Dental insurance does more than just fix teeth. It helps families get regular dental care without breaking the bank. Have you ever considered why dental plans prioritize checkups over major dental work?

Delta Dental reports that 85% of Americans believe oral health is crucial to overall well-being. But only 78% have dental insurance. Regular visits can catch problems early, saving money and pain.

Dr. Michael Cohen, president of the Academy of General Dentistry, says, “Prevention costs pennies, while restoration costs dollars.” This advice has helped my clients in Idaho Falls for over 10 years.

I’ve seen how families with insurance avoid big dental bills. Most plans pay for preventive care fully. This means less money out of pocket for important dental work.

Quick hits:

- Preventive visits usually get full coverage

- Spotting problems early saves a lot of money

- Insurance makes going to the dentist a habit

- It also makes dental treatments cheaper

- Good oral health is linked to feeling well overall

What Dental Insurance Truly Covers

Dental insurance has a tiered system. It focuses on some treatments more than others. Services are grouped into three levels: preventive, basic, and major.

Preventive care gets the best coverage. Most plans cover 100% of routine cleanings and exams. They also cover basic x-rays.

Basic dental services get 70-80% coverage after you meet your deductible. These include:

- Fillings for cavities

- Simple extractions

- Non-surgical periodontal treatment

- Emergency pain relief

Major dental treatments get 50% coverage. Families often face high costs for these services. Major procedures include crowns and dentures.

| Service Category | Typical Coverage | Examples | Waiting Period |

|---|---|---|---|

| Preventive | 100% | Cleanings, exams, x-rays | None |

| Basic | 70-80% | Fillings, extractions | 3-6 months |

| Major | 50% | Crowns, bridges, dentures | 6-12 months |

Dental insurance has an annual cap. Most plans stop paying after $1,000-$1,500. After that, you pay all costs yourself.

Most dental PPO plans limit annual benefits to $1,000–$2,000; once that ceiling is met, the plan pays nothing further, so patients must budget or stage major work across calendar years. Ref.: “Shinn, L. (2024). What Does Dental Insurance Cover? Investopedia.” [!]

Dental insurance isn’t designed to cover everything—it’s structured to fully cover preventive care while providing partial assistance for more extensive treatments.

Some dental treatments aren’t covered. Cosmetic services like whitening and veneers get no help. Some plans offer orthodontic benefits, but with limits.

Waiting periods are another limit. Preventive services are available immediately, but basic and major services have waiting times of 3-12 months.

Knowing what dental insurance covers helps set realistic expectations. It’s best for preventive care and some unexpected needs. But it doesn’t cover all dental work.

Preventive Care Benefits and Savings

Dental insurance is more about keeping your teeth healthy than fixing problems. After looking at hundreds of policies, I see that preventive care is key. It shows the real value of dental plans.

Preventive care includes cleanings, x-rays, exams, fluoride, and sealants for kids. These steps help avoid big dental problems that cost a lot.

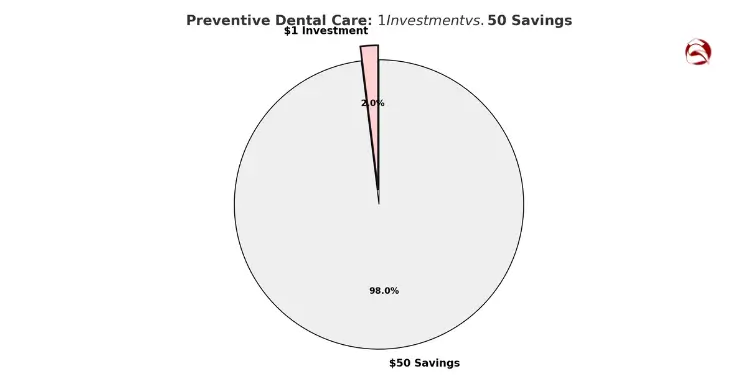

Preventive care saves a lot of money. For every dollar spent, you save about $50 later. This makes preventive care a smart choice for families.

Insurance companies know this. That’s why they cover preventive care fully. This means you can get regular checkups without worrying about the cost.

Families with dental insurance get more preventive care. This leads to better health and fewer expensive emergencies.

Routine Cleanings, Fluoride and Exams

Cleanings and exams are the base of preventive care. Most plans cover these twice a year. These visits help find problems early.

Your dentist can find issues like cavities or gum disease early. Kids get fluoride and sealants to protect their teeth. These services help prevent problems.

Most plans cover these services right away. This is different from major procedures that have waiting periods.

| Preventive Service | Typical Coverage | Average Cost Without Insurance | Your Cost With Insurance | Annual Savings |

|---|---|---|---|---|

| Routine Cleaning | 100% (2x yearly) | $75-$200 per visit | $0 | $150-$400 |

| Comprehensive Exam | 100% (2x yearly) | $100-$300 per exam | $0 | $200-$600 |

| Bitewing X-rays | 100% (1x yearly) | $60-$150 | $0 | $60-$150 |

| Fluoride Treatment | 100% for children | $20-$50 | $0 | $20-$50 |

| Dental Sealants | 80-100% for children | $30-$60 per tooth | $0-$12 per tooth | $120-$240 (4 molars) |

Book your cleanings in January and July for the best savings. This schedule helps you use your benefits fully.

Some people get reminders for covered services. This way, they never miss out on the care they’ve already paid for.

For kids, the savings are even bigger. They need more care, and plans cover extra services like fluoride and sealants. These can save parents a lot of money.

Preventive care is the main benefit of dental insurance. It helps keep your teeth healthy and saves you money. By using these benefits, you make your insurance a valuable tool for your budget and smile.

Deciding If Dental Plans Are Necessary

Figuring out if dental plans are worth it means looking at costs. You need to compare what you pay out of pocket to what you pay for the plan. Your family’s health history, size, and dental needs are key to deciding.

Out of Pocket Cost Comparisons

Without dental insurance, you pay for all dental care yourself. This can add up fast, even for big families.

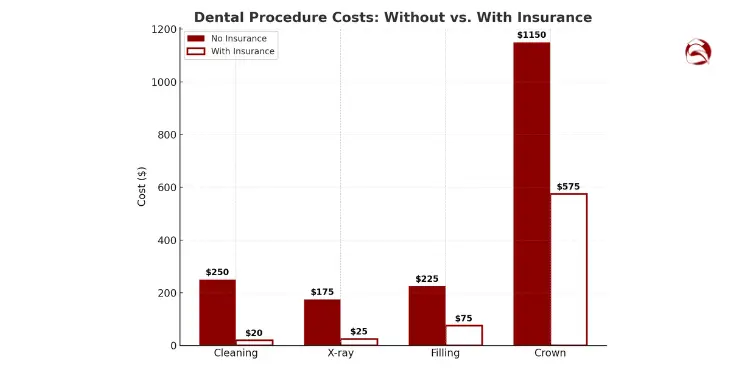

| Common Procedure | Average Cost Without Insurance | Typical Cost With Insurance | Annual Savings |

|---|---|---|---|

| Routine Cleaning (2x yearly) | $200-300 | $0-40 | $160-300 |

| X-rays | $100-250 | $0-50 | $50-250 |

| Filling (single) | $150-300 | $50-100 | $100-200 |

| Crown | $800-1,500 | $400-750 | $400-750 |

For a family of four, dental care without insurance could cost over $2,000 a year. With insurance, it might be less than $800, including premiums.

WebMD places the average cost of traditional metal braces between $3,000 and $7,000 before insurance—underscoring the need to verify lifetime orthodontic maximums when choosing a plan. Ref.: “WebMD Editorial Team. (2025). Lingual Braces: What Are the Advantages and Disadvantages? WebMD.” [!]

If your premiums and out-of-pocket costs are less than without insurance, it’s worth it. Families with good oral health and few dental needs might save money by not getting insurance.

Coverage Gaps in Health Insurance

Many people find out their medical insurance doesn’t cover dental care. Dental and medical insurance have been separate for decades.

Your medical plan won’t cover:

- Routine dental cleanings and exams

- Fillings, crowns, or root canals

- Dentures or bridges

- Most orthodontic work

- Cosmetic dental procedures

But, some medical plans might cover emergency dental care from accidents. They might also cover some oral surgery if it’s medically necessary.

This gap in coverage can leave you vulnerable. Untreated dental problems can lead to bigger health issues that cost more money and affect your health.

Gain insights into the Purpose of Professional Liability Insurance Protecting Expertise from Costly Mistakes and how it shields professionals from potential legal claims.

Orthodontic Needs for Growing Families

Families with kids should look closely at orthodontic benefits in dental plans. Braces or aligners can cost $3,000-7,000 without insurance.

Most dental plans don’t cover much for orthodontics. When they do, there are often limits:

- Lifetime maximums (usually $1,000-2,000 per person)

- Age limits (often for kids under 19)

- Waiting periods (12-24 months before benefits start)

- Coverage percentages (usually 50%, not 100% like for preventive care)

Choosing a plan with good orthodontic coverage can save thousands per child. For families needing braces for multiple kids, the savings can be huge, even with higher premiums.

“The best dental insurance plans for families needing orthodontic work are those that balance higher orthodontic lifetime maximums against reasonable premium increases.”

Deciding on dental insurance depends on your risk tolerance and finances. Some families might choose to self-insure, while others prefer the peace of mind and savings from dental plans.

Consider these when deciding:

- Your family’s dental history and genetic risks

- The number of family members needing coverage

- Your ability to handle unexpected dental costs

- The quality and cost of dental care in your area

- If you think you’ll need major dental work soon

Dental insurance does more than save money. It encourages regular care to avoid expensive problems later.

Read about the Purpose of Commercial Property Insurance Safeguarding Assets from Catastrophic Losses to understand how to protect your business assets effectively.

Premium Structures Waiting Periods and Limits

Dental insurance has three key parts: premiums, waiting periods, and limits. These parts affect how much you pay and what’s covered.

When you sign up for dental insurance, you pay a monthly fee. This fee changes based on where you live, how big your family is, and the coverage you choose.

A family of four in the Midwest might pay $120-180 monthly for good coverage. But an individual in a coastal city could pay $35-50 for basic coverage. Many families don’t think about how these factors add up to their final cost.

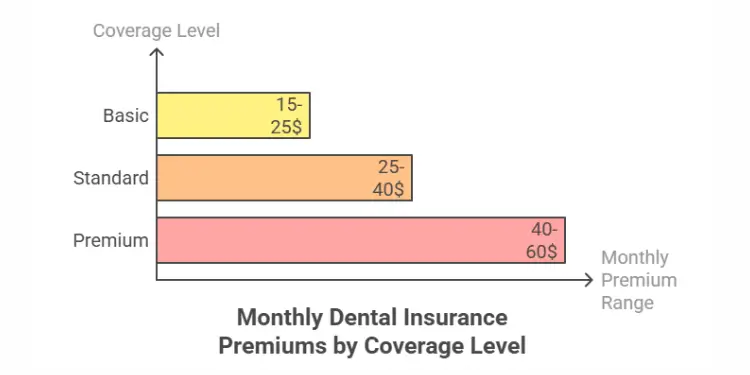

| Coverage Level | Typical Monthly Premium (Individual) | What It Typically Covers | Best For |

|---|---|---|---|

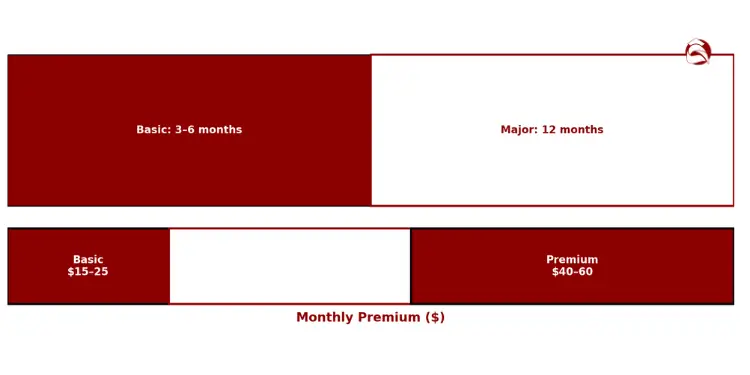

| Basic | $15-25 | Preventive care, some basic procedures | Young adults, minimal dental needs |

| Standard | $25-40 | Preventive plus most basic procedures | Most adults with average dental needs |

| Premium | $40-60 | Comprehensive coverage including major work | Families, seniors, ongoing dental issues |

Dental plans have waiting periods before covering some services. These periods, usually 3-6 months for basic and 12 months for major work, stop people from buying insurance just before expensive treatments. This keeps premiums from rising too high.

NADP confirms the prevailing “100-80-50” model—100% for preventive, 80% for basic, 50% for major procedures—making full use of no-cost cleanings the smartest savings move. Ref.: “National Association of Dental Plans. (2025). Dental Benefits Q&A. NADP.” [!]

To deal with waiting periods, try these tips:

- Sign up during open enrollment to skip waiting periods

- Find plans that count past coverage toward waiting periods

- Enroll a few months before you need major dental work

Dental insurance has its own financial rules, unlike medical insurance. After your dental deductible, you enter the coinsurance phase. Here, insurance pays a part of costs, and you pay the rest.

Most plans use a “100-80-50” structure. This means insurance covers 100% of preventive care, 80% of basic procedures, and 50% of major work. You pay 20% for basic and 50% for major procedures.

The annual maximum benefit is the highest amount your dental insurance will pay in a year, usually between $1,000 and $2,000. Once this limit is reached, you pay 100% of costs until the next year.

This limit can affect families needing a lot of dental work. For example, if your plan’s annual maximum is $1,500 and you need a $3,000 treatment, insurance covers only the first $1,500 (minus any deductible and coinsurance).

Understanding these financial parts helps you see the real value of dental plans. A plan with a low premium but high deductible and limited annual maximum might cost more than a higher-premium plan with better coverage.

When comparing plans, look at more than just the monthly premium. Think about the total costs for your family’s dental needs. This way, you choose coverage that really protects your finances, not just seems to.

Choosing a Dental Insurance Provider

Choosing the right dental insurance is key to protecting your smile. It’s about finding the right balance of coverage, network, and cost. I’ve helped many families make these choices, and I know how important it is to understand your options.

There are three main ways to get dental coverage. Employer plans are often cheaper and easy to pay for through payroll. Individual plans offer more freedom for those who work for themselves. Delta Dental and other companies sell direct-purchase plans that fit your area.

The type of network matters a lot. Dental HMOs are cheaper but limit you to in-network dentists. PPO plans cost more but let you see any dentist, though you pay more out of pocket.

Before picking a plan, check if your dentist is in the network. I’ve seen families find out too late that their dentist isn’t in their new plan.

Understand the Purpose of Business Owners Policy Combining Property and Liability Protections to see how bundled policies can offer comprehensive business coverage.

Essential Questions When Comparing Plans

Here’s a checklist for comparing dental insurance plans:

- Coverage percentages: What percentage does the plan pay for different procedures?

- Annual maximum: How much does the plan pay out each year? Most plans cap at $1,000-$2,000.

- Waiting periods: Do you have to wait 6-12 months for certain procedures?

- Network size: How many dentists are in your area?

- Exclusions: Are certain treatments or pre-existing conditions not covered?

The fine print is very important with dental benefits. Read plan documents carefully. Look for limits on how often you can get certain treatments.

| Plan Type | Best For | Typical Premium | Key Advantage |

|---|---|---|---|

| DHMO | Budget-conscious individuals | $15-25/month | Predictable costs, no annual maximum |

| PPO | Those with established dentists | $30-50/month | Provider flexibility, better coverage |

| Discount Plan | Immediate needs, seniors | $8-15/month | No waiting periods, simple structure |

Dental discount plans are another option. They offer discounts at participating dentists without annual limits or waiting periods. They’re great for seniors or those needing quick dental care.

The best dental insurance depends on your needs. Families with kids need plans that cover a lot of preventive care. Adults with dental history need plans with high annual maximums.

Seniors should look at plans that cover implants and dentures. Many plans don’t cover these, but some senior plans do, often for more money.

“The true value of a dental plan isn’t in its premium but in how well it matches your specific oral health needs and usage patterns.”

When looking at costs, compare the annual premium to the plan’s maximum benefit. If you pay $600 a year for a $1,000 maximum, you need to use at least $600 in benefits to break even.

Dental insurance providers vary by region. Delta Dental and others offer plans nationwide, but details and prices differ by state. Always check plan specifics for your area.

Actionable Tips for Maximizing Dental Benefits

Knowing your dental insurance is more than just what’s covered. Families can save a lot by using their insurance wisely. It’s not just for emergencies, but also for regular care to save money in the long run.

Dental insurance benefits are for a year, and they expire on December 31st. Plan big procedures to use up your benefits in two years. For example, start a crown in December and finish it in January.

Explore the

- Purpose of Gap Insurance Explained for Drivers with Loan Balances

- Why Get Umbrella Insurance for Expanded Personal Liability Protection Needs

- Essential Purpose of Wedding Insurance for Protecting Your Perfect Celebration

Using Networks and Pre-Authorization Smartly

Choosing in-network dentists can save you a lot of money. They have agreed to lower rates for your benefit. Always ask for pre-authorization before big procedures to know what you’ll pay.

Keep track of your dental benefits all year. Many insurance companies have online tools to help. If you have more than one insurance, pick one as the main one for each family member.

Preventive care like cleanings is usually 100% covered. But basic and major services have different coverage. Knowing this and talking to your dentist and insurance can help avoid unexpected costs. It also keeps your teeth healthy.

{kind=link}