Mobile home insurance is key to protect your home from sudden disasters. It gives you a financial safety net that regular home insurance can’t. Did you know over 22 million Americans live in manufactured homes? Yet, nearly 40% don’t have enough insurance.

One client said, “I never thought I needed coverage until a windstorm hit my community.” I’ve helped Idaho families for ten years. I’ve seen how good insurance saves money after bad weather.

Manufactured homes (built after 1976) and mobile homes (pre-1976 models) need special insurance. It’s not always needed, but it’s key when you finance your home or live in risky areas.

Your policy guards against common dangers like storm damage, fire, theft, and visitor injuries. It’s your financial shield.

Quick hits:

- Protects structure and attached features

- Covers personal belongings inside

- Provides liability for visitor injuries

- Helps with temporary living expenses

- Addresses unique manufactured home risks

Mobile Home Insurance Fundamentals Explained Clearly

Mobile home insurance is special. It protects your home and things inside. Many people in Idaho don’t know how it works. Let’s talk about what you get with mobile home insurance.

This insurance is like regular homeowners insurance but different. It’s made for mobile homes. These homes are built differently and face special risks. Unlike regular homes, they often lose value over time.

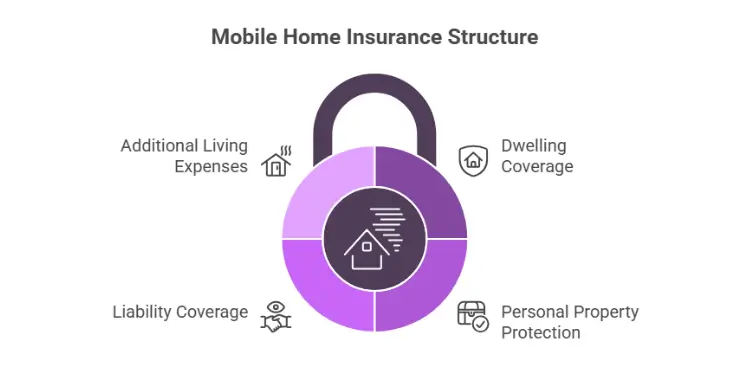

Mobile home insurance has four main parts:

- Dwelling coverage – Keeps your home safe from damage like fire and wind

- Personal property protection – Covers your stuff inside the home

- Liability coverage – Helps if someone gets hurt on your property

- Additional living expenses – Pays for a place to stay if your home is not safe

Let’s say a storm damaged Sarah’s roof. Her insurance paid for the $7,800 fix, minus a $500 deductible. Without insurance, she’d have had to pay all of it herself.

Most policies cover things like fire and theft. But, they don’t cover everything. Some risks need extra coverage. This can be a surprise for many.

| Typically Covered | Usually Excluded | Available as Add-ons |

|---|---|---|

| Fire and smoke | Flood damage | Flood insurance |

| Wind and hail | Earthquake damage | Earthquake rider |

| Theft and vandalism | Transit damage | Transportation coverage |

| Falling objects | Mold and pest damage | Extended protection riders |

Don’t forget about transportation coverage. Mobile homes might need to be moved. Standard policies usually don’t cover damage during transport. It’s smart to add this coverage, even if you don’t plan to move soon.

Policy limits and deductibles work like regular insurance. The limit is the most your insurer will pay. The deductible is what you pay first. Higher deductibles can lower your premium but mean you pay more when you file a claim.

It’s important to know about replacement cost and actual cash value. Replacement cost means paying today’s prices for new items. Actual cash value means paying what something is worth now, which might be less. For example, a five-year-old TV might be worth less than what you paid, leaving a gap in coverage.

“The most common mistake I see mobile homeowners make is assuming their policy covers everything. Take time to understand what’s included and what isn’t—then fill those gaps with appropriate riders.”

Next, check your policy or quotes for the four main coverages. Look for flood, earthquake, and transit protection if you need it. We’ll look at these coverages more in the next sections and help you figure out your risks.

Read More:

Core Coverages Dwelling Personal Property Liability

Mobile home insurance gives you three main coverages. These are special for mobile homes. They protect against risks that regular homes don’t face.

Dwelling coverage is the base of your policy. It protects your mobile home’s structure. This includes walls, roof, and floors. You can choose between actual cash value or replacement cost value.

Actual cash value means you get the current market value of damaged items. Replacement cost pays to replace items at today’s prices. Replacement cost is more expensive but better for claims.

Personal property coverage protects your belongings inside the home. This includes furniture and electronics. Policies usually cover personal property at 50-70% of your dwelling coverage amount.

High-value items like jewelry need special coverage. Make a home inventory with photos and receipts. This helps when you need to replace damaged items.

Liability protection is also key. It covers you if someone gets hurt on your property or if you damage someone else’s. This includes medical costs, legal defense, and property damage.

Most insurers suggest at least $100,000 in liability coverage. But $300,000 or more is better. The extra cost for more liability coverage is small compared to the extra protection.

Weather and Transportation Hazard Protection

Mobile homes face special weather risks. Their light construction and high position make them vulnerable to wind damage. Knowing how your insurance covers these hazards is key for mobile home owners.

Standard policies cover many weather-related damages. But, flood damage is not included. If your home is in a flood area, you need separate flood insurance.

Another important thing is coverage for mobile home transportation. Most policies don’t cover damage during moving. You need a special endorsement for this.

To protect your home during transport, get a trip transit endorsement. This coverage is for damage during moving. Before moving, talk to your insurance agent to add this coverage.

Loss of Use and Additional Living Expenses

Loss of use coverage is very important. It helps with extra living costs if your home is damaged and you can’t live there. This coverage keeps your living standard the same while repairs are done.

Imagine a storm damages your roof and water gets in. Loss of use coverage helps with hotel costs and other expenses. It covers things like restaurant meals and laundry services.

Most policies offer 10-20% of your dwelling coverage for loss of use. For example, if your home is insured for $80,000, you might get $8,000 to $16,000. Some policies have a time limit, like up to 12 months.

When using this coverage, keep all receipts. Insurance companies pay the difference between your usual and increased living costs. For example, if you spend $300 monthly on groceries but $600 on meals while displaced, they cover the $300 difference.

Loss of use coverage is very helpful in areas with severe weather. It provides financial stability during stressful times.

Assessing Risk for Manufactured Housing Owners

Protecting your manufactured property starts with finding hazards. Manufactured homes face risks different from site-built homes. Knowing your risks helps avoid gaps in coverage and saves money.

Manufactured homes are built lighter and can get damaged easily. Their design and how they’re moved make them more vulnerable. This is different from traditional homes.

Regional Risk Factors

Your location affects your insurance needs. For example, Florida homes face more hurricane damage. I’ve seen how risks change in different places:

- Coastal Areas: Hurricanes can damage homes more than inland areas.

- Midwest Regions: Tornadoes are a big risk for manufactured homes.

- Western States: Wildfires are a growing danger.

- Low-Lying Areas: Floods can cause a lot of damage. Standard insurance doesn’t cover floods.

The age and quality of your home matter. Newer homes built after 1976 are safer. Roof damage can lead to big problems if not fixed.

How your home is built affects its safety. Better foundations and tie-downs can reduce damage and save money on insurance.

Lifestyle Considerations

How you use your home changes your insurance needs. Homes used full-time need more protection than vacation homes. Unoccupied homes face different risks.

Living in a community can affect your safety. Communities may have better security but can also have more neighbor issues.

Valuable items inside your home need extra care. Standard insurance covers some items, but special items might need extra coverage.

Risk Assessment Checklist

Use this checklist to understand your risks:

- Know your home’s age, size, and HUD status

- Take photos of safety features

- Find out about local dangers

- Make a list of valuable items

- Check how close you are to emergency services

- Record any recent improvements

- Think about how much you can afford to pay for insurance

This checklist helps you get the right insurance. It’s not about spending too much. It’s about getting the right coverage for your home.

Your home is a big investment and a safe place. Understanding its risks helps you get the right insurance. This way, you’re protected without wasting money.

Related Posts:

Premium Drivers Age Location Build Quality

Mobile home insurance costs are based on risk factors. These factors change for each owner. Knowing these helps you choose the right policy.

The age of your home affects your premium. Newer homes get better rates because they meet safety standards. Homes made after 1994 cost less to insure.

Where you live is key to your premium. Insurers look at:

- Weather and natural disaster risk

- Local crime and theft rates

- Fire protection class rating

- Distance to fire hydrants or stations

- Flood zone designation

Build quality matters too. Insurers check materials, roof type, and foundation. HUD-certified homes get better rates. Metal roofs can save you money.

Your claims history shows your risk level. Many claims mean higher premiums. Credit scores also matter in most states.

What you choose for coverage and deductibles affects your premium. Higher coverage costs more. But, a higher deductible lowers your monthly payment.

The most expensive policy is one that doesn’t protect your home. Focus on enough coverage first, then look for ways to save.

Bundling policies can save you money. Combining mobile home insurance with other policies can cut costs. Families can save 15-25% this way.

Discounts for Tie Downs and Alarms

Adding safety features can lower your insurance costs. These features protect your home and show you’re a responsible owner.

Tie-downs reduce wind damage risk. They’re a smart investment for lower premiums. The tie-down class affects your discount:

| Tie-Down Class | Wind Resistance | Installation Cost | Typical Discount | ROI Timeline |

|---|---|---|---|---|

| Basic | Up to 70 mph | $800-1,200 | 5-8% | 3-4 years |

| Standard | Up to 90 mph | $1,200-2,000 | 8-12% | 2-3 years |

| Hurricane-rated | 110+ mph | $2,000-3,500 | 12-20% | 2-5 years |

Security systems also lower premiums. Different alarms offer different discounts:

- Smoke detectors and carbon monoxide monitors – Basic protection; limited discount but essential

- Burglar alarms – Local alarms save 2-5%; monitored systems save 5-10%

- Water leak detection systems – New; can save 3-8% and prevent water damage

- Monitored security services – Full monitoring can save 10-15%

Other improvements like impact-resistant roofing and storm shutters can also save money. Each addresses a specific risk for mobile homes.

To get discounts, you need proof. Keep receipts and certificates. Some features need professional installation for discounts.

When asking for quotes, list all safety features. Photograph them for proof. This ensures you get all discounts you deserve.

Many safety features together can save a lot. I’ve seen homeowners save 25-30% with smart improvements. The cost pays off in 2-4 years, protecting your home.

Shopping for Reliable Mobile Home Policies

Looking for good mobile home insurance? A smart plan is key. I’ve helped many find great insurance. This way, they save money and worry less.

First, write down your home’s important facts. Include the year, make, model, size, and any extra parts. These details affect your insurance choices and costs. Take photos of your home from all sides, showing off its special features.

Next, list what’s inside your home. Use your phone to video each room. For expensive items, write down their serial numbers and how much they cost. This info is very helpful if you need to make a claim.

The biggest mistake I see manufactured homeowners make is choosing a policy based solely on price. The few dollars saved monthly can cost thousands in uncovered losses after a disaster.

Before getting quotes, do your homework on insurance companies. Look for AM Best ratings of B+ or higher for stability. Check J.D. Power for customer satisfaction and the NAIC for complaints.

Get quotes from at least three insurers. Some focus on mobile homes, while others cover them as part of their general insurance. Specialists might know more about mobile home risks, but generalists might offer better deals for bundling.

Ask each agent these questions:

- What perils are not covered?

- How do they figure out actual cash value versus replacement cost?

- How fast do they handle claims?

- Do they offer discounts for safety features or bundling?

- How do they handle moving your home if needed?

Ask for a sample policy before deciding. Look closely at parts about wind damage, water damage, and liability. I’ve seen people find out about coverage gaps after a claim.

Think about whether bundling is right for you. While it can save money, sometimes separate policies are better. Bundling works best for newer homes with fewer risks.

| Evaluation Factor | What to Look For | Red Flags | Ideal Scenario |

|---|---|---|---|

| Financial Strength | AM Best rating B+ or higher | Ratings below B, limited history | A or A+ rating with 10+ years stability |

| Claims Process | 24/7 reporting, mobile app options | Limited hours, mail-only claims | Multiple reporting methods, local adjusters |

| Coverage Definitions | Clear language on perils covered | Vague exclusions, excessive limitations | Comprehensive coverage with minimal exclusions |

| Premium Structure | Transparent pricing factors | Unexplained surcharges, high fees | Predictable premium increases, multiple discount options |

| Customer Service | Multiple contact methods, quick response | Limited availability, offshore call centers | Dedicated agent, 24/7 support options |

The cheapest policy isn’t always the best. I’ve seen big differences in coverage. Look for a balance between good protection and cost.

Before you buy, make sure your home’s extras are listed. Policies often don’t cover things like carports or sunrooms unless you add them. This small step can save you a lot of money.

After picking a policy, check it every year. Your home’s value and what you own can change. Keeping your insurance up to date is easy and important.

Check out the below:

Steps to Maintain Continuous Mobile Coverage

Keeping your manufactured home safe is more than just buying insurance. It needs constant care. Over the years, I’ve helped many Idaho families. They learned that regular checks prevent big problems.

Annual Policy Review and Updates

Make sure to review your mobile home insurance every year. Check if your coverage matches the cost to rebuild your home. Prices for materials and labor change a lot.

Has your family bought new things like electronics or jewelry? Update your policy to cover these items.

Life events like getting married or starting a business change your insurance needs. Call your agent when these happen. Don’t wait until your policy is up for renewal.

Documenting Upgrades for Coverage Adjustments

Keep records of any upgrades to your home. This includes things like a new roof or better electrical system. Take photos before and after and save all receipts.

Make a simple list of your upgrades. Include:

– When you installed it

– How much it cost

– Who did the work

– What materials were used

– How long it’s expected to last

Share this list with your insurance company. They might lower your rates and make sure you’re covered right. Many people miss out on discounts because they don’t tell their insurance about upgrades.

Your insurance should grow with your home and life. Being proactive helps you stay protected without spending too much.

{kind=link}