Cyber insurance helps small businesses avoid huge financial losses from digital attacks. It’s a special insurance that pays for the costs of cyber attacks. This way, small businesses don’t have to worry about the high costs.

But, what if hackers don’t see small businesses as a threat? The FBI got 847,376 cybercrime complaints in 2021. These cost Americans $6.9 billion. “Small businesses are the soft underbelly of the digital economy,” says cybersecurity expert Brian Krebs.

I’ve seen three shops in Idaho Falls close because of ransomware attacks. None of them had cybersecurity insurance.

Cyber insurance for small businesses provides coverage for direct costs arising from data breaches and cyber incidents. It includes expenses for breach notification, credit monitoring, forensic investigation, legal consultation, system restoration, and business interruption losses. Policies mandate baseline security controls and enable rapid incident response to limit financial impact and maintain operational continuity.

Coverage also addresses ransomware payments, third-party liability, reputational management, and regulatory fines. Underwriting assesses security posture and incentivizes ongoing risk management. Integration with backup systems and incident response processes optimizes recovery timelines and mitigates premium volatility. Cyber insurance complements but does not replace core cybersecurity measures.

Quick hits:

- Cyber liability insurance covers breach costs

- Insurance coverage includes ransomware payments

- Purpose cyber protection: financial survival

- Cyber threats cost millions without coverage

Coverage for data breach expenses

When cyber attacks happen, money problems come fast. A cyber insurance policy helps with the quick costs after data breaches. It keeps businesses going while they deal with the crisis.

The purpose cyber insurance is clear when you have to tell people about a breach. Laws say you must tell customers quickly. If you don’t, you face fines. Insurance helps with sending out notices, setting up call centers, and updating websites.

Notification costs and credit monitoring

Cyber insurance helps protect people whose data was stolen. Most insurance policies include credit monitoring. This service watches for bad stuff on credit reports for 12-24 months.

A good cyber insurance policy covers many things:

- Legal advice to follow privacy laws

- Forensic investigation to find out how big the breach is

- Help to fix identity problems for customers

- Support to keep your reputation good

- Money for fixing data and systems

Looking at real cases, we see why this coverage is key. After Equifax’s breach, they gave free help to fix credit. Without cyber security and insurance, small companies could go under.

Smart businesses know cyber risk is always there. Having the right cyber insurance coverage means you can act fast. This limits damage and keeps customers’ trust.

Read More:

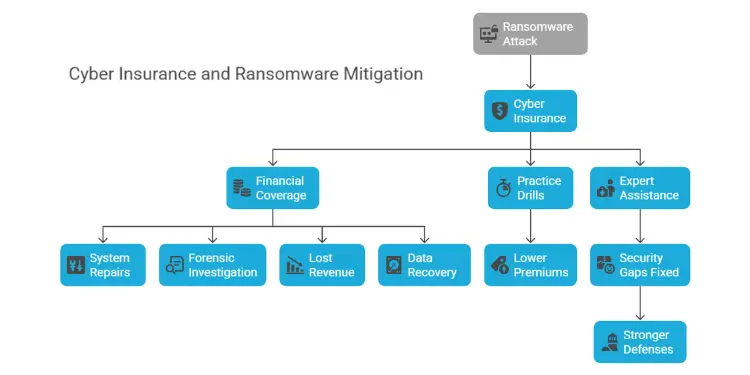

Mitigation of ransomware attack losses

Ransomware attacks lock your business files until you pay criminals to unlock them. Cyber insurance is a type of insurance that steps in when these digital kidnappers strike. This insurance product helps pay the ransom so you can get back your systems.

Cyber risk insurance also covers other damage from attacks. The costs associated with cyber incidents include:

- System repairs and hardware replacement

- Forensic investigation fees

- Lost revenue during downtime

- Data recovery expenses

Smart businesses do practice drills before disaster hits. They run ransomware simulations to show insurers they’re serious about security. This can lead to lower premiums because they don’t have to file as many claims.

In the event of a cyberattack, your policy kicks in right away. Cyber insurance provides coverage for experts who figure out how hackers got in. These experts help fix security gaps to prevent future attacks.

Remember, insurance is a type of financial protection, not a substitute for strong security. Combining this type of insurance with good backup systems is your best defense. If a cyber incident happens, you’ll have the money and data to recover fast.

Every cyber attack teaches us something new. Your insurance covers the immediate crisis and helps build stronger defenses for the future.

“Dive Deeper: What is the purpose of business owners policy?“

Third party liability and reputational harm

When customer data gets stolen, businesses face big problems. Cyber liability insurance coverage helps protect them. It covers legal costs, settlements, and damages from third parties.

Regular business policies don’t cover cyber attacks. General and professional liability plans don’t help with lawsuits over stolen credit card info. That’s why cyber liability insurance is key for any business with sensitive data.

This insurance also helps with reputation:

- Public relations specialists write breach notifications

- Crisis communication teams handle media

- Customer outreach programs help rebuild trust

- Credit monitoring services for those affected

The costs of data breaches are rising. Healthcare breaches cost $10.93 million on average, IBM’s 2023 report says. Retail breaches cost about $3.28 million, and financial services breaches cost $5.97 million.

Insurance shows you care about data protection. It’s often a must-have for contracts. It shows you’re serious about keeping data safe.

Insurance also covers costs for following laws. Laws like California’s CCPA can lead to big fines. Your insurance pays for legal help and penalties.

“Read Also: What is the purpose of general liability insurance?“

Business interruption coverage and recovery

Cyber attacks hurt businesses more than just data loss. They stop money from coming in and systems freeze. Cyber insurance helps businesses stay afloat during these tough times. It protects your money flow when you can’t work.

Loss of income during downtime

System outages cost money fast. E-commerce sites lose sales when customers can’t shop. Banks get stuck with too many transactions, upsetting customers.

This insurance helps cover lost money during these times.

Coverage includes:

- Daily revenue averages from the past year

- Fixed costs that keep going even when you’re not working

- Wages for employees who can’t work

- Money for customer refunds or compensation

Extra expense reimbursement coverage options

Recovering from attacks costs more than usual. You might need to hire experts, rent equipment, or find new places to work. Your policy can help pay for these unexpected costs.

Insurance covers important recovery costs like:

- Forensic investigation services

- Experts to fix your systems

- Extra pay for tech staff working overtime

- Fast shipping for new equipment

- Costs to tell everyone what’s happening

This coverage lets you focus on getting back to work. Talk to your agent about what’s covered and how to get help before a problem happens.

“For More Information: What is the purpose of an insurance policy?“

Compliance with evolving data regulations

Data laws change fast and breaking them costs a lot. A cyber insurance policy helps when your small business gets fined for privacy issues. It covers legal fees and penalties after a breach, no matter the data type.

Privacy laws and regulatory fines

Every state has its own data breach rules. Missing these deadlines can lead to big fines. Cyber insurance helps businesses pay these fines and deal with legal stuff. Your cyber insurance coverage includes experts for contacting the right agencies.

For Beginner business owners, following laws can feel hard. Insurance policies require basic cyber security steps. Ignore these, and your claim might get denied when you need it most. Regular checks keep your coverage good.

| Industry | Common Violations | Average Fine | What Insurance Covers |

|---|---|---|---|

| Healthcare | Late breach notice | $50,000 | Legal fees, fines |

| Retail | Poor data encryption | $35,000 | Defense costs, penalties |

| Education | Improper record disposal | $25,000 | Investigation, fines |

Insurance helps keep up with changing laws across states. Your policy changes with new laws, keeping up with tighter rules. Schools, clinics, and shops all face different risks. Cyber insurance helps manage these without a full-time legal team.

“Further Reading: What is the purpose of mobile home insurance?“

Risk management and cybersecurity posture

Cyber insurance is a way to protect your business. It works with your current security steps. When you apply, insurers check your security through audits or ask for NIST Cybersecurity Framework papers.

Companies like Chubb and AIG use these checks to decide what insurance to offer. They also figure out how much to charge. Businesses with weak security pay more because they face more cyber risk.

Cyber insurance helps with many costs from cyber attacks. But it won’t fix basic security issues. Your insurance won’t cover problems caused by ignoring known vulnerabilities or by an employee on purpose.

State Farm and Travelers won’t pay for improving your tech after an attack. The coverage also doesn’t help with breaches before you bought the policy.

Smart businesses see insurance as part of their defense. Training your team is key, as one in four workers can’t spot phishing. Companies that check their risk regularly and match it with the right insurance get better protection.

Insurance supports your security work but doesn’t replace strong passwords or updated software. It also doesn’t replace careful data handling.

{kind=link}