10 (with PIP option) | Partial (under 21 or without insurance) | Can opt out with proof of financial responsibility |

| Texas | 30/60/25 | Partial (under 21) | Requires proof of insurance for registration |

Mandatory Equipment and Safety Certifications

States often link insurance to safety gear use. Insurance is more than just money protection. It’s part of a safety plan. For example, not wearing a helmet in a helmet law state can lower your claim.

Here are some safety gear needs:

- DOT-approved helmets (required in many states)

- Eye protection (goggles or windshields)

- Proper lighting and reflectors

- Working horns and mirrors

- Compliant exhaust systems

Some insurance companies give discounts for safety courses. These courses improve your skills and show you care about safety. They make you a better rider and can lower your costs.

It’s easy to find your state’s rules. Check your state’s Department of Insurance or Department of Motor Vehicles websites. They have the latest rules and help you know what coverage you need.

If you ride in different states, your policy must meet each state’s rules. Most insurers adjust your policy for you. But, always check with your agent.

Insurance is only as good as your understanding of it. Know your state’s requirements before you ride, not after an incident occurs.

State rules can change often. What was okay last year might not be this year. Always check your motorcycle insurance policy every year, if you move or ride in different states.

Check out the below:

Tips for selecting affordable motorcycle coverage

Finding the right motorcycle insurance doesn’t have to be expensive. Many riders find good coverage without spending too much. The cost of your bike affects your insurance rates. More expensive bikes cost more to fix or replace, leading to higher premiums.

Engine size also plays a role. Bigger engines usually mean higher insurance costs. If you change your engine, tell your insurer right away to avoid coverage gaps. Even with a cheap bike, your policy covers damage to others’ property.

Here are some ways to lower your motorcycle insurance costs:

Bundle your policies with one company. Getting motorcycle coverage with your home or auto insurance can save you 5-15%.

Take a motorcycle safety course. Many insurers give discounts to riders who show they care about safety through training.

Change your deductibles. Going from a $250 to a $500 deductible can cut your premiums by 15-30% for both collision and comp.

Look for specific discounts. Some companies offer lower rates for things like anti-theft devices, garage storage, or riding association memberships.

Check your coverage every year. As your bike gets older, you might change some coverages. But keep the main goal of insurance in mind: to protect your money from unexpected damage.

The best policy is one that’s affordable but also protects you well. It should fit your riding habits and budget.

{kind=link}