Earthquake insurance is like a shield for your home when regular insurance doesn’t help during earthquakes. Your usual homeowners insurance doesn’t cover damage from earthquakes. This leaves a big gap in protection.

Only 10% of American homeowners in high-risk areas have this special coverage. Did you know that?

FEMA says fixing earthquake damage can cost $60,000 to $100,000. The California Earthquake Authority says being financially ready is as important as being physically ready.

In my 10 years helping Idaho Falls families, I’ve seen how this insurance saves them from huge debts. Without it, they have to pay for repairs themselves. This can use up their retirement savings or force them to sell their homes for less.

Quick hits:

- Covers what standard policies exclude

- Protects against catastrophic financial loss

- Maintains property resale value

- Offers peace of mind

- Prevents huge out-of-pocket costs

Earthquake insurance essentials and tectonic risk context

Earthquake insurance is special because it covers big risks that regular policies don’t. I’ve helped many homeowners understand these policies. They are made for the big dangers of earthquakes.

Earthquake policies have high deductibles, often 10-20% of your home’s value. This means they help a lot when your home is badly damaged. But, they might not help as much for small damage.

Your home’s location affects your risk and how much you pay for insurance. Homes on solid ground are safer than those on loose soil. Wood homes are also safer because they can move a bit during earthquakes.

Add a stand-alone earthquake policy or endorsement to eliminate the “earth-movement” exclusion in standard homeowners coverage and secure full rebuilding protection. Ref.: “Insurance Information Institute. (2025). Earthquake insurance for homeowners. Insurance Information Institute.” [!]

“The earth’s crust is divided into tectonic plates that constantly move against each other. Where these plates meet—at fault lines—is where earthquakes are most likely to occur, creating varying risk zones across the country.”

Differences from Standard Homeowners Insurance Policies

Standard homeowners policies don’t cover earthquake damage. This leaves a big gap in areas where earthquakes happen a lot. I always explain these differences to my clients.

| Coverage Element | Standard Homeowners Policy | Earthquake Policy | Financial Impact |

|---|---|---|---|

| Earth Movement Damage | Explicitly excluded | Primary coverage | Potential total loss without earthquake coverage |

| Deductible Structure | Fixed dollar amount ($500-$2,500) | Percentage of home value (10-20%) | Much higher out-of-pocket costs |

| Fire Following Earthquake | Typically covered | Sometimes supplemental | Coverage overlap possible |

| Personal Property | Higher coverage limits | Limited coverage (often separate deductible) | Significant personal property losses possible |

Standard policies cover fire damage, even if it’s from an earthquake. But, they don’t cover damage from the earthquake itself. This is important when you file a claim after an earthquake. Water damage from broken pipes is also not covered.

The 2024 National Seismic Hazard Model shows that nearly 75 % of the United States could experience damaging earthquake shaking—highlighting that risk extends far beyond the West Coast. Ref.: “U.S. Geological Survey. (2024). New USGS map shows where damaging earthquakes are most likely to occur in US. U.S. Geological Survey.” [!]

The California Earthquake Authority (CEA) offers special policies for California. These policies are designed for the state’s high earthquake risk. Private insurers also offer earthquake coverage, but with different terms.

Earthquake policies usually have lower limits for personal property. They might cover $5,000 to $25,000, while standard policies cover 50-70% of your home’s value.

- Additional living expenses coverage helps with temporary housing if your home becomes uninhabitable after an earthquake

- Building code upgrade coverage helps pay for required updates when rebuilding

- Emergency repairs coverage helps prevent further damage after an earthquake

- Land restoration is typically excluded or severely limited

Renters insurance doesn’t cover earthquake damage to your belongings. If you rent in a seismically active area, you need a separate earthquake policy for your personal property.

Earthquake policies have high deductibles because of the big risks. For example, if your home is worth $500,000 and you have a 15% deductible, you pay the first $75,000. This makes them more valuable for big damage than small repairs.

Knowing these differences helps you decide if you need earthquake insurance. The next section will talk about how these policies protect your home and belongings.

Structural and personal property loss protection

Earthquake insurance has three main parts that protect your home. Over ten years, I’ve helped many homeowners understand these parts. This knowledge helps them choose the right coverage.

Dwelling Coverage: Your Home’s Structure

Dwelling coverage is the base of your earthquake policy. It covers your home’s structure, like walls and ceilings. If an earthquake damages your home, this coverage kicks in.

For example, if a 5.5 magnitude earthquake damages your home, this coverage helps pay for repairs. You can adjust this amount based on your needs.

But, dwelling coverage doesn’t cover detached structures like fences. Always check these exclusions with your agent.

Personal Property Protection

The second part covers your belongings inside the home. This includes furniture and clothes damaged during an earthquake. If your bookshelf falls and breaks your TV, this coverage helps replace it.

Most policies set personal property limits at 50% of dwelling coverage. The California Earthquake Authority (CEA) offers coverage from $5,000 to 75% of dwelling coverage.

High-value items like jewelry have sub-limits. Document these items before damage occurs. I suggest making a home inventory with photos and receipts.

Additional Living Expenses (ALE)

The third part covers temporary housing costs if your home is not livable after an earthquake. This coverage helps pay for hotels and meals while your home is repaired.

If you need to leave your home for repairs, ALE coverage helps with costs. Most policies offer this coverage for 12 to 24 months with specific limits.

| Coverage Component | Typical Limit | Common Exclusions | Real-World Application |

|---|---|---|---|

| Dwelling | 100% of home value | Detached structures, landscaping | Foundation repairs, wall reconstruction |

| Personal Property | 50% of dwelling coverage | High-value items, business equipment | Furniture, electronics, clothing replacement |

| Additional Living Expenses | 20% of dwelling coverage | Non-essential upgrades, mortgage payments | Hotel stays, temporary rentals, meals |

Knowing these three parts helps you avoid paying too much or too little. Talk to your agent about your specific needs. For example, a home with expensive items might need more personal property coverage.

Remember, earthquake policies don’t cover fire damage. Fire damage is covered by your standard homeowners policy. Flood damage, even from earthquakes, needs separate insurance. The California Department of Insurance has resources to help understand these differences.

Your policy limits affect your premium and protection after an earthquake. Review these limits every year as your home and belongings change.

“read also: What is the purpose of critical illness insurance?“

Deductible structures and claim settlement timelines

When you deal with earthquake insurance, knowing about the special deductibles is key. Unlike regular homeowners insurance, earthquake insurance deductibles are based on a percentage. This percentage is usually between 10% and 20% of your home’s coverage.

This means you’ll have to pay a lot before your insurance starts helping. For example, if your home is insured for $500,000 and you have a 15% deductible, you’ll pay the first $75,000. Then, your insurance will start covering the rest.

Each part of your coverage, like your home, belongings, and detached buildings, might have its own deductible. This means you’ll have to meet the deductible for each part before getting paid for damage.

Earthquake deductibles run 5 – 25 % of the dwelling limit—so a \$500 k home could face \$25 k–\$125 k out-of-pocket before insurance pays. Lower premiums come at the cost of much higher post-quake expenses. Ref.: “California Earthquake Authority. (2025). CEA Homeowners Policy Coverages & Deductibles. California Earthquake Authority.” [!]

“The deductible structure is the most misunderstood aspect of earthquake insurance. Many homeowners are shocked to learn they must cover tens of thousands in damages before their policy pays a dime.”

The California Earthquake Authority (CEA) and private insurers offer different deductible choices. A higher deductible can lower your premiums but means you’ll pay more after an earthquake. You need to think about your finances and how much risk you can handle.

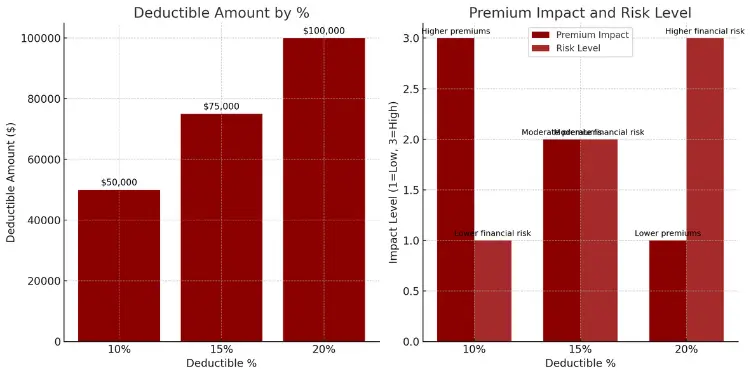

| Deductible % | On $500,000 Dwelling | Premium Impact | Risk Level |

|---|---|---|---|

| 10% | $50,000 | Higher premiums | Lower financial risk |

| 15% | $75,000 | Moderate premiums | Moderate financial risk |

| 20% | $100,000 | Lower premiums | Higher financial risk |

When an earthquake damages your property, the claim process has a timeline. First, call your homeowners insurance right away. They’ll tell you who to contact for earthquake claims. Take photos and videos of the damage before moving anything.

Usually, an adjuster will visit your property within 1-2 weeks. This depends on how big the disaster is. If your home is old, consider getting an independent inspector who knows about earthquakes.

Loss of use coverage in your policy can help with temporary housing costs. This coverage doesn’t have a deductible. It gives you quick help while your claim is being processed.

- Immediate post-earthquake steps: Make sure you’re safe, document the damage, and fix temporary repairs to avoid more damage

- Claim filing: Call your insurer, get a claim number, and understand your coverage limits

- Damage assessment: Talk to the adjuster, and think about getting an independent inspection

- Documentation: Give a list of damaged items with their replacement costs

- Settlement negotiation: Check the offer, and appeal if needed

A joint 2023 USGS–FEMA analysis pegs annual building losses from earthquakes at \$14.7 billion, with recent decades averaging \$1.5 – 3 billion per year—underscoring the scale of unrecovered costs when coverage is lacking. Ref.: “U.S. Geological Survey & Federal Emergency Management Agency. (2023). New USGS-FEMA study highlights economic earthquake risk in the United States. U.S. Geological Survey.” [!]

The insurance industry usually handles earthquake claims in 30-90 days. But, claims for big structural damage might take longer. California law makes sure insurance companies act fast on claims.

Understanding your earthquake insurance, including deductibles and the claim process, is key. Review your policy now to avoid confusion after an earthquake.

“read more: What is the purpose of mobile home insurance?“

Assessing seismic hazard and purchase necessity

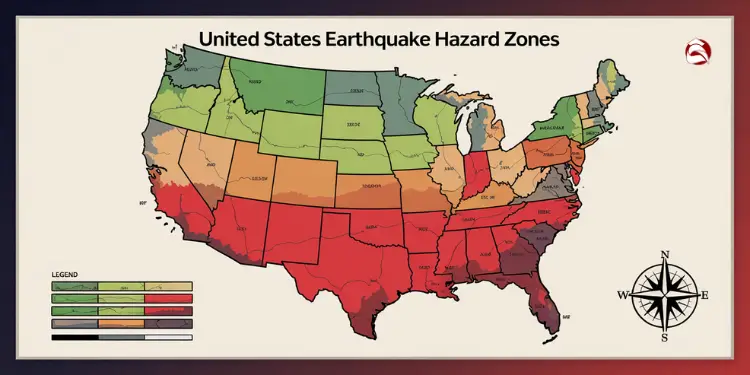

First, check if your home is in a high-risk area for earthquakes. Many people think they’re safe, but earthquakes can happen anywhere. In fact, 42 states have some earthquake risk, with 16 being very high.

Even if you’re not on a fault line, your home can get damaged. Earthquake waves can travel far and hurt buildings. Knowing your risk is key before you decide on earthquake insurance.

Using USGS Maps for Regional Risk

The USGS has maps that show earthquake risk. These maps use colors to show how likely it is to shake the ground. They help you see your risk clearly.

Visit the USGS Earthquake Hazards Program website to see these maps. The national map shows risk areas in different colors. Red and orange mean high risk, while blue and green mean low risk.

“Understanding your local seismic hazard is the first step in making informed decisions about earthquake preparedness and insurance needs. USGS hazard maps provide this critical information in an accessible format for homeowners.”

The highest-risk states are:

- Alaska

- California

- Hawaii

- Idaho

- Kentucky

- Missouri

- Montana

- Oregon

- South Carolina

- Tennessee

- Washington

- Wyoming

But, earthquakes have also hit states not usually seen as risky. Oklahoma, Texas, and Ohio are examples. This shows why you can’t just guess about risk.

Look at the “peak ground acceleration” values on the maps. Values over 0.4g mean severe shaking. This could damage your home a lot.

Mortgage Lender Earthquake Coverage Requirements Overview

Most lenders don’t require earthquake insurance, even in high-risk areas. But, this choice is yours. There are important exceptions to know about.

In California and other high-risk areas, some lenders now require earthquake insurance. This is because more people understand the risk. Check your mortgage documents for any earthquake insurance clauses if you’re buying a home in a high-risk area.

Even if there’s no requirement, lenders want to protect your property. They might suggest earthquake coverage if your home is in a seismic zone. Remember, standard homeowners insurance doesn’t cover earthquake damage. Without specific coverage, you’re fully responsible for these costs.

Consider these factors when deciding if you need earthquake insurance:

| Assessment Factor | Higher Need for Coverage | Lower Need for Coverage | How to Evaluate |

|---|---|---|---|

| Home Equity | High equity (>50%) | Low equity ( | Calculate current home value minus mortgage balance |

| Construction Type | Masonry, brick, concrete | Wood frame with retrofitting | Review building materials and structural design |

| Financial Reserves | Limited savings | Substantial emergency fund | Assess ability to cover 20% of home value |

| Soil Conditions | Liquefaction-prone areas | Solid bedrock | Check local soil maps or geotechnical reports |

| Home Age | Pre-1980 construction | Built after 2000 | Review building date and code compliance |

Ask yourself these questions to decide if you need earthquake insurance:

- Could you afford to rebuild your home without insurance if it were severely damaged?

- Do you have enough savings to cover temporary housing costs while repairs are made?

- Would the loss of your home equity significantly impact your financial future?

- Does your home have features that make it vulnerable to earthquake damage?

- How would you manage financially if your personal property was destroyed?

If you said “no” to the first two questions or “yes” to the last three, you might need earthquake insurance. Even in moderate-risk areas, the risk of big losses is worth the cost. Insurance companies that are members of state programs often offer better deals.

Only about 10% of California residents have earthquake insurance. This low number shows a common mistake: thinking earthquake damage won’t happen or that government help will be enough. But, federal aid usually offers only loans that must be repaid.

Your home insurance policy needs an earthquake endorsement or a separate policy for earthquake protection. Without it, you’re fully responsible for earthquake damage costs.

Comparing CEA and private policy options

Choosing between California Earthquake Authority coverage and private earthquake insurance is big. It affects how well your home is protected and your budget. I’ve helped homeowners for years and seen how this choice matters a lot.

The 1994 Northridge earthquake changed California’s insurance world a lot. Insurance companies stopped selling earthquake coverage because of the risk. This was because of California’s “mandatory offer law” that requires insurance companies to offer earthquake insurance if they sell homeowners insurance.

To fix this, the California legislature made the California Earthquake Authority (CEA). It’s a special group that helps people get earthquake insurance. This group is funded by private money but managed by the public.

“The CEA was born out of necessity. Without this innovative approach, many California homeowners would have found themselves without any option for earthquake protection after Northridge changed everything.”

Understanding CEA vs. Private Market Fundamentals

When you look at your options, knowing the differences is key. The CEA offers standard policies, while private insurers can customize more. This means the CEA is more predictable, but private insurers might fit your needs better.

| Feature | CEA Policies | Private Market Policies | What This Means For You |

|---|---|---|---|

| Availability | Available to all qualifying California homeowners | May have stricter underwriting criteria | CEA might be your only option in high-risk areas |

| Coverage Limits | Standardized with some flexibility | Often more customizable | Private policies may better fit unique properties |

| Deductible Options | 5% to 25% of dwelling coverage | Typically 2.5% to 20% of dwelling coverage | Private markets may offer lower entry points |

| Personal Property Coverage | Limited, with separate deductible | Often more extensive | Consider your belongings’ value when choosing |

In California, any insurance company that sells homeowners insurance must also offer earthquake coverage. This offer must be in writing and clearly explain what’s covered and what’s not. Many homeowners don’t realize they need to make this separate decision.

If private insurers won’t cover you because of your property’s location or type, the CEA is there to help. As a not-for-profit, the CEA focuses on making earthquake insurance available, not on making money.

Evaluating Deductible Percentages Versus Premium Savings

One big difference between earthquake policies and standard home insurance is deductibles. While your typical homeowners policy might have a $1,000 or $2,500 deductible, earthquake insurance uses percentage-based deductibles. These can range from 5% to 25% of your dwelling coverage.

This means your costs could be high if your home is damaged by an earthquake. Let’s look at how different deductible choices affect your premiums and claims:

- Lower deductible (5-10%): Higher premiums but less out-of-pocket expense when you file an insurance claim

- Mid-range deductible (15%): The standard “mini policy” deductible required by California law

- Higher earthquake deductible (20-25%): Significantly reduced premiums but requires substantial personal resources if a major event occurs

For example, if your home is worth $500,000, a 15% deductible means you pay the first $75,000 in damages before your coverage starts. Choosing a 25% deductible might save you 20-30% on premiums but means you could have to pay up to $125,000 out-of-pocket.

When deciding, think about what you can afford to pay in a worst-case scenario. Your emergency fund should guide your deductible choice.

Remember, damage from an earthquake isn’t covered by your standard homeowners policy. This makes your choice very important. The CEA’s “mini policy” covers only structural damage with that 15% deductible. Claims for personal property losses and “loss of use” face big limits.

Private insurers might offer more flexible policies with lower deductibles but at higher premiums. Some private policies also offer discounts on your primary homeowners insurance if you buy earthquake coverage.

For condominium owners and renters, the situation is different. The CEA offers special policies for personal property coverage and loss of use. These might be more affordable than full homeowner policies.

Insurance can help you get back on your feet after an earthquake, but only if the policy fits your needs and budget. Finding the right balance between premium costs and deductible levels depends on your property’s value, location, and your financial situation.

Read More:

Premium determinants and mitigation discount programs

When you buy earthquake insurance, many things affect your costs. The age and where your home is matter a lot. Homes near active fault lines cost more.

The California Earthquake Authority looks at your home’s type, stories, and foundation. This helps figure out your premium.

Completing a code-compliant seismic retrofit on an older home can earn up to a 25 % premium discount while sharply reducing structural damage risk—a dual win for safety and savings. Ref.: “California Earthquake Authority. (2025). Premium discount for older houses that have been retrofitted. California Earthquake Authority.” [!]

Smart homeowners can lower their insurance by making their homes safer. The CEA policy gives a 21% discount for mobile homes with special bracing. Standard homes can get discounts if they meet certain building codes.

Mobile homes need special bracing to be safe. Standard homes must have strong walls and foundation support. Even small steps, like securing your water heater, can help.

Getting your home fully braced can cost a lot. But, there’s a $3,000 program to help with the cost. Your insurance agent can tell you how this helps your insurance.

Investing in retrofitting is smart for most people with earthquake insurance. It lowers your premiums and protects your home from earthquakes. Talk to your insurance about the best ways to save money and keep your home safe.

{kind=link}