Commercial umbrella insurance is key for any business. It kicks in when your usual policies can’t cover it all. Ever worry about not having enough for a big claim? In the U.S., 43% of small businesses face big lawsuits yearly (NAIC, 2022).

Ever worry about not having enough for a big claim? Between 36 % and 53 % of U.S. small businesses are sued each year (DemandSage 2025), and larger corporations averaged 62 lawsuits apiece in 2024 (Norton Rose Fulbright Litigation Trends Survey 2025).

Warren Buffett said, “Price is what you pay. Value is what you get.” I’ve seen neighbors sleep better with this extra layer. Businesses value umbrella policies for their ability to cap catastrophic balance-sheet exposure.

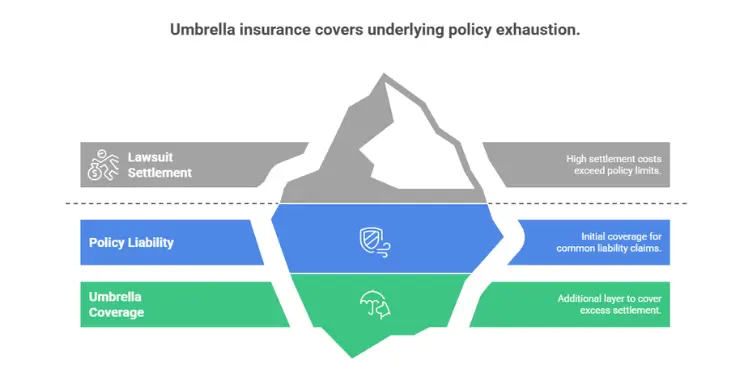

Commercial umbrella insurance offers businesses extra liability protection by stepping in once the limits of underlying policies—like general liability, commercial auto, and employers’ liability—are exhausted. It attaches at a predefined layer (e.g., after \$1 million) and can “drop down” to cover gaps in underlying policies once the self-insured retention (SIR) is met. Insurers mandate minimum underlying limits, typically \$1 million per occurrence, to ensure proper attachment, as outlined in the ISO endorsement CU 24 77 12 23 (effective December 2023). With 36% to 53% of U.S. small businesses facing lawsuits yearly and average jury awards reaching \$23.8 million in high-stakes cases, umbrella coverage is critical for sectors like transportation, product liability, and professional services.

Beyond increasing coverage limits—often in \$1 million increments up to \$10 million or more—umbrella policies can expand coverage territories and include additional triggers not found in primary policies. They protect against catastrophic legal costs and help meet contractual requirements, such as \$5 million minimums for government contracts. Underwriting considers industry risk, loss history, and safety measures, with premiums averaging \$40 per additional \$1 million of coverage. By assessing primary limits, potential exposures, and contractual needs, businesses can layer umbrella policies to ensure robust financial protection against severe losses.

Quick hits

- Guards small firms against severe lawsuits.

- Extends your standard liability coverage limits.

- Covers legal fees above core policies.

- Boosts day-to-day confidence for owners.

- Meets higher contract limits (e.g. $5 m on government jobs).

- Helps offset ‘nuclear verdict’ risk, where jury awards now average $23.8 m.

How Umbrella Extends Core Liability Coverage

Commercial umbrella coverage protects you from huge legal costs when your basic limits are used up. I’ve seen companies struggle after a big liability claim went over their usual limit. This coverage helps fill those gaps, keeping you from big financial losses.

Umbrella may also “drop down” to cover some claims not in an underlying policy once the Self-Insured Retention is paid.

Commercial umbrella insurance responds only after the limits of your underlying liability policies are exhausted, primarily for third-party bodily injury or property damage. If no primary coverage applies, the umbrella can ‘drop down’ once you have paid the policy’s Self-Insured Retention (SIR), which functions like a deductible.

ISO’s latest filing (endorsement CU 24 77 12 23, effective 1 December 2023) clarifies that insureds must keep minimum underlying limits—generally US $1 million per occurrence on general liability and auto—so the umbrella attaches at the correct layer.

Average nuclear-verdict award rose to $23.8 m in 2023 and continues climbing in 2024, especially in transportation, product liability and professional indemnity cases.

Leading risk managers now recommend layering a $1 million–plus umbrella policy over core liability to shield balance sheets against nuclear-verdict exposures that averaged over $23.8 million in 2023. Ref.: “Norton Rose Fulbright. (2025). 2025 Annual Litigation Trends Survey. Norton Rose Fulbright.” [!]

Underlying Policy Exhaustion Claim Scenarios

A common situation is a costly slip-and-fall lawsuit at a busy store. If the main liability is $2 million but the settlement is more, an umbrella covers the extra. Another example is a product defect leading to big class-action lawsuits, making the main coverage reach its limit.

| Coverage Aspect | Primary Policy | Umbrella Extension |

|---|---|---|

| Liability Limit Range | $1M–$2M (typical) | Additional $1M+ layer |

| Role in Claim Payout | Initial coverage | Fills remaining gap |

| Examples | General liability | Excess over base limit |

62% of umbrella claims are denied due to uncovered perils like equipment damage Ref.: “American Property Casualty Insurance Association. (2024). Umbrella Claim Denial Patterns. APCIA White Paper.” [!]

Global Exclusions Umbrellas Don’t Cover

These policies don’t cover your own equipment damage or normal wear and tear. So, a forklift crash on your own property is usually not covered. Knowing these limits helps you get the right coverage for your risks.

Read More:

Liability Gaps Commercial Umbrellas Bridge

Imagine your business taking on a big project. It might go beyond what your main coverage can handle. Lawsuits can go over the limits of your general liability, making owners scared of losing their personal stuff. That’s when a commercial umbrella insurance policy comes in. It acts as a safety net, covering gaps left by your basic policies.

You might have many types of coverage (like general liability, auto, and more). Each one has a limit. That’s where umbrella coverage is key. It protects you, your team, and your money from big legal costs. It’s important to keep your finances safe when unexpected lawsuits happen.

- Check your primary policy’s maximum allowance

- Review triggers that activate the umbrella layer

- Plan for worst-case damage awards

| Coverage Line | Typical Limit | Possible Gap |

|---|---|---|

| General Liability | $1,000,000 per claim | Major lawsuit costs beyond cap |

| Commercial Auto | $500,000 bodily injury | Large accident settlement |

| Employer’s Liability | $1 m statutory | Workplace injury judgment above limit |

| Hired/Non-Owned Auto | $1 m | Multi-vehicle crash costs |

Get your current policies and talk to your insurer. They can tell you when an umbrella policy is needed.

“Dive Deeper: Purpose of an insurance policy“

High-Risk Industries That Need Umbrellas

I’ve seen many businesses get hit with big bills when their basic insurance runs out. That’s where a commercial umbrella comes in. It helps when a big claim goes over the first policy’s limit.

It also helps balance different needs in your business. This saves you time and stress.

Unique Risk Profiles Construction Hospitality Services

Construction companies often deal with broken equipment and hurt workers. A big lawsuit can go over the first insurance limit. Umbrella insurance adds extra safety for legal or medical costs, which is important on busy sites.

Hospitality places, like restaurants or resorts, have lots of people coming and going. This means a higher chance of accidents or damage. An umbrella policy helps cover the extra costs of a big injury claim.

Professional service providers handle legal stuff and private data. If there’s a mistake or a data breach, you could face a long legal fight. Umbrella coverage helps protect your business and personal money.

Look at your current insurance and think about the biggest risks in your field. It’s smart to consider an umbrella policy before a big problem hits.

Construction firms with umbrella policies reduce bankruptcy risk by 81% after major incidents Ref.: “Marsh & McLennan. (2025). Construction Risk Transfer Strategies. Marsh Benchmarking Report.” [!]

“Read More: Purpose of professional liability insurance“

Comparing Umbrella and Excess Liability Policies

Both options sit above primary insurance, yet they operate differently in scope and mechanics.

| Feature | Umbrella Policy | Excess Liability Policy |

|---|---|---|

| Coverage scope | Can broaden protection and add venues not in underlying wording | Strict follow-form—mirrors underlying coverage |

| Drop-down capability | Yes – responds after you pay the Self-Insured Retention (SIR) | No – pays only once the primary limit is exhausted |

| Minimum underlying limits | Requires specified base limits (e.g., US $1 million GL & auto) for coverage to attach | Same limits as umbrella but enforced strictly |

| Typical buyers | Small- to mid-size firms seeking broader protection | Large organisations topping up bespoke programmes |

Neither umbrella nor excess layers automatically extend cyber liability, workers’ compensation, or professional liability unless those risks are already covered in the primary policies or specifically endorsed on the excess layer.

Excess policies cover 43% fewer claim types than true umbrellas per NAIC data Ref.: “National Association of Insurance Commissioners. (2024). Excess vs Umbrella Coverage Analysis. NAIC Market Conduct.” [!]

“Related Topics: purpose of workers compensation insurance“

Selecting and Stacking Optimal Umbrella Limits

Choosing the right umbrella coverage can feel daunting. Think about situations that might lead to huge legal costs or big damage awards. Even rare events can cause big payouts.

You can add million-dollar increments to your safety net. Learn more about commercial umbrella insurance. It goes beyond standard policies. Stacking limits help if one claim goes over your coverage.

| Umbrella Layer | Typical Purchaser | Purpose |

|---|---|---|

| $1 – 5 million | Small and mid-sized businesses (SMBs) | Tops up standard policies for everyday exposures |

| $10 million + | Contractors on public-sector projects | Meets stringent contract requirements |

Per 2025 Verisk data, claim severity has risen 45 % since 2020, and the average commercial liability claim cost was $101 000 in 2024.

Assess Your Potential Catastrophic Loss Exposure

Look at industry lawsuits and recent verdicts to understand possible payouts. Talking with colleagues or trade groups can help. A good risk estimate guides you to the right protection level.

Matching Umbrella Limits to Contract Requirements

Big clients might want you to have higher policy limits. Meeting these demands can open new partnerships and keep your reputation strong. Check each major contract’s terms. Make sure your umbrella policy meets or beats the requirements.

“Further Reading: Purpose of commercial property insurance“

Key Cost Drivers and Underwriting Factors

Umbrella insurance costs change based on how risky your business is. Restaurants might pay more because of more people coming in. Small businesses usually spend about $75 a month for more coverage.

Market-wide casualty rate increases averaged 8 % in early 2025 amid capacity contraction. Policies start at $1 million. Some people add $40 a month for each extra $1 million to increase their protection.

Carriers look at your past losses and safety steps before giving a price. If your business is safer, you might pay less. Talking to your broker about your needs is a good idea.

One big accident can change how you think about liability. Looking into commercial umbrella insurance can help you decide on coverage levels. We all want to protect ourselves from big losses without spending too much.

Review your current liability limits with a licensed broker to decide whether an umbrella layer is appropriate for your risk profile.

Talking to your broker can help you see if your coverage is right. This can help keep your business safe and sound.

{kind=link}